Securing a business loan is often a critical step for entrepreneurs looking to start, grow, or sustain their ventures. Whether you’re aiming to expand operations, purchase new equipment, boost working capital, or simply bridge a temporary cash flow gap, understanding the intricacies of the loan application process is paramount. This guide will demystify the journey, providing a professional, insightful, and engaging roadmap for navigating the world of business finance. By meticulously preparing and strategically approaching lenders, you can significantly enhance your chances of securing the funding necessary to achieve your business aspirations.

Understanding Business Loans: Types and Eligibility

Before embarking on the application process, it’s crucial to grasp what business loans entail, the various forms they take, and the fundamental criteria lenders use to assess potential borrowers. This foundational knowledge will help you identify the most suitable financing option for your specific needs.

What is a Business Loan?

At its core, a business loan is a sum of money lent to a business by a financial institution or individual, which the business is expected to repay with interest over a predetermined period. These loans serve as external capital, providing businesses with the financial leverage to undertake projects or operations that their current cash flow might not support. Unlike equity financing, where investors receive a share of ownership, a business loan is a debt obligation, meaning the lender does not gain ownership in the company. The specific terms, interest rates, and repayment schedules vary widely depending on the type of loan, the lender, and the borrower’s creditworthiness.

Common Types of Business Loans

The landscape of business financing is diverse, offering a multitude of loan products designed to cater to different business sizes, stages, and needs. Understanding these options is key to selecting the right one:

- SBA Loans (Small Business Administration Loans): These are government-backed loans, partially guaranteed by the SBA, which reduces the risk for lenders. This makes it easier for small businesses to qualify for loans with favorable terms, lower down payments, and longer repayment periods. SBA loans are not direct loans from the government but rather facilitated through partner lenders.

- Term Loans: Perhaps the most straightforward type, a term loan provides a lump sum of capital that is repaid over a fixed period (the “term”) with regular, often monthly, payments. These can be short-term (1-3 years) or long-term (3-10+ years) and are typically used for significant investments like equipment purchases, facility expansion, or major inventory buys.

- Lines of Credit: Similar to a credit card, a business line of credit offers access to a flexible pool of funds up to a certain limit. Businesses can draw funds as needed, repay them, and then draw again, paying interest only on the amount borrowed. This is ideal for managing working capital, covering seasonal fluctuations, or addressing unexpected expenses.

- Equipment Loans: Specifically designed to finance the purchase of machinery, vehicles, or other business equipment, these loans often use the purchased equipment itself as collateral. This can make them easier to obtain for businesses that might not have other assets to pledge.

- Invoice Factoring (Accounts Receivable Financing): Rather than a traditional loan, invoice factoring involves selling your unpaid invoices (accounts receivable) to a third-party factor at a discount. The factor then collects the payment directly from your customers. This provides immediate cash flow but can be more expensive than other options.

- Merchant Cash Advance (MCA): An MCA provides an upfront lump sum in exchange for a percentage of future credit card sales. While quick to obtain and often requiring less stringent credit checks, MCAs typically come with very high effective interest rates and can be difficult to manage for businesses with fluctuating sales.

- Commercial Real Estate Loans: Used to purchase or refinance property for business use, these are long-term loans, often with large principal amounts, tailored for commercial properties.

- Startup Loans: Specifically designed for new businesses with little or no operating history, these can be harder to obtain and often require a strong business plan, personal guarantees, and sometimes crowdfunding or angel investment in conjunction with traditional loans.

Key Eligibility Criteria for Borrowers

Lenders evaluate several factors to assess a borrower’s ability to repay a loan. While specific criteria vary by lender and loan type, common elements include:

- Credit Score (Personal and Business): A strong personal credit score (typically FICO 680+) is often required, especially for newer businesses. Established businesses will also have a business credit score, which lenders heavily scrutinize.

- Time in Business: Most traditional lenders prefer businesses that have been operating for at least 2-3 years, as this demonstrates stability and a track record. Newer businesses might need to seek alternative lenders or startup-specific financing.

- Annual Revenue: Lenders want to see consistent revenue to ensure the business can generate sufficient cash flow to cover loan repayments. Minimum revenue requirements vary significantly.

- Profitability: While revenue is important, profitability indicates a healthy business that can sustain itself and service debt without strain.

