In the intricate world of personal finance, certain pieces of information act as the bedrock for nearly every transaction. Among these, your bank’s routing number and your personal account number stand out as essential identifiers, critical for everything from receiving your paycheck to setting up automated bill payments. While these numbers are fundamental to modern banking, it’s surprisingly common for individuals to not know them off-hand or to struggle with locating them when needed.

Understanding where to find these crucial identifiers, as well as their significance and how to protect them, is a cornerstone of effective financial management. This article will guide you through the most reliable methods for locating your routing and account numbers, shed light on their purpose, and offer best practices for their secure handling.

Understanding Routing and Account Numbers: The Foundation of Financial Transactions

Before diving into where to find these numbers, it’s vital to grasp what they are and why they are indispensable. Think of them as the precise coordinates for your financial destination. Without them, money would simply float in a digital void.

What is a Routing Number?

A routing number, also known as an ABA (American Bankers Association) routing transit number, is a nine-digit code that identifies your specific financial institution. It’s like the bank’s unique zip code, enabling funds to be directed to the correct bank during interbank transactions.

- Definition and Purpose: This 9-digit number is primarily used for Automated Clearing House (ACH) transactions, such as direct deposits, direct debits, and electronic transfers between banks. It’s also required for wire transfers, though sometimes a different routing number or specific wire transfer instructions might be used depending on the bank and the nature of the transfer (domestic vs. international). The ABA assigns these numbers, ensuring each bank has a unique identifier for transaction processing.

- Regional Variations: While most banks use one primary routing number, some larger institutions might have different routing numbers for specific regions or types of transactions (e.g., one for checking, one for savings, or distinct ones for wire transfers versus ACH). It’s crucial to verify the correct routing number for the specific type of transaction you’re undertaking. If in doubt, contacting your bank is always the safest bet.

- Importance for Different Transaction Types: For direct deposits and automated payments, the standard ACH routing number is almost always what you need. For wire transfers, particularly international ones, the process can be more complex, sometimes requiring a SWIFT/BIC code in addition to, or instead of, a routing number, along with specific intermediary bank details.

What is an Account Number?

Your account number is a unique string of digits—typically 10 to 12 digits, though it can vary—that identifies your specific checking, savings, or money market account within your financial institution. While the routing number points to the bank, the account number directs funds to your particular account at that bank.

- Definition and Purpose: This number is the individual identifier for your personal funds. Every transaction into or out of your account relies on this number to ensure the money lands in or departs from the correct place. It’s what distinguishes your checking account from your savings account, or your account from someone else’s at the same bank.

- Security Considerations: Due to its specificity, your account number is highly sensitive information. Coupled with a routing number, it enables financial transactions. Therefore, safeguarding your account number is paramount to preventing unauthorized access or fraud.

Why You Need Them: Common Scenarios

You’ll find yourself needing your routing and account numbers in a variety of common financial situations:

- Setting up Direct Deposit: This is perhaps the most frequent need. Employers, government benefit agencies (like Social Security), and other payers require these numbers to deposit funds directly into your bank account.

- Paying Bills Online: Many utility companies, landlords, or service providers allow you to set up automatic payments directly from your bank account, which requires providing these numbers.

- Setting Up Automatic Transfers: If you want to regularly move money between your own accounts (e.g., from checking to savings) at different institutions, or to an investment account, you’ll need these details.

- Sending or Receiving Wire Transfers: For larger or time-sensitive transfers, wire transfers are often used. Both sending and receiving parties will need the correct routing and account information.

- Linking External Accounts: Many budgeting apps, investment platforms, or peer-to-peer payment services will require these numbers to securely link your bank account for transfers.

Your Bank Statement: The Most Reliable Source

For many, the bank statement is the first and most accessible place to find both your routing and account numbers. Whether you receive paper statements or opt for digital versions, this document is designed to provide a comprehensive overview of your account activity, including these vital details.

Locating the Information on Paper Statements

If you receive traditional paper bank statements in the mail, locating your routing and account numbers is typically straightforward.

- Visual Guide: Most banks print both numbers prominently on the statement. Look towards the bottom of the statement or in a dedicated “Account Summary” box, usually on the first page. The routing number is almost always a 9-digit code, while your account number will be longer. Sometimes, the routing number is labeled explicitly as “ABA Routing Number.”

- Consistency: The placement might vary slightly from bank to bank, but the numbers will consistently be present. Take a moment to familiarize yourself with their location on your statement for future reference.

Accessing Digital Statements Online

For those who’ve embraced paperless banking, digital statements are equally, if not more, convenient.

- Logging into Your Online Banking Portal: The first step is to log into your bank’s official website using your secure credentials.

- Navigating to “Statements” or “Documents”: Once logged in, look for a section typically labeled “Statements,” “Documents,” “eStatements,” or “Account Activity.”

