The thought of owing money to the Internal Revenue Service (IRS) can be a source of significant anxiety for many individuals and businesses. Whether it’s a forgotten payment, an unexpected tax bill, or simply a nagging uncertainty, understanding your tax obligations and proactively addressing them is a cornerstone of sound financial health. Ignoring potential tax debt can lead to mounting penalties, interest, and greater financial complications down the line. This comprehensive guide is designed to empower you with the knowledge and tools to accurately determine your IRS tax status, understand any outstanding liabilities, and navigate the pathways to resolution. By demystifying the process, we aim to provide clarity and instill confidence in managing your financial relationship with the nation’s tax agency.

The Critical Importance of Knowing Your IRS Tax Status

In personal finance, few things are as critical as understanding your liabilities, and tax debt is often among the most impactful. Knowing whether you owe the IRS money, and how much, is not just about fulfilling a civic duty; it’s about protecting your financial future and peace of mind. The ramifications of an unaddressed tax debt can extend far beyond a simple bill.

Avoiding Penalties and Interest

One of the most immediate and significant consequences of outstanding tax debt is the accumulation of penalties and interest. The IRS charges penalties for various reasons, including failure to file on time, failure to pay on time, and underpayment of estimated taxes. These penalties are often a percentage of the unpaid tax, and they can grow surprisingly quickly. On top of penalties, the IRS also charges interest on underpayments and unpaid taxes, which can compound daily. What might start as a manageable sum can, over time, become a substantial burden. Proactively discovering and addressing a debt allows you to halt this escalation, often leading to significant savings.

Maintaining Financial Health and Creditworthiness

Unresolved tax debt can cast a long shadow over your overall financial health. While the IRS doesn’t directly report tax debt to major credit bureaus in the same way a credit card company might, they do file a Notice of Federal Tax Lien when a taxpayer neglects or refuses to pay a tax debt. This public record can significantly damage your credit score, making it harder to secure loans, mortgages, or even certain jobs. Furthermore, the psychological burden of unknown or unaddressed debt can lead to stress, impacting your decision-making and preventing you from focusing on wealth-building activities. A clear understanding of your tax standing is essential for sound financial planning and maintaining a healthy credit profile.

Preventing Future Complications

Beyond penalties and credit implications, ignoring IRS debt can lead to more severe enforcement actions. The IRS has powerful collection tools at its disposal, including tax levies (seizing bank accounts, wages, or other property) and tax seizures (taking possession of physical assets). In extreme cases, outstanding tax debt can even impact your ability to renew your passport. Identifying and resolving debt early can prevent these disruptive and often distressing actions, ensuring that your financial affairs remain orderly and your future plans unhindered. Proactivity is key to safeguarding against these more aggressive collection measures.

Official Channels to Ascertain Your IRS Debt

The IRS provides several secure and reliable methods for taxpayers to check their account status and determine if they owe money. These official channels are your first and best recourse for accurate information.

