In the intricate world of finance, few metrics hold as much sway over the economy and individual pocketbooks as the prime interest rate. Far from an obscure banking term, the prime rate is a foundational benchmark that directly influences the cost of borrowing for consumers and businesses alike. Understanding what it is, how it’s determined, and its far-reaching implications is not just for economists or financial professionals; it’s essential knowledge for anyone looking to make informed decisions about their money.

Today’s prime interest rate isn’t merely a number; it’s a dynamic reflection of monetary policy and economic health, impacting everything from your mortgage payments and credit card interest to a business’s ability to invest and expand. In this comprehensive guide, we’ll demystify the prime rate, explore its profound influence, and equip you with the insights needed to navigate its fluctuations.

Understanding the Prime Rate: A Core Financial Metric

At its heart, the prime interest rate represents the interest rate that commercial banks charge their most creditworthy corporate customers. It’s not a rate that’s individually negotiated for every loan, but rather a benchmark that other lending rates are often pegged to. Think of it as a base layer upon which other interest rates are built, reflecting the lowest risk lending scenario.

Defining the Prime Interest Rate

The prime rate is generally defined as the interest rate that commercial banks in the United States charge their most creditworthy corporate customers on short-term loans. While individual banks may theoretically set their own prime rates, in practice, the vast majority of U.S. banks maintain a uniform prime rate. This rate is usually published daily in financial news outlets and is critical for understanding broader economic trends. It’s an indicator of the general cost of money in the economy. When the prime rate is high, borrowing becomes more expensive, potentially slowing down economic activity. Conversely, a lower prime rate makes borrowing cheaper, often stimulating spending and investment.

Who Sets the Prime Rate? The Role of the Federal Reserve

While individual banks charge the prime rate, its ultimate determination is heavily influenced by the actions of the U.S. central bank: the Federal Reserve (the Fed). Specifically, the prime rate moves in lockstep with the Federal Funds Rate target range set by the Federal Open Market Committee (FOMC), the Fed’s principal monetary policymaking body.

The Federal Funds Rate is the target rate for overnight lending between banks. When the Fed raises or lowers its target for the Federal Funds Rate, commercial banks typically adjust their prime rate by the same amount. Historically, the prime rate has been approximately 3.00% higher than the upper bound of the Federal Funds Rate target range. This consistent spread reflects the additional risk and overhead banks incur when lending to their customers compared to overnight interbank lending. Thus, while no single entity “sets” the prime rate in isolation, the Fed’s monetary policy decisions are the primary catalyst for its changes.

Why the Prime Rate Matters to Everyone

The prime rate’s significance extends far beyond big corporations and financial institutions. Its movements ripple through the entire economy, touching individuals, small businesses, and large corporations alike. For individuals, it directly affects the interest rates on variable-rate mortgages, home equity lines of credit (HELOCs), auto loans, and many credit card products. A change in the prime rate can mean higher or lower monthly payments for those with variable-rate debt.

For businesses, especially small and medium-sized enterprises (SMEs), the prime rate is crucial. Many business loans, lines of credit, and even equipment financing options are tied to the prime rate. A favorable prime rate can make it cheaper for businesses to borrow money for expansion, inventory, or operational needs, fostering growth and job creation. Conversely, a rising prime rate can increase borrowing costs, potentially squeezing profit margins and slowing investment. In essence, the prime rate serves as a barometer for the cost of capital in the economy, influencing spending, saving, and investment decisions across the board.

The Mechanics Behind the Rate: How It’s Determined and Communicated

Understanding the prime rate requires delving into the underlying mechanisms that govern its shifts. It’s not an arbitrary number but rather the direct consequence of deliberate monetary policy decisions and market forces.

The Federal Funds Rate and Its Relationship to Prime

The cornerstone of the prime rate’s calculation is the Federal Funds Rate. This is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight, on an uncollateralized basis. The FOMC does not directly set the Federal Funds Rate; rather, it sets a target range for the rate. Through open market operations, primarily buying and selling government securities, the Federal Reserve influences the supply of reserves in the banking system, thereby guiding the actual Federal Funds Rate within its target range.

The prime rate, as mentioned, is almost always the upper bound of the Federal Funds Rate target range plus an additional 300 basis points (3.00%). For instance, if the FOMC sets the Federal Funds Rate target range at 5.00% to 5.25%, the prime rate would typically be 8.25% (5.25% + 3.00%). This stable spread highlights the direct and predictable link between the Fed’s policy and the rates consumers and businesses face. Any adjustment to the Federal Funds Rate target is almost immediately reflected in the prime rate published by banks.

