The question “how many banks are there in the US?” is more complex than it first appears, largely due to the dynamic nature of the financial industry and the varying definitions of what constitutes a “bank.” The number fluctuates constantly due to mergers, acquisitions, failures, and the rare formation of new institutions. What is clear, however, is a significant trend of consolidation over the past few decades, profoundly reshaping the American financial landscape. Understanding this number involves delving into regulatory classifications, historical trends, and the fundamental distinctions between various financial service providers.

Navigating the US Banking Landscape

The sheer size and complexity of the US financial system mean that a simple, static count of “banks” is elusive. The most common and authoritative figures typically refer to commercial banks and savings institutions insured by the Federal Deposit Insurance Corporation (FDIC). These institutions are the bedrock of the traditional banking system, offering deposit accounts, loans, and various financial services to individuals and businesses. However, the ecosystem extends beyond these chartered banks to include credit unions, which operate under a different model, and a burgeoning array of non-bank financial technology (FinTech) companies.

The Regulatory Framework Defining “Bank”

In the United States, the definition of a “bank” for official counting purposes largely falls under the purview of federal and state regulatory bodies. The FDIC, for instance, publishes a regular list of insured institutions, which includes both commercial banks and savings institutions (like savings banks and savings and loan associations). The Office of the Comptroller of the Currency (OCC) charters and supervises national banks and federal savings associations, while state banking departments oversee state-chartered banks. The Federal Reserve, meanwhile, plays a critical role in supervising bank holding companies and state-chartered member banks. This multi-layered regulatory environment means that an institution’s classification directly impacts its regulatory oversight and, consequently, how it is counted in official statistics. The data frequently cited reflects institutions holding a banking charter and offering traditional deposit and lending services, making them distinct from investment banks or other financial services firms that do not accept insured deposits.