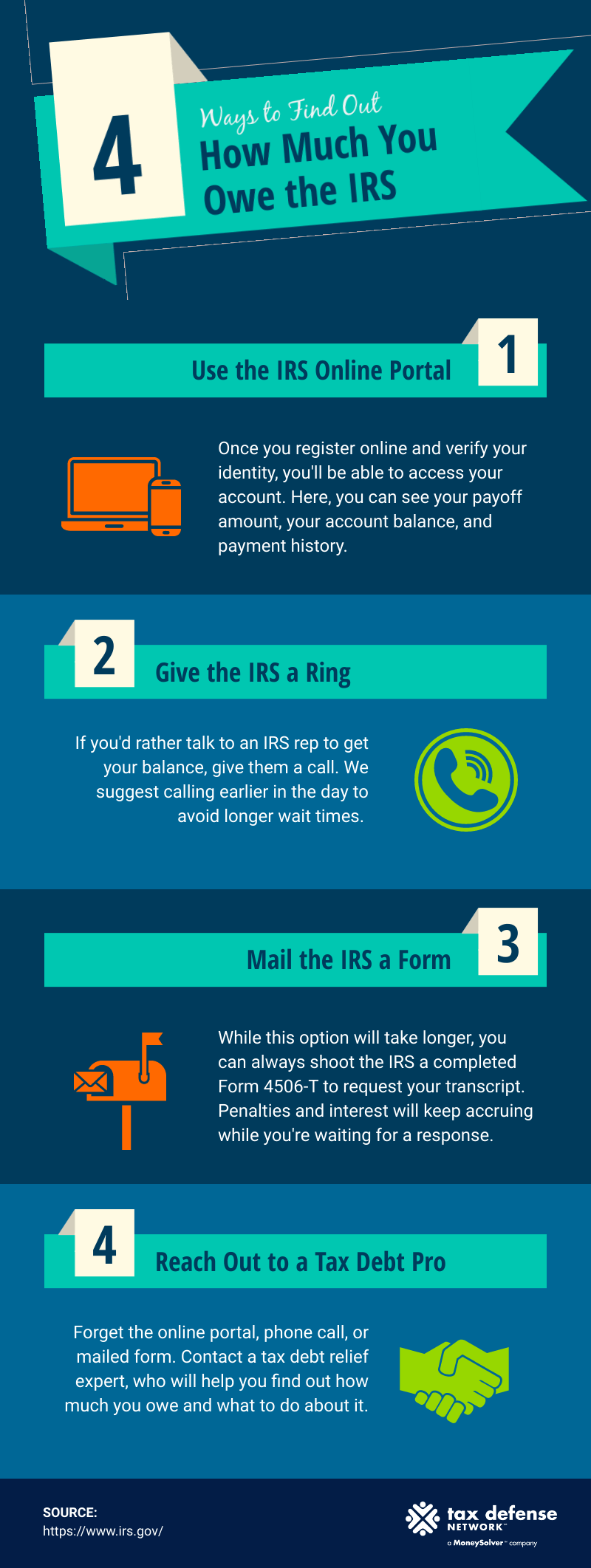

Utilizing the IRS Online Account

The IRS Online Account is arguably the most convenient and comprehensive tool for individual taxpayers to manage their tax affairs digitally. By creating and accessing your account on the IRS website, you can:

- View your balance, including tax, penalties, and interest.

- See your payment history, including scheduled and pending payments.

- Access tax records, such as transcripts.

- View notices from the IRS.

- Manage communication preferences.

- Make payments directly from your bank account or through other options.

Setting up an account requires a robust identity verification process to protect your sensitive financial information, often involving multiple authentication factors. Once established, it offers a real-time snapshot of your tax situation, making it an invaluable resource for proactive financial management.

Requesting a Tax Transcript

A tax transcript is a summary of your tax return information or account activity. While it doesn’t always show the current balance due directly, it provides a detailed history that can help you understand your tax situation, including any assessments or adjustments made by the IRS. There are several types of transcripts:

- Account Transcript: Shows basic return information, payment history, and adjustments made by you or the IRS after the return was filed. It typically covers the past 10 years.

- Record of Account Transcript: Combines the Account Transcript with line-by-line information from your original return.

- Tax Return Transcript: Shows most line items from your original tax return as it was filed, including any accompanying forms and schedules.

You can request transcripts online, by mail (Form 4506-T or 4506T-EZ), or by phone. They are often used by lenders, for student loan applications, or when you need to verify income for various purposes. By reviewing your Account Transcript, you can spot any discrepancies or unexpected charges that might indicate an outstanding balance.

Contacting the IRS Directly

For a direct conversation about your specific tax situation, contacting the IRS by phone is an option. While wait times can sometimes be long, speaking with an IRS representative can provide clarity, especially if your situation is complex or if you have questions about specific notices.

- Individual Taxpayers: Call 1-800-829-1040 (TTY/TDD 1-800-829-4059 for hearing impaired).

- Business Taxpayers: Call 1-800-829-4933.

- International Callers: Refer to the IRS website for specific international contact numbers.

Before calling, ensure you have all relevant personal information, such as your Social Security number, date of birth, and any prior tax returns or IRS notices, ready for verification. It’s often advisable to call early in the morning on a weekday to potentially reduce wait times.

Consulting a Tax Professional

When in doubt, or if your situation is particularly intricate, enlisting the help of a qualified tax professional is often the best course of action. Certified Public Accountants (CPAs), Enrolled Agents (EAs), and tax attorneys are authorized to represent taxpayers before the IRS. They can:

- Access your tax records with your permission (via a Power of Attorney, Form 2848).

- Interpret complex IRS notices and statements.

- Advise you on the exact nature of your debt.

- Help identify any errors made by you or the IRS.

- Guide you through payment options or dispute processes.

A professional can provide invaluable expertise, saving you time and stress, and potentially identifying solutions you might not discover on your own. This is particularly recommended if you receive multiple notices, are dealing with significant amounts, or have a history of non-compliance.

Deciphering Your Tax Obligations

Once you’ve identified that you might owe the IRS, the next crucial step is to understand the nature and origin of that debt. Tax obligations can arise from various scenarios, and knowing the specifics is key to effective resolution.