The Federal Open Market Committee (FOMC) and Its Decisions

The decisions that ultimately drive the prime rate originate from the FOMC, which comprises twelve members: the seven members of the Board of Governors of the Federal Reserve System; the president of the Federal Reserve Bank of New York; and presidents of four other Federal Reserve Banks on a rotating basis. This committee meets eight times a year, approximately every six weeks, to assess economic conditions and determine the appropriate stance of monetary policy.

During these meetings, the FOMC analyzes a vast array of economic data, including inflation rates, employment figures, GDP growth, and global economic developments. Their primary mandates are to promote maximum employment and stable prices (low inflation). If inflation is too high, the FOMC might decide to raise the Federal Funds Rate target to slow down economic activity and cool price pressures. If the economy is sluggish and unemployment is rising, they might lower the rate to stimulate borrowing and investment. These decisions are highly anticipated by financial markets and have profound implications for interest rates across the economy, including the prime rate.

Where to Find Today’s Prime Rate

Given its importance, finding today’s prime interest rate is relatively straightforward. Most major financial news outlets, such as The Wall Street Journal, Bloomberg, and Reuters, publish the current prime rate daily. Many large banks also display their prime rate prominently on their websites. Additionally, financial data providers and economic research websites regularly update this information.

It’s important to note that while the prime rate is generally uniform across major U.S. banks, there can be slight variations or delays in reporting, though these are typically minor. When researching the prime rate, ensure you are looking at the current rate as determined by the Federal Reserve’s most recent FOMC announcement, as this will be the most accurate and widely adopted benchmark. Staying informed about the prime rate requires checking reliable financial news sources or directly consulting the Federal Reserve’s official publications.

Impact on Your Finances: Personal and Business Implications

The prime rate isn’t an abstract concept; it has tangible effects on the financial decisions and health of individuals and businesses every day. Understanding these impacts is crucial for strategic financial planning.

For Individuals: Loans, Mortgages, and Credit Cards

The influence of the prime rate on personal finance is pervasive. For homeowners, particularly those with adjustable-rate mortgages (ARMs), a change in the prime rate can directly alter monthly mortgage payments. While fixed-rate mortgages remain unaffected, ARMs typically adjust periodically (e.g., annually) based on a specified index, which often includes the prime rate or another rate that closely tracks it. Similarly, home equity lines of credit (HELOCs) are almost universally tied to the prime rate. If the prime rate rises, the interest rate on your outstanding HELOC balance will increase, leading to higher minimum payments and a greater overall cost of borrowing.

Credit cards, especially those with variable interest rates, are also highly sensitive to prime rate movements. The annual percentage rate (APR) on most variable-rate credit cards is calculated as the prime rate plus a margin set by the issuer. When the prime rate increases, so does the interest you pay on your credit card balances, making it more expensive to carry debt. For auto loans and personal loans, while many are fixed-rate, some variable-rate options do exist, and even fixed-rate offerings can see their initial rates influenced by changes in the broader interest rate environment, including the prime rate. Savvy individuals monitor the prime rate to anticipate changes in their debt obligations and plan accordingly, potentially opting to refinance or consolidate debt when rates are favorable.

For Businesses: Working Capital and Expansion

For businesses, the prime rate is a critical factor in their operational and growth strategies. Many business loans and lines of credit are structured with interest rates tied to the prime rate (e.g., “prime plus 1%”). A lower prime rate translates to reduced borrowing costs, making it cheaper for companies to finance daily operations, manage cash flow, purchase inventory, or cover short-term expenses. This reduction in overhead can free up capital for other investments or even contribute to higher profit margins.

When the prime rate is low, businesses are more inclined to borrow for expansion projects, such as investing in new equipment, facilities, or research and development. Cheaper capital encourages greater investment, which can lead to increased productivity, job creation, and economic growth. Conversely, a rising prime rate means higher borrowing costs, which can deter businesses from taking on new debt, potentially slowing down expansion plans, limiting hiring, and even increasing the risk of default for companies with significant variable-rate debt. Understanding and forecasting prime rate movements is therefore a key component of a business’s financial planning and risk management strategy.

Investment Landscape: Stocks, Bonds, and Savings

The prime rate also sends ripples through the broader investment landscape, influencing everything from the attractiveness of bonds to the valuation of stocks and the returns on savings.

For savings accounts, money market accounts, and certificates of deposit (CDs), a rising prime rate environment typically leads to higher interest payouts from banks. As the cost of borrowing increases for banks (due to higher Federal Funds Rate), they often pass on some of those increased returns to depositors to attract funds. This can make saving more attractive compared to other investments, especially for risk-averse individuals.

In the bond market, a rising prime rate generally correlates with rising bond yields. New bonds issued in a higher interest rate environment will offer better returns, which can make existing lower-yielding bonds less attractive, causing their prices to fall. Conversely, falling prime rates can make existing bonds with higher yields more valuable.

