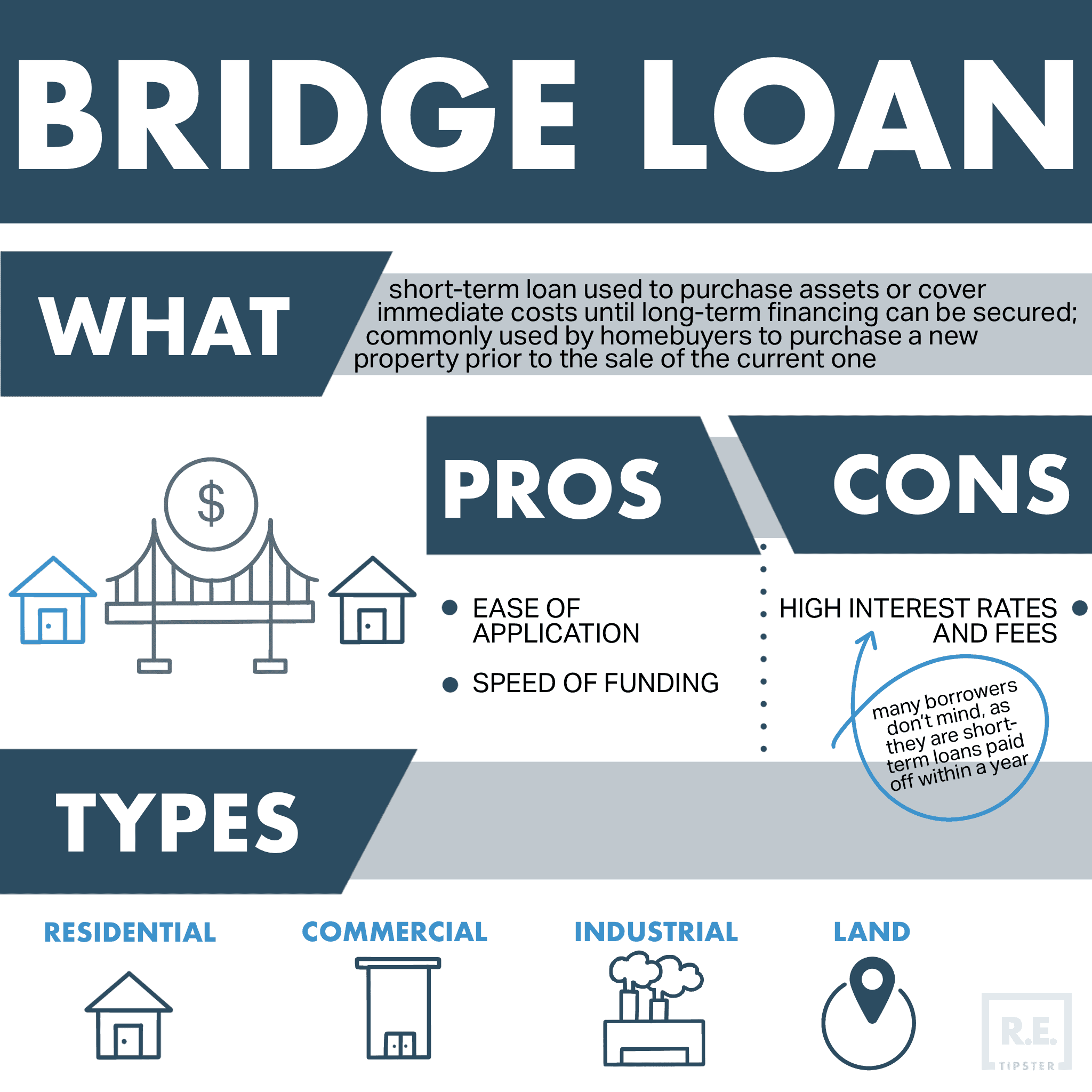

A bridge loan mortgage, often simply referred to as a bridge loan, is a short-term financing option designed to “bridge the gap” between the purchase of a new asset and the sale of an existing one. In the realm of real estate, this typically means providing funds to buy a new home before the current one has sold. It acts as a temporary financial solution, granting homeowners the flexibility to close on a new property without the immediate proceeds from their old property’s sale, thus avoiding contingent offers or the stress of needing to move twice.

This specialized financial instrument is a critical tool for individuals and businesses navigating complex real estate transitions. Unlike traditional mortgages that span 15 to 30 years, bridge loans have a much shorter repayment period, usually ranging from six months to one year, though some can extend up to two years. Their purpose is specific and finite, intended to be repaid quickly once the primary asset, usually the previous home, is sold.

