Credit cards are ubiquitous tools in modern finance, offering convenience, purchasing power, and the potential to build a credit history. However, the simple act of swiping, tapping, or entering your card details often comes with a hidden layer of costs – the “charges” of credit cards. Beyond the immediate transaction, a credit card issuer levies various fees and interest rates that can significantly impact your financial well-being. Understanding these charges is paramount for responsible credit card usage, enabling you to maximize benefits and minimize unnecessary expenses. This exploration delves into the multifaceted world of credit card charges, drawing insights from the intersection of technology, smart branding, and sound personal finance.

The Foundation of Credit Card Charges: Interest and Annual Fees

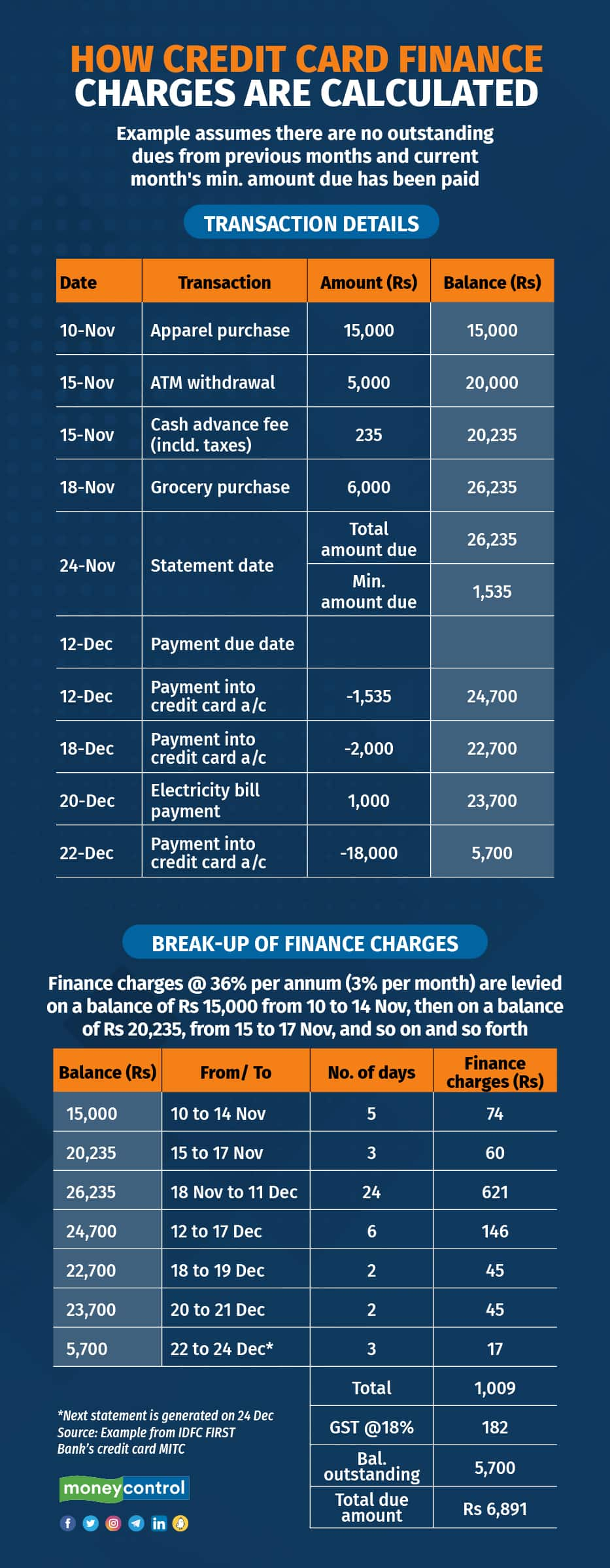

At the heart of most credit card charges lies the concept of interest. When you carry a balance on your credit card – meaning you don’t pay off your entire statement balance by the due date – you’ll be charged interest on the outstanding amount. This is how credit card companies make a substantial portion of their profit.

Understanding Interest Rates: APR and Its Nuances

The primary metric for credit card interest is the Annual Percentage Rate (APR). This figure represents the yearly cost of borrowing money on your credit card. However, it’s crucial to understand that APR is not simply applied once a year. Instead, it’s typically converted into a periodic rate (usually a daily rate) and applied to your balance each billing cycle.

- Purchase APR: This is the most common APR and applies to purchases you make with your credit card. If you carry a balance, this rate will be applied to those purchases.

- Balance Transfer APR: If you transfer a balance from another credit card to this one, a specific APR will apply. Often, balance transfer APRs are introductory and can increase after a promotional period.

- Cash Advance APR: Taking out cash using your credit card (a cash advance) usually incurs a much higher APR than your regular purchase APR. Furthermore, interest on cash advances typically begins accruing immediately, with no grace period.