- Debt-to-Income Ratio (Personal) / Debt Service Coverage Ratio (Business): Lenders assess how much existing debt you or your business already carry relative to income or cash flow. A low debt burden is favorable.

- Collateral: For secured loans, lenders require assets (like real estate, equipment, or accounts receivable) that can be seized if the borrower defaults.

- Industry and Business Type: Some industries are perceived as higher risk than others, which can influence loan availability and terms.

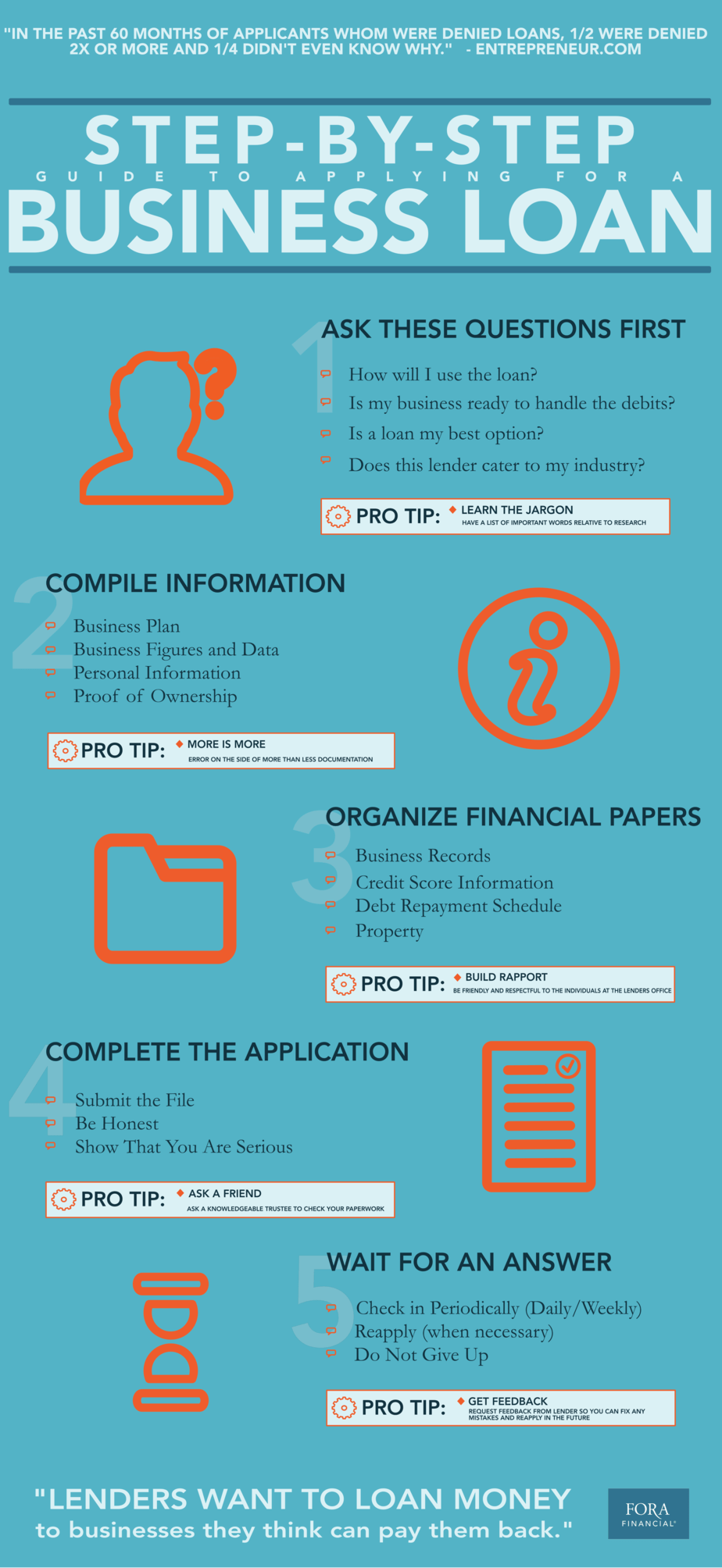

Preparing Your Application: Essential Documents and Information

The cornerstone of a successful loan application is thorough preparation. Lenders require a comprehensive understanding of your business’s financial health, operational strategy, and future potential. Assembling the necessary documentation meticulously will not only streamline the process but also present your business in the most favorable light.

