Navigating the landscape of personal finance can often feel like deciphering a complex code. Among the most frequent challenges individuals face is understanding and calculating their monthly payments for various financial commitments. From mortgages and auto loans to credit card bills and personal lines of credit, these recurring obligations form the backbone of our financial lives. Knowing how to accurately figure out these payments is not just a useful skill; it’s a critical component of effective budgeting, debt management, and long-term financial planning. This article will demystify the process, breaking down the variables, methods, and strategies you can employ to gain a clear command over your monthly financial outflows.

Understanding the Fundamentals of Monthly Payments

Before diving into specific calculations, it’s essential to grasp the core concepts that dictate how monthly payments are structured and determined. These foundational elements apply across most forms of lending and recurring obligations, providing a universal framework for understanding your financial commitments.

What Constitutes a Monthly Payment?

At its simplest, a monthly payment is a recurring sum of money you are obligated to pay at regular intervals, typically once a month, for a service, a loan, or a purchase made on credit. While seemingly straightforward, the components of these payments can vary significantly. For a loan, a payment usually consists of two primary parts: a portion that goes towards reducing the principal amount (the original sum borrowed) and a portion that covers the interest charged by the lender for the use of their money. For subscription services or rental agreements, the payment is generally a fixed fee for access or use. Understanding these distinctions is the first step toward effective financial management.

Key Variables Influencing Payment Calculations

Several critical variables interact to determine the exact amount of your monthly payment. Mastery over these factors empowers you to anticipate and even influence your financial obligations:

- Principal (P): This is the initial amount of money borrowed or the total cost of an item being financed. A higher principal will naturally lead to higher payments, assuming all other variables remain constant.

- Interest Rate (i/r): Expressed as an annual percentage rate (APR), the interest rate is the cost of borrowing money. For monthly payment calculations, the annual rate is typically divided by 12 to get a monthly interest rate. Even small differences in the interest rate can significantly impact the total amount paid over the life of a loan and, consequently, the monthly payment.

- Loan Term (n/t): This refers to the duration over which the loan is to be repaid, usually expressed in years or months. A longer loan term generally results in lower monthly payments but can lead to a higher total amount of interest paid over the life of the loan. Conversely, a shorter term means higher monthly payments but less interest paid overall.

- Fees and Other Charges: Some loans or services might include additional fees, such as origination fees, service charges, or insurance premiums, which can either be added to the principal or paid separately, affecting the overall financial burden.

The Time Value of Money Principle

Underlying all loan calculations is the fundamental economic concept of the “time value of money.” This principle asserts that a sum of money is worth more now than the same sum will be at a future date due to its potential earning capacity. Lenders charge interest because they are deferring the use of their money, and they account for inflation and the opportunity cost of lending. For borrowers, this means that the sooner you pay off a debt, the less interest you will pay in total, effectively saving you money in the long run by reducing the impact of the time value of money on your finances.

Common Types of Monthly Payments and Their Formulas

While the core principles remain consistent, the specific formulas and considerations for calculating monthly payments vary depending on the type of financial commitment. Here, we’ll explore some of the most common scenarios and the methods used to determine their respective payments.

