Accrued liabilities represent a fundamental concept in the world of business finance, central to accurate financial reporting and analysis. Far from being a mere accounting technicality, understanding accrued liabilities offers deep insights into a company’s operational efficiency, financial health, and adherence to accepted accounting principles. At its core, an accrued liability is an expense that a business has incurred but has not yet paid. It reflects a current obligation for goods or services received, even if the invoice has not yet been processed or the payment due date has not arrived.

Defining Accrued Liabilities in Business Finance

The existence of accrued liabilities stems directly from the accrual basis of accounting, the standard method for most businesses. Unlike cash basis accounting, which recognizes revenues and expenses only when cash changes hands, accrual accounting aims to match revenues with the expenses incurred to generate them in the same period. This provides a more accurate picture of a company’s financial performance over a given period, irrespective of cash movements.

When a company incurs an expense for which it has received the benefit (e.g., employees worked, electricity was consumed, interest on a loan accumulated) but has not yet disbursed cash, that obligation becomes an accrued liability. These liabilities are critical for accurately representing a company’s financial position at a specific point in time and its performance over a period. Without their recognition, financial statements would understate expenses and overstate profits, leading to misleading conclusions about the business’s true economic reality.

The Accrual Accounting Principle

The matching principle, a cornerstone of accrual accounting, mandates that expenses must be recognized in the same accounting period as the revenues they helped to generate. If an expense is incurred in December, even if the payment isn’t due until January, it must be recorded as an expense and a corresponding liability in December’s financial statements. This principle ensures that financial reports reflect the economic substance of transactions rather than just the timing of cash flows.

For instance, consider a company that uses electricity throughout December but doesn’t receive its utility bill until mid-January, with a payment due date at the end of January. Under the accrual principle, the electricity cost for December must be recognized as an expense in December. Since it hasn’t been paid yet, it simultaneously creates an accrued liability on the balance sheet for the estimated amount. This meticulous approach prevents the distortion of a company’s profitability by ensuring all costs associated with generating revenue are accounted for in the correct period.

Common Examples of Accrued Liabilities

Accrued liabilities are ubiquitous across industries and take various forms. Recognizing these common examples helps solidify the concept:

- Accrued Salaries and Wages: Perhaps the most common example, this represents the wages and salaries owed to employees for work performed up to the end of an accounting period but not yet paid. If a payroll cycle ends on the 15th of the month, and the period-end is the 31st, two weeks of employee wages would be an accrued liability.

- Accrued Interest Expense: For companies with outstanding loans or lines of credit, interest accrues daily. The portion of interest incurred but not yet paid by the end of an accounting period constitutes an accrued interest liability.

- Accrued Utilities: As seen in the electricity example, the cost of services like electricity, water, and gas consumed but not yet billed or paid for at the close of an accounting period.

- Accrued Rent: If a company pays rent in arrears (after the usage period), the portion of rent owed for the current period but not yet paid would be an accrued liability.

- Accrued Taxes: This includes taxes like property taxes or sales taxes collected from customers but not yet remitted to the taxing authorities. Income tax payable can also be an accrued liability if estimated taxes exceed payments made.

- Accrued Professional Fees: Fees for legal, accounting, or consulting services that have been rendered but not yet invoiced or paid by the period end.

- Accrued Warranty Expenses: For companies selling products with warranties, an estimate of future warranty costs for products sold during the period is often accrued to match the expense with the revenue from sales.

Why Accrued Liabilities Matter

Beyond mere compliance with accounting standards, understanding and accurately reporting accrued liabilities is crucial for both internal management and external stakeholders. They provide a more complete and realistic picture of a company’s financial obligations and operational expenses, informing strategic decisions and investment appraisals.

Impact on Financial Statements

Accrued liabilities have a direct and significant impact on a company’s primary financial statements:

- Balance Sheet: Accrued liabilities are reported as current liabilities on the balance sheet. This is because they are typically expected to be settled within one year or one operating cycle, whichever is longer. Their presence increases total liabilities and, consequently, reduces owner’s equity if not properly accounted for as an expense that reduces retained earnings. A growing trend in accrued liabilities relative to other assets or revenues might indicate operational changes or efficiency issues.

