The world of real estate and mortgage finance is replete with intricate legal provisions designed to protect various parties. Among the most significant of these is the due-on-sale clause, a standard yet often misunderstood component of nearly every mortgage agreement. For anyone involved in property ownership, sales, or financing, a comprehensive understanding of this clause is not merely beneficial but essential for sound financial decision-making.

The Fundamentals of the Due-on-Sale Clause

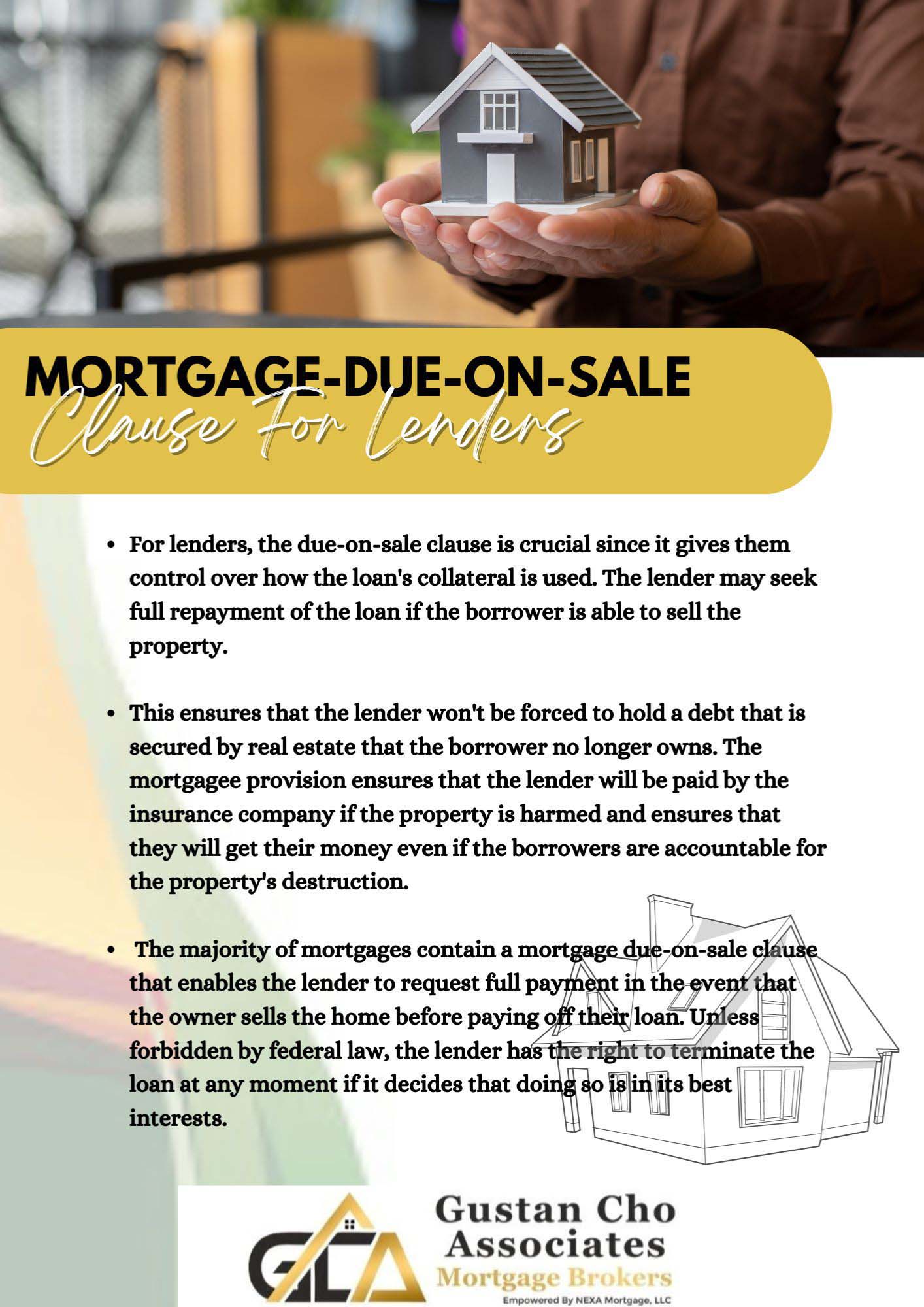

At its core, a due-on-sale clause, sometimes referred to as an “acceleration clause” or a “call clause,” is a contractual provision found in most mortgage or deed of trust documents. Its primary function is to give the mortgage lender the right to demand immediate repayment of the entire outstanding balance of a loan if the mortgaged property is sold or transferred to a new owner without the lender’s prior consent.

Definition and Purpose

Explicitly, the due-on-sale clause stipulates that if the borrower transfers any interest in the property—whether through an outright sale, a land contract, a lease-option, or even the conveyance of property into a trust or LLC—the lender has the option to “accelerate” the loan. This means the full remaining principal balance, along with any accrued interest and fees, becomes instantly due and payable. The overarching purpose is to protect the lender’s financial interests by ensuring that the party responsible for the mortgage payments remains the one whose creditworthiness and financial stability were originally evaluated during the loan underwriting process.

Without this clause, a homeowner could potentially sell their property to another individual who would then take over the existing mortgage at its original interest rate and terms, regardless of their own financial standing or the prevailing market interest rates. This could expose the lender to undue risk and circumvent their ability to re-evaluate the loan terms based on current economic conditions or the new borrower’s profile.

How it Works

When a property subject to a due-on-sale clause is transferred, the lender typically monitors public records for changes in ownership. Upon detecting such a transfer, or being notified by the original borrower, the lender may choose to exercise the clause. If they do, they will issue a formal notice to the original borrower, demanding full repayment of the loan within a specified timeframe, usually 30 to 60 days.

Should the borrower fail to pay off the loan as demanded, the lender has the legal right to initiate foreclosure proceedings on the property. This mechanism ensures that lenders maintain control over who holds their mortgages and under what terms, effectively preventing unauthorized assumptions of loans.

