Navigating the complexities of the tax system is a fundamental pillar of personal finance management. Whether you are a salaried employee, a burgeoning freelancer, or a seasoned small business owner, understanding the mechanics of how to pay your taxes is as critical as earning the income itself. Tax season often brings a sense of trepidation, but with a structured approach to financial planning and a clear understanding of the available payment corridors, you can transform a stressful annual obligation into a streamlined component of your wealth management strategy.

In this guide, we will explore the various methodologies for settling your tax liabilities, the strategic financial habits that make the process seamless, and the professional tools available to ensure you remain in good standing with the authorities while optimizing your cash flow.

1. Understanding Your Tax Obligations: The Foundation of Financial Health

Before diving into the “how” of payment, one must master the “what” and “why.” In the realm of personal finance, tax liability is not a static number; it is a dynamic figure influenced by your lifestyle choices, investment strategies, and filing status.

Identifying Your Tax Bracket and Liability

The first step in paying your taxes is determining how much you actually owe. The progressive tax system means that as your income increases, so does the percentage of tax you pay on marginal dollars. For a savvy financial planner, knowing your effective tax rate—the actual percentage of your total income that goes to the government—is more important than knowing your top tax bracket. By calculating this early in the fiscal year, you can avoid the “sticker shock” that often occurs in April.

The Importance of Accurate Record-Keeping

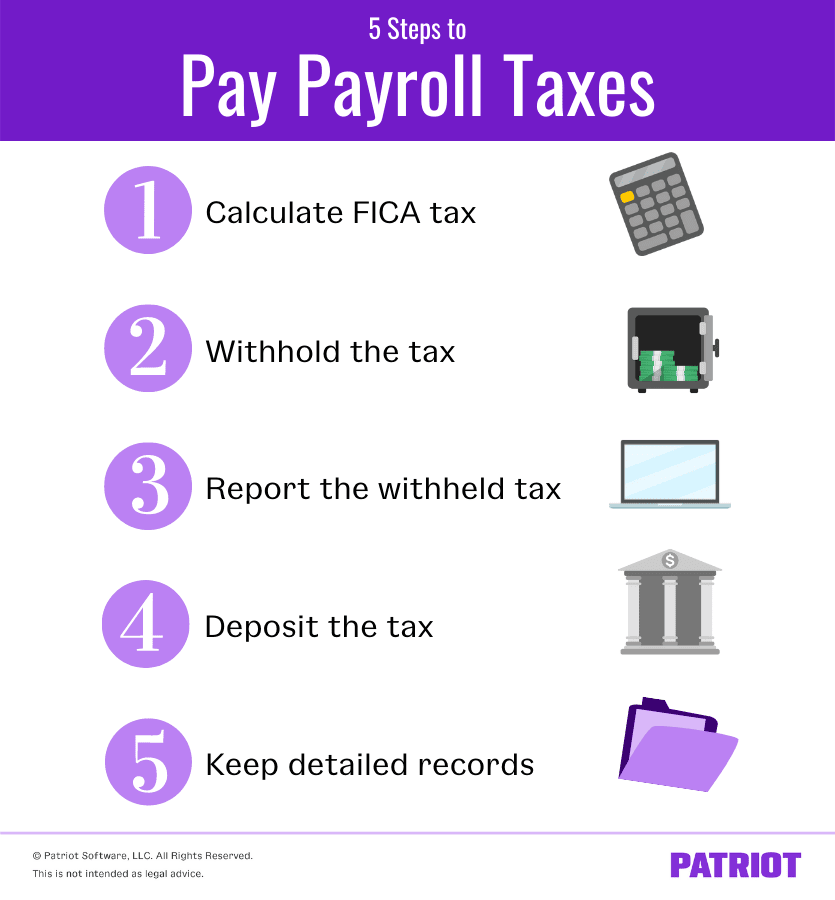

Financial transparency is the bedrock of an efficient tax process. To pay your taxes accurately, you must maintain a rigorous “paper trail” (or digital equivalent). This includes tracking 1099 forms for contract work, W-2s for traditional employment, and 1099-INT forms for interest earned on savings accounts. In the Money niche, we view record-keeping not as a chore, but as an audit-proofing strategy. Utilizing dedicated business accounts for professional expenses ensures that when it comes time to pay, you are only paying on your net profit, not your gross revenue.

2. Modern Methods to Pay Your Taxes Efficiently

The days of mailing a paper check and hoping it arrives on time are largely behind us. Modern financial tools have introduced several secure, rapid, and even rewarding ways to settle tax debts. Choosing the right method depends on your liquidity, your preference for digital security, and your desire to leverage financial incentives.

Electronic Funds Withdrawal (EFW) and Direct Pay

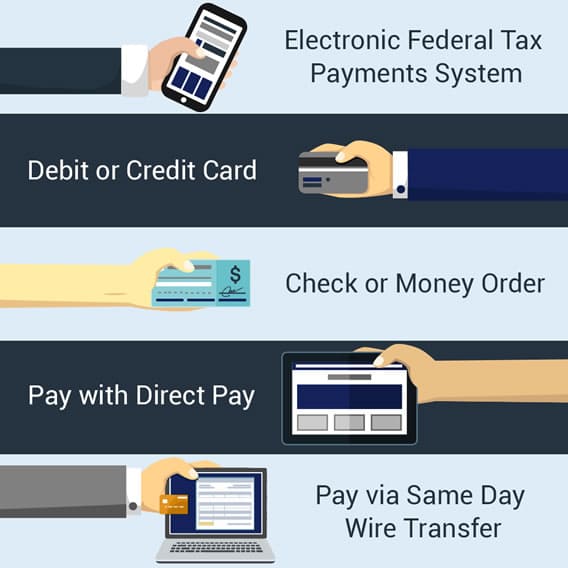

For most individual taxpayers, IRS Direct Pay is the gold standard of payment methods. This tool allows you to pay your taxes directly from a checking or savings account without any processing fees. From a personal finance perspective, this is the most efficient method because it provides an immediate confirmation number, ensuring that your funds are accounted for and eliminating the risk of mail fraud. Electronic Funds Withdrawal (EFW) is a similar option used when filing via tax software, allowing you to schedule a payment for a future date, which helps in managing cash flow.