Mortgage Payments: The Amortization Schedule

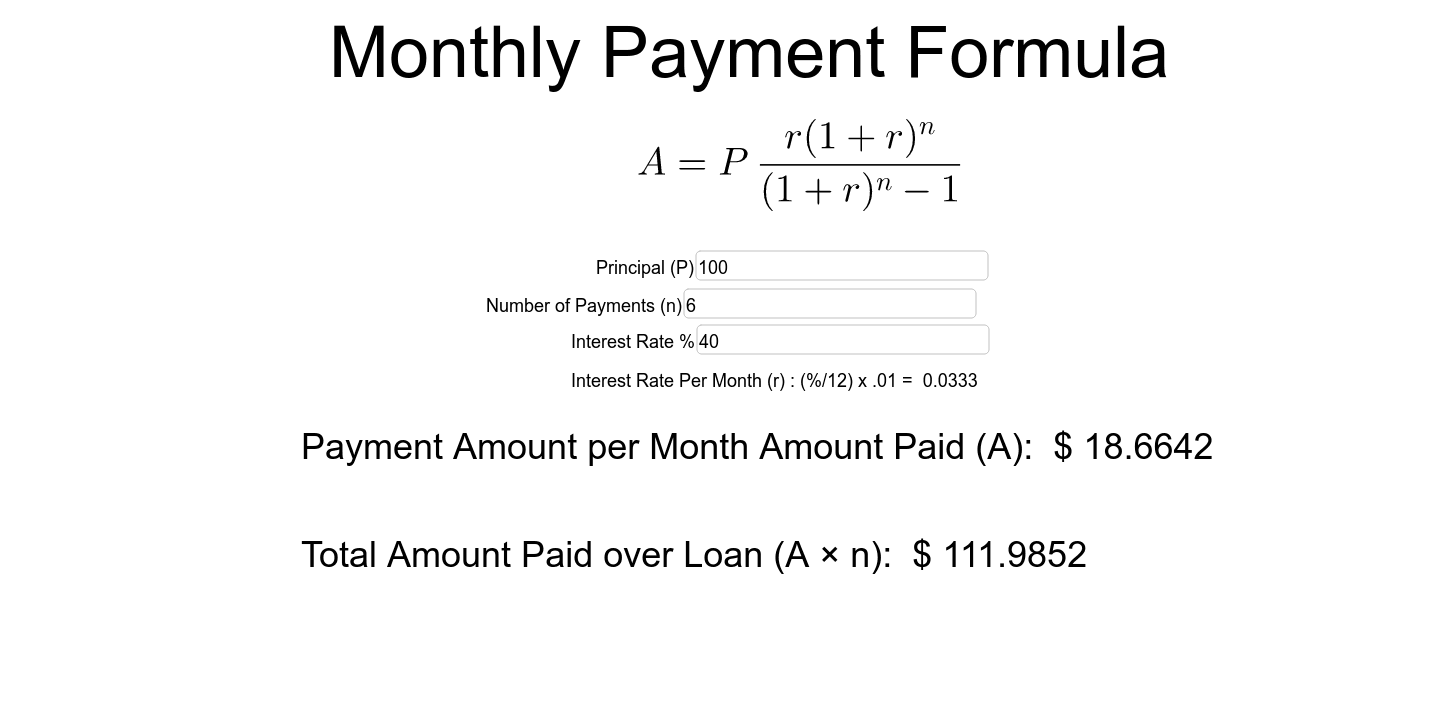

Mortgages are often the largest financial commitment an individual undertakes, and their monthly payments are calculated using an amortization formula. Amortization means gradually paying off a debt over a fixed period through regular installments. Each payment includes both principal and interest, with the interest portion being larger at the beginning of the loan and gradually decreasing as more principal is paid off.

The standard formula for calculating a fixed-rate mortgage payment is:

PMT = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- PMT = Monthly Payment

- P = Principal Loan Amount (the total amount borrowed)

- i = Monthly Interest Rate (annual interest rate divided by 12)

- n = Total Number of Payments (loan term in years multiplied by 12)

Example:

Suppose you borrow $200,000 for a mortgage at an annual interest rate of 4.5% over 30 years.

- P = $200,000

- i = 0.045 / 12 = 0.00375

- n = 30 * 12 = 360

Plugging these values into the formula yields a monthly payment of approximately $1,013.37. This amount covers principal and interest. Property taxes and homeowner’s insurance (often held in an escrow account) are typically added to this sum, making the total housing payment higher.

Auto Loan Payments: A Simpler Calculation

Auto loans also follow an amortization schedule, but they typically have shorter terms (e.g., 3-7 years) and may sometimes have slightly different interest rate structures depending on the lender and borrower’s creditworthiness. The same mortgage payment formula can be applied here, simply by substituting the car loan’s principal, interest rate, and term.

For example, a $25,000 auto loan at 3% annual interest over 5 years (60 months):

- P = $25,000

- i = 0.03 / 12 = 0.0025

- n = 5 * 12 = 60

The monthly payment would be approximately $449.20.

Personal Loans and Credit Card Minimums: Different Approaches

- Personal Loans: These are often unsecured loans with fixed terms and interest rates, calculated similarly to auto loans using the amortization formula. They can be used for various purposes, from debt consolidation to home improvements.