Historical Context

The enforceability of due-on-sale clauses faced significant challenges in various state courts during the late 1970s and early 1980s. Some courts viewed these clauses as restraints on alienation, meaning they hindered the free transferability of property. However, this legal uncertainty created significant instability in the mortgage market, particularly for savings and loan institutions.

To address this, the U.S. Congress passed the Garn-St. Germain Depository Institutions Act of 1982. This landmark federal legislation largely preempted state laws that restricted the enforceability of due-on-sale clauses, making them broadly enforceable nationwide, with specific, narrow exemptions. The act solidified the lender’s right to call a loan due upon the transfer of property, thereby stabilizing the financial industry and protecting lenders’ portfolios.

Why Lenders Enforce the Due-on-Sale Clause

Lenders are financial institutions operating on risk assessment and profitability. The due-on-sale clause serves as a critical tool in managing both. Its enforcement is rooted in several key financial and risk management principles.

Risk Management

Every mortgage loan is underwritten based on a meticulous evaluation of the original borrower’s credit history, income stability, debt-to-income ratio, and the property’s appraised value. This process quantifies the risk associated with lending to that specific individual for that specific asset. When a property is transferred to a new owner, the lender has no information about the new owner’s financial capabilities or their propensity to default. Enforcing the due-on-sale clause allows the lender to mitigate this unknown risk by either requiring the loan to be paid off or by forcing the new buyer to apply for a new loan, thereby undergoing their own underwriting process.

Interest Rate Protection

Perhaps one of the most significant motivations for enforcing the due-on-sale clause, especially in a rising interest rate environment, is interest rate protection. If a borrower secured a mortgage at a low interest rate (e.g., 3%) and market rates subsequently rise significantly (e.g., to 7%), a buyer could, in theory, assume the original low-rate mortgage without the clause. This would deny the lender the opportunity to issue a new loan at the higher, more profitable current market rate. The due-on-sale clause prevents this arbitrage, ensuring that lenders can recalibrate their loan portfolios to reflect current market conditions and maintain their profit margins.