- Downloading PDFs: Most online banking platforms allow you to view or download PDF versions of your past statements. These digital versions are identical to their paper counterparts and will contain your routing and account numbers in the same locations. Downloading them provides a reliable, archivable record.

- Benefits of Digital Access: Digital statements offer immediate access, reduce clutter, and are generally more secure than physical mail. They also make it easy to quickly find historical data without digging through physical files.

Online Banking & Mobile Apps: Instant Access at Your Fingertips

In today’s digital age, your bank’s online portal and mobile app are often the quickest ways to access your financial information, including your routing and account numbers. These platforms are designed for convenience and real-time access.

Using Your Bank’s Website

Your bank’s website is usually the go-to resource for detailed account information.

- Login Process: Begin by securely logging into your online banking account with your username and password. Always ensure you are on your bank’s legitimate website (check the URL and for “https://”).

- Common Sections to Check: Once logged in, navigate to your account summary page. Look for specific links or sections such as “Account Details,” “View Account Information,” “Profile,” or sometimes a dedicated “Direct Deposit Information” link. Banks usually want to make it easy for you to find these details.

- Direct Display: Many banks will display your routing number and a masked (e.g., showing only the last few digits) or full account number directly on the account summary page or within the “Account Details” section for a specific account (checking, savings, etc.). You may need to click a “show full number” or “reveal” button for security purposes.

Navigating Your Mobile Banking App

Mobile banking apps have revolutionized how we interact with our money, offering unparalleled convenience.

- Similar Steps to Online Banking: The process mirrors online banking, but is optimized for smaller screens and touch interaction. Log into your bank’s official mobile app using your credentials or biometric authentication (fingerprint, facial recognition).

- Typical Locations: Within the app, select the specific account you need information for (e.g., your checking account). Look for options like “Account Details,” “Show Account Info,” “Routing & Account Numbers,” or a dedicated “Direct Deposit” section. These are usually found by tapping on the account itself from the main dashboard.

- Security Features: Mobile apps often incorporate enhanced security features like multi-factor authentication and biometric logins, making them a secure way to access sensitive financial data on the go. Always ensure your app is updated to the latest version for optimal security.

Alternative Methods: When Digital Access Isn’t an Option

While digital tools are incredibly convenient, there might be situations where you don’t have internet access, or prefer a physical reference. Fortunately, there are other reliable ways to find your routing and account numbers.