- Credit Card Minimums: This is where calculations diverge significantly. Credit card minimum payments are usually a small percentage of your outstanding balance (e.g., 1-3%) plus any accrued interest and fees, or a fixed dollar amount, whichever is greater. This calculation method often leads to very low principal repayment, prolonging the debt and significantly increasing the total interest paid over time. Relying solely on minimum payments can be a dangerous trap, as it barely chips away at the principal, keeping you in debt for years.

Subscription Services and Recurring Bills: Budgeting Simplicity

For services like Netflix, gym memberships, internet, or utilities, calculating the monthly payment is usually straightforward as it’s a fixed amount or easily quantifiable. The main task here is not calculation but rather diligent tracking and budgeting to ensure these recurring expenses fit within your financial plan without straining your cash flow. Automated payments are common for these services, which adds convenience but also requires regular monitoring to prevent forgotten subscriptions from draining your account.

Practical Tools and Methods for Calculation

In today’s digital age, you don’t always need to wield a financial calculator or complex formulas manually. A range of tools and methods can simplify the process of figuring out monthly payments, ensuring accuracy and saving you time.

Online Calculators: Convenience and Accuracy

The easiest and most common way to calculate monthly payments is by using online calculators. Nearly every financial institution, mortgage lender, and even independent financial websites offer free, user-friendly calculators for mortgages, auto loans, personal loans, and more. You simply input the principal amount, interest rate, and loan term, and the calculator instantly provides the estimated monthly payment. These tools are excellent for quick estimates and comparing different loan scenarios.

Spreadsheet Software: Customization and Scenario Planning

For those who prefer a more hands-on approach or need to perform detailed scenario analysis, spreadsheet software like Microsoft Excel or Google Sheets is invaluable. These programs offer built-in financial functions specifically designed for payment calculations:

- PMT Function: The

PMT(rate, nper, pv, [fv], [type])function in Excel directly calculates the payment for a loan based on constant payments and a constant interest rate.rate: The interest rate per period (e.g., annual rate/12).nper: The total number of payments for the loan (e.g., years*12).pv: The present value, or the total amount that a series of future payments is worth now (the principal).fv: [optional] The future value, or a cash balance you want to attain after the last payment is made. (Defaults to 0).type: [optional] The number 0 or 1 and indicates when payments are due. (0 for end of period, 1 for beginning of period. Defaults to 0).

Using spreadsheets allows you to create your own amortization schedules, adjust variables on the fly, and visualize how changes in interest rates or loan terms impact your payments over time. This level of customization is particularly useful for complex financial planning.

Manual Calculation: The Power of Understanding

While less practical for everyday use, performing a manual calculation of your monthly payments at least once can be incredibly insightful. It solidifies your understanding of the underlying math and variables, fostering a deeper appreciation for how interest accrues and how payments are structured. It helps demystify the process and empowers you to critically evaluate loan offers rather than blindly accepting figures presented to you.

Financial Advisors and Software: Professional Insights

For complex financial situations, large loans, or comprehensive financial planning, consulting with a financial advisor can be highly beneficial. They can not only help you calculate payments but also provide personalized advice on debt management strategies, investment opportunities, and overall financial health. Additionally, various personal finance software tools and apps offer integrated payment calculation features, alongside budgeting, tracking, and reporting functionalities, providing a holistic view of your financial landscape.

Strategies for Managing and Optimizing Monthly Payments

Knowing how to calculate your monthly payments is just the beginning. The next crucial step is to effectively manage and, where possible, optimize these payments to enhance your financial well-being.

Budgeting for Payments: The Foundation of Financial Health

The most fundamental strategy is to integrate all your monthly payments into a comprehensive budget. A budget allows you to see where your money is going, ensure that your income can comfortably cover all your obligations, and identify areas for potential savings. Allocating specific funds for each payment ensures you never miss a due date, avoiding late fees and negative impacts on your credit score. Tools and apps for budgeting can automate this process, tracking your expenses against your income and payment schedules.