Preventing Unapproved Transfers

The clause also acts as a safeguard against informal, unapproved transfers of property that could occur outside the formal lending process. Without it, creative financing schemes like “subject to” mortgages (where a buyer takes over payments without formally assuming the loan) would be far more prevalent, leading to confusion regarding loan responsibility and making default more likely without the lender’s knowledge. It ensures transparency and adherence to formal lending procedures.

Maintaining Portfolio Quality

By ensuring that loans are either paid off upon transfer or re-underwritten, lenders maintain the overall quality and predictability of their mortgage portfolios. This is crucial for managing their balance sheets, meeting regulatory requirements, and ensuring long-term financial stability. A portfolio of loans with known, qualified borrowers is far more stable than one where ownership has been informally transferred multiple times.

Common Scenarios and Exemptions

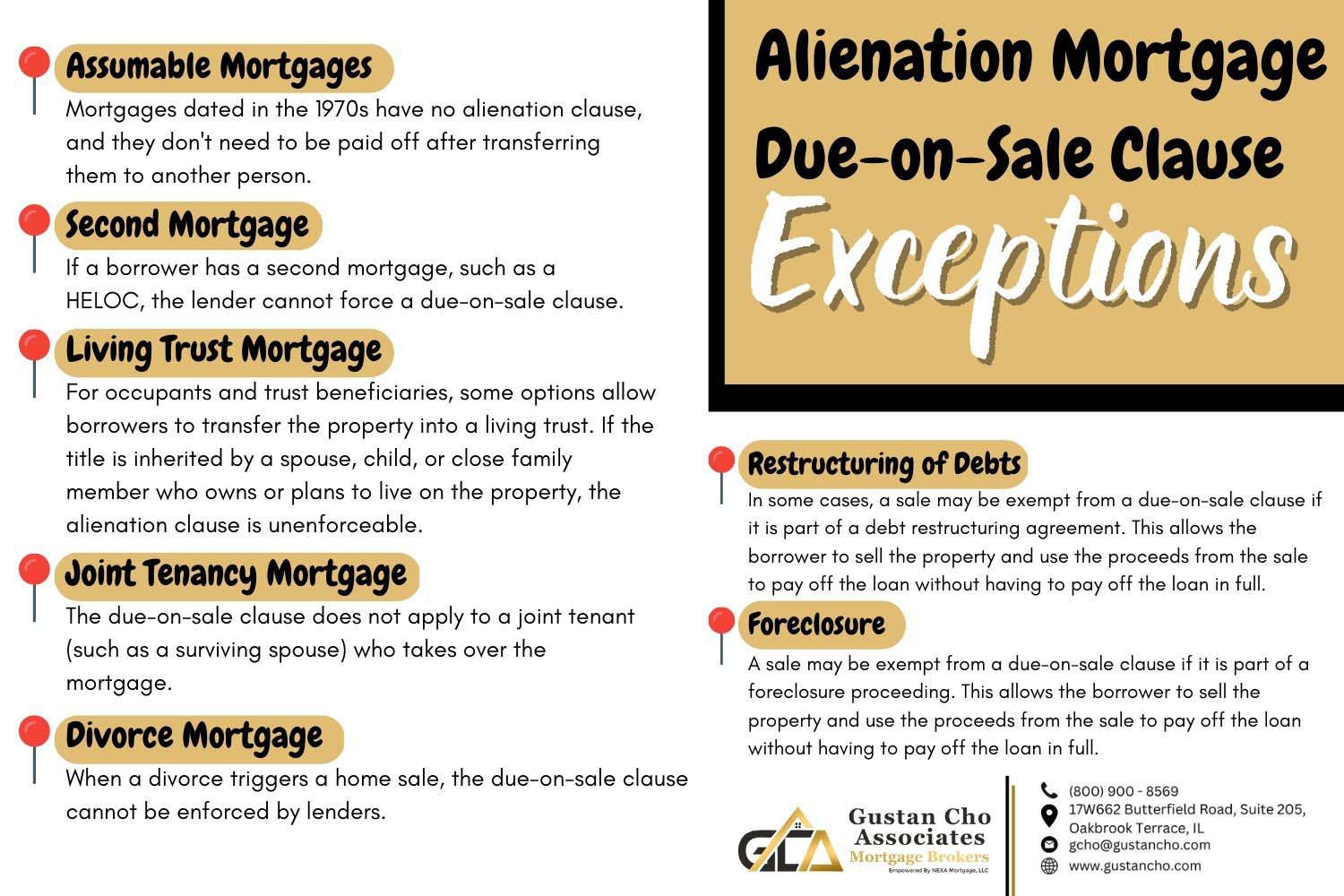

While the due-on-sale clause is broadly enforceable, it’s not without its nuances. Specific types of transfers are legally exempt from triggering the clause, primarily under the provisions of the Garn-St. Germain Act. Understanding these exemptions is critical for property owners and their heirs.

When it is Typically Triggered

![]()

The due-on-sale clause is generally triggered by any voluntary or involuntary transfer of a beneficial interest in the property. Common scenarios include:

- Outright Sale of the Property: The most straightforward trigger, where the property is sold to a new owner.

- Transfer into an Unapproved Trust or LLC: Moving the property title from an individual’s name into a living trust, a land trust, or a limited liability company (LLC) without the express consent of the lender. This is a common pitfall for real estate investors.

- Installment Land Contracts (Contract for Deed): Where the buyer makes payments directly to the seller, who retains legal title until the full purchase price is paid. Lenders often consider this a transfer of equitable interest.

- Lease-Option Agreements: If the lease agreement includes an option to purchase, lenders may view this as a beneficial transfer that triggers the clause, especially if the lease term is long or the rent payments include an equity build-up component.

- Junior Liens (in some cases): While less common, some mortgage documents might state that the creation of a junior lien (like a second mortgage or home equity line of credit) without lender consent could trigger the clause. However, this is rarely enforced for typical homeowner loans.

Key Exemptions (Garn-St. Germain Act)