The Shifting Sands of Bank Counts Over Time

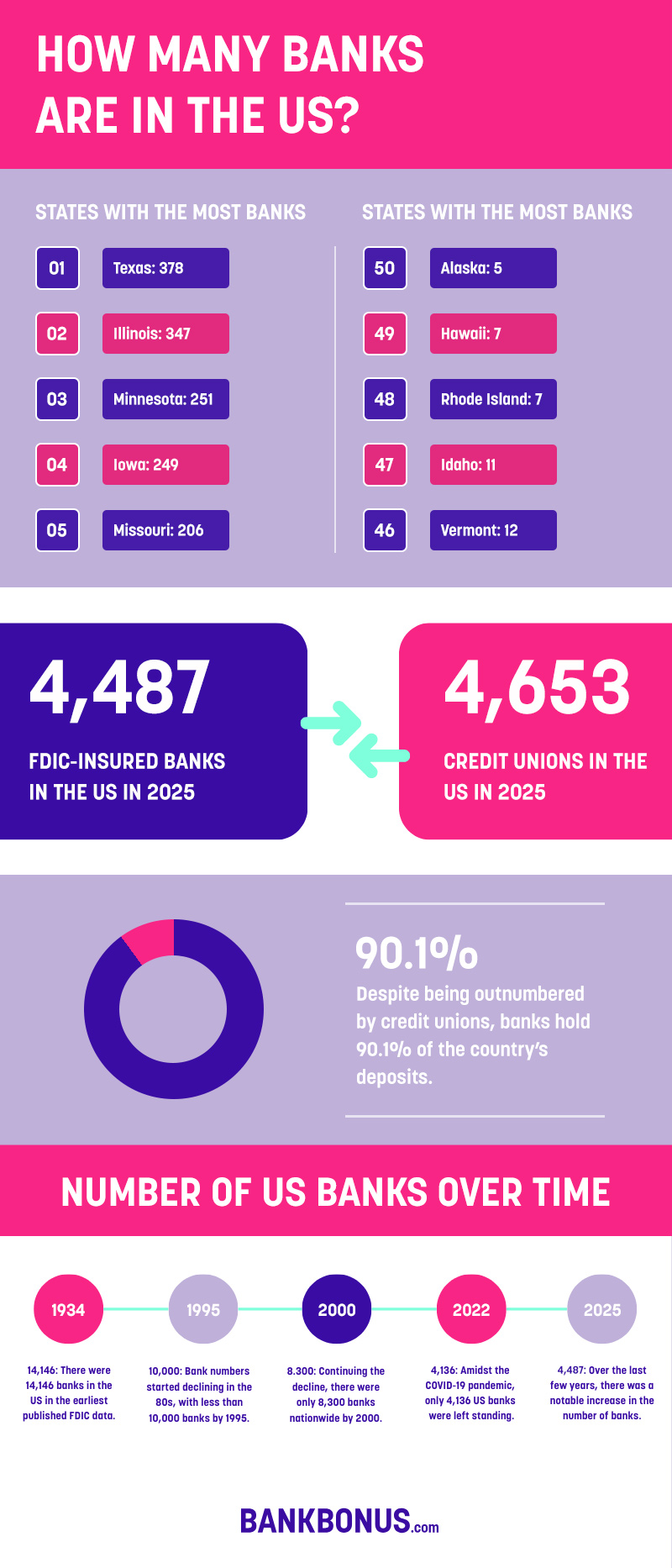

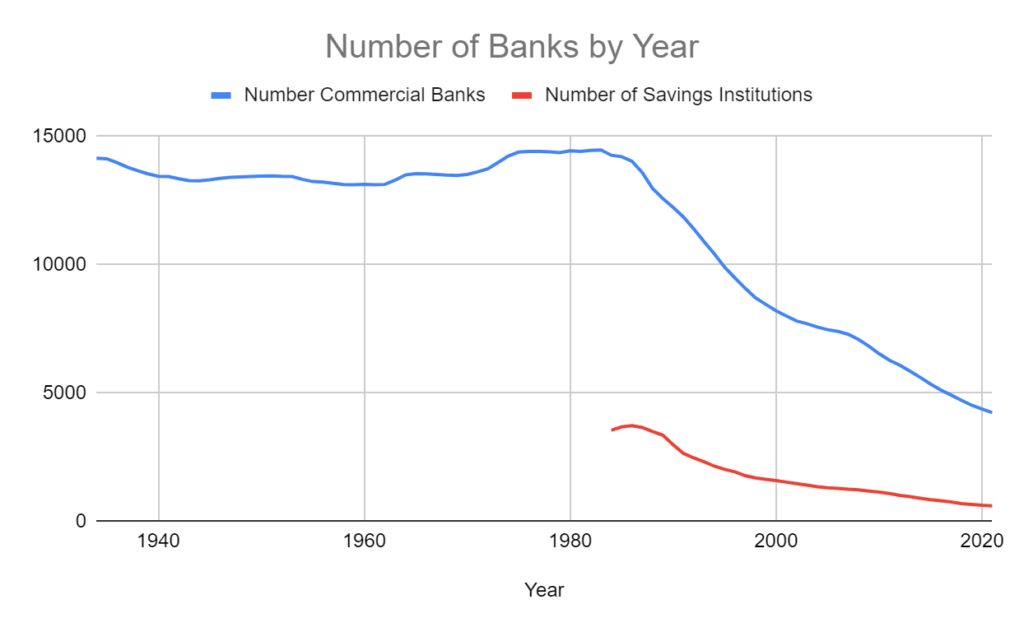

Historically, the US boasted a vast number of small, independent banks, often serving very specific local communities. In the early 1980s, the number of FDIC-insured commercial banks and savings institutions exceeded 14,000. This era was characterized by a highly fragmented banking system. However, beginning in the mid-1980s and accelerating in subsequent decades, a significant wave of consolidation swept through the industry. Deregulation, technological advancements, and economic pressures fueled a period of aggressive mergers and acquisitions. This trend has led to a dramatic reduction in the total number of banks, reaching a trough of just over 4,000 FDIC-insured institutions by the early 2020s. While new bank charters (known as “de novo” banks) have emerged, especially in the wake of the 2008 financial crisis, their numbers have been insufficient to counteract the overwhelming pace of consolidation. This persistent decline reflects a fundamental restructuring of the financial sector, moving towards fewer, larger, and often more technologically sophisticated entities.

Decoding the Numbers: Commercial Banks vs. Credit Unions

When discussing the number of “banks,” it’s crucial to differentiate between the two primary types of deposit-taking institutions: commercial banks and credit unions. While both offer similar services to consumers and businesses, their ownership structures, regulatory frameworks, and underlying philosophies are distinct, leading to separate counts and often different trends in their respective numbers.