- Income Statement: The corresponding expense (e.g., wages expense, interest expense, utilities expense) is recognized on the income statement in the period it is incurred, regardless of payment timing. This ensures that the income statement accurately reflects the true cost of doing business during that period, leading to a more precise calculation of net income or loss.

- Cash Flow Statement (Indirect Method): When preparing the cash flow statement using the indirect method, changes in current liabilities like accrued liabilities are an adjustment to net income to arrive at cash flow from operating activities. An increase in accrued liabilities implies that an expense was recognized but not yet paid in cash, thus increasing cash flow (since less cash left the business than was expensed). Conversely, a decrease means more cash was paid for expenses than was recognized in the period, reducing cash flow.

Role in Financial Analysis

For analysts and investors, accrued liabilities offer valuable insights. They help in:

- Assessing Solvency and Liquidity: A high level of accrued liabilities relative to current assets or revenues can be a concern if it indicates that the company is accumulating expenses without the immediate cash flow to cover them. Conversely, a stable or well-managed level suggests efficient operations.

- Evaluating Profitability: By ensuring all expenses are matched with revenues, accrued liabilities contribute to a more accurate gross and net profit calculation, preventing an overstatement of earnings.

- Forecasting and Budgeting: Management uses historical accrued liability data to improve budgeting for future periods. Accurate accruals mean more reliable expense forecasts, contributing to better financial planning.

- Identifying Operational Changes: Significant fluctuations in accrued liabilities can signal operational shifts. For example, a sudden jump in accrued payroll could mean increased hiring or overtime, while a change in accrued interest might reflect new borrowing or repayment strategies.

Accounting for Accrued Liabilities

The recognition and measurement of accrued liabilities require meticulous attention to detail and adherence to accounting principles. They are not merely placeholders but integral components of financial reporting.

Journal Entries and Recognition

Recognizing an accrued liability involves a simple but critical journal entry. At the end of the accounting period, an adjusting entry is made:

- Debit an Expense Account: This increases the relevant expense account (e.g., Wages Expense, Interest Expense) on the income statement, reflecting the cost incurred.

- Credit an Accrued Liability Account: This increases the specific liability account (e.g., Accrued Wages Payable, Accrued Interest Payable) on the balance sheet, reflecting the obligation to pay in the future.

For example, if a company estimates it owes $5,000 in wages for work performed but unpaid at month-end:

Debit: Wages Expense $5,000

Credit: Accrued Wages Payable $5,000

When the actual payment is made in the next period, the accrued liability is removed, and cash is credited:

Debit: Accrued Wages Payable $5,000

Credit: Cash $5,000

Estimation and Adjustments

One of the challenges with accrued liabilities is that their exact amount may not be known at the time of recognition. For instance, a utility bill might not arrive until after the accounting period closes. In such cases, businesses must make reasonable estimates based on historical data, usage patterns, or contractual agreements.

These estimates are crucial. If an estimate is later found to be significantly different from the actual amount when the bill arrives or payment is made, an adjustment will be required in the subsequent period. The goal is always to provide the most accurate estimate possible to ensure financial statements are as reliable as they can be. Material misstatements, even if unintentional, can lead to questions about the accuracy of financial reporting.

Distinguishing Accrued Liabilities from Other Liabilities

It’s common for individuals new to business finance to confuse accrued liabilities with other types of liabilities. While all represent obligations, their nature and recognition timing differ.