The Garn-St. Germain Act specifically enumerates several transfers that lenders cannot use to trigger a due-on-sale clause. These exemptions are primarily designed to protect consumers in specific personal and familial situations:

- Transfers to a Spouse or Children: If the property is transferred to a spouse or children of the borrower.

- Transfers by Devise, Descent, or Operation of Law: Transfers that occur automatically, such as upon the death of a joint tenant, where the surviving joint tenant automatically receives full ownership.

- Leases of Less Than Three Years (No Purchase Option): A leasehold interest of three years or less, provided it does not contain an option to purchase.

- Transfer into an Inter Vivos Trust: A transfer into an inter vivos trust (a living trust) where the borrower remains a beneficiary of the trust and retains the right to occupy the property. This is a common estate planning tool and is specifically protected.

- Creation of a Purchase Money Security Interest for Household Appliances: This exemption is quite specific and relates to certain financing arrangements for appliances.

- Transfers Resulting from Divorce or Legal Separation: If a divorce decree or legal separation agreement mandates the transfer of the property to a spouse.

- Transfers to an Existing Co-owner: If one co-owner transfers their share of the property to another co-owner (e.g., from one joint tenant to another).

It is crucial to understand that these exemptions apply only to owner-occupied residential properties of one-to-four units. For investment properties or commercial real estate, these exemptions typically do not apply, and lenders have broader discretion to enforce the clause.

The “Subject To” Mortgage Strategy

A strategy sometimes discussed in real estate investment circles is purchasing a property “subject to” the existing mortgage. In this scenario, the buyer takes over the mortgage payments without formally assuming the loan, and the deed to the property is transferred. The original borrower remains legally responsible for the loan, but the new owner makes the payments.

While this approach bypasses the formal assumption process, it does not nullify the due-on-sale clause. The lender still has the right to enforce the clause upon discovering the transfer. The success of such a strategy hinges on the lender not exercising their right, which is inherently risky. If the lender discovers the transfer and calls the loan due, the new owner would face immediate repayment demands or potential foreclosure, and the original borrower’s credit would be severely impacted. This strategy is fraught with legal and financial peril and is generally advised against without expert legal counsel.