The Core Concept of a Bridge Loan

At its heart, a bridge loan is about timing and liquidity. Real estate transactions rarely align perfectly, and the traditional process often leaves sellers in a predicament: either sell their current home first and face temporary housing, or buy a new home contingent on selling the old one, which can make their offer less attractive in a competitive market. A bridge loan mitigates these challenges by providing immediate capital.

Bridging the Gap in Real Estate

The most common application of a bridge loan is in residential real estate. Imagine a homeowner who finds their dream home but hasn’t yet sold their current residence. Without a bridge loan, they might have to wait for their existing home to sell, potentially losing out on the new property. Alternatively, they could make a contingent offer, which is often less appealing to sellers who prefer swift, unconditional sales.

A bridge loan allows the homeowner to secure the funds needed for the down payment and other closing costs on the new home, effectively “bridging” the financial gap until their old home sells. Once the old home sells, the proceeds are used to repay the bridge loan, often in a lump sum. This seamless transition can reduce stress, eliminate the need for temporary housing, and strengthen a buyer’s position in a competitive market.

Typical Scenarios for Bridge Loans

While home purchasing is the primary use case, bridge loans serve various strategic purposes:

- Non-Contingent Offers: Allows buyers to make a stronger, non-contingent offer on a new home, increasing their chances of acceptance, especially in seller’s markets.

- Time for Renovations: Provides funds to purchase a new home and perform necessary renovations or upgrades before moving in, without the pressure of needing to sell the old home immediately.

- Estate Sales: Can provide quick liquidity for heirs to pay estate taxes or other immediate expenses while a property is being prepared for sale and marketed.

- Investment Property Flips: Real estate investors often use bridge loans to acquire and rehabilitate properties quickly. The short-term nature aligns with the expedited timeline of a “fix and flip” strategy, with the loan repaid once the renovated property is sold.

- Commercial Real Estate: Businesses might use bridge loans to acquire new premises or refinance existing debt quickly while awaiting long-term financing approval or the sale of an existing commercial asset.

How Bridge Loans Work: Mechanics and Features

Understanding the operational aspects of a bridge loan is crucial for evaluating its suitability. These loans differ significantly from conventional mortgages in their structure, terms, and costs.

Short-Term Nature and Repayment

The defining characteristic of a bridge loan is its short duration. Typically, terms range from 6 to 12 months, though some lenders may offer up to 24 months. The expectation is that the borrower will sell their existing property within this timeframe, using the proceeds to pay off the bridge loan in full.

Repayment structures can vary. Some bridge loans are interest-only, meaning the borrower only pays the interest each month, with the principal due in a single balloon payment at the end of the term or upon the sale of the old home. Others might require full principal and interest payments, similar to a traditional loan, though this is less common for the shortest terms. The specific repayment terms are heavily influenced by the lender’s risk assessment and the borrower’s financial profile.

Collateral and Underwriting

Bridge loans are secured loans, meaning they require collateral. In residential real estate, this collateral is typically the equity in the borrower’s existing home, the new home being purchased, or sometimes both. Lenders assess the borrower’s equity position, the value of the properties involved, and the likelihood of the existing property selling within the loan term.

Underwriting for bridge loans tends to be faster and less stringent than for traditional mortgages. Lenders focus more on the collateral value and the borrower’s exit strategy (i.e., the plan to sell the old home) rather than solely on their debt-to-income ratio or credit score, although these factors are still considered. The loan-to-value (LTV) ratio for bridge loans is generally lower than for conventional mortgages, reflecting the higher risk profile of short-term, asset-backed lending. LTVs often range from 65% to 80% of the combined value of both properties or the equity in the existing home.

Interest Rates and Fees

Due to their short-term nature and higher perceived risk compared to conventional mortgages, bridge loans typically come with higher interest rates. These rates can be several percentage points above standard mortgage rates, often fluctuating based on market conditions, the borrower’s creditworthiness, and the loan-to-value ratio. Rates are frequently variable, tied to a benchmark like the prime rate plus a margin.

Beyond interest, bridge loans also involve various fees that can significantly impact the overall cost. These often include:

- Origination Fees: A percentage of the loan amount, typically ranging from 1% to 3%, paid to the lender for processing the loan.

- Appraisal Fees: Costs associated with valuing the properties involved.

- Closing Costs: Legal fees, title insurance, recording fees, and other administrative expenses similar to those in a traditional mortgage.

