Understanding the “average interest rate” on a mortgage is a fundamental, yet often complex, aspect of personal finance that can significantly impact a homeowner’s financial well-being. Far from being a static number, this figure is a dynamic reflection of broader economic forces, individual financial health, and the specific choices made during the loan application process. For first-time homebuyers, seasoned investors, or those considering refinancing, deciphering what an average rate entails – and, more importantly, what influences their personal average rate – is crucial for making informed decisions.

Mortgages represent one of the most substantial financial commitments most individuals undertake in their lifetime. Even a fraction of a percentage point difference in the interest rate can translate into tens of thousands of dollars saved or spent over the lifespan of a 15- or 30-year loan. Therefore, moving beyond a simple Google search result for “average mortgage rate today” requires a deeper dive into the mechanics that drive these numbers. This article will demystify the factors shaping mortgage rates, explore the different types of mortgage products, guide you on where to find accurate rate information, and outline strategies to secure the most favorable terms for your specific situation, all within the context of sound financial management.

Decoding the “Average”: Factors Influencing Mortgage Rates

The concept of an “average” mortgage rate is inherently fluid, shifting daily, sometimes hourly, in response to a myriad of interconnected factors. To truly grasp what constitutes a typical rate, one must appreciate the intricate dance between macroeconomic indicators, lender-specific policies, and individual borrower characteristics.

Economic Indicators

The broader economic landscape plays an outsized role in dictating the direction and magnitude of mortgage rates. These are the powerful currents that lenders and borrowers alike must navigate.

- Federal Funds Rate and Monetary Policy: While the Federal Funds Rate (the target rate for overnight lending between banks, set by the Federal Reserve) doesn’t directly dictate mortgage rates, it heavily influences them. Changes in this rate signal the Fed’s stance on inflation and economic growth. When the Fed raises rates, it generally makes borrowing more expensive across the economy, pushing mortgage rates upward. Conversely, rate cuts typically lead to lower mortgage rates.

- Inflation: Inflation erodes the purchasing power of money over time. Lenders, who are essentially “renting out” money, need to ensure that the return on their loans keeps pace with or exceeds inflation to maintain profitability. High inflation often leads to higher interest rates as lenders demand greater compensation for the reduced value of future repayments.

- Economic Growth and Employment: A robust economy, characterized by strong GDP growth and low unemployment, generally correlates with higher consumer confidence and increased demand for housing. This demand can put upward pressure on rates. Conversely, economic slowdowns or recessions might lead to lower rates as the Fed attempts to stimulate activity.

- Treasury Yields: The yield on the 10-year U.S. Treasury note is a particularly influential benchmark. Mortgage rates, especially for 30-year fixed-rate loans, often move in tandem with Treasury yields because both are long-term, fixed-income investments. When bond investors demand higher yields for Treasuries, mortgage rates tend to follow suit.

Lender-Specific Factors

Beyond the broader economy, individual lenders also have their own internal mechanisms that affect the rates they offer.

- Lender’s Overhead and Profit Margins: Every financial institution has operating costs, including employee salaries, technology, marketing, and regulatory compliance. These overheads, along with a desired profit margin, are factored into the interest rates offered to borrowers.

- Competition Among Lenders: The mortgage market is highly competitive. Lenders constantly adjust their rates and offerings to attract borrowers. In periods of fierce competition, lenders might trim their profit margins to offer more appealing rates, potentially pushing the “average” down.

- Loan Product Type: Different mortgage products carry different risk profiles and structures, which directly impacts their rates. For instance, a 15-year fixed-rate mortgage typically has a lower interest rate than a 30-year fixed-rate mortgage because the lender’s money is tied up for a shorter period, reducing their long-term interest rate risk. Similarly, government-backed loans (FHA, VA, USDA) often have different rate characteristics compared to conventional loans.

Borrower-Specific Factors

Crucially, the “average” rate you see advertised might not be the rate you actually receive. Your personal financial profile is a significant determinant.

