Purchasing a car is often one of the most significant financial decisions an individual makes, second only to buying a home. For many, financing a vehicle is a necessity, transforming a large upfront cost into manageable monthly payments. However, beneath the surface of alluring advertisements and low monthly figures lies the often-misunderstood mechanism of car finance interest. Understanding how this interest works is paramount for making informed decisions, minimizing costs, and ultimately securing a vehicle without unnecessary financial burden. This comprehensive guide will demystify car finance interest, breaking down its components, various types, and crucial factors that influence your final borrowing cost.

Understanding the Fundamentals of Car Finance Interest

At its core, interest is the cost of borrowing money. When you finance a car, a lender provides you with the capital to purchase the vehicle, and in return, you pay back that capital (the principal) plus an additional fee – the interest – over a predetermined period. This fee compensates the lender for the risk they take and the opportunity cost of not investing that money elsewhere.

What is Interest and Why Does It Apply to Car Loans?

Every loan, whether for a house, education, or a car, involves interest because lenders are essentially selling you access to their capital. They assess your creditworthiness, the term of the loan, and prevailing market conditions to determine a rate that reflects the risk and profit margin they require. For car loans, the vehicle itself often serves as collateral, meaning the lender can repossess it if you fail to make payments. This reduces some risk for the lender, but interest still applies as a core component of the lending business model. It’s the price you pay for the convenience of driving a car today that you can’t afford to buy outright.

Key Terminology: Principal, Interest Rate, Loan Term, and APR

To truly grasp car finance, familiarity with key terms is essential:

- Principal: This is the original amount of money you borrow to purchase the car, excluding any interest or fees. If a car costs $30,000 and you put down $5,000, your principal loan amount is $25,000.

- Interest Rate: Expressed as a percentage, this is the cost charged by the lender for the use of their money. A higher interest rate means you’ll pay more over the life of the loan. This can be fixed (stays the same) or variable (changes over time). Car loans are predominantly fixed-rate.

- Loan Term: This refers to the duration over which you agree to repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months). A longer loan term generally results in lower monthly payments but a higher total interest paid over the life of the loan.

- Annual Percentage Rate (APR): This is perhaps the most critical figure. The APR represents the total cost of borrowing each year, expressed as a percentage. Unlike a simple interest rate, the APR includes not only the nominal interest rate but also any additional fees associated with the loan, such as origination fees, administrative charges, or dealer add-ons, amortized over the loan term. It provides a more accurate, apples-to-apples comparison of different loan offers.

The Mechanics of Interest Calculation and Loan Types

The way interest is calculated can vary slightly depending on the type of finance agreement you enter into. While most car loans use a simple interest method, understanding the nuances of different financing products is crucial.

Simple Interest vs. Pre-computed Interest

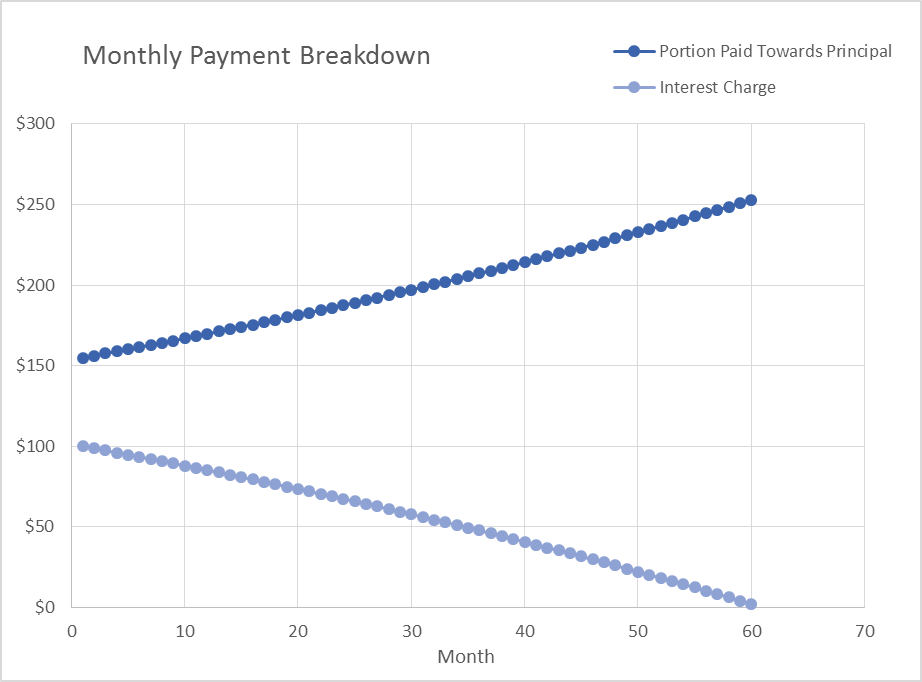

Most modern car loans operate on a simple interest basis. This means interest is calculated daily or monthly on the remaining principal balance. As you make payments, a portion goes towards the interest accrued since your last payment, and the remainder reduces your principal. Over time, as the principal decreases, less interest accrues, and a larger portion of your payment goes towards reducing the principal. This method benefits borrowers who make extra payments, as doing so directly reduces the principal, leading to less interest paid overall.