Business Plan: Your Blueprint for Success

A well-crafted business plan is more than just a formality; it’s a strategic roadmap that articulates your vision, mission, and how you intend to achieve financial success. For lenders, it demonstrates your understanding of the market, your competitive advantages, and your ability to execute. Key components include:

- Executive Summary: A concise overview of your business, its products/services, market opportunity, and financial projections.

- Company Description: Legal structure, history, and mission statement.

- Products and Services: Detailed description of what you offer and their unique selling propositions.

- Market Analysis: Industry overview, target market, customer segments, and competitive landscape.

- Marketing and Sales Strategy: How you plan to reach customers and generate revenue.

- Management Team: Resumes and experience of key personnel, highlighting their expertise.

- Financial Projections: Detailed forecasts of income, expenses, and cash flow (usually for 3-5 years), demonstrating how the loan will impact profitability and repayment capacity.

- Funding Request: A clear articulation of the loan amount requested, how it will be used, and the anticipated impact on the business.

Financial Statements

These documents provide a historical and projected snapshot of your business’s financial health. Lenders rely heavily on them to assess your ability to manage finances and repay debt.

- Profit & Loss Statement (Income Statement): Shows your revenues, costs, and profits (or losses) over a specific period (e.g., quarterly, annually). Lenders typically request statements for the past 2-3 years.

- Balance Sheet: A snapshot of your business’s assets, liabilities, and owner’s equity at a specific point in time. It provides insight into your financial stability and net worth.

- Cash Flow Statement: Tracks the movement of cash into and out of your business over a period, detailing operating, investing, and financing activities. This is crucial for demonstrating your ability to generate cash to cover loan payments.

- Pro Forma Financial Projections: Forward-looking statements (P&L, Balance Sheet, Cash Flow) for the next 3-5 years, often incorporating the impact of the requested loan.

Personal Financial Information

Especially for small businesses or startups, the owner’s personal financial health is often intertwined with the business’s perceived creditworthiness.

- Personal Credit Score and Report: Lenders will pull your personal credit report to assess your history of managing personal debt. A good score signifies financial responsibility.

- Personal Bank Statements: For the past 6-12 months, demonstrating personal income and expenditure patterns.

- Personal Tax Returns: Copies of federal income tax returns for the past 2-3 years, verifying personal income and financial obligations.

- Statement of Personal Assets and Liabilities: A comprehensive list of your personal holdings (real estate, investments, savings) and debts (mortgages, car loans, credit cards).

Legal Documents

These verify the legitimacy and legal standing of your business.

- Business Registration Documents: Articles of Incorporation or Organization, LLC operating agreement, partnership agreement, or sole proprietorship registration.

- Business Licenses and Permits: Proof that your business is legally authorized to operate in its industry and location.

- Employer Identification Number (EIN): Your business’s unique tax ID from the IRS.

- Commercial Leases: If applicable, demonstrating your business premises.

- Contracts and Agreements: Any significant vendor or customer contracts that demonstrate revenue streams or operational stability.

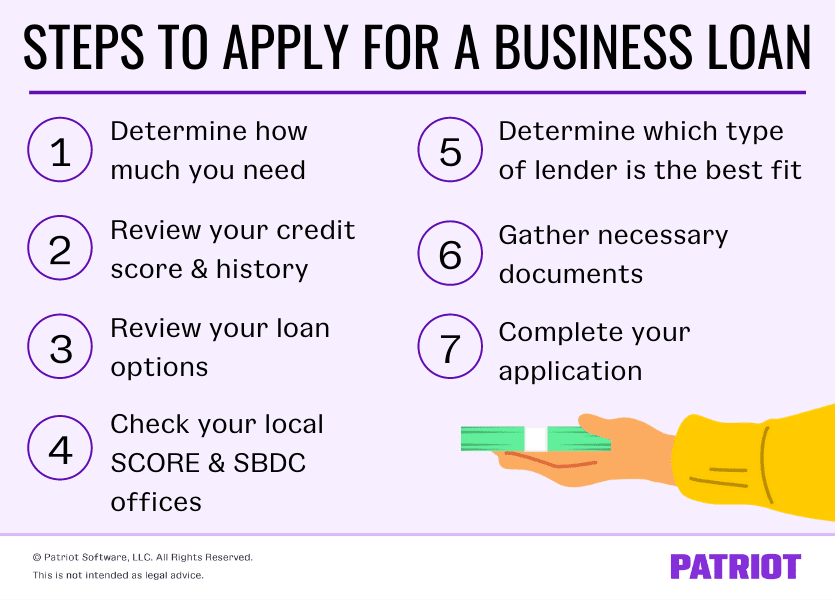

Navigating the Application Process: Step-by-Step

With your documents in order, you’re ready to tackle the application itself. This process involves strategic decision-making, careful completion of forms, and diligent follow-up.