Understanding Different Types of Tax Debts

Tax debt isn’t a monolith; it can stem from several distinct sources, each with its own implications:

- Unpaid Income Tax: This is the most common form, occurring when your withholdings or estimated tax payments throughout the year were insufficient to cover your total tax liability.

- Estimated Tax Underpayment Penalties: If you’re self-employed or have significant income not subject to withholding (e.g., investment income), you’re typically required to pay estimated taxes quarterly. Failing to pay enough by the due dates can result in penalties, even if you pay your full tax by the April deadline.

- Failure to File Penalty: If you don’t file your tax return by the due date (including extensions), the IRS may impose a penalty, which is generally 5% of the unpaid taxes for each month or part of a month that a return is late, capped at 25%.

- Failure to Pay Penalty: This applies if you don’t pay the taxes you owe by the due date. The penalty is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, with a maximum of 25% of your unpaid tax.

- Accuracy-Related Penalties: These can be imposed if you underpay your tax due to negligence, substantial understatement of income, or substantial valuation misstatement.

Understanding which of these categories your debt falls into helps in determining the best course of action and exploring potential penalty abatements.

Interpreting IRS Notices and Letters

The IRS primarily communicates through mail. Receiving a letter from the IRS can be unsettling, but it’s crucial not to ignore it. Each notice or letter typically explains the reason for the contact, the issue, and what action you need to take. Common notices include:

- CP14: Balance Due – A straightforward bill indicating an outstanding tax amount.

- CP2000: Proposed Changes to Your Tax Return – Usually generated when information reported by third parties (like employers or banks) doesn’t match what you reported on your return.

- CP504: Notice of Intent to Levy – A serious warning that the IRS intends to seize assets if the debt isn’t resolved.

Always read IRS notices carefully, paying attention to the notice number (top right corner), the specific tax year it refers to, the amount due, and the response deadline. If you don’t understand a notice, contact the IRS or a tax professional for clarification. Ignoring them only exacerbates the problem.

Identifying Potential Errors

While the IRS is diligent, errors can occur, either on their part or yours. Before accepting a tax debt as legitimate, review your records and the IRS’s calculations for any potential mistakes.

- Your Errors: Did you miscalculate deductions, report income incorrectly, or forget to include certain income sources?

- IRS Errors: Less common, but possible, are errors in processing your return, applying payments, or calculating penalties.

If you believe there’s an error, gather documentation to support your claim. For discrepancies in a CP2000 notice, for example, you’ll typically send a response with supporting documents within the specified timeframe. A tax professional can be instrumental in identifying and disputing errors on your behalf, often leading to a reduction or elimination of the alleged debt.

Strategies for Addressing an IRS Tax Debt

Discovering you owe the IRS money doesn’t have to be a catastrophe. The IRS offers various programs and payment options to help taxpayers resolve their debts. The key is to act promptly and choose the right strategy for your financial situation.

Full Payment Options

If you have the financial means, paying your tax debt in full is generally the best option, as it stops the accumulation of penalties and interest immediately. The IRS provides several convenient ways to make a full payment:

- IRS Direct Pay: A free, secure way to pay directly from your checking or savings account.

- Debit Card, Credit Card, or Digital Wallet: Payments can be made online, by phone, or through a mobile device via authorized third-party payment processors (fees apply).

- Electronic Federal Tax Payment System (EFTPS): A free service for individuals and businesses, allowing payments to be scheduled up to 365 days in advance.

- Check or Money Order: Mailed with a payment voucher (Form 1040-V) to the appropriate IRS address.

Choosing the method that best suits your needs ensures that your payment is processed correctly and on time.

Payment Plans

For taxpayers who cannot pay their debt in full immediately, the IRS offers several payment arrangements:

- Short-Term Payment Plan: You may be granted up to 180 days to pay your tax liability in full, though interest and penalties still apply. This is an informal agreement and is suitable for those who anticipate receiving funds within that timeframe. You can often request this through your IRS Online Account.

- Installment Agreement: This allows you to make monthly payments for up to 72 months (6 years). An installment agreement is generally available to taxpayers who owe a combined total of under $50,000 (for individuals) or $25,000 (for businesses) in tax, penalties, and interest, and who have filed all required tax returns. While interest and penalties continue to accrue, they may be reduced once the agreement is in place. Setting up an agreement online is often the fastest way to get approved.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owed. This option is generally available if you can demonstrate that you have a genuine inability to pay the full amount due to your current financial situation, or if there is doubt as to the amount of tax you actually owe. The IRS evaluates OIC applications based on your ability to pay, your income, expenses, and asset equity. An OIC is a complex process and typically requires the assistance of a tax professional.