- Pre-payment Penalties: Some bridge loans may include penalties if the loan is paid off much earlier than anticipated, though this is less common for loans specifically designed to be short-term.

- Junk Fees: Miscellaneous charges that can accumulate.

Borrowers must meticulously review all fees and the annual percentage rate (APR) to understand the true cost of a bridge loan and compare it against alternatives.

Advantages and Disadvantages of Using a Bridge Loan

While bridge loans offer significant flexibility, they are not without their drawbacks. A thorough assessment of their pros and cons is essential before committing.

Benefits: Speed and Flexibility

- Quick Access to Funds: Bridge loans are processed much faster than traditional mortgages, often closing within weeks or even days, allowing borrowers to act swiftly on new opportunities.

- Seamless Transition: They eliminate the need for temporary housing, enabling homeowners to move directly from their old home into their new one without the stress of being caught between properties.

- Stronger Buyer Position: By removing the “sale contingency,” buyers can present a more attractive and competitive offer, particularly in hot real estate markets.

- Leveraging Equity: Allows homeowners to tap into the equity of their current home before it’s sold, providing immediate liquidity for a down payment or other expenses.

- Financial Flexibility: Offers a buffer period to prepare the old home for sale, potentially increasing its market value without the pressure of an immediate move-out date.

Risks: Cost and Contingencies

- Higher Interest Rates: The most significant drawback is the increased cost of borrowing. Interest rates are generally higher than conventional mortgages, and when combined with fees, the total cost can be substantial for a short-term loan.

- Multiple Loan Payments: For a period, the borrower will be responsible for two mortgage payments – their existing home loan, and the bridge loan. This can strain cash flow, especially if the old home takes longer to sell.

- Risk of Double Payment Burden: If the old home does not sell within the bridge loan’s term, borrowers can face significant financial pressure. They might need to extend the bridge loan (if possible, with additional fees) or find alternative financing, potentially at even less favorable terms.

- Reliance on Home Sale: The entire strategy hinges on the successful and timely sale of the existing property. Market downturns or unexpected issues with the old home can complicate the exit strategy.

- Additional Closing Costs: Borrowers incur a second set of closing costs with a bridge loan, adding to the overall expense.

Alternatives and When to Consider a Bridge Loan

Before opting for a bridge loan, it’s prudent to explore other financing avenues and carefully consider the specific circumstances that make a bridge loan the most suitable choice.

Home Equity Loans and HELOCs

- Home Equity Loan (HEL): A second mortgage that provides a lump sum based on the equity in your current home. It has a fixed interest rate and a set repayment schedule. While it provides immediate cash, it adds another monthly payment and typically requires a longer repayment period than a bridge loan.

- Home Equity Line of Credit (HELOC): A revolving line of credit secured by your home’s equity. You can draw funds as needed, up to a certain limit, during a draw period. Interest rates are often variable. HELOCs offer flexibility but also add a second monthly payment and usually require the existing home to remain in your possession for longer.

Both HELs and HELOCs are generally cheaper than bridge loans in terms of interest rates but might not offer the same speed or comprehensive coverage of costs for a new home purchase, and they still involve carrying two loans simultaneously.

Personal Loans and Other Options

- Unsecured Personal Loans: These are typically for smaller amounts, have even higher interest rates than bridge loans, and shorter terms. They are generally not sufficient for covering the down payment of a new home.

- 401(k) Loans: Borrowing from your 401(k) can offer low interest rates and flexible repayment, but it reduces your retirement savings and can have tax implications if not repaid on time.

- Family Loans: Borrowing from family members can be an interest-free or low-interest option but comes with its own set of personal considerations.

Strategic Considerations

A bridge loan is most advantageous when:

- Time is of the essence: You’ve found an ideal property and need to move quickly to secure it, especially in a competitive market.

- Strong Equity Position: You have substantial equity in your current home that can serve as ample collateral.

- High Confidence in Sale: You are confident your existing home will sell quickly and at a good price, minimizing the duration and cost of the bridge loan.

- Financial Capacity: You have the financial stability to comfortably manage two mortgage payments for several months, even if the sale of your old home is delayed.

- Desire for a Smooth Transition: You prioritize avoiding temporary housing and the inconvenience of moving twice.

Ultimately, a bridge loan mortgage is a powerful, albeit expensive, financial tool that offers unparalleled flexibility for specific real estate transitions. Its utility lies in its ability to provide immediate liquidity and eliminate timing conflicts, but its high cost and reliance on a swift sale necessitate careful planning and a clear understanding of the associated risks.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.