Conversely, some older or less transparent finance agreements might use pre-computed interest. In this method, the total interest for the entire loan term is calculated upfront and added to the principal. You then pay this fixed total regardless of when you pay off the loan. This means making extra payments won’t reduce the total interest you owe, which is generally disadvantageous for the borrower. Always ensure your loan uses simple interest.

Common Car Finance Options and Their Interest Structures

- Hire Purchase (HP) / Installment Loan: This is a straightforward method where you borrow a fixed sum to buy the car and repay it in equal monthly installments over a set period. Ownership transfers to you once the final payment is made. Interest is typically fixed and calculated on the initial principal balance, often using a simple interest methodology. It’s transparent and predictable.

- Personal Contract Purchase (PCP) / Balloon Payment Loan: Popular for new cars, PCP splits the car’s value into three parts: your deposit, monthly payments, and a large “balloon payment” (Guaranteed Future Value – GFV) at the end. Your monthly payments only cover the depreciation of the car over the term plus interest on the entire loan amount (including the GFV). At the end, you can pay the GFV to own the car, trade it in, or return it. The interest is calculated on the full loan amount, making the total interest paid potentially higher than HP for the same car and term, even though monthly payments are lower.

- Personal Loans: You can also take out an unsecured personal loan from a bank or credit union and use the funds to buy the car outright. Interest rates for personal loans can vary widely based on your creditworthiness, but they offer flexibility as the car is immediately yours, and there are no mileage restrictions or return conditions associated with the loan itself. Interest calculation is typically simple interest.

Factors Influencing Your Car Finance Interest Rate

The interest rate you receive isn’t arbitrary; it’s a reflection of several key factors that lenders assess to determine their risk and potential profit. Understanding these can empower you to improve your position before applying for finance.

Your Creditworthiness: The Cornerstone of Interest Rates

Your credit score and credit history are arguably the most significant determinants of the interest rate you’ll be offered. Lenders use your credit report to gauge your reliability as a borrower.

- Excellent Credit (720+ FICO): Indicates a very low risk. You’ll likely qualify for the lowest available interest rates.

- Good Credit (660-719 FICO): Still considered low risk, qualifying for competitive rates, though slightly higher than excellent credit.

- Fair/Average Credit (620-659 FICO): Moderate risk. Interest rates will be noticeably higher.

- Poor Credit (<620 FICO): High risk. You’ll face significantly higher interest rates, and approval might be more challenging.

A strong credit history demonstrates a consistent ability to manage debt, make payments on time, and avoid excessive borrowing.

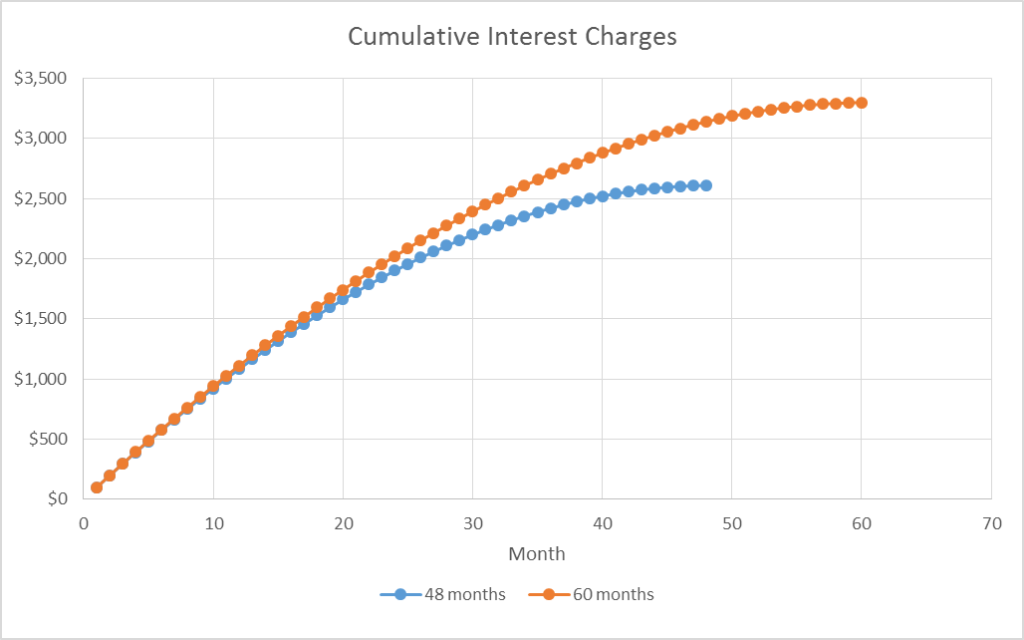

The Loan Term: Length vs. Total Cost

As mentioned, the loan term directly impacts both your monthly payment and the total interest paid.