Refinancing and Loan Consolidation: Reducing Your Burden

If you find your current monthly payments burdensome, explore options like refinancing or loan consolidation. Refinancing involves taking out a new loan to pay off an existing one, often at a lower interest rate or with a longer term, which can reduce your monthly payment. Loan consolidation combines multiple debts (like credit cards or personal loans) into a single new loan, often with a lower overall interest rate and a single, more manageable monthly payment. Both strategies can free up cash flow but require careful analysis to ensure they save you money in the long run and don’t extend your debt unnecessarily.

Making Extra Payments: Accelerating Debt Repayment

One of the most powerful strategies to save money and reduce your total interest paid is to make extra payments whenever possible. Even small additional payments directly applied to the principal can significantly shorten the loan term and reduce the total interest. For example, making one extra mortgage payment per year can shave years off a 30-year mortgage. Before doing so, always confirm with your lender that extra payments will be applied to the principal and check for any prepayment penalties.

Negotiating Terms: When and How to Engage

Don’t assume loan terms are always set in stone. For new loans, always be prepared to negotiate the interest rate or fees. A good credit score gives you leverage. For existing debts, especially credit card debt, you might be able to negotiate with your lender for a lower interest rate or a more favorable payment plan, particularly if you are experiencing financial hardship. Being proactive and transparent with your financial situation can sometimes yield positive results.

The Impact of Credit Score on Payment Terms

Your credit score is a crucial determinant of the interest rates and terms you’ll be offered for future loans. A higher credit score signals lower risk to lenders, allowing you to qualify for lower interest rates, which directly translates to lower monthly payments and less money paid over the life of the loan. Conversely, a poor credit score can result in higher interest rates, making your monthly payments more expensive and increasing the total cost of borrowing. Regularly monitoring and actively working to improve your credit score is a long-term strategy for optimizing all future monthly payments.

Beyond the Numbers: The Broader Financial Implications

Figuring out monthly payments extends beyond mere arithmetic; it’s about understanding their ripple effect on your entire financial ecosystem and leveraging this knowledge for broader financial goals.

Impact on Cash Flow and Savings

Every dollar committed to a monthly payment is a dollar that cannot be used for other purposes. Understanding the aggregate of your monthly payments allows you to assess your available cash flow – the money left over after all essential expenses and payments are covered. A healthy cash flow is vital for building savings, investing, and affording discretionary spending without incurring new debt. Conversely, a disproportionately high burden of monthly payments can severely restrict your cash flow, making it challenging to save or respond to unexpected expenses.

Planning for Future Financial Goals

Accurate calculation and strategic management of monthly payments are indispensable for long-term financial planning. Whether you’re saving for a down payment on a home, funding a child’s education, or planning for retirement, your current payment obligations dictate how much disposable income you have to allocate towards these future goals. By optimizing your payments, such as paying off high-interest debt sooner, you free up more capital to invest in assets that grow your wealth, bringing your financial aspirations within reach more quickly.

The Importance of Emergency Funds

An often-overlooked aspect of managing monthly payments is the role of an emergency fund. Life is unpredictable, and unexpected events like job loss, medical emergencies, or significant home/auto repairs can suddenly make it difficult to meet your monthly obligations. An emergency fund, typically holding 3-6 months’ worth of living expenses (including all your monthly payments), acts as a financial safety net, providing stability and peace of mind. It prevents you from resorting to high-interest debt or defaulting on payments during crises, thereby protecting your credit and long-term financial health.

Avoiding Payment Traps: Late Fees, Penalties, and Over-indebtedness

Finally, understanding monthly payments empowers you to steer clear of common financial pitfalls. Missing payments leads to late fees, penalty interest rates, and a damaged credit score, all of which snowball into greater financial difficulty. Over-committing to too many monthly payments can lead to over-indebtedness, a state where your debt obligations are unsustainable relative to your income. By diligently calculating, budgeting for, and strategically managing your monthly payments, you maintain control over your finances, avoiding these traps and building a resilient financial future.

In conclusion, the ability to figure out monthly payments is a cornerstone of sound personal finance. It’s a skill that empowers you to make informed decisions, manage debt effectively, and ultimately achieve your financial goals. By applying the formulas, utilizing the available tools, and implementing intelligent management strategies, you can transform the daunting task of deciphering monthly payments into a clear path towards financial clarity and control.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.