- Credit Score: This is perhaps the most impactful borrower-specific factor. A higher credit score (e.g., FICO score of 740+) indicates a lower risk of default to lenders, allowing them to offer more favorable, lower interest rates. Conversely, a lower credit score will result in higher rates to compensate the lender for the increased risk.

- Down Payment Amount: The size of your down payment directly affects your loan-to-value (LTV) ratio. A larger down payment (e.g., 20% or more) means you’re borrowing less relative to the home’s value, reducing the lender’s risk and often resulting in a lower interest rate. A smaller down payment might require private mortgage insurance (PMI) and could lead to a higher rate.

- Debt-to-Income (DTI) Ratio: Your DTI ratio measures how much of your gross monthly income goes towards debt payments. Lenders use this to assess your ability to manage additional mortgage payments. A lower DTI (generally below 36-43%) signals greater financial stability and can help secure a better rate.

- Loan Term: As mentioned, a 15-year mortgage generally has a lower interest rate than a 30-year mortgage. While the monthly payments are higher on a 15-year loan, you pay significantly less interest over the life of the loan.

- Loan Amount and Conforming Limits: Loans that exceed the “conforming limits” set by Fannie Mae and Freddie Mac are considered jumbo loans. These often carry slightly different rates due to their higher risk profile and different secondary market dynamics.

Understanding Different Mortgage Rate Structures

Beyond the factors influencing the level of the interest rate, it’s equally important to understand the structure of the rate itself. The choice between different mortgage types can have profound implications for your monthly payments, long-term costs, and financial flexibility.

Fixed-Rate Mortgages (FRM)

The most common and straightforward mortgage product, a fixed-rate mortgage offers stability and predictability.

- Definition and Predictability: With an FRM, the interest rate remains constant for the entire duration of the loan, typically 15 or 30 years. This means your principal and interest payment will never change, regardless of market fluctuations.

- Common Terms (15-year vs. 30-year): The 30-year fixed mortgage is the most popular, offering lower monthly payments due to the extended repayment period. However, it accrues significantly more interest over the loan’s life. The 15-year fixed mortgage, while having higher monthly payments, saves borrowers a substantial amount in interest and allows for quicker homeownership.

- Pros and Cons: The primary advantage of an FRM is certainty; you are protected from rising interest rates. This makes budgeting easier and provides peace of mind. The main disadvantage is that if market rates fall significantly, you won’t benefit unless you refinance, which involves new closing costs.

Adjustable-Rate Mortgages (ARM)

ARMs offer a different risk-reward profile, potentially starting with lower payments but introducing future uncertainty.

- Definition, Initial Fixed Period, and Adjustment Frequency: An ARM starts with an initial fixed interest rate for a set period (e.g., 3, 5, 7, or 10 years). After this initial period, the rate adjusts periodically (e.g., annually) based on a specified financial index plus a fixed margin. Common ARMs are often structured as 5/1, 7/1, or 10/1, meaning the rate is fixed for the first 5, 7, or 10 years, then adjusts annually thereafter.

- Index and Margin: The adjustable rate is calculated by adding a fixed “margin” (determined by the lender at the time of origination) to a fluctuating “index” (e.g., SOFR – Secured Overnight Financing Rate). The index is what changes, causing the interest rate to adjust.

- Caps (Periodic, Lifetime): To protect borrowers from extreme rate hikes, ARMs include caps. A “periodic cap” limits how much the interest rate can change during each adjustment period. A “lifetime cap” sets the maximum interest rate the loan can ever reach over its entire term.

- Pros and Cons: ARMs often feature a lower initial interest rate compared to fixed-rate mortgages, leading to lower initial monthly payments. This can be attractive for borrowers who plan to sell or refinance before the fixed period ends, or those who expect their income to rise significantly. However, the risk lies in the uncertainty of future interest rate adjustments, which could lead to substantially higher payments if market rates climb.

