Understanding the intricate web of factors that influence mortgage rates is crucial for anyone navigating the housing market, whether as a first-time homebuyer or a seasoned investor. Mortgage rates are not set in a vacuum; they are dynamic, responsive to a confluence of economic indicators, central bank policies, and even global events. Delving into these drivers provides valuable foresight and empowers individuals to make informed financial decisions regarding one of their most significant investments.

The Federal Reserve’s Orchestration: Monetary Policy and Interest Rates

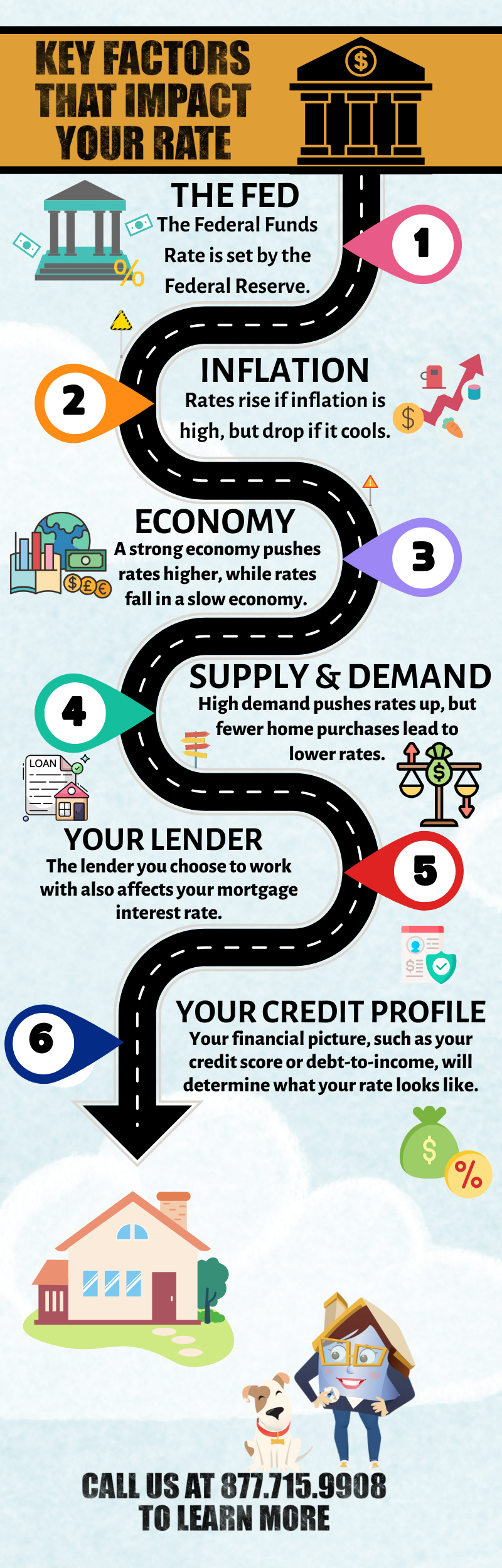

At the heart of the U.S. financial system, the Federal Reserve (the Fed) plays a pivotal role in shaping the economic landscape, with its actions directly and indirectly impacting mortgage rates. While the Fed does not directly set mortgage rates, its monetary policy decisions ripple through the economy, influencing the cost of borrowing across the board.

The Federal Funds Rate and Its Echoes

The most widely publicized tool of the Federal Reserve is the federal funds rate. This is the target interest rate at which commercial banks borrow and lend their excess reserves to each other overnight. When the Fed raises the federal funds rate, it becomes more expensive for banks to borrow money, a cost they then pass on to consumers in the form of higher interest rates for various loans, including credit cards, auto loans, and to some extent, mortgages.

However, mortgage rates, particularly for long-term fixed-rate mortgages, are more closely tied to the yields on long-term U.S. Treasury bonds than to the federal funds rate itself. Still, the federal funds rate influences the overall economic environment and inflation expectations, which in turn affect bond yields. A higher federal funds rate generally signals the Fed’s intent to cool inflation, which can lead to higher bond yields as investors demand greater returns to offset potential future inflation. Conversely, a lower federal funds rate often aims to stimulate economic activity, potentially leading to lower bond yields and, consequently, lower mortgage rates.

Quantitative Easing, Tightening, and the Mortgage Market

Beyond the federal funds rate, the Fed employs other powerful tools, such as quantitative easing (QE) and quantitative tightening (QT). During QE, the Fed purchases vast quantities of government bonds and mortgage-backed securities (MBS) from the open market. The primary goal is to inject liquidity into the financial system, lower long-term interest rates (including mortgage rates), and encourage lending and investment. By increasing demand for MBS, the Fed drives up their prices, which pushes down their yields, thereby making mortgages cheaper for consumers.

