A hospital stay, whether planned or unexpected, often brings with it a cascade of concerns, not least among them the financial implications. While the immediate focus is rightly on health and recovery, a strategic approach to what you pack—and what financial preparations you make—can significantly mitigate the monetary stress associated with medical care. This isn’t just about assembling a bag; it’s about financial foresight, smart resource management, and safeguarding your economic well-being during a vulnerable period. By meticulously considering the financial facets of your hospital visit, you can avoid unnecessary expenses, streamline administrative processes, and secure your financial future.

The Fiscal Prudence of Strategic Packing

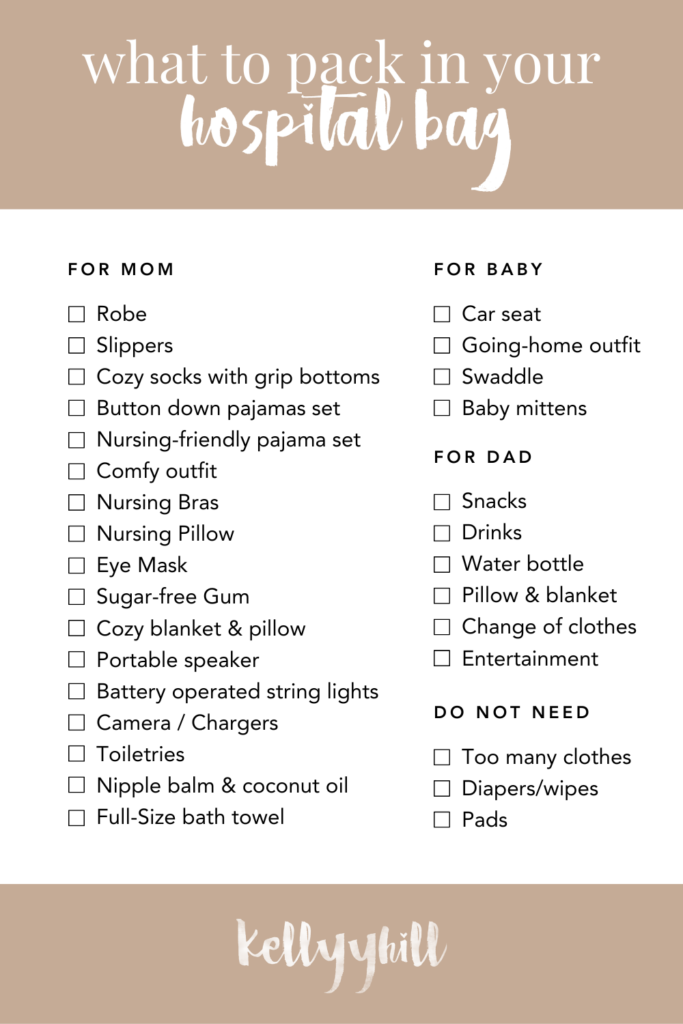

The seemingly innocuous act of packing a bag for a hospital stay holds substantial financial leverage. Hospitals, like any service provider, have markups on convenience items, and a lack of preparedness can lead to unplanned out-of-pocket expenses that quickly accumulate. Thoughtful packing is a proactive financial strategy, ensuring you bring essential personal items rather than incurring inflated costs for hospital-provided substitutes.

Avoiding In-Hospital Markups: Personal Comfort Items

Hospital gift shops and convenience stores often charge premium prices for everyday items such as snacks, beverages, reading materials, or even basic toiletries. Packing a small stash of your preferred non-perishable snacks, a reusable water bottle, and a personal comfort item like a familiar blanket or pillow can save you daily expenditures. While seemingly minor, these small costs can add up over a multi-day stay, diverting funds that could be better allocated elsewhere, perhaps towards post-discharge medications or co-pays. Furthermore, bringing your own device for entertainment—a tablet, e-reader, or smartphone with pre-downloaded content—avoids potential charges for hospital-provided television or internet services, or the impulse purchase of magazines and puzzle books.