Assess Your Funding Needs and Loan Purpose

Before approaching any lender, clearly define why you need the loan and how much you need. Over-borrowing leads to unnecessary interest payments, while under-borrowing can leave you short of funds. Create a detailed breakdown of how the loan funds will be utilized (e.g., equipment purchase, inventory, marketing campaign, working capital buffer). This clarity will not only guide your loan search but also impress potential lenders.

Research Lenders and Loan Options

Different lenders specialize in different types of loans and cater to various business profiles.

- Traditional Banks: Often offer the lowest interest rates and most favorable terms for established businesses with strong credit. However, their application processes can be lengthy and stringent.

- Credit Unions: Similar to banks but member-owned, sometimes offering more personalized service and slightly more flexible terms for small businesses.

- Online Lenders: Known for faster application and funding processes, and often more lenient criteria, making them suitable for businesses that might not qualify for traditional bank loans or need funds quickly. However, interest rates can be higher.

- SBA-Approved Lenders: Banks and credit unions that partner with the Small Business Administration to offer SBA-guaranteed loans.

- Community Development Financial Institutions (CDFIs): Non-profit organizations focused on providing affordable financial services to underserved communities and small businesses, often offering specialized programs.

Compare interest rates, repayment terms, fees, collateral requirements, and eligibility criteria across various lenders and loan types. Don’t be afraid to solicit quotes from multiple sources.

Prepare Your Loan Application Package

Once you’ve identified a suitable lender and loan product, organize all your compiled documents into a comprehensive application package. Ensure everything is up-to-date, accurate, and easy to review. A well-organized submission reflects professionalism and attention to detail. Double-check all forms for completeness and accuracy to avoid delays.

Submit Your Application

Most lenders now offer online application portals, which can speed up the initial submission. Some may still prefer in-person meetings or mailed documentation. Follow the lender’s specific instructions for submission. Once submitted, acknowledge that this is often just the beginning of a dialogue.

Due Diligence and Underwriting

After submission, the lender’s underwriting team will meticulously review your application and supporting documents. They will verify all information, assess risks, and confirm your ability to repay. This phase may involve:

- Requests for Additional Information: Be prepared to promptly provide any further details or documents the lender asks for.

- Interviews: You might be required to meet with loan officers to discuss your business plan, financial projections, and overall strategy.

- Site Visits: For larger loans, the lender might conduct a physical visit to your business premises.

- Credit Checks: Lenders will run both personal and business credit checks.

This stage requires patience and responsiveness. Timely and accurate responses can significantly expedite the process.

Loan Approval and Funding

If your application is approved, you will receive a loan offer outlining the terms, interest rate, repayment schedule, fees, and any covenants (conditions you must meet, such as maintaining certain financial ratios). Carefully review this offer, ideally with legal counsel, before signing. Once the agreement is signed, the funds will be disbursed to your business account. The timing of funding can range from a few days for online lenders to several weeks or even months for traditional banks and SBA loans.

Key Factors for Loan Approval and Success

While a thorough application is vital, several underlying factors heavily influence a lender’s decision. Understanding and strengthening these areas can significantly improve your chances of approval.

Strong Creditworthiness (Personal & Business)

Lenders view credit history as a strong indicator of future repayment behavior.

- Personal Credit Score: A high personal FICO score (typically 680+ for traditional lenders, 720+ for the best rates) demonstrates responsible financial management. Pay bills on time, keep credit utilization low, and review your credit report for errors regularly.

- Business Credit Score: Establish a separate business credit profile by registering your business, getting a DUNS number, and ensuring suppliers report your payment history to business credit bureaus (e.g., Dun & Bradstreet, Experian Business, Equifax Business).

Demonstrating Repayment Capacity

This is arguably the most critical factor. Lenders need assurance that your business generates enough cash flow to comfortably cover loan payments in addition to operational expenses.