- Penalty APR: If you miss payments or violate the terms of your cardholder agreement (e.g., by exceeding your credit limit), your credit card issuer can impose a penalty APR. This rate is often significantly higher and can remain in effect for an extended period.

The APR on your credit card is influenced by several factors, including your creditworthiness at the time of application, the prevailing economic conditions, and the specific terms offered by the issuer. Technology plays a role here, with sophisticated algorithms used by lenders to assess risk and set interest rates. The “tech” behind credit scoring and personalized offers allows for dynamic APRs.

The Annual Fee: A Trade-Off for Perks

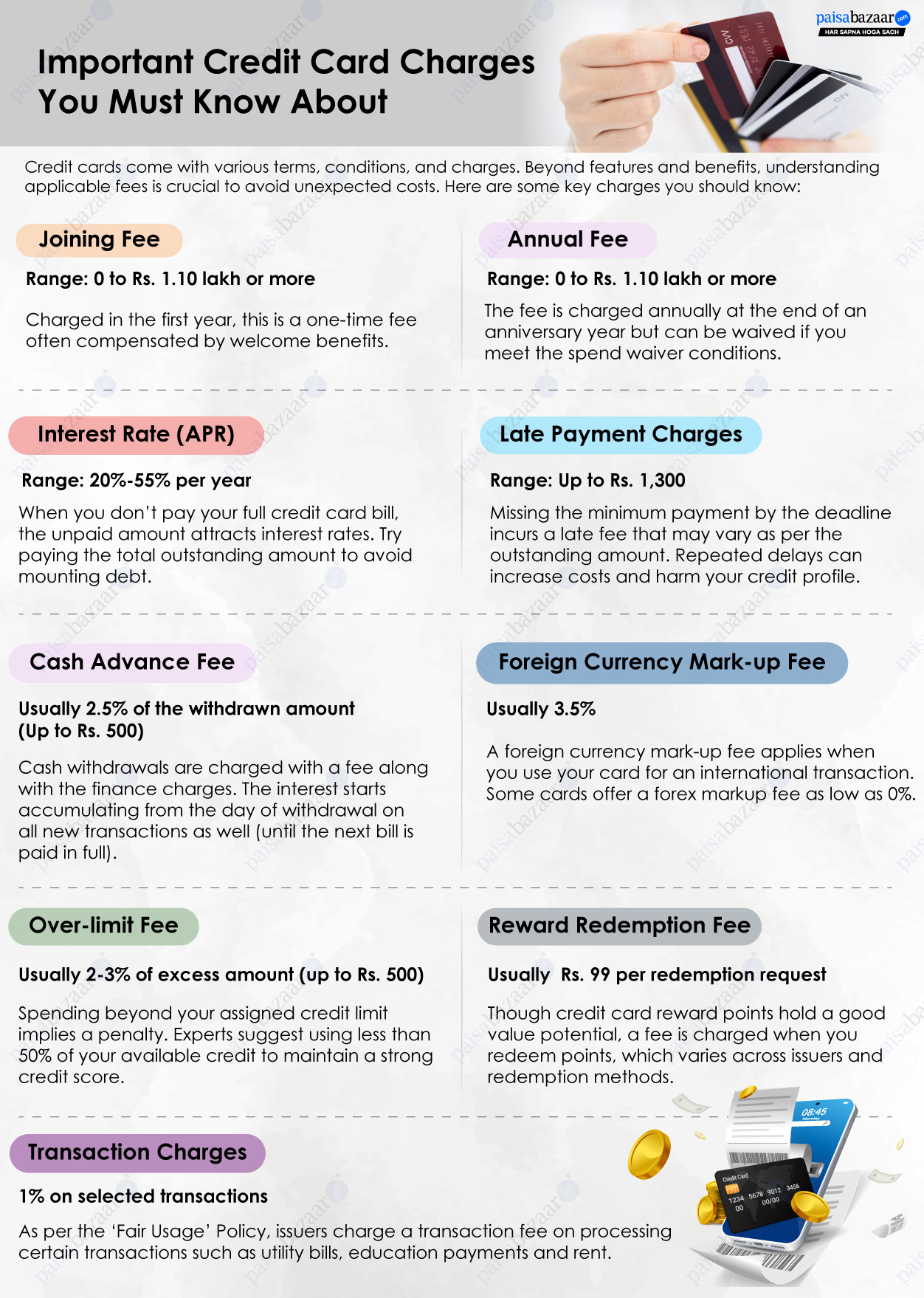

Many credit cards, especially those offering premium rewards or benefits, come with an annual fee. This is a fixed charge levied once a year for the privilege of holding the card. The decision of whether an annual fee is “worth it” is a cornerstone of personal finance strategy and depends heavily on how you utilize the card’s benefits.