Strategic Toiletries: Bringing Your Own vs. Hospital Provisions

Hospitals typically provide basic toiletries, but their quality and range are often limited. Opting to pack your preferred toothbrush, toothpaste, shampoo, conditioner, body wash, moisturizer, and other personal hygiene products ensures comfort while bypassing the expense of purchasing them from the hospital or relying on potentially irritating generic options. This isn’t merely a matter of preference; it’s an economic choice. A full-size bottle of shampoo at a retail pharmacy costs a fraction of a travel-sized version purchased at a hospital, and the cumulative savings over a prolonged stay become considerable. Moreover, packing specific items like unscented lotions or specialized dental care products can prevent allergic reactions or discomfort, potentially avoiding additional medical consultations or expenses.

Clothing and Footwear: Practicality and Post-Discharge Savings

While hospital gowns are standard, having your own comfortable, loose-fitting clothing and non-slip footwear is not just about dignity; it’s also a financial decision. Post-discharge, you’ll need suitable attire to leave the hospital. Relying on hospital-provided clothing can lead to discomfort or, in some cases, the need to purchase items from their gift shop if your original clothes are soiled or unsuitable. Packing soft pajamas, a robe, and a change of clothes for discharge can eliminate last-minute purchases. Non-slip slippers or shoes are also crucial for mobility and safety, preventing falls that could lead to further injury and subsequent medical bills.

Essential Financial & Administrative Documents for Your Pack

Beyond personal comfort, the most critical “packing” for a hospital stay involves your financial and administrative documents. These papers are the bedrock of efficient billing, insurance claims, and legal protection, directly impacting your out-of-pocket expenses and peace of mind. Without them, you risk significant delays, claim denials, and potentially higher costs.

Insurance Information: The Cornerstone of Coverage

This is non-negotiable. Pack your primary health insurance card, supplemental insurance cards (if applicable), and any relevant prescription drug cards. It’s also wise to have copies of your policy details, including your member ID, group number, claims address, and customer service contact information. Knowing your deductible, co-pays, and out-of-pocket maximums upfront can inform discussions with hospital billing departments and prevent unexpected charges. Having this information readily available enables quick verification of coverage, expediting admissions and ensuring accurate billing from the outset, thus minimizing the likelihood of denied claims due to administrative errors.

Identification and Emergency Contacts

While not strictly financial, your government-issued identification (driver’s license, state ID) and a list of emergency contacts are essential for administrative processes that impact financial responsibility. Accurate identification ensures your medical records are correctly linked to your insurance, preventing billing errors. The emergency contact list should include names, relationships, and phone numbers, allowing the hospital to reach designated individuals who may have access to your financial information or can make decisions if you are incapacitated. For international travelers, passport and visa details are equally critical for insurance claims and repatriation considerations.

Advance Directives and Powers of Attorney

For comprehensive financial and medical protection, especially in unforeseen circumstances, pack copies of your advance directives. This includes a Living Will, which outlines your preferences for medical treatment, and a Durable Power of Attorney for Healthcare, which designates someone to make medical decisions on your behalf if you cannot. Crucially, a Durable Power of Attorney for Finances names someone to manage your financial affairs (pay bills, access accounts) during your incapacitation. While not every hospital admission requires these, having them readily accessible can prevent legal entanglements, expensive court proceedings, and ensure your financial wishes are honored, thereby protecting your assets and estate from unnecessary administrative costs or mismanagement.

Pre-Hospital Financial Preparedness: Beyond the Bag

The financial implications of a hospital stay extend far beyond what fits into a physical bag. Proactive financial planning before an anticipated admission can significantly cushion the economic blow and empower you to focus on recovery without undue financial strain. This involves a thorough review of your financial standing and insurance coverage.

Reviewing Your Health Insurance Policy

Before an elective procedure or if you have time before an emergency admission, meticulously review your health insurance policy. Understand what your plan covers (e.g., specific tests, procedures, medications, specialists), what it doesn’t, and any pre-authorization requirements. Pay close attention to in-network versus out-of-network providers, as choosing the former can lead to substantial savings. Clarify your deductible, co-insurance, co-pays, and your annual out-of-pocket maximum. Knowledge of these figures allows you to anticipate potential costs and allocate funds accordingly, preventing sticker shock post-discharge. Contact your insurer directly with any questions, documenting dates and names of representatives for future reference.