Each option has specific criteria and implications, so it’s essential to understand which one is best suited for your circumstances.

Seeking Professional Guidance

Navigating IRS debt can be complex and intimidating. A qualified tax professional—such as a CPA, Enrolled Agent, or tax attorney—can be an invaluable ally. They can:

- Evaluate your financial situation: To determine the most appropriate payment option.

- Negotiate on your behalf: With the IRS, particularly for complex agreements like an OIC or penalty abatement requests.

- Represent you in audits or appeals: If your debt stems from a dispute with the IRS.

- Provide peace of mind: By ensuring all procedures are followed correctly and effectively.

For significant tax debts or complicated scenarios, professional guidance is highly recommended to achieve the best possible outcome and alleviate stress.

Proactive Steps for Future Tax Compliance

The best defense against future IRS debt is a robust offense rooted in good financial habits and proactive tax planning. By implementing smart strategies, you can minimize the risk of owing money and ensure a smoother tax season year after year.

Accurate Record Keeping

Meticulous record keeping is the bedrock of sound financial management and tax compliance. Retain all financial documents for at least three to seven years, depending on the document type and potential audit risk. This includes:

- Pay stubs and W-2 forms.

- 1099 forms for interest, dividends, or contract work.

- Receipts for deductible expenses (charitable contributions, medical expenses, business expenses).

- Bank and investment statements.

- Records of asset purchases and sales.

Organized records not only make tax preparation easier but also serve as crucial evidence if the IRS ever questions your return or claims. Digital copies backed up in the cloud can be particularly helpful for security and accessibility.

Regular Tax Withholding Review

For employees, reviewing your tax withholding is a simple yet powerful way to prevent underpayment. Your Form W-4 determines how much federal income tax your employer withholds from your paycheck. Life events such as marriage, divorce, having a child, buying a home, or changing jobs can significantly impact your tax liability.

- Use the IRS Tax Withholding Estimator: This online tool on the IRS website helps you determine if you’re withholding the correct amount.

- Adjust your W-4: If the estimator suggests changes, submit a new Form W-4 to your employer to adjust your withholdings.

- Annual Check-up: Make it a habit to review your W-4 annually, especially at the beginning of the year or after any major life changes.

Adjusting your withholdings to match your expected tax liability can prevent a large tax bill (or a surprisingly large refund, which means you’ve essentially given the government an interest-free loan).

Understanding Estimated Taxes

If you are self-employed, a freelancer, own a small business, or have significant income not subject to withholding (e.g., rental income, investment income, alimony), you are likely required to pay estimated taxes throughout the year. The U.S. tax system operates on a “pay-as-you-go” basis.

- Calculate your estimated tax: Use Form 1040-ES, Estimated Tax for Individuals, to calculate and pay your estimated tax quarterly.

- Pay on time: Estimated tax payments are typically due on April 15, June 15, September 15, and January 15 of the following year.

- Avoid penalties: Paying enough estimated tax (or through adequate withholding) throughout the year can help you avoid underpayment penalties. Generally, you need to pay at least 90% of your current year’s tax liability or 100% of your prior year’s tax liability (110% if your Adjusted Gross Income was over $150,000) through withholding and estimated payments.

This is a critical area for many independent workers, and understanding and adhering to estimated tax requirements can save you from unexpected tax bills and penalties.

Annual Tax Health Checks

Beyond specific adjustments, make an annual tax “health check” a part of your financial routine. This involves:

- Reviewing your overall financial picture: Are there new income sources? Changes in deductions?

- Anticipating major life changes: Will you get married, have a child, or sell assets next year? Plan for the tax implications.

- Consulting a tax professional: Even if you typically do your own taxes, a periodic consultation with a tax advisor can help identify potential issues, suggest strategies for tax savings, and ensure you’re on track with compliance.

This proactive approach transforms tax planning from a reactive chore into an integral part of your year-round financial strategy, significantly reducing the likelihood of encountering unexpected IRS debt.

The potential of owing the IRS money can be a daunting prospect, but it is one that can be managed and mitigated with knowledge and proactive engagement. By utilizing the official channels to ascertain your tax status, diligently interpreting any notices, and strategically addressing any existing debts, you maintain control over your financial narrative. Furthermore, by adopting robust record-keeping practices, reviewing your withholdings, understanding estimated taxes, and performing annual financial health checks, you empower yourself to prevent future complications. Financial peace of mind often stems from clarity and action, and when it comes to the IRS, being informed is your most powerful asset. Take the initiative, leverage the resources available, and confidently manage your tax obligations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.