- Profitability: Consistent profitability indicates a healthy business model.

- Cash Flow: Positive and predictable cash flow is paramount. Lenders will analyze your cash flow statements and projections to ensure you have a comfortable buffer.

- Debt Service Coverage Ratio (DSCR): This metric compares your business’s net operating income to its total debt obligations. A DSCR of 1.25 or higher is often preferred, meaning your income is 1.25 times greater than your debt payments.

Collateral and Guarantees

For many business loans, especially traditional ones, lenders require some form of security.

- Collateral: Assets pledged by the borrower that the lender can seize if the loan defaults (e.g., real estate, equipment, inventory, accounts receivable). The value of the collateral should ideally cover the loan amount.

- Personal Guarantee: For small businesses, owners are often required to personally guarantee the loan. This means you are personally liable for the debt if the business cannot repay it, putting your personal assets at risk. Understand the implications of a personal guarantee before signing.

A Clear and Compelling Business Case

Beyond numbers, lenders want to understand the story behind your business and the rationale for the loan.

- Viable Business Model: Does your business operate in a sustainable market with a clear competitive advantage?

- Market Opportunity: Is there a demonstrable demand for your products or services?

- Management Expertise: Does your team have the experience and skills to execute your business plan and manage the new debt effectively?

- Clear Loan Purpose: Precisely articulate how the loan funds will be used and how this investment will contribute to the business’s growth and ability to repay the debt. Show a clear return on investment.

Post-Approval: Managing Your Business Loan Wisely

Receiving loan approval is a significant milestone, but it’s just the beginning. Responsible management of your new debt is essential for long-term financial health and future access to capital.

Understanding Loan Terms and Covenants

Before the funds hit your account, meticulously review every clause of your loan agreement.

- Interest Rate and Fees: Confirm the exact interest rate (fixed or variable), annual percentage rate (APR), and all associated fees (origination, closing, late payment, prepayment penalties).

- Repayment Schedule: Understand the frequency and amount of payments.

- Covenants: Be aware of any specific conditions or promises you’ve made to the lender. These can include maintaining certain financial ratios, providing regular financial statements, restricting further debt, or avoiding significant changes in ownership. Violating covenants can lead to default, even if payments are current.

- Default Provisions: Understand what constitutes a default and the lender’s rights in such an event.

Responsible Fund Utilization

Stick to the purpose outlined in your loan application. Using funds for unapproved purposes can violate your loan agreement and hinder your business’s ability to achieve the intended growth, making repayment more challenging. Track how the funds are spent and ensure they are deployed efficiently to generate the expected return.

Maintaining Good Financial Health

Your relationship with the lender is ongoing. Continue to manage your finances meticulously:

- Consistent Payments: Always make loan payments on time to avoid penalties, maintain a good credit history, and avoid defaulting. Set up automatic payments if possible.

- Monitor Cash Flow: Continuously track your business’s cash inflows and outflows to ensure you always have enough liquidity to cover operating expenses and debt service.

- Regular Financial Reporting: If required by your loan covenants, consistently provide accurate and timely financial statements to your lender.

- Budget Adherence: Operate within your budget, especially concerning the projects or investments funded by the loan.

Building Lender Relationships

A positive relationship with your lender can be invaluable.

- Communicate Proactively: If you anticipate any financial difficulties that might affect your ability to make payments, communicate with your lender before you miss a payment. Lenders are often more willing to work with proactive borrowers to restructure terms or offer temporary relief than to deal with a sudden default.

- Be Transparent: Maintain an open and honest dialogue.

- Future Needs: A strong track record of responsible borrowing and repayment builds trust, making it easier to secure additional financing from the same lender in the future, often with more favorable terms.

Conclusion: Empowering Your Business Growth

Applying for a business loan is a significant undertaking that requires careful planning, meticulous preparation, and a deep understanding of financial principles. By thoroughly assessing your needs, preparing a robust application, strategically choosing a lender, and responsibly managing your debt post-approval, you position your business for sustainable growth. While the process can seem daunting, viewing it as a strategic exercise in financial stewardship will not only secure the capital you need but also strengthen your business’s foundation for future success in the dynamic world of entrepreneurship. With the right approach, a business loan can be a powerful catalyst, transforming your vision into a thriving reality.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.