The stock market also reacts to prime rate changes, albeit more indirectly. Higher interest rates (driven by a higher prime rate) can increase borrowing costs for companies, which may reduce their earnings. Additionally, higher rates make risk-free investments like government bonds more attractive, potentially drawing capital away from the stock market. Certain sectors, such as financials (banks profit from higher rates), may benefit, while growth stocks (which often rely on future earnings and debt for expansion) might face headwinds. Lower rates, conversely, can stimulate economic growth and corporate profits, making stocks more appealing. Investors must therefore consider the prime rate’s trajectory when constructing and managing their portfolios.

Navigating a Changing Rate Environment: Strategies and Considerations

The prime rate is not static; it fluctuates in response to economic conditions and the Federal Reserve’s policy decisions. Adapting to these changes is critical for both personal and business financial health.

When Rates Rise: Adapting Your Financial Strategy

A rising prime rate environment signals that borrowing costs are increasing. For individuals, this is a call to action regarding variable-rate debt. Prioritize paying down credit card balances, HELOCs, and variable-rate loans to minimize the impact of higher interest payments. Consider refinancing variable-rate debt into fixed-rate alternatives if market conditions permit, locking in your payments before rates climb further. Review your budget to accommodate potentially higher monthly expenses and look for areas to cut back or increase income.

For businesses, rising rates necessitate a re-evaluation of debt. Explore hedging strategies to mitigate interest rate risk on variable-rate loans. Consider locking in financing for planned capital expenditures before rates become prohibitive. Businesses might also need to adjust pricing strategies or operational efficiencies to absorb higher borrowing costs without significantly impacting profitability. Tightening cash flow management and optimizing working capital become even more critical during these periods. Strategic planning in a rising rate environment focuses on reducing exposure to variable interest, enhancing efficiency, and carefully managing debt.

When Rates Fall: Seizing Opportunities

A declining prime rate, conversely, presents distinct opportunities. For individuals, this is an ideal time to refinance existing high-interest debt, such as mortgages, HELOCs, or personal loans, to secure lower interest rates and reduce monthly payments. This can free up cash flow, which can then be used for savings, investments, or accelerating debt repayment. Consider taking out new loans for large purchases, such as a home or vehicle, as borrowing costs will be lower. It’s also an opportune time to reassess investment strategies, as lower interest rates can make certain asset classes more attractive.

Businesses can leverage falling rates to their advantage by refinancing existing debt at more favorable terms, thereby reducing interest expenses and improving their bottom line. This can also be an excellent time to secure financing for expansion, new projects, or acquisitions at a lower cost of capital, stimulating growth and competitiveness. Companies might also consider increasing their inventory or investing in equipment, as the cost of borrowing to support these activities is reduced. For both individuals and businesses, a falling rate environment is a window of opportunity to optimize financial structures, reduce costs, and strategically invest for the future.

Long-Term Financial Planning with the Prime Rate in Mind

Beyond immediate reactions, understanding the prime rate’s cyclical nature is vital for long-term financial planning. This involves anticipating potential future movements and structuring your finances resiliently. For individuals, this means cultivating a strong emergency fund to weather unexpected increases in debt payments, and making informed choices about fixed versus variable-rate debt products based on your risk tolerance and financial outlook. Diversifying investments and regularly reviewing your portfolio’s sensitivity to interest rate changes are also key.

For businesses, long-term planning involves maintaining a healthy debt-to-equity ratio, developing robust cash flow projections, and having contingency plans for different interest rate scenarios. It also means building strong relationships with lenders to ensure access to capital during all economic cycles. Integrating prime rate forecasts into strategic planning helps businesses make prudent decisions about capital allocation, expansion, and risk management, fostering sustainable growth and resilience against economic headwinds.

Beyond Today: Historical Context and Future Outlook

The prime rate is a product of history, shaped by decades of monetary policy and economic cycles. Understanding its past trajectory provides valuable context for anticipating its future movements.

A Brief History of the Prime Rate in the U.S.