Conversely, quantitative tightening involves the Fed allowing its bond holdings to mature without reinvesting the proceeds, or actively selling them. This process effectively removes liquidity from the financial system, putting upward pressure on long-term interest rates and potentially leading to higher mortgage rates as the supply of bonds increases and their prices fall (yields rise). These less direct, yet highly impactful, policies underscore the Fed’s profound influence on the mortgage market.

Economic Vital Signs: Inflation, Growth, and the Labor Market

Beyond direct central bank interventions, the broader economic health of a nation significantly dictates the direction of mortgage rates. Key economic indicators provide insights into the forces of supply and demand for credit, directly affecting how lenders price their mortgage products.

Inflation Expectations: A Double-Edged Sword

Inflation, the rate at which the general level of prices for goods and services is rising, is a critical factor for mortgage rates. Lenders need to ensure that the return on their loans will outpace inflation; otherwise, the real value of the money they get back will be less than the money they lent. Therefore, when inflation expectations rise, lenders demand higher interest rates to compensate for the anticipated erosion of their future earnings’ purchasing power. This leads to higher mortgage rates. Conversely, if inflation is low and expected to remain so, lenders can afford to offer lower rates.

Moreover, inflation directly impacts the bond market. Investors in bonds (including MBS) demand a yield that at least compensates for inflation. If inflation rises, bond prices fall, and their yields (interest rates) rise. Since mortgage rates are often benchmarked to the yield on 10-year Treasury notes, an increase in inflation expectations usually translates to higher mortgage rates.

The Yield Curve and Treasury Bonds

As previously mentioned, fixed-rate mortgage rates are closely correlated with the yield on the 10-year U.S. Treasury note. This benchmark represents the risk-free rate of return that investors can expect over a decade. When the yield on the 10-year Treasury rises, mortgage rates tend to follow suit, and vice versa.

The relationship between short-term and long-term Treasury yields, known as the yield curve, also provides valuable signals. An upward-sloping yield curve, where long-term yields are higher than short-term yields, is typical and reflects expectations of future economic growth and inflation. However, an inverted yield curve, where short-term yields surpass long-term yields, is often seen as a predictor of a recession, as investors anticipate future economic weakness and thus lower long-term inflation. While an inverted curve can temporarily lower long-term rates (including mortgages) due to recession fears, the overall economic impact is often negative.

Employment and Economic Growth: Indicators of Demand

Robust economic growth and a strong labor market typically lead to higher mortgage rates. A healthy economy often means more jobs, higher wages, and increased consumer confidence, which translates into greater demand for housing and, subsequently, higher demand for mortgages. Lenders can then charge more for their loans due to this increased demand. Additionally, a strong economy often brings with it the risk of inflation, which, as discussed, pushes rates higher.

Conversely, during periods of economic slowdown or recession, job losses and reduced consumer confidence lead to lower demand for housing. Lenders may then lower mortgage rates to stimulate borrowing and investment in the housing market. Employment reports, Gross Domestic Product (GDP) figures, and consumer confidence indices are therefore closely watched for their potential impact on future mortgage rate trends.

Individual Borrowers and Lender Dynamics

While macroeconomic forces paint the broad strokes, individual borrower characteristics and the competitive landscape among lenders refine the specific mortgage rate offered to each applicant. These micro-level factors determine an individual’s perceived risk and the cost of capital for the lender.