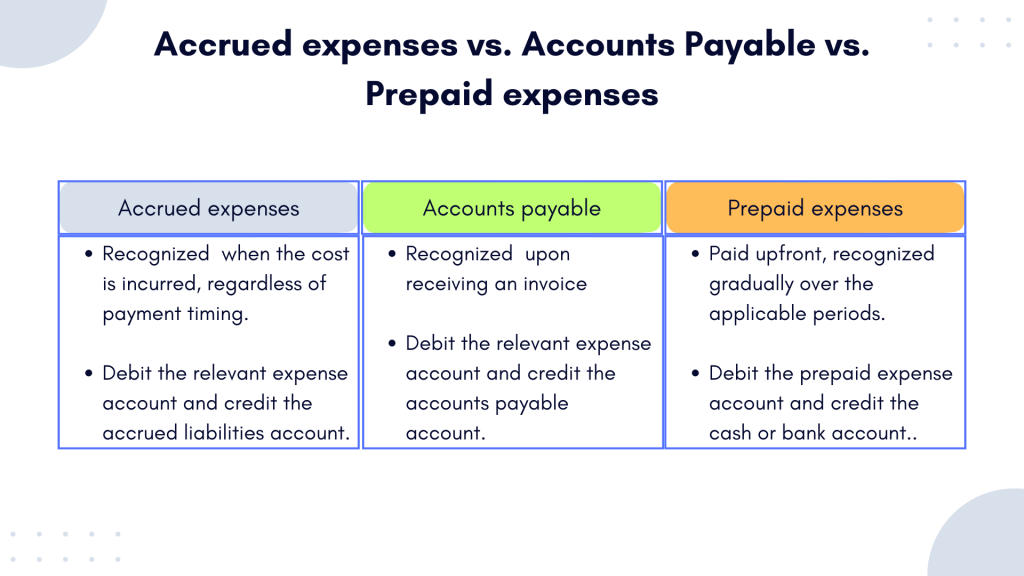

Accrued vs. Accounts Payable

The distinction between accrued liabilities and accounts payable (AP) is often subtle but important:

- Accounts Payable: These are liabilities for goods or services purchased on credit for which an invoice has been received from the vendor. The company has formally been billed and the amount is usually known and agreed upon.

- Accrued Liabilities: These are liabilities for expenses incurred where the benefit has been received, but an invoice has not yet been received or processed. The amount might be estimated.

Think of it this way: once an estimated accrued utility bill arrives and is processed, the accrued utility liability is typically reclassified to accounts payable, or eliminated as the actual expense is recorded against the accrual.

Accrued vs. Unearned Revenue

Unearned revenue (also known as deferred revenue) is another current liability that is conceptually distinct from accrued liabilities:

- Accrued Liability: An expense incurred by the business for which payment is owed to a third party. The business owes money for services/goods it received.

- Unearned Revenue: Money received by the business in advance for goods or services it owes to a customer in the future. Here, the business owes a service/good, not cash payment for an expense it incurred.

For example, a subscription service receiving an annual payment upfront records this as unearned revenue until the service is delivered. It’s a liability because the company has an obligation to provide a future service, not because it incurred an expense.

Managing and Monitoring Accrued Liabilities

Effective management of accrued liabilities is vital for maintaining sound financial health and accurate reporting. Businesses must implement robust processes to ensure these obligations are properly identified, estimated, and settled.

Best Practices for Businesses

- Strong Internal Controls: Establish clear policies and procedures for identifying and recording accrued expenses. This includes setting up cut-off procedures at period-end to ensure all expenses are captured.

- Regular Reconciliation: Periodically reconcile accrued liability accounts against supporting documentation (e.g., payroll records, loan statements, utility estimates) to ensure accuracy and identify discrepancies.

- Timely Recognition: Implement systems that prompt the recognition of common accruals, such as payroll, interest, and utilities, at the close of each accounting period.

- Conservative Estimation: When estimation is necessary, use a conservative but realistic approach to avoid understating liabilities or overstating profits. Regularly review and adjust estimation methodologies.

- Automation: Utilize accounting software that can automate the tracking and generation of recurring accrued liabilities, reducing manual errors and improving efficiency.

Implications for Investors

Investors should pay close attention to the trends in a company’s accrued liabilities. While they are a normal part of business, significant or unexplained changes can warrant further investigation:

- Increasing Accruals: A consistent increase in accrued liabilities might suggest a company is growing rapidly, incurring more expenses before payment. However, it could also signal liquidity issues if the company is delaying payments more frequently.

- Decreasing Accruals: A decrease might indicate efficient payment practices or a reduction in the level of operations requiring such accruals.

- Accruals vs. Cash Flow: Compare the growth of accrued expenses to the growth of cash flow from operations. If expenses are consistently growing faster than cash generation, it might indicate future cash shortages when those accruals become due.

In conclusion, accrued liabilities are more than just numbers on a balance sheet; they are a window into the operational realities and financial discipline of a business. By diligently applying accrual accounting principles, companies can provide a transparent and accurate financial narrative, benefiting management in decision-making and empowering investors with deeper insights into economic performance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.