The North Carolina standard deduction is a critical component of the state’s income tax system, playing a pivotal role in determining an individual’s taxable income and ultimately, their tax liability. For countless residents, understanding this deduction is the first step toward optimizing their state tax strategy. Unlike the federal tax system, where the standard deduction is often the subject of extensive national debate, North Carolina maintains its own set of rules and deduction amounts, tailored to its unique economic and legislative landscape. This fixed monetary amount serves to reduce a taxpayer’s gross income before calculating their tax obligation, effectively lowering the amount of income subject to taxation. Choosing whether to take the standard deduction or itemize deductions is one of the most significant decisions a taxpayer makes annually, directly impacting the money they keep versus the money they pay to the state.

The Foundation of Tax Deductions: Standard vs. Itemized

To truly grasp the significance of the North Carolina standard deduction, it’s essential to first understand the fundamental concept of tax deductions in general, and the distinction between standard and itemized deductions. This foundational knowledge provides the necessary context for making informed financial decisions at the state level.

Federal Context First

At the federal level, taxpayers have a choice: take the standard deduction or itemize. The federal standard deduction is a fixed dollar amount, adjusted annually for inflation, that reduces your adjusted gross income (AGI). It’s a no-questions-asked reduction, requiring no specific expenses to claim. Its primary purpose is to simplify tax filing for millions of Americans, providing an immediate tax benefit without the need for extensive record-keeping or complex calculations. Factors like filing status (single, married filing jointly, head of household, etc.), age, and blindness can all influence the federal standard deduction amount. This federal framework often serves as a mental baseline for taxpayers, but it’s crucial to remember that state tax systems can, and often do, diverge significantly.

State-Level Variations

While many states mirror the federal approach to some extent, others establish entirely independent systems. North Carolina falls into the latter category, with its own distinct standard deduction amounts and rules. This means that even if a taxpayer claims the federal standard deduction, they still need to evaluate their options specifically for their NC state income tax return. The North Carolina General Assembly periodically reviews and adjusts these amounts, reflecting state economic conditions and legislative priorities. Consequently, taxpayers cannot simply assume their federal deduction strategy will automatically translate to their state obligations; a separate analysis is always required for their NC return.

Navigating North Carolina’s Standard Deduction

Understanding the specific details of North Carolina’s standard deduction is paramount for any resident taxpayer. These amounts directly influence the taxable income calculation and necessitate careful consideration.

