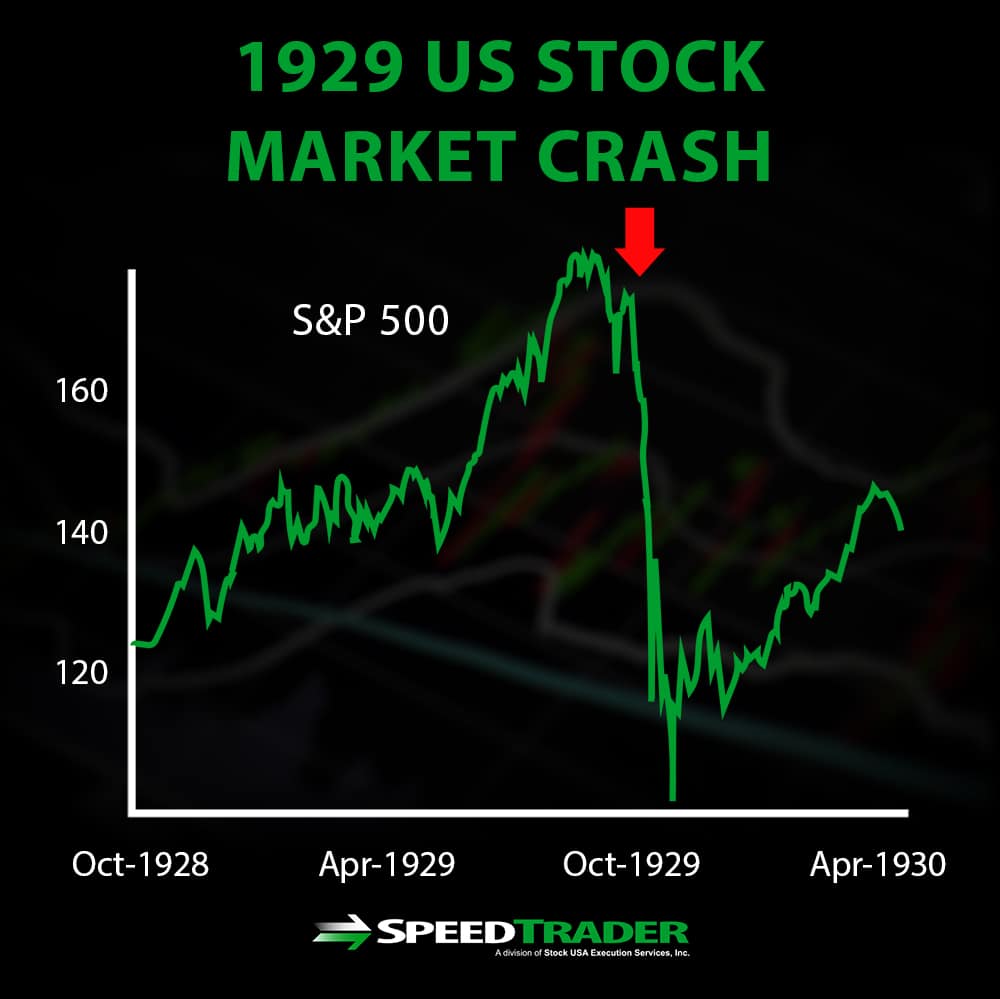

The phrase “stock market crash” conjures images of economic chaos, financial ruin, and widespread panic. While rare, the historical occurrences of such events – from the Great Depression’s Black Tuesday to the Dot-Com Bust and the 2008 Global Financial Crisis – serve as stark reminders of their potential for profound and lasting impact. Understanding what a stock market crash entails, its mechanisms, and its far-reaching consequences is crucial for investors, policymakers, and the general public alike. It’s not merely about numbers on a screen; it’s about the tangible effects on personal wealth, business stability, and the overall health of the global economy.

A stock market crash is typically defined by a sudden and dramatic decline in stock prices across a significant portion of the market, often characterized by a double-digit percentage drop in major indices like the S&P 500 or Dow Jones Industrial Average over a very short period (days or weeks). Unlike a market correction, which is a decline of 10-20% that typically resolves relatively quickly, a crash is more severe, often marking the onset of a bear market or a recession. Its origins can be manifold, including economic bubbles bursting, geopolitical crises, unexpected technological shifts, or a loss of confidence in financial systems. The critical question isn’t if one will happen again, but what the ramifications would be and how we might navigate such an turbulent period.

The Immediate Aftermath: Panic and Price Plunge

When the stock market crashes, the initial moments and days are characterized by intense volatility, a rapid erosion of value, and a palpable sense of fear that can quickly spread from institutional traders to individual investors. This is the stage where the theoretical risks of investing become brutally real.