Commercial Banks: Pillars of the Economy

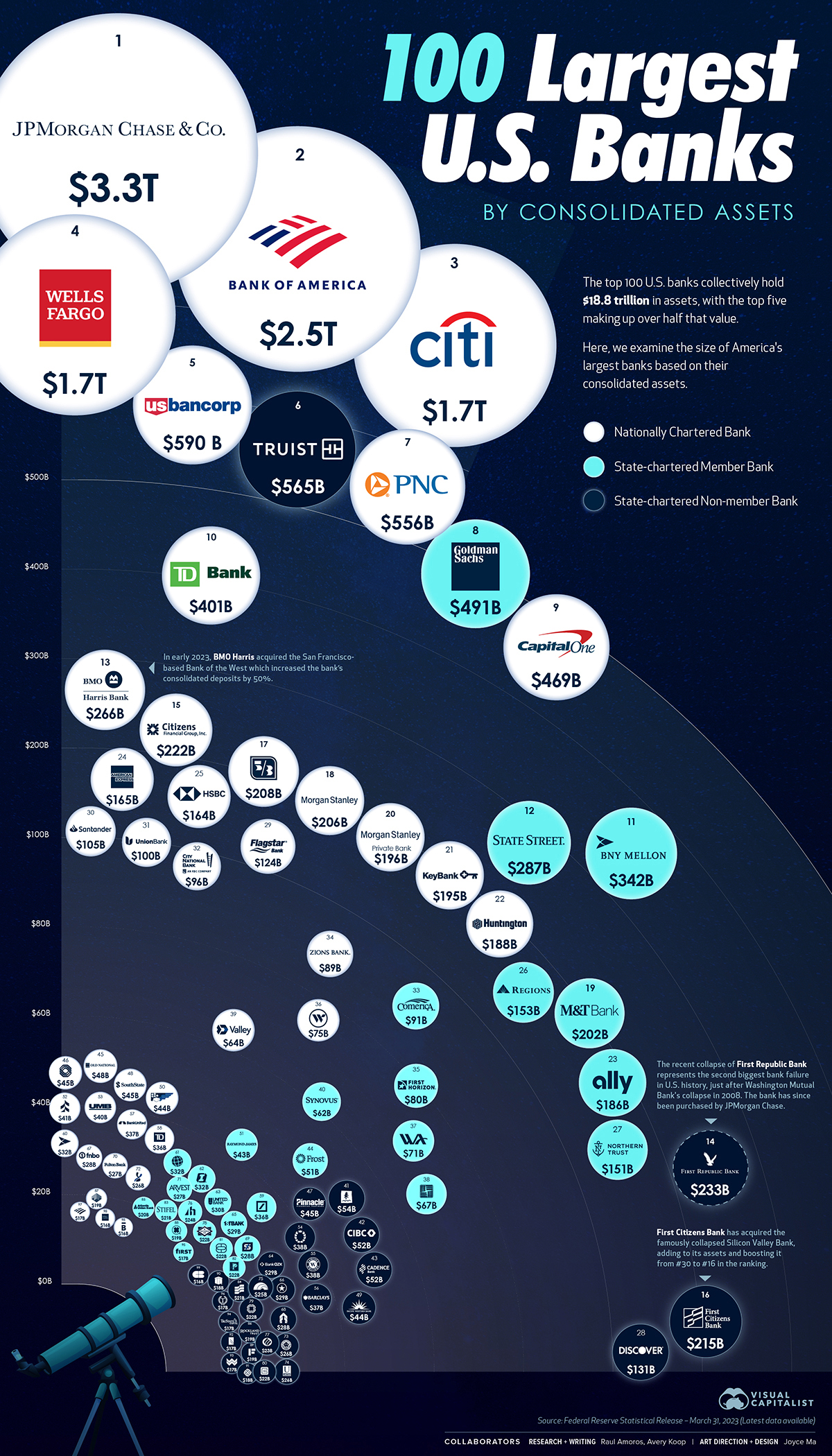

Commercial banks are typically for-profit entities, owned by shareholders, and are the most common type of institution counted in general banking statistics. They range dramatically in size, from global behemoths like JPMorgan Chase and Bank of America, which operate across states and continents, to regional banks serving multiple states, and thousands of community banks focused on specific towns or counties. Community banks, despite their smaller individual footprint, collectively play a vital role in local economies, often providing more personalized service and relationship-based lending. The number of commercial banks has seen the most significant decline over the past few decades due to the aforementioned consolidation. Factors such as the pursuit of economies of scale, the desire to expand market share, and the need to invest heavily in technology have driven larger institutions to acquire smaller ones. This trend has reduced competition in some areas but also arguably led to greater efficiency and financial stability across the sector.

