Navigating the complexities of car insurance can feel like a daunting task, but understanding the process is crucial for protecting yourself financially and legally on the road. In essence, obtaining car insurance is a transaction designed to transfer the financial risk of an accident from you to an insurance company. This article will guide you through the fundamental steps and considerations involved in securing adequate car insurance coverage.

Understanding the Basics of Car Insurance

Before you can acquire car insurance, it’s essential to grasp what it is and why it’s necessary. Car insurance is a contract between you and an insurance provider. In exchange for regular premium payments, the insurer agrees to cover specific financial losses you might incur due to a car accident or other covered events. These losses can include damage to your vehicle, damage to another person’s vehicle or property, and medical expenses for injuries sustained by you or others involved in an accident.

Why is Car Insurance Necessary?

The primary reasons for having car insurance are legal requirements and financial protection. Most jurisdictions mandate that drivers carry a minimum level of liability insurance. This ensures that if you are at fault in an accident, you have the financial means to compensate the other party for their damages and injuries. Without insurance, you could be personally liable for these costs, which can amount to tens or even hundreds of thousands of dollars.

Beyond legal obligations, car insurance serves as a critical financial safety net. Even if you are a cautious driver, accidents can happen due to the actions of others, unforeseen circumstances like adverse weather, or mechanical failures. Having comprehensive coverage can prevent a single incident from devastating your personal finances, potentially leading to bankruptcy or significant debt.

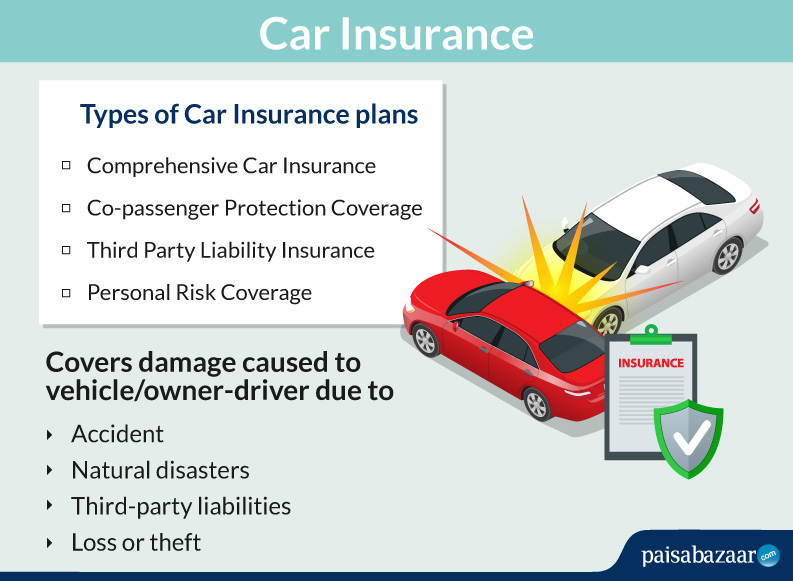

Key Types of Car Insurance Coverage

Understanding the different types of coverage available is fundamental to selecting the right policy. While specific names and offerings may vary slightly by insurer and state, the core components remain consistent:

Liability Coverage

This is the cornerstone of most car insurance policies and is typically legally required. Liability coverage is divided into two parts:

- Bodily Injury Liability (BI): This covers medical expenses, lost wages, and pain and suffering for individuals injured in an accident for which you are responsible. It’s usually expressed in limits per person and per accident (e.g., $25,000/$50,000, meaning up to $25,000 for injuries to one person, and up to $50,000 total for all injuries in a single accident).

- Property Damage Liability (PD): This covers the cost of repairing or replacing property damaged in an accident where you are at fault. This most commonly includes damage to the other driver’s vehicle, but can also extend to other property like fences, buildings, or utility poles. It’s typically expressed as a limit per accident (e.g., $25,000 for property damage).

Collision Coverage

Collision coverage pays for damage to your own vehicle resulting from a collision with another object (like a car, tree, or guardrail) or if your car overturns. This coverage is usually optional unless you have a car loan or lease, in which case the lender will likely require it. Collision coverage has a deductible, which is the amount you pay out-of-pocket before the insurance company starts paying.

Comprehensive Coverage

Also often optional but required by lenders, comprehensive coverage pays for damage to your vehicle that is not caused by a collision. This includes incidents like theft, vandalism, fire, natural disasters (hail, flood, wind), falling objects, and hitting an animal. Like collision coverage, comprehensive coverage also has a deductible.

Uninsured/Underinsured Motorist (UM/UIM) Coverage

This coverage is designed to protect you if you are involved in an accident with a driver who has no insurance (uninsured) or insufficient insurance (underinsured) to cover your damages and injuries. It can help pay for medical bills, lost wages, and sometimes vehicle repairs. This is highly recommended, even if not legally mandated in all areas.

Medical Payments (MedPay) or Personal Injury Protection (PIP)

These coverages help pay for medical expenses for you and your passengers, regardless of who is at fault in an accident. PIP is generally more comprehensive and may also cover lost wages and other related expenses. The availability and specific benefits of these coverages can vary significantly by state.

The Process of Getting Car Insurance

The journey to obtaining car insurance involves several distinct steps, from gathering necessary information to comparing quotes and making your selection. A methodical approach will ensure you secure the right coverage at a competitive price.

Step 1: Gather Essential Information

Before you start shopping, it’s crucial to have certain information readily available. This will streamline the quoting process and ensure accuracy. Key details you’ll need include:

- Driver Information: Full names, dates of birth, driver’s license numbers, and driving history (including any accidents, tickets, or DUIs) for all individuals who will be driving the insured vehicle.

- Vehicle Information: Year, make, model, Vehicle Identification Number (VIN), and any safety features or anti-theft devices installed on the vehicle.

