Marriage is often viewed through the lens of romance, tradition, and personal fulfillment. However, from a strictly economic perspective, marriage is one of the most significant financial contracts an individual will ever sign. As societal trends shift and the percentage of Americans opting for matrimony declines, the financial implications of this choice have become increasingly complex. Understanding the current marital landscape requires looking beyond the ceremony and into the balance sheets that define modern households.

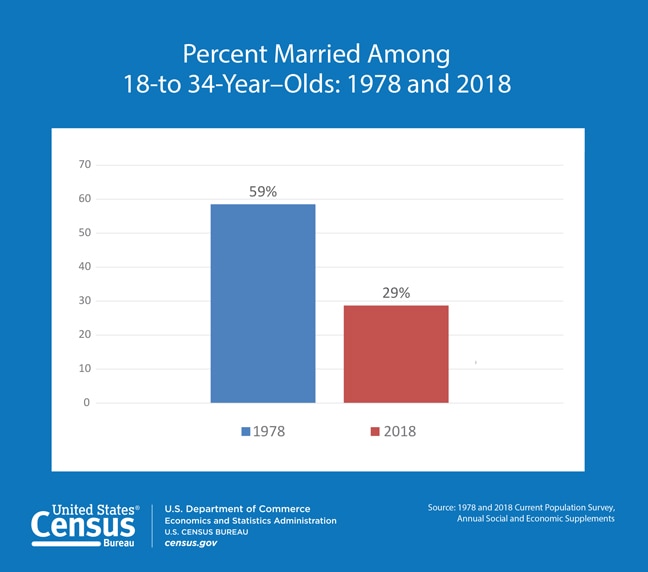

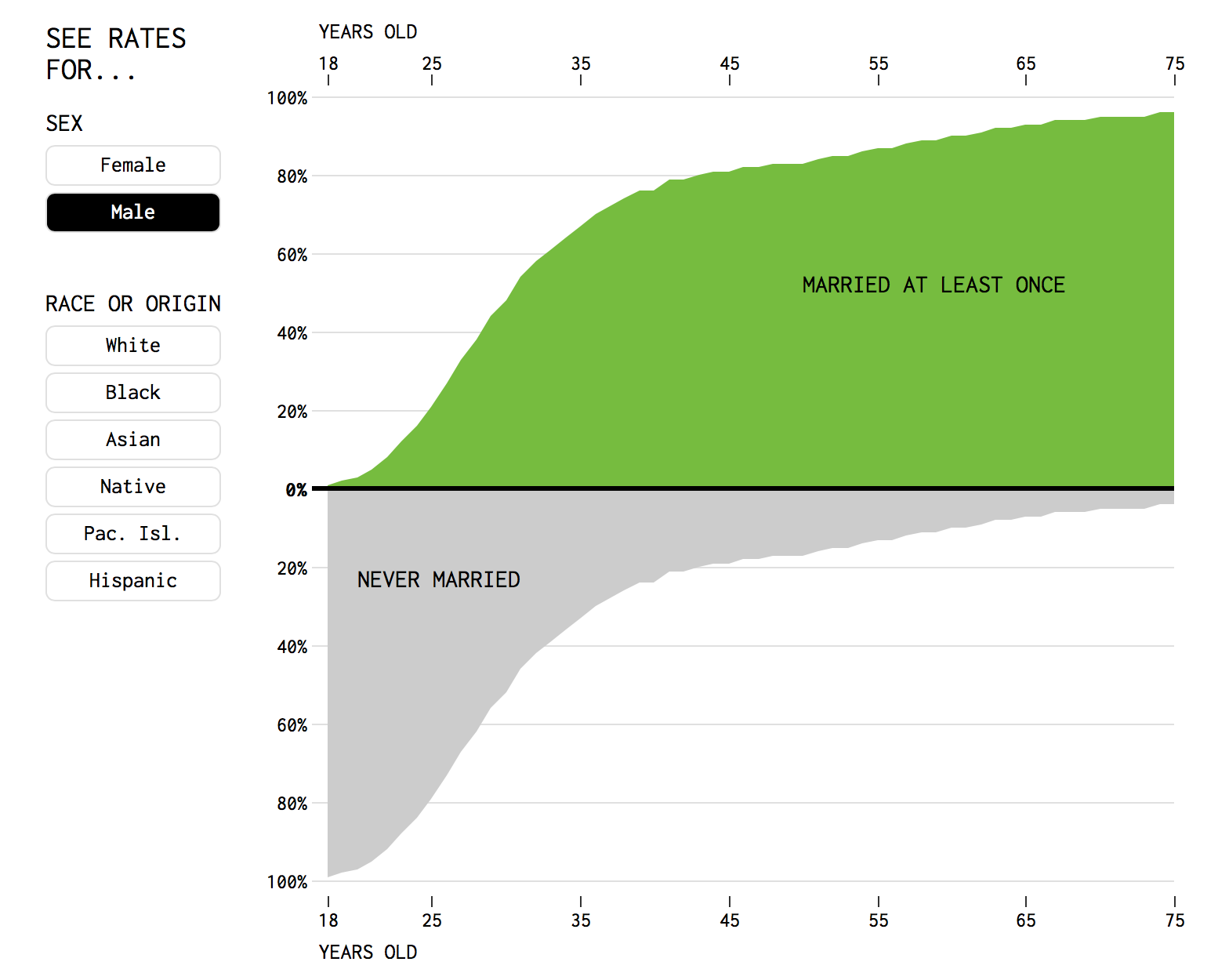

The Shrinking Pool: Analyzing Current Marriage Rates

According to data from the U.S. Census Bureau, the percentage of Americans who are married has been on a steady downward trajectory for several decades. In the 1960s, nearly 72% of American adults were married. Today, that number has dipped significantly, hovering closer to 50%. This shift is not merely a cultural curiosity; it is a financial phenomenon driven by changing economic priorities, the rising cost of living, and an increased emphasis on individual financial stability before commitment.