- Rewards Cards: Premium travel, cashback, or lifestyle rewards cards often have annual fees. The idea is that the value of the rewards you earn (e.g., free flights, hotel stays, significant cashback) should outweigh the annual fee. Smart branding by credit card companies emphasizes these aspirational rewards to justify the fee.

- Low-Interest Cards: Some cards with competitive low APRs might also come with an annual fee, though this is less common for basic cards.

- Secured Credit Cards: Cards designed for individuals with poor or no credit history often have annual fees, which can contribute to the lower credit line or security deposit required.

The “brand” of a credit card often dictates its fee structure. High-end travel cards from established brands will likely command higher annual fees than basic cashback cards. Understanding the brand’s promise and aligning it with your spending habits is crucial.

Navigating the Labyrinth of Other Credit Card Charges

Beyond interest and annual fees, credit card companies have devised a range of other charges that can catch the unwary consumer. These fees are often tied to specific actions or circumstances related to your account.

Fees for Account Management and Actions

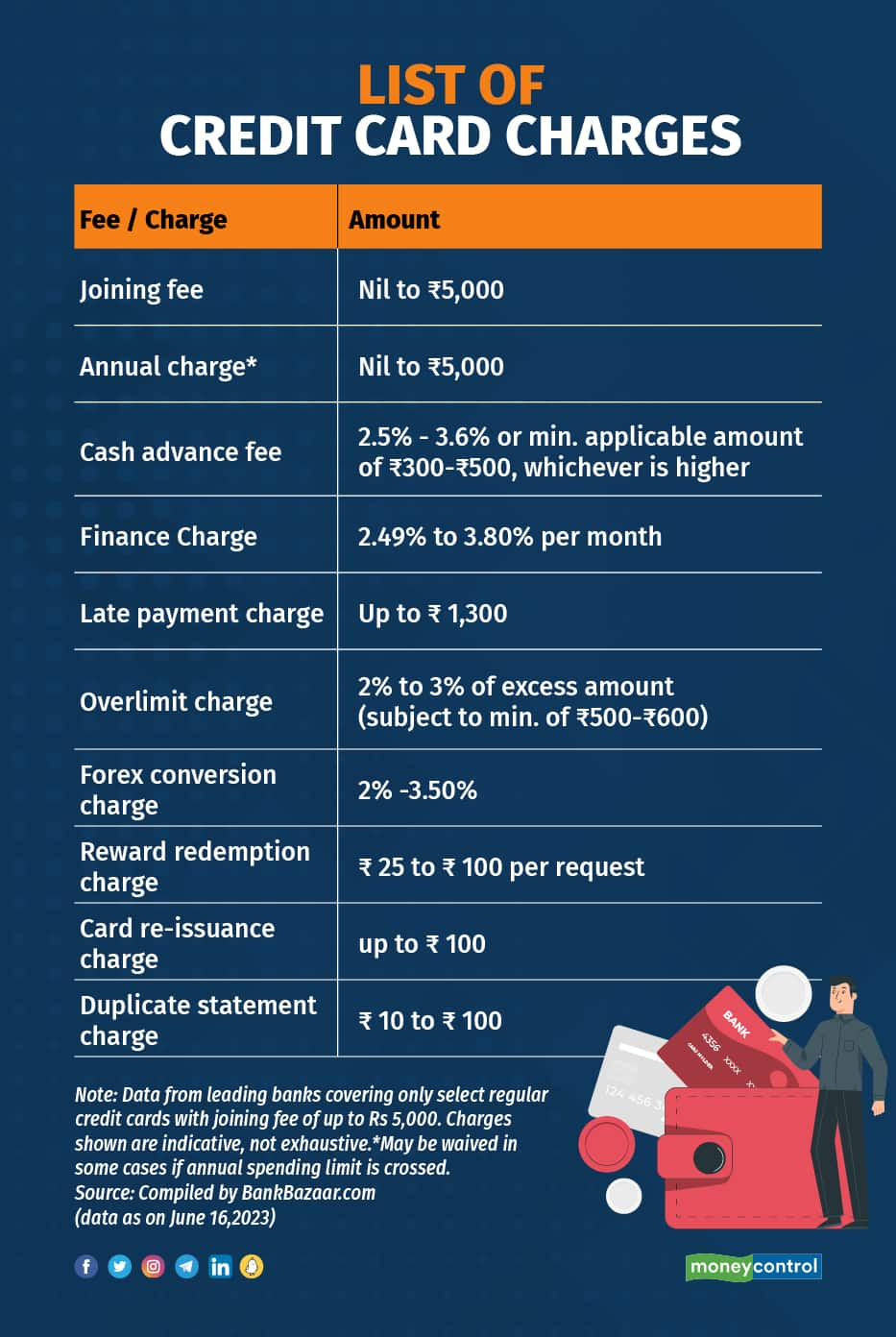

- Late Payment Fee: This is one of the most common and easily avoidable fees. If you fail to make at least the minimum payment by the due date, you’ll be charged a late fee. This fee can be a flat amount or a percentage of your outstanding balance, up to a certain limit. Missing payments also negatively impacts your credit score, a critical aspect of your “personal finance” journey.