Government-Backed Loans

These loans are insured or guaranteed by federal agencies, making them more accessible to certain borrowers, often with different rate structures and eligibility requirements.

- FHA Loans: Insured by the Federal Housing Administration, FHA loans are popular for first-time homebuyers and those with lower credit scores or smaller down payments (as low as 3.5%). While rates are generally competitive, FHA loans require both upfront and annual mortgage insurance premiums (MIP).

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, VA loans offer eligible veterans, service members, and surviving spouses the significant benefit of 0% down payment and often do not require private mortgage insurance. Their interest rates are typically among the lowest available due to the government guarantee.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed to promote homeownership in eligible rural and suburban areas. They offer 0% down payment options for low- to moderate-income borrowers and competitive interest rates, though they do carry guarantee fees similar to mortgage insurance.

Where to Find and Compare Current Mortgage Rates

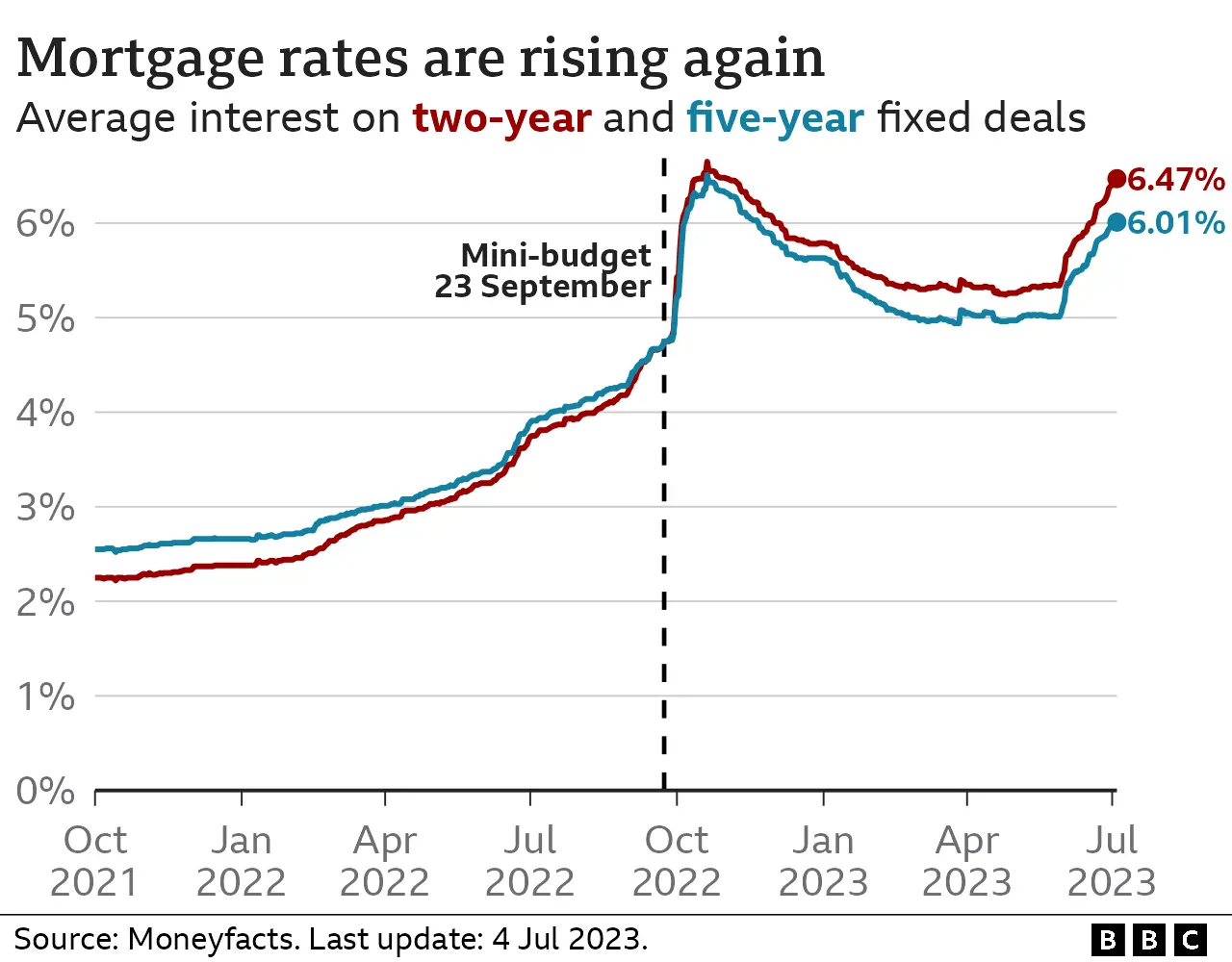

![]()

Finding the “average” rate is one thing; finding your best rate is another. The process of discovering competitive mortgage rates involves a combination of leveraging online tools and engaging directly with lenders.

Online Aggregators and Comparison Sites

The digital age has streamlined the initial research phase, providing a wealth of information at your fingertips.

- Benefits: Websites like Bankrate, LendingTree, and Zillow provide a convenient way to get a snapshot of current mortgage rates from multiple lenders simultaneously. They offer broad market views, allowing for quick comparisons based on general criteria (e.g., loan type, credit score range, down payment percentage). This can be a great starting point to gauge the general market temperature.

- Limitations: While useful for initial exploration, the rates displayed on these sites are often estimated or “teaser” rates. They may not reflect the exact rate you’d qualify for, as they can’t fully account for all your specific financial details. You’ll need to provide more personal information to get a firm, personalized quote.

Direct from Lenders

For accurate and personalized rates, direct engagement with financial institutions is indispensable.