Credit Unions: A Member-Owned Alternative

Credit unions offer a distinct model within the financial landscape. Unlike commercial banks, they are not-for-profit cooperative institutions owned by their members. Their primary mission is to serve their members, often providing lower fees on services and more favorable rates on savings and loans compared to traditional banks. Credit unions are chartered federally or by states and are insured by the National Credit Union Administration (NCUA), a federal agency similar to the FDIC. The number of credit unions has also seen a gradual decline, though not as steep as that of commercial banks. This decline is largely due to mergers among credit unions seeking to expand services or achieve efficiencies. However, new credit union formations are also less common than new bank formations, and their overall footprint remains significant, offering a valuable alternative for consumers seeking a member-centric financial institution.

Other Financial Entities and the Broader Ecosystem

Beyond traditional commercial banks and credit unions, the broader financial ecosystem includes other entities that perform bank-like functions. Savings and loan associations, sometimes referred to as thrifts, traditionally focused on mortgage lending and savings accounts but have largely converged with commercial banks in terms of services offered, and their numbers are often included in the broader FDIC-insured institution count. Industrial Loan Companies (ILCs) are another niche category, often owned by commercial companies (like car manufacturers or retail chains) and can accept deposits and make loans, operating under specific state charters. More recently, the rise of FinTech companies has blurred the lines further. While many FinTechs partner with existing banks to offer services, some are beginning to acquire bank charters or operate under specialized lending licenses, effectively competing with traditional banks without being counted as such in all statistical analyses. This evolving landscape means that the total number of entities providing core banking services is arguably much higher and more diverse than the count of traditional, chartered banks.

Key Drivers Behind Banking Consolidation and Evolution

The dramatic shift in the number of US banks is not accidental; it is the result of powerful economic, regulatory, and technological forces. Understanding these drivers is essential to grasp the current state and future trajectory of the banking sector.

Mergers and Acquisitions: The Dominant Force

The primary reason for the decline in the number of banks is the relentless pace of mergers and acquisitions (M&A). Banks engage in M&A for a variety of strategic reasons: to achieve economies of scale and reduce operational costs, to expand their geographic reach or customer base, to acquire specific technological capabilities, or to gain access to new markets. Larger institutions often view smaller community banks as attractive targets, acquiring their deposit bases, loan portfolios, and local expertise. While M&A can lead to increased efficiency and stronger financial institutions, it also raises concerns about reduced competition, particularly in local markets, and the potential for a more impersonal banking experience for consumers accustomed to community-focused services.

Regulatory Burdens and Compliance Costs

Following major financial crises, particularly the 2008 meltdown, the regulatory environment for banks has become significantly more complex and stringent. Legislation like the Dodd-Frank Act introduced extensive new rules regarding capital requirements, liquidity, consumer protection, and risk management. While these regulations are crucial for maintaining financial stability, they impose substantial compliance costs. Smaller banks, in particular, often struggle to bear the financial and human resource burden of navigating these complex requirements. This disproportionate impact can make it difficult for them to compete effectively, sometimes pushing them towards being acquired by larger institutions that have the resources to manage extensive compliance departments. This regulatory pressure effectively raises the barrier to entry for new banks and increases operating costs for existing smaller ones.

Technological Advancements and FinTech Competition

The digital revolution has fundamentally transformed the banking industry. Consumers increasingly expect seamless online and mobile banking experiences, advanced payment solutions, and personalized financial tools. Meeting these expectations requires significant and continuous investment in technology infrastructure, cybersecurity, and skilled IT personnel. Smaller banks often lack the capital and expertise to compete with larger banks or agile FinTech companies in this arena. The rise of FinTech has also introduced new competition in areas traditionally dominated by banks, such as lending, payments, and wealth management. Companies like PayPal, Square, and various online lenders have carved out significant market shares, forcing traditional banks to innovate or risk losing customers. This technological imperative and competitive pressure act as another catalyst for consolidation, as smaller players find it challenging to keep pace independently.

De Novo Charters: A Glimmer of New Growth

Despite the overwhelming trend of consolidation, there is a small but steady stream of new bank formations, known as “de novo” banks. These are entirely new institutions, typically formed by experienced bankers, entrepreneurs, or local community leaders who see an unmet need in the market. Many de novo banks are community-focused, aiming to serve specific niches or geographic areas that might be underserved by larger banks. However, establishing a new bank is a challenging and capital-intensive endeavor. It requires navigating a rigorous regulatory approval process, raising substantial capital, and building a customer base from scratch. While their numbers are far fewer than the banks that are acquired or fail, the continued formation of de novo institutions indicates a persistent demand for localized, relationship-based banking and a belief among some entrepreneurs that there are viable opportunities to innovate within the traditional banking framework.