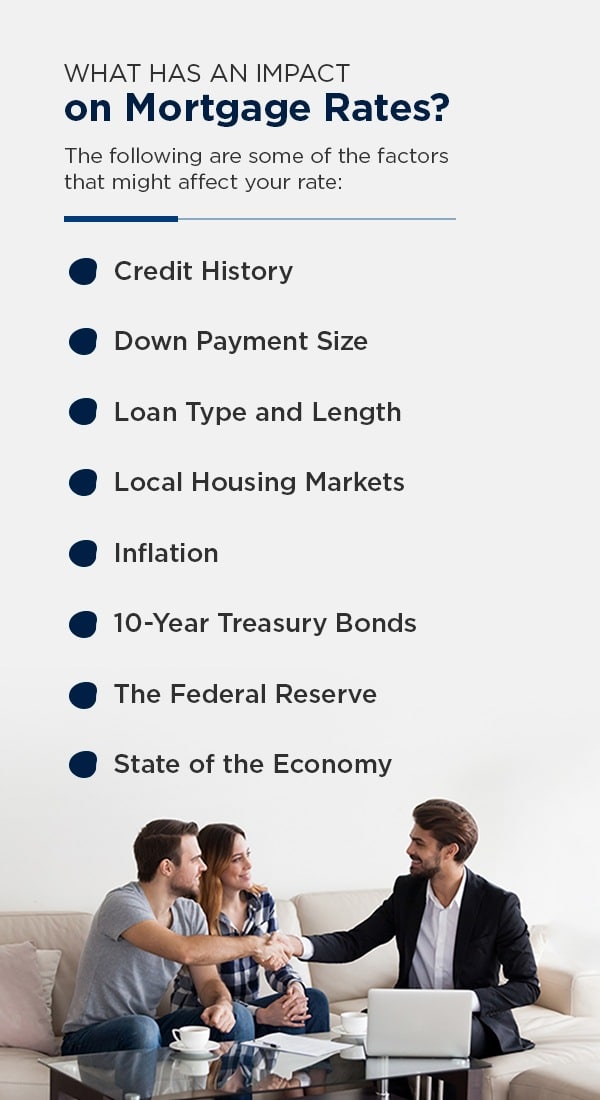

Your Credit Score and Debt-to-Income Ratio

Perhaps the most direct personal factor influencing your mortgage rate is your credit score. Lenders use credit scores (like FICO scores) to assess your creditworthiness – your likelihood of repaying the loan. A higher credit score (typically above 740-760) signals a lower risk to lenders, often qualifying you for the most favorable interest rates. Conversely, a lower credit score indicates higher risk, leading lenders to charge higher rates to compensate for that increased risk.

Your debt-to-income (DTI) ratio is another crucial metric. This compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover your mortgage payments, making you a less risky borrower. Lenders prefer a DTI ratio below 43%, though some may accept higher depending on other factors. A high DTI can result in a higher interest rate or even denial of the loan.

Loan-to-Value (LTV) and Down Payment Impact

The loan-to-value (LTV) ratio compares the amount of your mortgage to the appraised value of the home. A higher down payment results in a lower LTV ratio, signifying less risk for the lender. For example, a 20% down payment means an 80% LTV. Lenders often offer better rates for lower LTVs because the borrower has more equity in the home from the outset, reducing the lender’s exposure if the property value declines. A lower LTV also often eliminates the need for private mortgage insurance (PMI), which adds to the overall cost of borrowing.

Loan Products and Terms: Fixed vs. Adjustable

The type of mortgage you choose also directly impacts the rate.

- Fixed-Rate Mortgages: These offer a consistent interest rate for the entire life of the loan (e.g., 15-year or 30-year fixed). The rate is generally higher than initial adjustable-rate mortgages because the lender bears the risk of future interest rate increases.

- Adjustable-Rate Mortgages (ARMs): ARMs typically offer a lower initial interest rate for a set period (e.g., 3, 5, 7, or 10 years) before adjusting periodically based on a chosen index. The initial lower rate reflects the borrower taking on the risk of future rate fluctuations.

Shorter-term mortgages (e.g., 15-year fixed) generally have lower interest rates than longer-term mortgages (e.g., 30-year fixed) because the lender’s money is tied up for a shorter period, reducing their interest rate risk.

Lender’s Business Model and Market Competition

Even with all other factors being equal, different lenders may offer slightly varying rates. This is due to their individual operational costs, profit margins, and specific market strategies. Intense competition among lenders can drive rates down as they vie for market share. Conversely, if fewer lenders are active or if specific lenders dominate the market, rates might be higher. Shopping around and getting quotes from multiple lenders is always advisable to secure the most competitive rate.

Global Headwinds and Unforeseen Events

Beyond the domestic economic landscape, global events and geopolitical dynamics can introduce significant volatility into financial markets, consequently affecting mortgage rates. These factors often trigger shifts in investor sentiment and capital flows.

Geopolitical Stability and Investor Flight to Safety

Periods of global instability, such as geopolitical conflicts, trade wars, or widespread economic crises in major economies, often lead to a “flight to safety.” Investors tend to move their capital into less risky assets, and U.S. Treasury bonds are frequently considered one of the safest havens globally. Increased demand for U.S. Treasury bonds drives up their prices and, crucially, pushes down their yields. Since mortgage rates are often benchmarked to these yields, a flight to safety can paradoxically lead to lower mortgage rates, even amidst global turmoil.

However, prolonged instability can also create uncertainty about future economic growth and inflation, which might lead the Federal Reserve to adjust its monetary policy, potentially impacting rates in the opposite direction.

