Buying a home is often the largest financial transaction an individual undertakes, and navigating the complexities of mortgage financing is a critical step in this journey. Among the various terms and conditions homebuyers encounter, Private Mortgage Insurance (PMI) frequently emerges as a significant, often misunderstood, component of the monthly housing expense. Understanding PMI is essential for sound financial planning, impacting not only immediate affordability but also long-term wealth accumulation and investment strategies.

The Core Concept of Private Mortgage Insurance

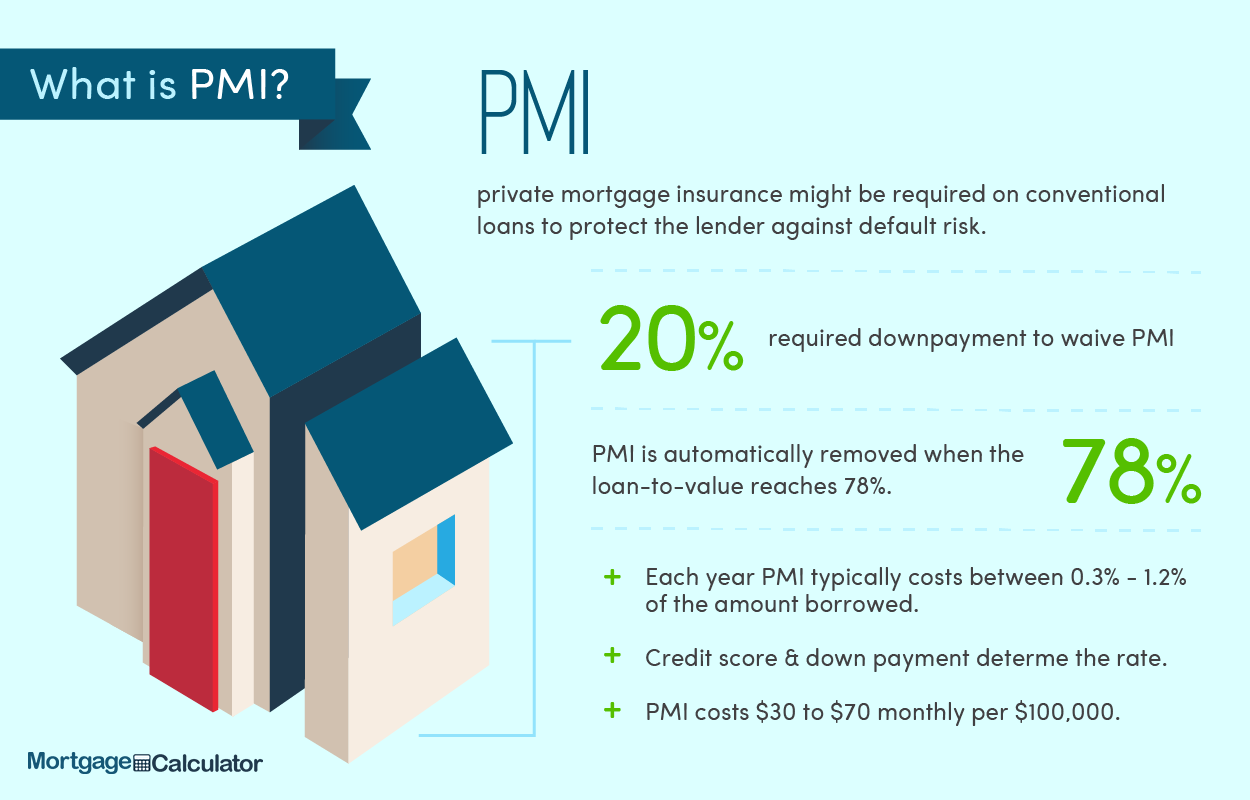

Private Mortgage Insurance (PMI) is a specific type of insurance policy designed to protect mortgage lenders, not the borrower, in the event that a homeowner defaults on their loan. It is typically required when a borrower makes a down payment of less than 20% of the home’s purchase price for a conventional loan. While the borrower pays the premiums, the primary beneficiary of PMI is the financial institution providing the mortgage.

Why Lenders Require PMI

The rationale behind PMI is rooted in risk mitigation. When a borrower puts down a smaller percentage (e.g., 5% or 10%), their equity stake in the home is initially low. This lower equity is perceived as a higher risk by lenders. If a borrower with limited equity defaults on their mortgage, the lender faces a greater potential for financial loss, as the sale of the foreclosed property might not cover the outstanding loan balance and associated costs. PMI acts as a safeguard, reimbursing the lender for a portion of that loss, thereby making it less risky for lenders to approve loans to individuals who can’t or choose not to make a substantial down payment. Without PMI, many homebuyers would be unable to secure a mortgage without saving up 20% or more for a down payment, significantly delaying homeownership for a large segment of the population.