- Banks (Large Institutions, Local Banks): Both large national banks (e.g., Chase, Wells Fargo) and smaller community banks offer mortgage products. Large banks often have robust online platforms and a wide range of products, while local banks might offer more personalized service and sometimes unique programs for local residents.

- Credit Unions: Credit unions are member-owned financial cooperatives and are often known for offering competitive interest rates and lower fees due to their non-profit status. Membership is typically required, but often easy to obtain.

- Mortgage Brokers: Unlike direct lenders, mortgage brokers act as intermediaries. They work with multiple lenders (wholesalers) and can shop your application around to find the best rate and terms that fit your profile. They are paid a commission (either by the lender or the borrower) and can be valuable for complex situations or when you want someone to do the legwork for you.

- Importance of Getting Personalized Quotes: The key takeaway is that you must get personalized quotes from several different lenders. This involves providing your Social Security number to allow a credit check (which will result in a “hard inquiry,” but multiple inquiries within a short period, typically 14-45 days depending on the scoring model, are usually treated as a single inquiry for rate shopping). This is the only way to compare apples-to-apples offers based on your unique financial situation.

Tools and Resources

Several financial tools can aid in your mortgage rate exploration.

- Mortgage Calculators: These online tools allow you to input different interest rates, loan terms, and down payments to estimate monthly payments, total interest paid, and amortization schedules. They are excellent for scenario planning.

- Pre-approval Process: Getting pre-approved for a mortgage is not only a crucial step for making an offer on a home but also an excellent way to get a firm, personalized interest rate quote. During pre-approval, the lender evaluates your credit, income, and assets, giving you a clear picture of how much you can borrow and at what rate. Some lenders may even allow you to “lock in” an interest rate during this stage, protecting you from rate increases for a specified period (e.g., 30-60 days) while you shop for a home.

Strategies for Securing a Favorable Mortgage Rate

Knowing what influences mortgage rates and where to find them is only part of the equation. Proactive strategies can significantly enhance your chances of securing the lowest possible interest rate, translating into substantial savings over the life of your loan.