Credit and Debit Card Payments: Pros and Cons

While the government accepts credit and debit card payments through third-party processors, this method requires a nuanced financial analysis. Processors typically charge a convenience fee ranging from 1.8% to 2.5%. If you are a practitioner of “credit card rewards” strategy, paying your tax bill with a card might make sense if the value of the points or cash back exceeds the processing fee. However, if you cannot pay off the balance immediately, the high interest rates on credit cards will quickly negate any benefits, turning a tax bill into a high-interest debt trap.

Using the EFTPS for Business and Large Payments

The Electronic Federal Tax Payment System (EFTPS) is a free service provided by the U.S. Department of the Treasury. While it requires a separate registration process, it is an essential tool for small business owners and high-net-worth individuals who need to make frequent or large payments. It offers the highest level of security and allows for detailed tracking of payment history, which is invaluable for long-term financial auditing.

3. Strategic Financial Planning for Tax Season

Paying your taxes should never be a reactive event. It should be the final step of a year-long financial strategy. By incorporating tax planning into your monthly budget, you ensure that the money is ready when the deadline approaches.

Setting Aside a “Tax Buffer” in High-Yield Savings

A common pitfall for freelancers and “side hustlers” is spending gross income rather than net income. A professional financial approach involves opening a separate High-Yield Savings Account (HYSA) specifically for taxes. By diverting 25% to 30% of every paycheck into this account, you not only ensure the funds are available for payment, but you also earn interest on the government’s money until the day it is due. This “tax buffer” acts as a psychological and financial safety net.

Estimating Quarterly Payments for Freelancers and Side Hustlers

If you expect to owe more than $1,000 in taxes, the government generally requires you to make quarterly estimated payments. In the world of business finance, this is known as staying “current.” Failing to make these payments can result in underpayment penalties. Strategic quarterly filing smooths out your cash flow; instead of one massive, debilitating payment in April, you break your liability into four manageable segments. This keeps your business’s working capital stable and predictable.

Maximizing Deductions and Credits to Lower Your Bill

The most effective way to “pay” your taxes is to legally reduce the amount you owe. This involves maximizing “above-the-line” deductions, such as contributions to a Traditional IRA or a Health Savings Account (HSA). These contributions lower your Adjusted Gross Income (AGI), which in turn lowers your tax liability. Furthermore, understanding the difference between a deduction (which lowers taxable income) and a credit (which provides a dollar-for-dollar reduction in the tax you owe) is vital for any serious investor or homeowner.

4. Managing Tax Debt and Payment Challenges

Sometimes, despite the best financial planning, life happens. A medical emergency or a business downturn can leave you without the liquid assets necessary to pay your tax bill in full. In the Money niche, the worst thing you can do is ignore the debt.

Installment Agreements and Payment Plans

The IRS and most state taxing authorities offer installment agreements. These are essentially loans from the government that allow you to pay your balance over several months or years. While these plans accrue interest and late-payment penalties, they are far less damaging than a tax lien or a levy. Setting up an installment agreement is a proactive move that protects your credit score and provides a structured path back to financial stability.

Offer in Compromise: A Last Resort

For those in extreme financial distress, an “Offer in Compromise” (OIC) allows you to settle your tax debt for less than the full amount you owe. This is a complex financial maneuver that requires proving that paying the full amount would create an unfair economic hardship. While difficult to obtain, it represents a “fresh start” for individuals looking to rebuild their personal finances from the ground up after a catastrophic financial event.

5. Leveraging Financial Tools and Professional Advice

As your financial life grows more complex—incorporating stock options, real estate investments, or international income—the “how” of paying taxes shifts from a simple transaction to a sophisticated operation.

Choosing the Right Financial Software for Your Profile

Technology has democratized tax filing, but not all tools are created equal. For a simple W-2 earner, free-file versions of popular software are sufficient. However, for those with diverse investment portfolios, premium versions that track cost basis and capital gains are necessary. These tools integrate directly with your brokerage accounts, ensuring that every dividend and stock sale is accounted for accurately, preventing overpayment.

When to Transition from DIY to a Certified Public Accountant (CPA)

There is a point in every successful person’s financial journey where the “cost” of a CPA becomes an investment rather than an expense. If you are spending dozens of hours navigating tax codes or if your financial situation involves K-1s, rental properties, or corporate structures, a professional is essential. A CPA doesn’t just help you pay your tax; they help you structure your wealth to minimize future liabilities. They provide a level of strategic insight—such as tax-loss harvesting or trust management—that software simply cannot replicate.

Conclusion

Paying your taxes is more than just a civic duty; it is a critical component of a disciplined financial life. By understanding the various payment portals, implementing a year-round savings strategy, and knowing when to seek professional counsel, you move from a position of tax-season anxiety to one of financial mastery. Remember, the goal of tax planning is not merely to pay what you owe, but to ensure that your hard-earned capital is utilized as efficiently as possible to build long-term wealth. Whether you are clicking “submit” on a Direct Pay transfer today or setting up a dedicated tax savings account for tomorrow, every step you take toward tax literacy is a step toward financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.