Who Pays for PMI

Crucially, it is the borrower who bears the cost of PMI. This insurance premium is an additional expense on top of the principal and interest payment, property taxes, and homeowner’s insurance (often collectively known as PITI). While it protects the lender, it directly impacts the borrower’s monthly housing budget, making it a critical consideration when evaluating the affordability of a home.

Common Scenarios Triggering PMI

The most common scenario triggering PMI is when a borrower secures a conventional mortgage with a loan-to-value (LTV) ratio exceeding 80%. This means the loan amount is more than 80% of the home’s appraised value or purchase price (whichever is lower). For example, if a home costs $300,000 and the borrower puts down $30,000 (10%), the loan amount is $270,000. Since $270,000 is 90% of $300,000, the LTV is 90%, and PMI would be required. It’s important to note that government-backed loans, like FHA loans, have their own mortgage insurance premiums (MIP) which operate similarly but have different rules for cancellation. VA loans, for eligible veterans, typically do not require PMI due to a different guarantee system.

Types and Costs of PMI

The structure and cost of PMI can vary, offering different payment options that impact a homeowner’s financial outlay. Understanding these variations is key to selecting the most suitable mortgage product.

Borrower-Paid PMI (BPMI)

The most prevalent form is Borrower-Paid PMI (BPMI), where the homeowner directly pays the insurance premiums. BPMI can manifest in a few ways:

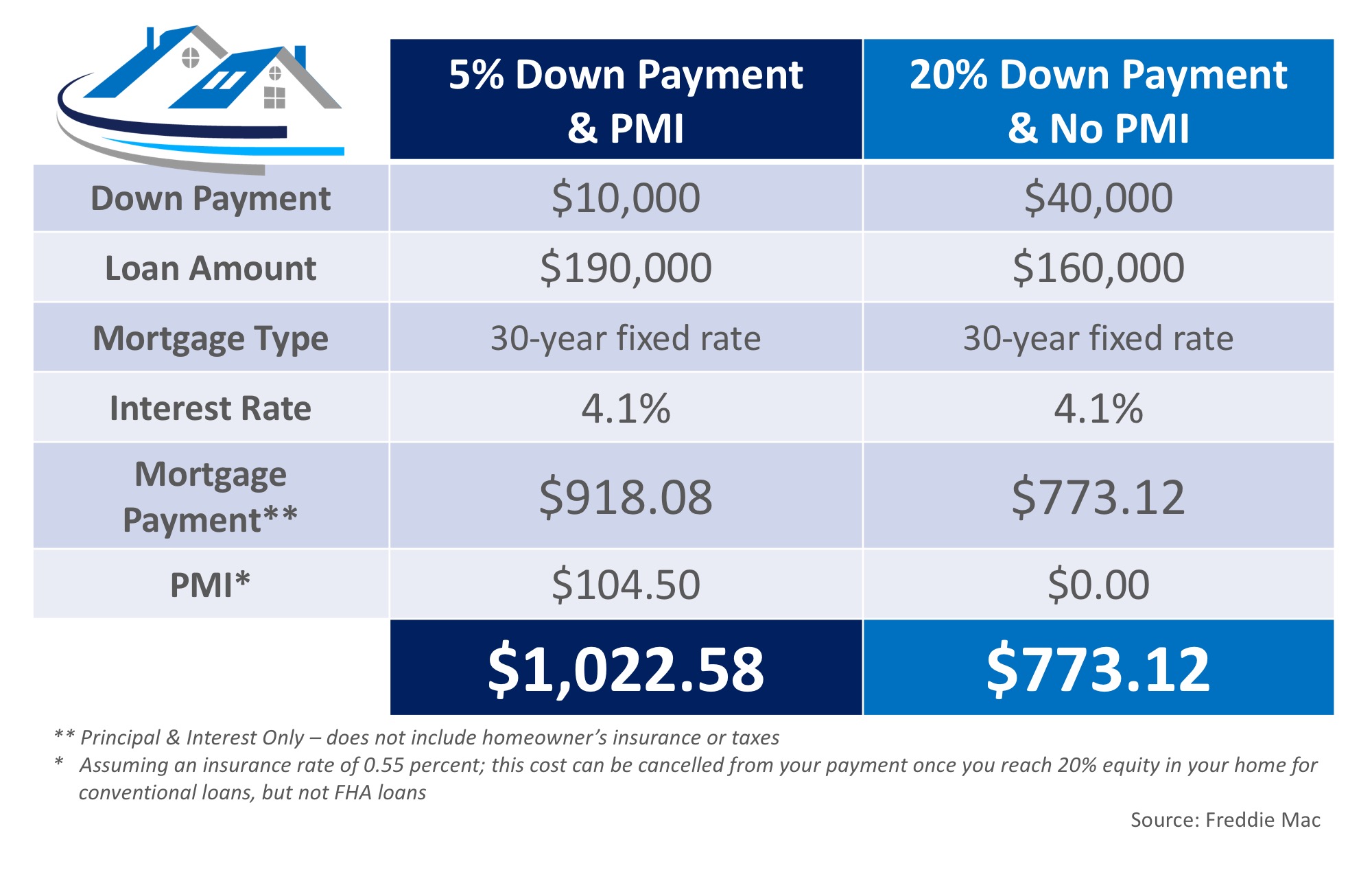

- Monthly PMI: This is the most common arrangement, where a portion of the PMI premium is added to the borrower’s regular monthly mortgage payment. It is typically calculated as a percentage of the original loan amount, ranging from approximately 0.3% to 1.5% annually. For instance, on a $250,000 loan, a 0.5% annual PMI would add about $104 per month ($250,000 * 0.005 / 12).

- Single-Premium PMI: In this option, the entire PMI premium is paid upfront in one lump sum at closing. This can reduce the monthly payment since there’s no ongoing PMI charge. However, it requires a significant amount of cash at closing, or the premium can be financed into the loan, which increases the overall loan amount and thus the interest paid over the life of the loan. A drawback is that if you refinance or sell the home shortly after, you may not get a refund of the unused portion.

- Split-Premium PMI: This is a hybrid approach where a portion of the PMI is paid upfront at closing, and the remaining balance is paid through monthly installments. This can lower both the upfront cost and the ongoing monthly payments compared to single-premium and monthly PMI respectively.

Lender-Paid PMI (LPMI)

Lender-Paid PMI (LPMI) is a less obvious form of PMI. In this scenario, the lender technically pays the PMI premium to the insurance company. However, the cost is passed on to the borrower in the form of a slightly higher interest rate on the mortgage loan. The advantage for the borrower is that there is no separate line item for PMI on their monthly statement, and the interest on the entire mortgage (including the LPMI component) may be tax-deductible (consult a tax advisor). The downside is that unlike BPMI, which can eventually be canceled, LPMI is embedded in the interest rate and typically lasts for the entire life of the loan unless the borrower refinances to a lower rate or a new loan without LPMI. This means a higher interest rate for the duration of the loan, potentially costing more in the long run than monthly BPMI that can be removed.

Factors Affecting PMI Cost

Several factors influence the actual cost of PMI:

- Loan-to-Value (LTV) Ratio: A higher LTV (meaning a smaller down payment) generally results in higher PMI premiums because the lender perceives greater risk.

- Credit Score: Borrowers with higher credit scores are seen as less risky, often qualifying for lower PMI rates.

- Loan Type: While we’re discussing conventional loans, different loan programs (e.g., high-balance loans) can have varying PMI structures.

- Loan Term: Shorter loan terms (e.g., 15-year mortgages) may sometimes have slightly lower PMI rates than longer terms (e.g., 30-year mortgages) due to less exposure to risk for the lender over time.

- Lender and Insurer: Different mortgage lenders use various PMI providers and have their own pricing models, so comparing offers is crucial.

- Appraisal Value: The appraisal value directly impacts the LTV calculation, influencing the PMI premium.

Strategies for Avoiding or Removing PMI

While PMI can enable earlier homeownership, it represents an additional cost that most homeowners aim to eliminate. Fortunately, several strategies exist for both avoiding PMI from the outset and removing it once the loan is established.

The 20% Down Payment Rule

The most direct way to avoid PMI altogether is to make a down payment of 20% or more of the home’s purchase price. A substantial down payment not only bypasses the need for PMI but also offers several significant financial advantages: a lower monthly mortgage payment (due to a smaller loan amount), less interest paid over the life of the loan, and instant equity in the property. For example, on a $300,000 home, a $60,000 down payment means no PMI, whereas a $30,000 down payment likely means PMI.