Building an Emergency Medical Fund

A dedicated emergency fund is paramount for absorbing unexpected medical costs, deductibles, and other expenses not covered by insurance. Aim to have at least three to six months of living expenses saved, with a portion specifically earmarked for medical emergencies. This fund can prevent you from dipping into retirement savings, taking on high-interest debt, or liquidating investments at an inopportune time to cover medical bills. Such a fund provides a critical safety net, allowing you to prioritize your health without simultaneously battling financial distress.

Understanding Potential Out-of-Pocket Expenses

Even with robust insurance, out-of-pocket expenses are almost inevitable. These can include co-pays for doctor visits, deductibles that must be met before insurance kicks in, co-insurance (a percentage of the bill you’re responsible for), and costs for services deemed non-essential or not covered by your plan. Research potential costs for your specific procedure or condition. Websites like Fair Health Consumer or your insurance provider’s cost estimator tool can offer insights into average charges. Preparing a conservative estimate for these expenses allows you to mentally and financially brace for the financial impact.

Disability Insurance and Income Replacement

For individuals whose income relies on their physical presence or direct work, a hospital stay and subsequent recovery can lead to significant lost wages. Short-term and long-term disability insurance policies are crucial financial safeguards. Short-term disability typically covers a portion of your income for a few months, while long-term policies can extend for years. Review your employer-provided benefits or consider purchasing a private policy. Ensuring you have a plan for income replacement during incapacitation is a critical component of comprehensive financial planning for a medical emergency, preventing financial hardship during a period of vulnerability.

Navigating Post-Discharge Financial Realities

The financial journey doesn’t end when you leave the hospital. The period immediately following discharge is often when the true weight of medical expenses becomes apparent. Proactive management of bills and continued financial planning are essential to avoid long-term financial strain.

Scrutinizing Hospital Bills and Explanation of Benefits (EOBs)

Upon discharge, a barrage of bills may follow from the hospital, individual doctors (anesthesiologists, surgeons, consulting physicians), labs, and other services. Do not pay them without careful scrutiny. Compare each bill against your Explanation of Benefits (EOB) from your insurance company. The EOB details what services were billed, what your insurer covered, and your remaining responsibility. Look for duplicate charges, incorrect service codes, charges for services not rendered, and discrepancies between the bill and your EOB. Mistakes are common, and identifying them can save you thousands. Don’t hesitate to request an itemized bill, which provides a detailed breakdown of every charge.

Planning for Recovery Costs

Recovery often involves ongoing costs that extend beyond the hospital stay. These can include prescription medications, follow-up appointments with specialists, physical therapy, occupational therapy, home health care, or even necessary modifications to your home. Factor these potential expenses into your financial planning. Research the cost of required medications, especially if they are long-term. Discuss potential post-hospital care needs and their associated costs with your medical team before discharge to prepare a realistic budget for your recovery period.

Managing Debt Accrued During Treatment

If medical debt accumulates despite your best efforts, develop a strategy for managing it. Contact hospital billing departments to discuss payment plans, often interest-free. Inquire about financial assistance programs or charity care, especially if you meet income eligibility requirements. For larger debts, consider low-interest personal loans or credit cards with introductory 0% APR periods, but exercise caution to avoid accumulating further debt. Prioritizing higher-interest medical debts can prevent them from spiraling out of control. Proactively engaging with creditors demonstrates responsibility and often leads to more favorable terms.

Leveraging Financial Assistance Programs

Many hospitals, pharmaceutical companies, and non-profit organizations offer financial assistance programs to help patients with the cost of care or medications. Research these options thoroughly. Hospital charity care policies can reduce or even eliminate bills for eligible patients. Pharmaceutical patient assistance programs can provide free or low-cost medications. Disease-specific foundations often offer grants or support services. Leveraging these resources can significantly lighten the financial burden, allowing you to focus on your health without the crushing weight of insurmountable medical debt.

Preparing for a hospital stay involves more than just packing a bag; it demands meticulous financial planning and a strategic approach to managing potential costs. By focusing on proactive financial preparedness—from smart packing choices to comprehensive insurance review and post-discharge bill management—you can transform a potentially overwhelming experience into a manageable one, safeguarding your financial stability while prioritizing your health and recovery.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.