The Economic Barrier to Entry

For many younger Americans, the high cost of weddings is a significant entry barrier, but it is the long-term cost of living that keeps marriage rates low. As housing costs, student loan debt, and childcare expenses continue to climb, individuals are increasingly prioritizing their own debt repayment and personal savings before entering into a legal partnership. The financial pressure of merging assets and liabilities—especially when one party brings significant debt into the relationship—has led many to choose cohabitation without the legal strings of marriage.

The Impact of Education and Income

There is a clear correlation between education levels and marriage rates. Individuals with higher levels of education and stable, higher-income career paths are statistically more likely to get married and stay married. Conversely, those in lower-income brackets face greater financial instability, which often serves as a deterrent to marriage. When financial stress is a constant presence, the idea of adding a legal contract that complicates asset division can be viewed as a risk rather than an opportunity for wealth building.

The Financial Architecture of the Modern Household

Marriage, at its core, is a financial merger. When two individuals decide to combine their lives, they are essentially creating a new economic unit. This merger offers distinct advantages that have historically incentivized marriage, though these benefits are being reassessed in the current financial climate.

Economies of Scale and Tax Advantages

One of the most touted financial benefits of marriage is the concept of economies of scale. Two people living in one household can often share costs for rent, utilities, and groceries more efficiently than two people living apart. Furthermore, the tax code in the United States remains heavily skewed toward married couples. Filing taxes jointly can result in significant savings, particularly for couples where one partner earns significantly more than the other. These “marriage premiums” are often cited by financial planners as a reason to consider the institutional benefits of the union.

Social Security and Retirement Planning

Beyond immediate tax savings, marriage provides a safety net that is difficult to replicate with other forms of partnership. The ability to claim spousal Social Security benefits, the transferability of retirement accounts (such as 401(k)s and IRAs) without penalty upon death, and the access to employer-sponsored health insurance are all massive financial multipliers. For many, the decision to get married is, in part, an insurance policy for their golden years. When we look at the percentage of Americans opting out of marriage, we are also looking at a population that may face higher challenges in retirement planning, as they lose access to these specific legal and financial protections.

The Risk of Divorced Finances: A Costly Reality

The decline in marriage rates is not purely a result of changing values; it is also a rational response to the high financial risk associated with divorce. With divorce rates fluctuating near 40% to 50% for first marriages, the financial “break-up” costs can be catastrophic for personal net worth.

Asset Division and Legal Fees

The dissolution of a marriage is arguably one of the most expensive financial transactions a person can undergo. Beyond the obvious loss of shared economies of scale, the legal fees, the liquidation of retirement assets, and the potential for long-term alimony obligations can set an individual’s wealth-building efforts back by decades. Because of this, modern couples are increasingly looking for ways to protect their financial future, leading to the rise of the prenuptial agreement.

The Prenuptial Agreement as a Financial Tool

Once considered a tool only for the ultra-wealthy, the prenuptial agreement is becoming common practice for middle-class couples. It is a proactive step that allows parties to define the terms of a potential separation before the emotional toll of a divorce ever enters the picture. By clearly outlining how debts, assets, and properties will be managed, couples can treat the institution of marriage as a business arrangement, which may actually alleviate the anxiety associated with the financial stakes of matrimony.

Wealth Building and the “Marriage Effect”

Despite the risks of divorce, data consistently shows that, on average, married couples accumulate more wealth than their single counterparts. This is often referred to as the “marriage effect.” By pooling income and assets, couples can often invest more aggressively, pay off high-interest debt faster, and reach significant financial milestones—like homeownership—sooner than single individuals.

The Power of Dual Incomes

The most obvious driver of this wealth gap is the dual-income effect. Two incomes provide a buffer against job loss or market downturns. This stability allows for a higher risk tolerance in investment portfolios. For instance, a married couple can weather a period of unemployment for one spouse more easily than a single individual, allowing them to keep their long-term investments in the market and avoid panic selling during volatility.

Shared Financial Goals and Accountability

Financial success is rarely a solo endeavor. Research suggests that married couples are more likely to set long-term financial goals, such as saving for a home, college tuition, or retirement, and are more likely to hold each other accountable for reaching those goals. This “accountability partner” effect is a massive, albeit intangible, asset that contributes to the statistically higher net worth found in married households. Whether it is through regular budget discussions or the pressure to maintain a certain standard of living, marriage often forces a level of financial discipline that is harder to maintain in isolation.

The Future of Matrimony and Personal Finance

As we look toward the future, the percentage of Americans getting married will likely continue to shift as the definition of what constitutes a “family” evolves. We are seeing a rise in domestic partnerships and long-term cohabitation that mimics marriage in function but avoids the legal status. However, from a financial perspective, these arrangements often leave individuals exposed. Without the legal status of marriage, individuals lack the protections afforded by the law, leaving them vulnerable in the event of disability, death, or separation.

Closing the Gap

For those who choose not to marry, the financial burden is higher. They must take proactive steps to secure their future through estate planning, individual life insurance, and robust savings plans that don’t rely on a partner’s benefits. As the financial world becomes more complex, the decision to marry or remain single is increasingly becoming a calculation of risk, reward, and long-term security.

Ultimately, while the percentage of Americans getting married may be shrinking, the importance of the financial decisions surrounding these unions—or lack thereof—is growing. Whether you are walking down the aisle or choosing a different path, the key to financial health remains the same: transparency, clear communication, and a rigorous approach to protecting your assets. Marriage is a financial institution, and like any investment, it requires careful management to yield the best possible returns for your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.