- Shorter Terms (e.g., 36-48 months): Generally come with lower interest rates because the lender’s risk is lower over a shorter period. Monthly payments are higher, but you pay significantly less interest overall.

- Longer Terms (e.g., 60-84 months): Offer lower monthly payments, making the car seem more affordable. However, they typically carry slightly higher interest rates and accrue interest for a longer duration, resulting in a substantially higher total cost of the loan. It also increases the risk of negative equity (owing more than the car is worth).

Down Payment Amount: Reducing the Principal and Risk

A larger down payment reduces the principal amount you need to borrow, which directly translates to less interest paid over the life of the loan. Furthermore, a substantial down payment reduces the lender’s risk, as they have less money at stake and the loan-to-value (LTV) ratio is more favorable. This reduced risk can sometimes lead to a slightly lower interest rate offer.

Market Interest Rates and Economic Conditions

Broader economic factors also play a role. Central bank interest rates (like the Federal Funds Rate in the US or the Bank of England Base Rate) influence the cost of borrowing for lenders. When these rates rise, the cost of car loans generally increases across the board. Conversely, during periods of economic stimulus, rates might be lower.

Strategies to Minimize Car Finance Interest Costs

Being proactive and informed can save you hundreds, if not thousands, of dollars in interest over the life of your car loan.

Enhance Your Credit Score Before Applying

Before you even step into a dealership, take steps to improve your credit score. Pay down existing debts, especially high-interest credit cards, and ensure all bill payments are made on time. Dispute any errors on your credit report. A few points improvement can shift you into a better rate bracket.

Make a Substantial Down Payment

Save up for as large a down payment as you can comfortably afford. This not only reduces your principal and, therefore, your total interest but also provides a buffer against depreciation and reduces the likelihood of negative equity.

Opt for the Shortest Loan Term You Can Afford

While longer terms offer lower monthly payments, prioritize affordability over the absolute lowest monthly figure. Calculate what you can genuinely afford each month and aim for the shortest loan term within that budget. The long-term savings in interest can be significant.

Shop Around and Compare Offers

Don’t settle for the first finance offer you receive, especially not from the dealership’s finance department alone. Get pre-approved for a car loan from multiple banks, credit unions, and online lenders before you visit the dealer. This not only gives you a benchmark but also puts you in a stronger negotiating position. Dealerships often offer their own financing options and may be able to beat outside offers, but having your own pre-approval acts as leverage.

Understand and Compare APR, Not Just Interest Rate

Always focus on the Annual Percentage Rate (APR) when comparing loan offers. This single figure encapsulates the true annual cost of borrowing, including the interest rate and all mandatory fees. A loan with a slightly lower nominal interest rate but higher fees might end up having a higher APR than a seemingly higher interest rate loan with no fees.

The Long-Term Financial Impact and Responsible Borrowing

A car loan is a significant financial commitment, and its impact extends beyond just the monthly payment. Responsible borrowing requires a holistic view of the total cost and long-term implications.

Beyond the Monthly Payment: Total Cost of Ownership

While an attractive monthly payment is often the focus, it’s crucial to calculate the total cost of the loan over its entire term. This involves multiplying your monthly payment by the number of months in the term and adding any initial fees. You might be surprised at how much more you pay in interest compared to the car’s sticker price. Factor this into your overall vehicle budget, which should also include insurance, fuel, maintenance, and potential depreciation.

Avoiding Negative Equity: The “Upside-Down” Loan Trap

Negative equity, or being “upside down” on your loan, occurs when you owe more on your car than its current market value. This is a common risk with long loan terms, small down payments, and rapid vehicle depreciation (especially with new cars). Should your car be stolen, totaled, or if you need to sell it early, you’d still owe the lender the difference. Gap insurance can protect against this in case of a total loss.

Refinancing Options: When and Why to Consider It

If your credit score has improved since you first took out your loan, or if market interest rates have dropped significantly, you might be able to refinance your car loan. Refinancing replaces your existing loan with a new one, potentially at a lower interest rate, which can reduce your monthly payments or the total interest paid. It’s a strategy worth exploring if your financial circumstances or market conditions have changed favorably.

Budgeting for Repayments: A Holistic Approach

Integrate your car loan payments into your overall personal budget. Ensure you have a clear understanding of your cash flow and that the payments are comfortably affordable, even with unexpected expenses. Don’t stretch your budget too thin just to get a particular car. A good rule of thumb is that your total vehicle expenses (payment, insurance, fuel, maintenance) should not exceed 10-15% of your net monthly income.

In conclusion, car finance interest is not just a number; it’s a dynamic element that significantly shapes the true cost of your vehicle purchase. By diligently understanding the various components of interest, evaluating different finance options, proactively managing your credit, and comparing offers, you can navigate the complexities of car financing with confidence. Responsible borrowing, underpinned by a clear understanding of how interest works, is the key to driving away in your dream car without financial regrets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.