- Over-Limit Fee: While less common now due to regulatory changes, some cards may still charge a fee if your balance exceeds your credit limit. Many issuers now require you to opt-in to allow transactions that would put you over your limit, but if you do, a fee may apply.

- Returned Payment Fee: If a payment you make to your credit card company is returned (e.g., due to insufficient funds in your bank account), you’ll likely incur a returned payment fee.

- Foreign Transaction Fee: If you use your credit card for purchases in a foreign currency or with a merchant located outside your home country, you might be charged a foreign transaction fee. This is often a percentage of the transaction amount. For frequent travelers, choosing a card with no foreign transaction fees is a smart “money” strategy.

Fees Associated with Accessing Funds and Services

- Balance Transfer Fee: As mentioned earlier, while balance transfer APRs can be attractive, there’s typically a fee for initiating the transfer. This fee is usually a percentage of the amount transferred, often with a minimum charge.

- Cash Advance Fee: In addition to the high APR, you’ll usually pay a fee for each cash advance you take. This fee is often a percentage of the amount withdrawn.

- Express Delivery Fee: If you need a replacement card urgently, some issuers may charge a fee for express shipping.

- Paper Statement Fee: In an effort to go “green” and reduce administrative costs, some card issuers might charge a fee for requesting paper statements instead of electronic ones.

The “tech” advancements in online banking and app development have made managing your credit card easier, but it’s still your responsibility to be aware of these potential charges. Many credit card apps provide alerts for upcoming due dates, helping you avoid late fees.

Strategies for Minimizing Credit Card Charges

Being informed about credit card charges is the first step; the next is implementing strategies to minimize them. This involves a blend of financial discipline, smart product selection, and leveraging available “financial tools.”

Mastering Your Payments and Balances

- Pay in Full and On Time: The most effective way to avoid interest charges is to pay your entire statement balance by the due date each month. This also prevents late fees and keeps your credit utilization low, positively impacting your credit score.

- Set Up Auto-Pay: For those prone to forgetting due dates, setting up automatic minimum payments can at least prevent late fees. However, it’s still advisable to review your statement and pay the full balance manually or adjust auto-pay to cover the full amount.

- Avoid Cash Advances: Unless it’s an absolute emergency, steer clear of cash advances. The fees and immediate interest accrual make them an expensive way to access cash.

- Be Mindful of Your Credit Limit: Monitor your spending to avoid exceeding your credit limit, which can trigger over-limit fees and damage your credit score.

Choosing the Right Credit Card for Your Needs

- Align Rewards with Spending: If you travel frequently, a travel rewards card with no foreign transaction fees and valuable travel perks might justify its annual fee. If you primarily spend on groceries and gas, a cashback card focused on these categories could be more beneficial. This is where “brand” strategy meets personal utility.

- Compare APRs and Fees: When applying for a new card, meticulously compare the APRs, annual fees, and other charges. For those looking to consolidate debt, a balance transfer card with a low introductory APR and reasonable transfer fee is key.

- Consider Secured Credit Cards Wisely: If you need to build or rebuild credit, secured credit cards can be a good option, but be sure to understand their fees and interest rates, as they can sometimes be higher than standard unsecured cards.

Leveraging Technology and Financial Tools

- Credit Card Comparison Websites: Numerous online platforms utilize “tech” to aggregate and compare credit card offers, helping you find the best options based on your credit profile and spending habits.

- Budgeting Apps: Personal finance apps can help you track your spending, set budgets, and visualize where your money is going, making it easier to manage your credit card payments and avoid overspending.

- Credit Monitoring Services: While not directly reducing charges, these services, often integrated into banking apps or offered by third parties, can alert you to changes in your credit report, which could indicate fraudulent activity or missed payments that might lead to fees.

- Issuer Apps and Online Portals: Utilize the tools provided by your credit card issuer. Most offer mobile apps and online portals where you can view your statements, make payments, set up alerts, and track your spending in real-time.

In conclusion, the “charges of credit card” encompass a spectrum of fees and interest rates that, if not managed carefully, can lead to significant financial burdens. By understanding the underlying mechanisms of these charges, strategically choosing the right credit card, and adopting disciplined financial habits, you can effectively navigate the complexities of credit card usage. This informed approach, bolstered by the advancements in “tech” and a clear understanding of “money” management, empowers you to harness the benefits of credit cards while minimizing their associated costs, contributing to a healthier and more robust financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.