Market Mechanics in Crisis

The speed and severity of a stock market crash are often amplified by modern trading mechanisms. Automated trading algorithms, designed to react to market conditions in milliseconds, can trigger massive sell-offs almost simultaneously, creating a cascade effect. To prevent total meltdown, exchanges employ “circuit breakers,” which are temporary trading halts designed to give investors a chance to pause, reassess, and cool down during extreme volatility. While intended to prevent panic-driven freefalls, these halts can also exacerbate anxiety when trading resumes, as pent-up selling pressure is released. Liquidity — the ease with which an asset can be bought or sold without affecting its price — can evaporate during a crash. Buyers disappear, and sellers are forced to unload assets at increasingly lower prices, further accelerating the decline. This ‘flight to safety’ often sees capital moving from equities to less risky assets like government bonds or gold, but even those markets can experience dislocations.

Investor Psychology and Behavioral Finance

At the heart of any market crash is human psychology. Fear, more potent than greed in driving market behavior during a crisis, can lead to irrational decisions. As prices fall, investors, fearing even greater losses, engage in “panic selling,” liquidating their holdings regardless of the underlying value of the assets. This herd mentality means that even fundamentally sound companies can see their stock prices plummet alongside struggling ones. Forced selling also plays a significant role. Investors who bought on margin (using borrowed money) receive margin calls when their investments decline. If they cannot provide additional collateral, their broker will forcibly sell their shares, adding to the selling pressure irrespective of the investor’s long-term conviction. The psychological toll extends beyond financial losses, impacting mental well-being and trust in the financial system.

Wealth Destruction and Portfolio Impact

The most immediate and tangible consequence of a stock market crash is the sheer destruction of wealth. For individual investors, retirement accounts like 401(k)s and IRAs, which are heavily invested in stocks, can see their values drastically reduced. Years of diligent saving can appear to vanish overnight, jeopardizing retirement plans, college savings, and other financial goals. This doesn’t just affect the wealthy; it impacts middle-class families whose financial security is tied to the performance of these investment vehicles. Institutional investors – pension funds, university endowments, mutual funds, and hedge funds – also suffer massive losses, which can ripple through the economy by affecting their ability to meet future obligations or invest in other ventures. The net effect is a significant reduction in collective purchasing power and capital available for future growth.

Ripples Through the Economy: Beyond Wall Street

While a stock market crash originates in the financial markets, its effects are rarely contained there. It acts as a powerful negative feedback loop, sending shockwaves through the real economy, affecting businesses, employment, and the daily lives of ordinary people.

Impact on Consumer Spending and Confidence

The “wealth effect” describes how changes in perceived wealth influence consumer behavior. When the stock market crashes, people feel poorer, even if their losses are only on paper. This leads to a sharp decline in consumer confidence and spending. Households become more cautious, delaying or canceling major purchases like cars, homes, or appliances. Discretionary spending on dining out, travel, and entertainment also plummets. Since consumer spending is a significant driver of economic activity in many developed nations, this reduction can quickly lead to a broader economic slowdown, or even a recession. Businesses, seeing reduced demand, respond by scaling back operations.

Business Investment and Employment

Companies, particularly those publicly traded, find it harder and more expensive to raise capital after a market crash. A lower stock price makes issuing new shares less attractive, and tighter credit conditions make borrowing more difficult and costly. With reduced access to financing and falling consumer demand, businesses scale back their expansion plans, cut investment in new projects, and often resort to hiring freezes or layoffs to reduce costs. Small businesses, which often have less access to diverse funding sources, are particularly vulnerable. The resulting increase in unemployment further dampens consumer spending and creates a vicious cycle of economic contraction.

Banking System and Credit Markets

A stock market crash can place immense strain on the banking system and credit markets. Banks and other financial institutions often hold significant investments in stocks or have lent money to businesses and individuals whose assets are now depreciating. A widespread decline in asset values can lead to an increase in loan defaults, as borrowers find it harder to service their debts. This can weaken banks’ balance sheets, making them more reluctant to lend, leading to a “credit crunch.” If banks become too distressed, it can trigger systemic risk – a cascading failure across the financial system, as seen during the 2008 crisis. The interbank lending market, where banks lend to each other, can seize up, paralyzing the flow of capital essential for economic activity.

Global Contagion

In today’s interconnected global economy, a significant stock market crash in one major financial center rarely stays isolated. Global investors hold diversified portfolios across different countries, and financial institutions have cross-border exposures. A crash in the U.S. market, for example, can trigger immediate declines in European and Asian markets as investors pull capital globally. Supply chains are international, and a downturn in demand in one major economy affects producers worldwide. Furthermore, a severe crash can lead to a “flight to safety” towards perceived stable currencies (like the U.S. dollar), causing currency volatility and creating additional economic stress for nations whose currencies weaken against the dollar, especially those with dollar-denominated debt.