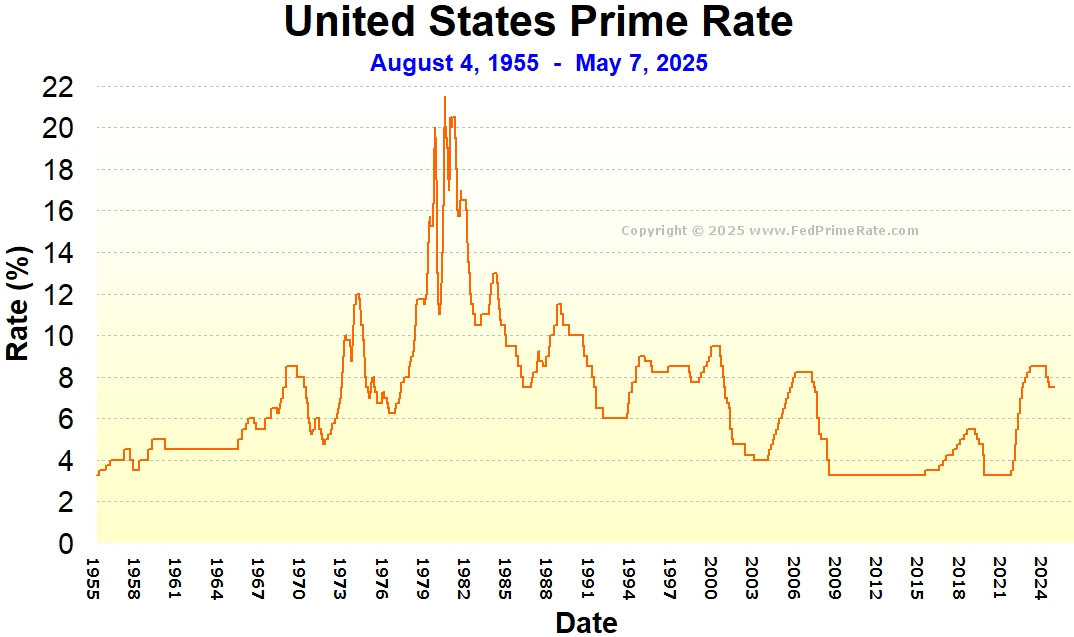

Historically, the prime rate has seen significant fluctuations, reflecting the economic booms, recessions, and policy responses of the U.S. Federal Reserve. In the late 1970s and early 1980s, under then-Fed Chair Paul Volcker, the prime rate soared to unprecedented levels, reaching over 20% to combat runaway inflation. This period was marked by severe economic strain but ultimately brought inflation under control. Conversely, following the 2008 financial crisis and during the COVID-19 pandemic, the Federal Reserve cut the Federal Funds Rate to near zero, causing the prime rate to drop to historically low levels (around 3.25%) in an effort to stimulate economic recovery.

These historical swings illustrate the Fed’s powerful role in steering the economy and the prime rate’s sensitivity to economic conditions, particularly inflation and unemployment. Analyzing past cycles helps financial professionals and individuals appreciate the dynamic nature of interest rates and the potential extremes they can reach under various economic pressures.

Factors Influencing Future Rate Movements

Predicting future prime rate movements involves analyzing a complex interplay of economic indicators and global events. The primary drivers remain inflation and employment. If inflation remains stubbornly high, the Fed is likely to keep interest rates elevated or even raise them further to cool price increases. Conversely, if economic growth slows significantly or unemployment rises, the Fed might consider cutting rates to stimulate activity.

Other factors include global economic conditions (e.g., geopolitical tensions, commodity prices, growth in major economies), fiscal policy (government spending and taxation), and financial market stability. The Fed constantly monitors these variables, and their public statements and economic projections (e.g., the “dot plot” that indicates FOMC members’ interest rate expectations) offer clues about potential future rate decisions. Staying informed about these economic indicators and the Fed’s communications is crucial for anticipating changes in the prime rate.

The Global Economic Interplay

While the U.S. prime rate is set domestically, it doesn’t operate in a vacuum. The global economy plays an increasingly important role in influencing the Federal Reserve’s decisions. Interest rate policies of other major central banks (e.g., the European Central Bank, Bank of England, Bank of Japan) can influence capital flows and exchange rates, which in turn can affect U.S. inflation and economic growth.

For instance, if other countries raise their rates significantly, it could attract capital away from the U.S., potentially putting downward pressure on the dollar and upward pressure on U.S. inflation, influencing the Fed’s stance. Similarly, global supply chain disruptions, international trade tensions, or worldwide economic downturns can all impact the U.S. economic outlook and, by extension, the prime rate. In an interconnected world, understanding the global economic interplay is an increasingly important dimension of comprehending the prime interest rate’s past, present, and future trajectory.

The prime interest rate, while seemingly just a number, is a powerful force that shapes the financial landscape for millions. It is the bedrock upon which much of our credit-based economy is built, directly influencing the cost of personal loans, business credit, and investment returns. By understanding its definition, how it’s determined by the Federal Reserve, its impact on your personal and business finances, and how to adapt to its fluctuations, you empower yourself to make more informed financial decisions. In a world where financial agility is paramount, knowledge of the prime rate isn’t just an advantage—it’s a necessity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.