- Current Insurance Information: If you have existing insurance, you’ll need policy details like the insurer’s name, policy number, and coverage limits.

- Driving Habits: Information about how you use the vehicle, such as your estimated annual mileage, whether it’s used for commuting to work or school, and if it’s primarily used for pleasure.

- Garaging Address: The primary location where your vehicle is parked overnight.

Step 2: Determine Your Coverage Needs

This is arguably the most critical step. Simply opting for the minimum required coverage might not be sufficient for your personal circumstances. Consider the following:

- Legal Minimums: Understand the minimum liability coverage mandated by your state. This is your baseline.

- Vehicle Value: If you have a newer or more valuable car, collision and comprehensive coverage are essential to protect your investment. For older, less valuable cars, you might consider dropping these coverages to save on premiums, but weigh this against the potential out-of-pocket costs if damage occurs.

- Financial Situation: Assess your personal financial resources. Can you afford to pay for significant repairs or medical bills out-of-pocket if an accident happens? If not, higher coverage limits and optional coverages like PIP or MedPay are advisable.

- Risk Tolerance: How comfortable are you with taking on financial risk? This will influence your deductible choices and the breadth of your coverage.

Step 3: Research and Compare Insurance Providers

Once you have your information and a clear idea of your needs, it’s time to explore the market. There are numerous car insurance companies, each with different pricing structures, customer service reputations, and available discounts.

- Online Comparison Tools: Utilize online insurance comparison websites. These platforms allow you to enter your information once and receive quotes from multiple insurers simultaneously. This is a highly efficient way to gauge the competitive landscape.

- Directly Contact Insurers: Don’t hesitate to visit the websites of individual insurance companies or call their agents directly. Some insurers offer discounts that are not always reflected on third-party comparison sites.

- Independent Insurance Agents: An independent agent works with several insurance companies and can offer unbiased advice tailored to your specific needs. They can help you navigate complex policies and find the best fit.

- Ask for Recommendations: Consult with friends, family, or colleagues who own cars. Their experiences and recommendations can be valuable insights.

Step 4: Obtain Quotes and Review Them Carefully

When you receive quotes, don’t just look at the bottom-line price. A thorough review is essential:

- Compare Coverage Levels: Ensure that the quotes you are comparing offer identical coverage limits and deductibles. A lower premium might be due to less coverage, which could leave you exposed.

- Understand Deductibles: Your deductible is the amount you pay before your insurance kicks in. A higher deductible generally results in lower premiums, but you’ll pay more out-of-pocket if you file a claim. Choose a deductible you can comfortably afford.

- Check for Discounts: Inquire about all available discounts. Common discounts include those for safe driving, good student, multi-car policies, bundling with other insurance products (like homeowners or renters insurance), low mileage, and safety features on your car.

- Review Policy Exclusions and Limitations: Read the fine print. Understand what is and is not covered by the policy and any limitations or exclusions that might apply.

Making Your Purchase and Maintaining Your Policy

After diligently comparing options, you’ll be ready to select a policy and make your purchase. The process doesn’t end there; ongoing maintenance is key to ensuring you remain adequately covered and benefit from the best possible rates.

Step 5: Choose Your Policy and Purchase It

Once you’ve identified the insurer and policy that best meets your needs and budget, it’s time to finalize the purchase.

- Online Purchase: Many insurers allow you to complete the entire process online, from getting a quote to purchasing the policy and printing temporary insurance cards.

- Phone Purchase: You can also often purchase a policy over the phone with an agent.

- In-Person Purchase: Some people prefer to meet with a local agent to discuss their options and complete the transaction in person.

You will typically need to pay your first premium or a portion of it to activate your coverage. You’ll receive your insurance documents, including your policy declarations page, which outlines your coverages, limits, deductibles, and premiums. Keep these documents in a safe place and consider carrying a copy of your proof of insurance in your vehicle.

Step 6: Understand Your Payment Options and Due Dates

Car insurance premiums are usually paid monthly, semi-annually, or annually. Understanding your payment schedule and the due dates is critical to avoid lapses in coverage.

- Payment Methods: Insurers typically offer various payment methods, including online payments, automatic bank withdrawals (auto-pay), phone payments, and mail-in checks. Auto-pay can often lead to additional discounts.

- Grace Periods: Be aware of your insurer’s grace period for late payments. While most offer a short grace period, it’s best to avoid relying on it, as a lapse in coverage can lead to higher premiums in the future and potential legal issues.

Step 7: Regularly Review and Update Your Policy

Your insurance needs are not static. Life circumstances change, and your insurance policy should adapt accordingly.

- Annual Reviews: Make it a habit to review your policy at least once a year, ideally before your renewal date. This is an excellent opportunity to reassess your coverage needs and shop around for better rates.

- Life Events: Notify your insurance provider immediately of any significant life events that could affect your insurance needs or eligibility for discounts. These include:

- Changes in Drivers: Adding or removing a driver from your household.

- Vehicle Changes: Purchasing a new car, selling an old one, or making significant modifications to your current vehicle.

- Address Changes: Moving to a new home or even a new zip code can impact your premiums.

- Changes in Driving Habits: A significant increase or decrease in your annual mileage.

- Changes in Marital Status: Getting married or divorced.

- Changes in Employment: Taking on a new job that involves significant driving or changes your commute.

- Shop Around Periodically: Even if your circumstances haven’t changed dramatically, it’s wise to compare quotes from different insurers every few years. Insurance companies adjust their pricing, and new discounts may become available. You might find a better deal elsewhere without compromising on coverage.

By following these steps and maintaining a proactive approach to your car insurance, you can ensure you have the appropriate protection for your vehicle and your finances, providing peace of mind on every journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.