Government and Central Bank Responses

When a stock market crash threatens to spiral into a full-blown economic crisis, governments and central banks typically step in with a range of powerful interventions aimed at stabilizing markets, restoring confidence, and stimulating economic recovery.

Monetary Policy Interventions

Central banks, such as the Federal Reserve in the U.S., are typically the first responders. Their primary tools include interest rate adjustments, quantitative easing (QE), and liquidity injections. Interest rate cuts are used to make borrowing cheaper, encouraging businesses to invest and consumers to spend. In a severe crash, rates can be slashed to near zero. Quantitative easing involves the central bank buying large quantities of government bonds and other securities to inject liquidity directly into the financial system, lower long-term interest rates, and encourage lending. Liquidity injections are direct infusions of cash into banks to ensure they have enough reserves to meet their obligations and continue lending. These measures aim to prevent a credit crunch and keep the wheels of finance turning.

Fiscal Policy Measures

Governments complement monetary policy with fiscal policy measures. These often involve large-scale stimulus packages, which can include increased government spending on infrastructure projects, direct payments to citizens, or tax cuts designed to boost consumer demand and business investment. Unemployment benefits are often expanded to provide a safety net for those who lose their jobs, helping to mitigate the decline in consumer spending. Bailouts of critical industries or financial institutions deemed “too big to fail” are also possible, aimed at preventing systemic collapse and protecting jobs. These fiscal interventions are often hotly debated but are seen as necessary to prevent a prolonged and deep recession.

Regulatory Changes and Reforms

Following a major crash, there is often a period of introspection and regulatory reform. Governments and regulatory bodies review the causes of the crash and implement new rules and safeguards to prevent future occurrences. This can include stricter oversight of financial institutions, reforms to trading practices (like circuit breaker modifications), increased capital requirements for banks, and enhanced investor protection measures. The aim is to build a more resilient financial system, reduce systemic risk, and restore public trust, though the effectiveness and scope of these reforms can vary significantly.

Preparing for the Unthinkable: Investor Strategies

While the prospect of a stock market crash can be daunting, investors are not powerless. Prudent financial planning and adherence to sound investment principles can significantly mitigate the impact and even present opportunities.

Diversification and Asset Allocation

The cornerstone of crash preparedness is diversification. Spreading investments across different asset classes – stocks, bonds, real estate, commodities, and cash – ensures that a downturn in one area doesn’t wipe out your entire portfolio. When stocks plummet, bonds often perform relatively well, acting as a cushion. Within equities, diversifying across different industries, geographies, and company sizes (large-cap, small-cap) can also reduce risk. Proper asset allocation, tailored to your risk tolerance, time horizon, and financial goals, is crucial. A younger investor with a long time horizon might have a higher allocation to stocks, while someone nearing retirement might favor a more conservative, bond-heavy portfolio.

Maintaining an Emergency Fund

One of the most critical personal finance measures is to have an adequate emergency fund – typically 3 to 6 months’ worth of living expenses – held in an easily accessible, liquid account like a savings account. This cash reserve provides a vital buffer during economic downturns, allowing you to cover unexpected expenses or job loss without having to sell investments at depressed prices. During a market crash, having cash on hand prevents forced selling and provides peace of mind, allowing you to ride out the volatility.

Long-Term Perspective and Avoiding Panic Selling

Market crashes are often temporary setbacks within a long-term upward trend for equity markets. Historically, markets have always recovered from every crash and gone on to reach new highs. Investors with a long-term perspective understand that short-term volatility is normal and resist the urge to panic sell. Selling during a crash crystallizes losses and prevents participation in the eventual recovery. Instead, sticking to an investment plan, continuing to contribute regularly (e.g., through dollar-cost averaging), and focusing on the underlying quality of your investments can be a more effective strategy.

Rebalancing and Opportunity

While crashes bring fear, they also present opportunities for disciplined investors. When the market falls, quality assets go “on sale.” For investors with available cash and a long-term outlook, a crash can be an opportune time to buy fundamentally strong companies at significantly reduced prices. Rebalancing your portfolio – selling some assets that have performed well and buying more of those that have underperformed – can also be a savvy move during a downturn. This strategy helps maintain your desired asset allocation and allows you to capitalize on undervalued assets, positioning your portfolio for strong returns during the inevitable recovery.

In conclusion, a stock market crash is far more than a financial headline; it’s a profound economic event with intricate causes and widespread consequences that touch every facet of our financial lives. From the immediate investor panic and wealth destruction to the ripple effects on consumer spending, business stability, and global trade, its reach is extensive. However, the history of finance also teaches us that such crises, while devastating, are often followed by recovery, spurred by coordinated actions from central banks and governments. For individual investors, preparedness through diversification, an emergency fund, and a steadfast long-term perspective, coupled with the ability to identify opportunities amid the turmoil, remains the most robust defense against the “unthinkable” and the pathway to financial resilience.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.