The Broader Implications for Consumers, Businesses, and the Economy

The changing number of banks in the US has profound implications that extend far beyond the banking sector itself, impacting individual consumers, small and large businesses, and the overall economic landscape.

Impact on Competition and Access to Services

A reduction in the number of banks generally leads to decreased competition. Fewer competitors in a market can potentially result in higher fees, less attractive interest rates on deposits and loans, and fewer product choices for consumers. In some rural or underserved areas, the closure of a local community bank or credit union branch can leave residents with limited or no physical access to financial services, forcing them to rely on online banking or travel long distances. While digital banking offers convenience, it may not adequately serve all demographics, particularly those less comfortable with technology or without reliable internet access. The concentration of banking assets in fewer, larger institutions also raises concerns about the potential for systemic risk, as the failure of a single giant bank could have cascading effects throughout the economy.

Lending Landscape for Small Businesses

Small businesses, often the engine of job creation and local economic growth, are particularly sensitive to changes in the banking landscape. Unlike large corporations that can access capital markets, small businesses frequently rely on local banks for loans, lines of credit, and business banking services. Community banks, in particular, are known for their relationship-based lending, where loan officers understand the local economy and the specific needs of small business owners. As community banks decline in number, small businesses may find it harder to secure financing, especially those without extensive credit histories or who operate in niche industries. Larger banks, while offering sophisticated products, may rely more on standardized underwriting criteria that can sometimes overlook the unique circumstances of smaller enterprises. This shift could stifle entrepreneurship and hinder local economic development.

Financial Stability and Systemic Risk

The debate over the ideal number and size of banks often centers on financial stability. Proponents of consolidation argue that larger banks are more diversified, better capitalized, and more resilient to economic shocks. They can also invest more heavily in risk management systems and technology. Conversely, critics argue that “too big to fail” institutions pose a greater systemic risk; if one of these giants falters, the ripple effect on the entire financial system and economy could be catastrophic. A system with a diverse array of banks—including numerous small, independent institutions—might distribute risk more broadly. If one small bank fails, the impact is localized, whereas the failure of a large, interconnected institution can trigger a crisis. The ongoing challenge for regulators is to strike a balance between promoting efficiency and innovation while mitigating systemic risks associated with consolidation.

The Future Trajectory of the US Banking Sector

The US banking sector is in a continuous state of evolution, driven by technological advancements, changing consumer expectations, and an adaptive regulatory environment. The future will likely see a continuation of current trends, alongside the emergence of new models and challenges.

Digitalization and Hyper-Personalization

The acceleration of digital transformation is inevitable. Banks will continue to invest heavily in online and mobile platforms, artificial intelligence, and data analytics to offer seamless, personalized banking experiences. This includes everything from instant account opening and digital lending to AI-powered financial advice and highly customized product recommendations. The future bank will be increasingly integrated into customers’ digital lives, offering proactive financial management rather than merely reactive transaction processing. This shift will require banks to become more like technology companies, constantly iterating and innovating to meet the demands of a digitally native customer base.

The Rise of Niche and Challenger Banks

While overall consolidation among traditional banks may continue, the ecosystem is also witnessing the emergence of specialized “niche” banks and “challenger” banks. These often digitally native institutions target specific demographics (e.g., Gen Z, freelancers, specific ethnic groups) or offer highly specialized services (e.g., sustainable banking, crypto-friendly accounts). Some FinTech companies are actively pursuing bank charters to offer a full suite of services, blurring the lines between technology providers and traditional financial institutions. This trend suggests that while the overall number of large, general-purpose banks might decrease, the diversity of financial service providers will likely increase, catering to a wider array of customer needs and preferences that larger, more traditional banks may struggle to serve profitably.

Regulatory Innovation and Adaptation

The regulatory framework will need to adapt to this evolving landscape. Regulators are increasingly exploring concepts like “regulatory sandboxes,” which allow FinTech firms and new bank models to test innovative products and services in a controlled environment, fostering innovation while managing risk. There’s also an ongoing discussion about how to regulate non-bank financial entities that perform bank-like functions, ensuring consumer protection and financial stability across the entire ecosystem. As technology advances and new business models emerge, regulators will be tasked with balancing the need to prevent systemic risk and ensure fair competition with the imperative to encourage innovation and ensure equitable access to financial services for all Americans. The question of “how many banks” will remain dynamic, but the broader discussion will increasingly center on the types of financial service providers and their collective impact.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.