International Economic Performance

The economic health of other major global economies also matters. For instance, if large economies like China or the Eurozone face significant downturns, it can dampen global demand, reduce inflationary pressures worldwide, and potentially lead to a decrease in U.S. bond yields as investors seek stable investments. This could then translate to lower mortgage rates in the U.S. Conversely, strong global economic growth could contribute to higher inflation expectations and higher U.S. bond yields, thereby increasing mortgage rates.

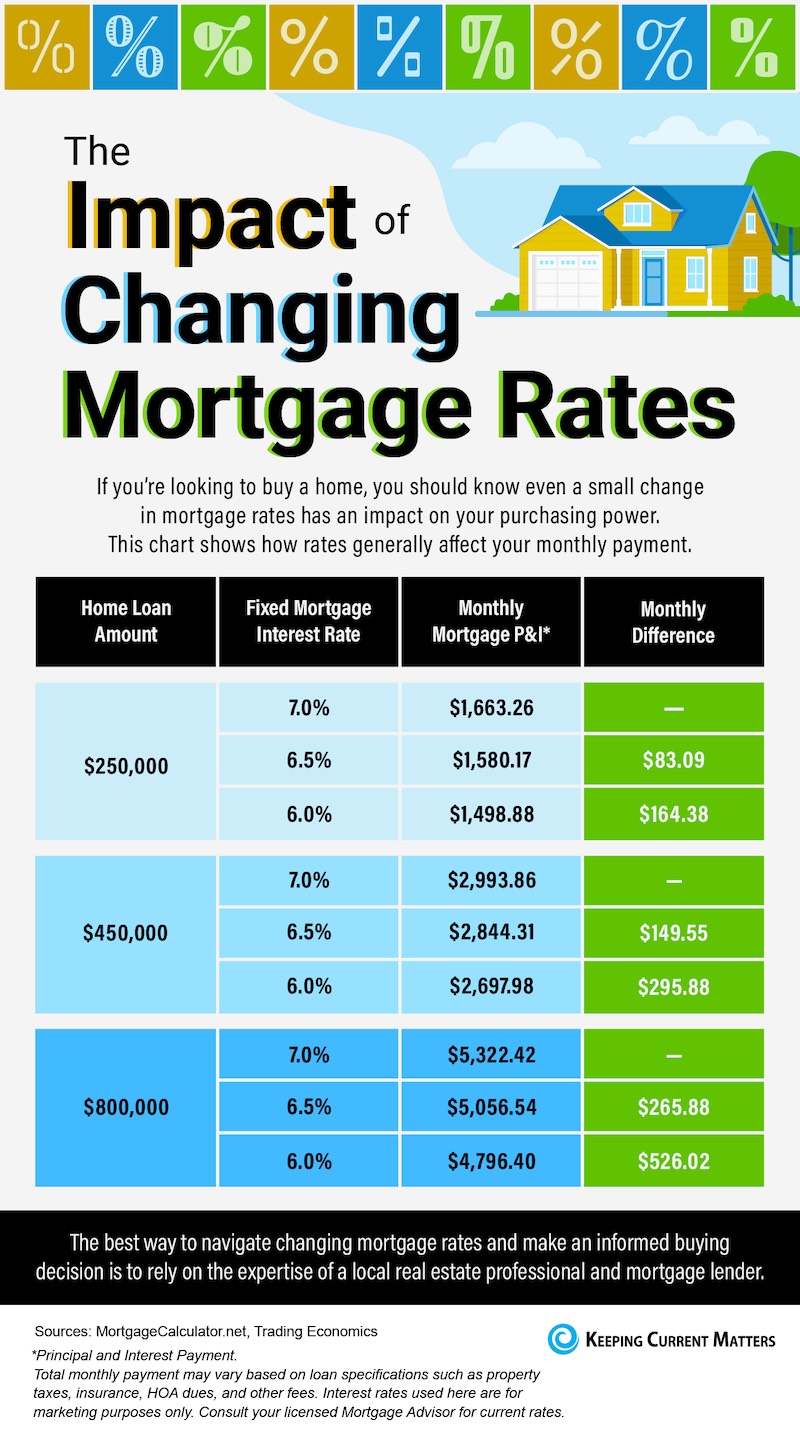

In conclusion, mortgage rates are a complex interplay of forces. From the commanding influence of the Federal Reserve’s monetary policy to the fundamental health of the domestic economy, individual borrower profiles, and even the ripple effects of global events, numerous factors converge to determine the cost of homeownership. A comprehensive understanding of these dynamics is essential for anyone looking to make strategic financial moves in the housing market.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.