Improving Your Financial Profile

Lenders assess risk, and a stronger financial profile signals lower risk, which translates directly into better rates.

- Boosting Your Credit Score: Prioritize improving your credit score months, or even a year, before applying for a mortgage. This involves paying all bills on time, reducing credit card balances to lower credit utilization (ideally below 30%), and avoiding opening new lines of credit. A higher FICO score demonstrates responsible financial behavior.

- Reducing Your Debt-to-Income (DTI) Ratio: Before applying, focus on paying down existing debts, especially high-interest consumer debt. A lower DTI (total monthly debt payments divided by gross monthly income) indicates you have more disposable income to comfortably handle a mortgage payment, making you a less risky borrower.

- Increasing Your Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, which is the amount you’re borrowing relative to the home’s appraisal value. A lower LTV means less risk for the lender. Aiming for 20% or more can often eliminate the need for private mortgage insurance (PMI) and frequently secures a lower interest rate.

Timing the Market (Cautiously)

While impossible to predict perfectly, understanding market trends can help.

- Understanding Market Trends: Keep an eye on economic indicators like inflation, unemployment, and the Federal Reserve’s monetary policy announcements. While no one can perfectly time the market, being aware of general trends can inform your decision on when to apply. For instance, if the Fed signals future rate hikes, securing a rate lock sooner might be prudent.

- Rate Locks: Once you’ve received a pre-approval or committed to a lender, inquire about a rate lock. A rate lock guarantees your interest rate for a specific period (e.g., 30, 45, or 60 days) while your loan application is processed. This protects you from rising rates. Be aware that some lenders might charge a fee for longer lock periods, or for a “float-down” option if rates drop significantly during your lock period.

Shopping Around and Negotiating

This is perhaps the most straightforward and effective strategy.

- Importance of Multiple Quotes: Do not settle for the first offer you receive. Contact at least three to five different lenders (banks, credit unions, mortgage brokers) and get personalized loan estimates (LEs). Compare the annual percentage rate (APR), which includes fees, to get a true comparison of the total cost of each loan.

- Leveraging Offers to Negotiate: Once you have multiple loan estimates, you can use a lower offer from one lender to negotiate with another, potentially getting them to match or beat a competitor’s rate or terms. Always ensure you are comparing identical loan products and terms.

Considering Points and Fees

Understanding closing costs can also impact your effective interest rate.

- Paying Points to Lower Interest Rate (Buy-Down): “Discount points” are fees paid upfront to the lender in exchange for a lower interest rate over the life of the loan. One point typically costs 1% of the loan amount. You’ll need to calculate the “break-even point” to determine if paying points is financially beneficial – how long it will take for the monthly savings to offset the upfront cost. This is often a good strategy if you plan to stay in the home for a long time.

- Understanding Closing Costs: Beyond points, be aware of all other closing costs, which can include origination fees, appraisal fees, title insurance, and more. While these don’t directly affect the interest rate, they are part of the total cost of the mortgage. Some lenders might offer a slightly higher rate in exchange for covering some of your closing costs.

Conclusion

The “average interest rate on a mortgage” is a crucial metric, yet it’s merely a starting point for understanding your unique financial journey into homeownership. It’s a dynamic figure influenced by the global economy, the specific lender, and, most importantly, your personal financial standing. By understanding the intricate interplay of economic indicators, lender policies, and your own creditworthiness, you empower yourself to navigate the mortgage market with confidence.

Whether you’re drawn to the predictability of a fixed-rate loan or the initial savings of an adjustable-rate mortgage, diligent research, proactive financial preparation, and savvy comparison shopping are your most potent tools. Take the time to bolster your credit, manage your debt, secure multiple personalized quotes, and strategically consider options like rate locks or paying points. Ultimately, the quest for the best mortgage rate is a personal finance project demanding patience, diligence, and informed decision-making. By mastering these elements, you not only secure a favorable interest rate but also lay a strong financial foundation for your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.