Implications for Borrowers and Buyers

The due-on-sale clause has profound implications for both parties in a real estate transaction, shaping the possibilities for financing, ownership transfers, and investment strategies.

For Borrowers (Sellers)

For the original borrower looking to sell their property, the due-on-sale clause largely dictates that they must pay off their existing mortgage in full at closing. This is typically done using the proceeds from the sale. This provision limits creative financing options, such as selling with seller financing where the buyer assumes the existing loan. If a borrower attempts to circumvent the clause and the lender discovers the transfer, they risk having the entire loan balance called due. Failure to pay could lead to foreclosure, severely damaging the borrower’s credit and financial standing. Therefore, transparency and adherence to loan terms are paramount.

For Buyers

For buyers, the due-on-sale clause primarily means that they generally cannot assume an existing mortgage from a seller, even if it has an attractive interest rate, without the explicit consent and approval of the lender. Instead, buyers will typically need to secure their own new financing at current market rates, or pay cash. This ensures fair market pricing for loans and prevents buyers from unduly benefiting from a seller’s older, lower-rate mortgage without proper underwriting. Buyers should always be wary of deals that promise to allow them to “take over” a mortgage without formal lender approval, as these arrangements carry significant risk.

Alternatives to Consider

Given the strict nature of the due-on-sale clause, parties seeking alternative financing or transfer methods must navigate carefully:

- Refinancing: The most common alternative for a buyer wanting to take advantage of low rates is for the current owner to refinance the mortgage into a new loan that the buyer can then assume, or for the buyer to obtain their own new mortgage.

- Seeking Lender Consent: In rare circumstances, lenders might agree to a loan assumption, particularly if the new borrower is exceptionally well-qualified and market rates haven’t changed dramatically. However, this is usually at the lender’s discretion and often involves a fee and a new underwriting process.

- Seller Financing (Free and Clear Property): If the seller owns the property free and clear (i.e., has no mortgage), they are not subject to a due-on-sale clause and can offer true seller financing or owner-occupied loan assumptions.

- Lease-Options with Caution: While general lease agreements are exempt, lease-options carry risk. If structured carefully (e.g., the option period is well past the lease term and no equity is built during the lease), they might avoid triggering the clause initially, but legal advice is crucial.

Navigating the Due-on-Sale Clause with Professional Guidance

The due-on-sale clause is a powerful legal instrument designed to protect lenders. Its implications for personal and business finance are significant, impacting everything from individual home sales to complex real estate investment strategies.

Legal and Financial Advice

Given the complexities and potential financial repercussions, it is always advisable for both sellers and buyers to seek professional legal and financial advice before engaging in any transaction that might involve an existing mortgage and a property transfer. A qualified real estate attorney can help interpret specific mortgage language, advise on the legality of proposed transfers, and explain the risks associated with different strategies. Financial advisors can help individuals understand the financial implications of the clause on their long-term wealth planning and investment goals.

Due Diligence

Before any property transfer, both parties should conduct thorough due diligence. This includes carefully reviewing all mortgage documents, especially the deed of trust or mortgage agreement, to identify the specific language of the due-on-sale clause. Understanding these terms beforehand can prevent costly surprises and ensure that all actions comply with legal and contractual obligations.

Transparency with Lenders

While avoiding enforcement of a due-on-sale clause through non-disclosure might seem appealing, it carries immense risk. Open and honest communication with the mortgage lender, where appropriate, can sometimes lead to approved solutions or at least a clear understanding of the lender’s stance. Attempting to circumvent the clause without their knowledge often leads to severe financial penalties and legal battles.

In conclusion, the due-on-sale clause is a fundamental aspect of modern mortgage finance. Its existence and enforceability underscore the importance of understanding the fine print in financial contracts and seeking expert guidance when navigating the intricacies of real estate transactions. For sound personal and business finance, respecting this clause is not just a legal necessity but a fundamental principle of risk management and financial prudence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.