Automatic Termination

The Homeowners Protection Act (HPA) of 1998 provides statutory rights for homeowners to cancel PMI on conventional loans. Under the HPA, a lender is legally obligated to automatically terminate PMI when the loan-to-value (LTV) ratio reaches 78% of the original appraised value or purchase price of the home, whichever is less. This termination is contingent on the borrower being current on their mortgage payments. The lender must provide a disclosure at closing outlining these termination rights and typically tracks the LTV based on the original amortization schedule.

Borrower-Initiated Cancellation

Homeowners can proactively request the cancellation of PMI sooner than the automatic termination date. This is generally possible when the LTV reaches 80% of the original appraised value or purchase price. To initiate this process, the borrower must submit a written request to their mortgage servicer. The servicer will then typically require:

- A good payment history (no late payments within a specified period, often 12-24 months).

- No junior liens (e.g., a second mortgage or home equity line of credit).

- Proof that the property’s value has not decreased below its original value. This often necessitates a new appraisal, paid for by the borrower, to confirm the current market value and ensure the LTV based on the current value is 80% or less. If the home has appreciated significantly, this can be a fast track to removing PMI.

Refinancing

Refinancing a mortgage can be an effective way to eliminate PMI. If a homeowner’s equity has grown significantly (either through principal payments or market appreciation) to the point where the new loan’s LTV is 80% or less, they can refinance into a new conventional loan without PMI. This strategy can also be combined with securing a lower interest rate, potentially saving a substantial amount over the life of the loan. However, refinancing involves closing costs, so borrowers must weigh these against the savings from eliminating PMI and potentially lowering their interest rate.

Home Value Appreciation

In a rising real estate market, home values can appreciate significantly over time. This increase in value naturally lowers the LTV ratio, even if the borrower hasn’t made extra principal payments. If a homeowner believes their property has appreciated substantially, they can initiate a new appraisal and, if the LTV based on the current market value is 80% or less, request PMI cancellation from their lender. This is particularly appealing in areas experiencing rapid property value growth.

The Financial Impact and Broader Perspective

PMI, while an additional expense, plays a significant role in the broader landscape of homeownership, particularly for those with limited capital for a large down payment. Its impact extends beyond the monthly payment, influencing financial planning and access to the housing market.

The Cost-Benefit Analysis

For many prospective homeowners, PMI presents a trade-off: pay an extra monthly fee, or wait years to save up a 20% down payment. In a rising housing market, waiting can mean paying significantly more for the same home later. Thus, PMI can be seen as a tool that enables individuals to build equity sooner, potentially benefiting from home value appreciation. The cost of PMI must be weighed against the opportunity cost of delaying homeownership and missing out on potential market gains. It can be a bridge to wealth creation through real estate for those who are otherwise financially stable but cash-poor.

Impact on Affordability

PMI directly increases the total monthly housing cost. For first-time homebuyers or those with tight budgets, this additional expense can be a significant burden, potentially pushing a desirable home out of reach or forcing them to compromise on other aspects of their financial life. It’s crucial for buyers to factor PMI into their overall affordability calculations, ensuring the total housing payment remains sustainable within their financial plan. Overextending oneself for a home, even with PMI, can lead to financial strain down the line.

When PMI Makes Sense

PMI makes strategic sense for individuals who:

- Have stable income but limited savings for a large down payment.

- Are purchasing in a market with rapidly appreciating home values, where getting into a home sooner could mean significant equity gains that outweigh the cost of PMI.

- Prefer to keep a portion of their savings liquid for emergencies or other investments, rather than tying it all up in a down payment.

- Can quickly pay down their principal or anticipate rapid home appreciation, allowing for early PMI cancellation.

Long-Term Financial Planning

Integrating PMI into long-term financial planning involves more than just budgeting for the monthly premium. It requires understanding the various avenues for its removal and actively pursuing them. Homeowners should regularly review their loan statements, track their LTV, and consider options like additional principal payments or appraisals to accelerate PMI cancellation. Proactive management of PMI can free up hundreds of dollars per month, which can then be redirected towards savings, investments, or further accelerating mortgage principal reduction.

In conclusion, Private Mortgage Insurance is a critical component of housing finance that facilitates homeownership for countless individuals. While it adds to the cost of a mortgage, it serves a vital role in lender risk management and broadens access to the housing market. A thorough understanding of how PMI works, its various forms, and the strategies for its avoidance or removal empowers homeowners to make informed financial decisions and manage their housing investment wisely.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.