Defining the NC Standard Deduction

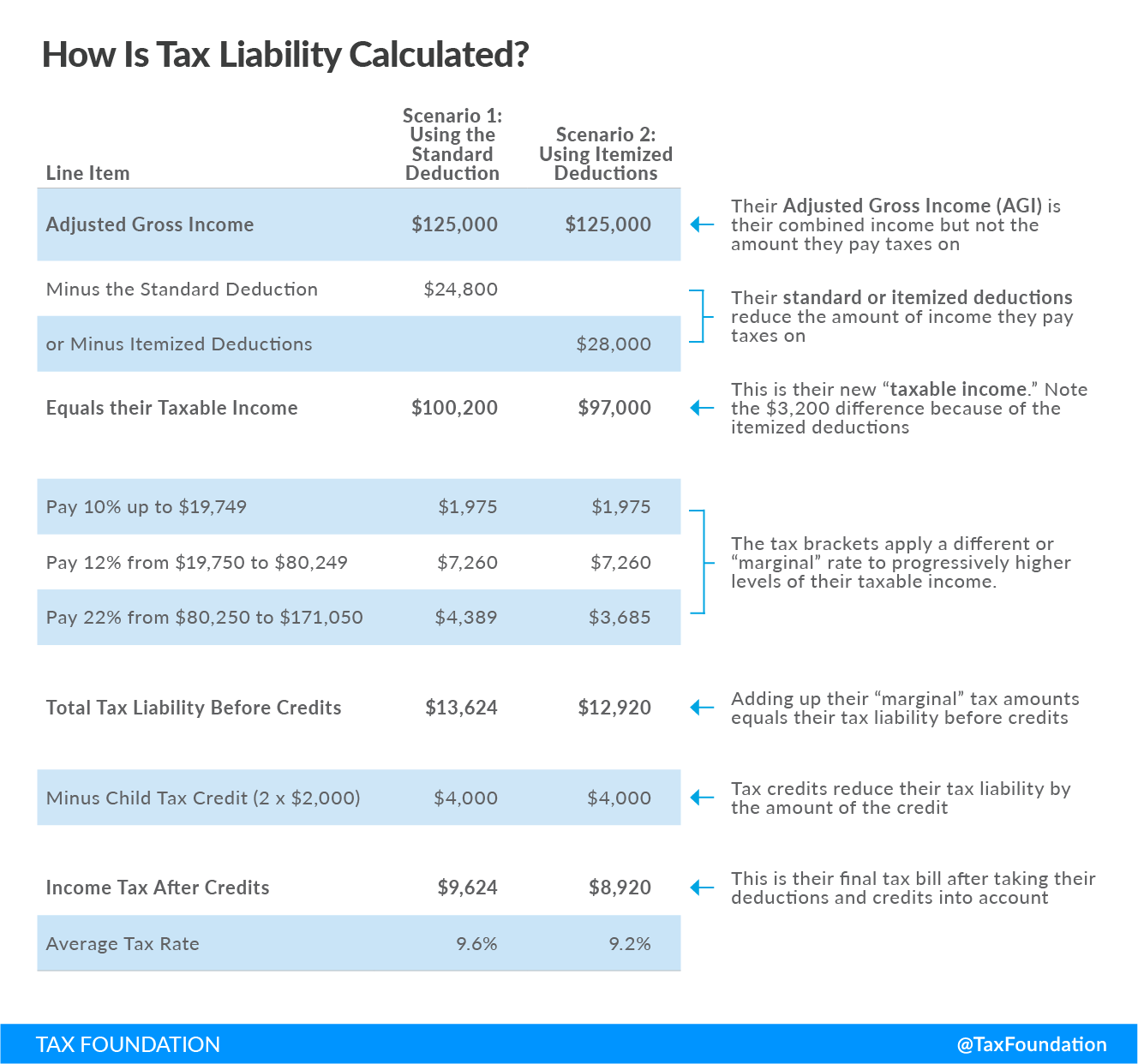

The North Carolina standard deduction is a predetermined fixed amount that a taxpayer can subtract from their North Carolina adjusted gross income (NC AGI) to arrive at their North Carolina taxable income. This deduction is available to all eligible taxpayers and does not require proof of specific expenses, unlike itemized deductions. It is designed to provide a straightforward and accessible tax benefit, especially for those whose allowable itemized expenses do not exceed the standard amount. For instance, if your NC AGI is $60,000 and you qualify for a $12,750 standard deduction, your NC taxable income would be $47,250. This reduction directly translates into lower state income tax obligations.

Current Amounts and Filing Status

The amount of the North Carolina standard deduction depends on your filing status. For the 2023 tax year (filed in 2024), the standard deduction amounts for North Carolina residents are as follows:

- Single: $12,750

- Married Filing Jointly: $25,500

- Married Filing Separately: $12,750

- Head of Household: $19,000

- Qualifying Widow(er): (Generally follows Married Filing Jointly)

It’s important to note that, unlike the federal system, North Carolina’s standard deduction does not typically include additional amounts for taxpayers who are age 65 or older, or who are blind. These adjustments are primarily federal provisions. The state focuses on the basic filing status to determine the standard deduction amount. These figures represent a significant reduction in taxable income for many households and are crucial benchmarks when deciding between the standard deduction and itemizing.

Evolution and Legislative Changes

The North Carolina standard deduction amounts are not static; they are subject to review and change by the North Carolina General Assembly. Historically, these amounts have seen increases, reflecting a legislative intent to reduce the tax burden on state residents or to align more closely with federal changes over time, though not directly copying them. For example, recent years have seen consistent increases in the standard deduction, often as part of broader state tax reform efforts aimed at simplifying the tax code and providing relief. Taxpayers should always consult the most current tax year’s official North Carolina Department of Revenue (NCDOR) publications or a qualified tax professional to ensure they are using the correct and most up-to-date figures, as relying on outdated information can lead to incorrect tax calculations and potential penalties.

Standard vs. Itemized: The Strategic Choice for NC Taxpayers

The decision to take the North Carolina standard deduction or to itemize deductions is a cornerstone of effective state tax planning. This choice can significantly impact a taxpayer’s final tax bill, making it imperative to understand the nuances of both options.

Understanding Itemized Deductions in NC

While the standard deduction offers a convenient, fixed reduction, itemized deductions allow taxpayers to subtract specific expenses from their taxable income. For North Carolina income tax purposes, many of the itemized deductions allowed by the federal government are also permitted by the state, with some critical distinctions. Common itemized deductions that can be claimed on an NC return include:

- Qualified Home Mortgage Interest: Interest paid on a mortgage for a primary residence and, in some cases, a second home, up to certain limits.

- Real Estate Property Taxes: Taxes paid on real property, such as your home. It’s crucial to note that for North Carolina income tax purposes, the state does not impose a cap on the deduction of state and local taxes (SALT) like the federal $10,000 limitation. This is a significant advantage for North Carolina homeowners, particularly those in high-property-tax areas.

- Charitable Contributions: Donations to qualified charitable organizations are deductible, up to a certain percentage of your adjusted gross income, similar to federal rules.

- Medical and Dental Expenses: Expenses exceeding a certain percentage of your adjusted gross income (usually 7.5% or 10%, aligning with federal thresholds) are deductible. This includes payments for diagnosis, cure, mitigation, treatment, or prevention of disease, and for treatments affecting any structure or function of the body.

- Certain Other Deductions: While many miscellaneous itemized deductions were eliminated at the federal level by the Tax Cuts and Jobs Act of 2017, North Carolina generally follows the federal rules regarding which itemized deductions are available. It’s always best to check the specific year’s NCDOR instructions for precise guidance.

The key is to meticulously track and document all eligible expenses throughout the year. Without proper records, even legitimate deductions cannot be claimed.

The Break-Even Point Analysis

The strategic choice between the standard and itemized deduction hinges on a simple comparison: which total is larger? If your combined eligible itemized deductions exceed the applicable North Carolina standard deduction for your filing status, then itemizing will result in a lower taxable income and, consequently, a lower tax bill.

For example, a married couple filing jointly in North Carolina has a standard deduction of $25,500 for the 2023 tax year. If their combined eligible itemized deductions—say, $15,000 in mortgage interest, $8,000 in property taxes, and $5,000 in charitable contributions—total $28,000, then they would benefit by itemizing because $28,000 is greater than $25,500. By itemizing, they would reduce their taxable income by an additional $2,500 compared to taking the standard deduction.

Conversely, if their itemized deductions only amounted to $20,000, they would be better off taking the $25,500 standard deduction, as it provides a larger reduction. Performing this comparison accurately requires diligent record-keeping of all potential itemized expenses.

Who Benefits Most from Itemizing in NC?

Generally, individuals or families who are likely to benefit most from itemizing their North Carolina deductions include:

- Homeowners with Significant Mortgage Interest: Especially those with larger mortgages in the early years of repayment.

- Individuals with High Property Tax Burdens: Given that NC does not impose a state-level SALT cap, this can be a substantial deduction.

- Generous Charitable Donors: Those who contribute significant amounts to qualified charities.

- Individuals with Substantial Unreimbursed Medical Expenses: Particularly if these expenses exceed the AGI threshold.

It’s crucial for these groups to diligently track their expenses to ensure they can take full advantage of itemized deductions if they prove more beneficial than the standard deduction.

Maximizing Your NC Tax Savings: Practical Strategies

Beyond simply choosing between the standard and itemized deduction, proactive planning and meticulous organization can further enhance your North Carolina tax savings.

Annual Review and Record Keeping

One of the most effective strategies for maximizing your tax deductions is to maintain thorough and organized records throughout the year. This means keeping track of all potential itemized expenses—mortgage interest statements (Form 1098), property tax bills, receipts for charitable contributions, and medical expense documentation. Even if you typically take the standard deduction, life circumstances can change, and having these records readily available allows for a quick and accurate comparison each tax season. Reviewing your financial situation annually, ideally before year-end, can help you project your total itemized deductions and determine if any additional deductible expenses could be made before December 31st to tip the scales in favor of itemizing.

Future Planning and Deductions

Major life events often have significant tax implications. Buying a home, incurring substantial medical expenses, or making large charitable donations can drastically alter whether the standard deduction or itemized deductions are more advantageous. For instance, the year you purchase a home, you’ll likely incur substantial mortgage interest and property taxes, making itemizing a strong possibility. Similarly, planning large charitable gifts in a single year (known as “bunching” deductions) can sometimes push you over the standard deduction threshold, allowing you to itemize in that year and potentially take the standard deduction in subsequent years. Strategic planning around these events can lead to substantial tax savings over time.

Utilizing Tax Software and Professionals

For many taxpayers, navigating the complexities of state tax law, especially when considering itemized deductions, can be daunting. Reputable tax software can guide you through the process, prompting you for relevant information and automatically performing the standard vs. itemized deduction calculation for both federal and state returns. These tools are designed to maximize your deductions and credits.

However, for more complex financial situations, such as owning multiple properties, significant investment income, or substantial business deductions, consulting a qualified tax professional (like a Certified Public Accountant or Enrolled Agent) is highly recommended. A professional can provide personalized advice, identify often-overlooked deductions, and ensure compliance with all state and federal tax laws, ultimately providing peace of mind and potentially greater tax savings. Their expertise can be invaluable in crafting a comprehensive tax strategy that accounts for all aspects of your financial life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.