Checking Your Physical Checks

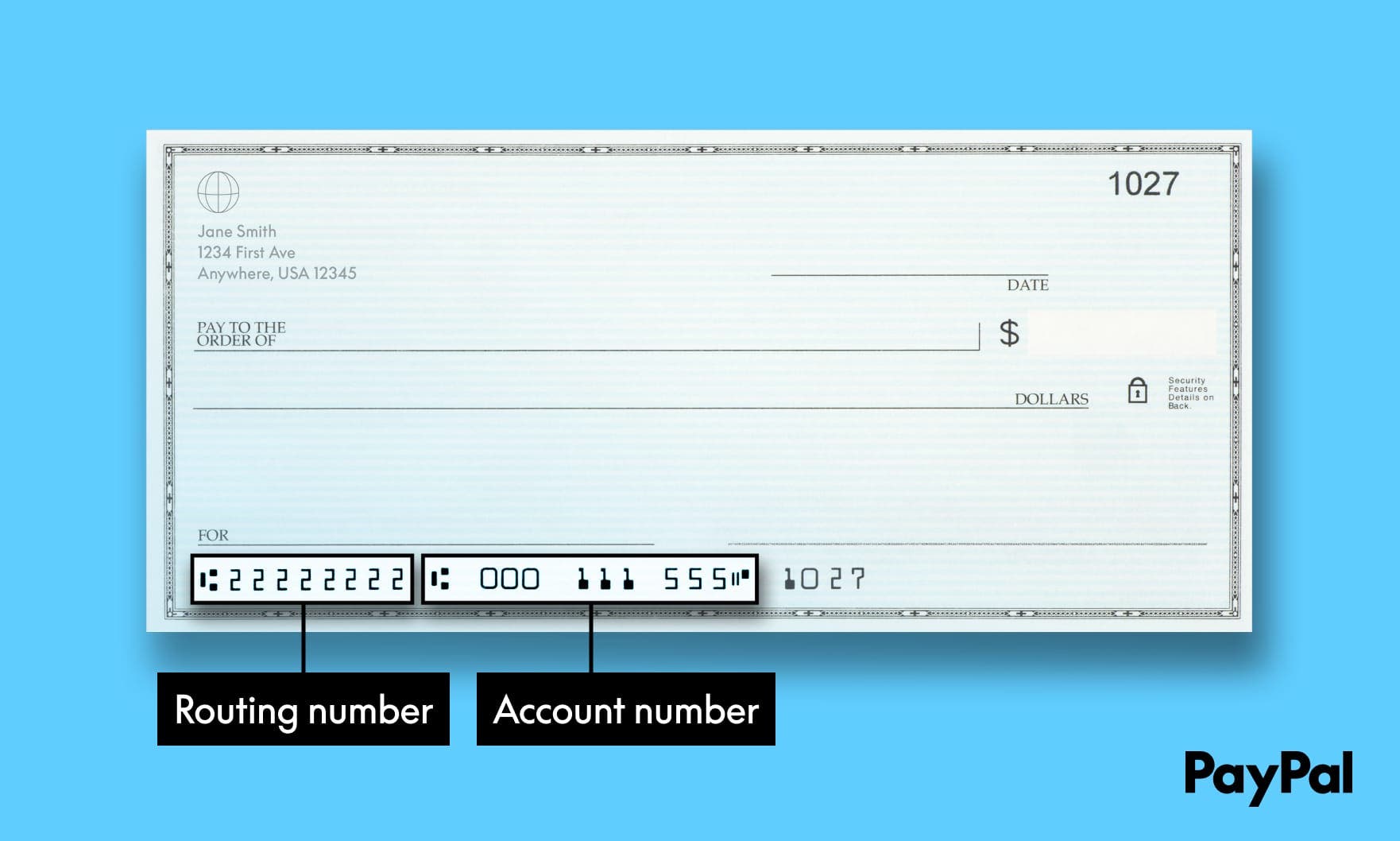

For checking accounts, your physical checks are a classic and very direct source of this information.

- Visual Guide: Look at the bottom of one of your personal checks. You’ll typically see three sets of numbers printed in a special magnetic ink (MICR line).

- The routing number is the first set of nine digits on the far left.

- Your account number is the middle set of numbers.

- The check number is the last set of numbers on the far right.

- Caution for Other Account Types: It’s important to note that checks only show the routing and account number for the checking account linked to that specific checkbook. If you need details for a savings account or money market account, a check won’t help. Also, for some business checks, the full account number might not be printed on the check itself, but rather on the check stub or associated documentation. Always double-check what you’re seeing.

Contacting Your Bank Directly

When all else fails, or if you prefer speaking to a representative, your bank’s customer service is an excellent resource.

- Customer Service Phone Number: The easiest way to reach them is by phone. You can usually find your bank’s customer service number on the back of your debit card, on any bank statement, or prominently displayed on their official website.

- In-Person Visit to a Branch: If you prefer face-to-face interaction, visit your local bank branch. A teller can provide you with your routing and account numbers after verifying your identity. Remember to bring a valid form of identification, such as a driver’s license or passport.

- Using Secure Messaging Services: Many online banking portals and mobile apps offer a secure messaging or chat feature. This can be a convenient way to ask for your account details without needing to make a phone call, as long as you can securely log in.

- Identity Verification: Be prepared to answer security questions and provide personal information (like your full name, address, date of birth, and possibly the last four digits of your Social Security number) to verify your identity. This is a crucial security measure to protect your financial data.

Security & Best Practices: Protecting Your Financial Information

While routing and account numbers are essential for managing your money, they are also sensitive data. Understanding how to protect them is as important as knowing how to find them.

Why Security Matters

The combination of your routing number and account number is powerful. While a routing number alone isn’t enough to compromise your account, when paired with your account number, it allows for money to be moved, primarily through ACH debits.

- Risk of Fraud and Identity Theft: If these numbers fall into the wrong hands, particularly through phishing scams or data breaches, unauthorized transactions can occur. Scammers can use this information to set up fraudulent direct debits, potentially draining your account or making unauthorized payments.

- Distinguishing Information: It’s important to understand that providing your routing and account number generally allows someone to deposit money into your account (e.g., direct deposit from an employer) or debit money from it (e.g., an automated bill payment you authorized). For someone to withdraw cash or perform other types of transactions, they would typically need additional information, such as your debit card PIN or online banking login credentials. However, the risk of unauthorized debits remains significant.

Safely Storing and Sharing Your Numbers

Prudent handling of your financial information is key to preventing fraud.

- Only Share with Trusted Parties: Only provide your routing and account numbers to legitimate and trusted entities, such as your employer, utility companies, government agencies, or established financial institutions when setting up authorized payments or direct deposits.

- Avoid Unsecured Communication: Never send your routing and account numbers via unsecured email, text message, or over public Wi-Fi networks. If you must send them digitally, use secure messaging platforms or encrypted documents, and ideally, only to known and verified recipients.

- Be Wary of Phishing Scams: Be highly suspicious of unsolicited requests for your banking information, whether by email, phone, or text. Banks will rarely ask for your full account number via email or text message. Always verify the authenticity of such requests directly with your bank using a known contact number.

- What to Do if You Suspect Compromise: If you believe your routing or account numbers have been compromised, contact your bank immediately. They can monitor your account for suspicious activity, place alerts, and guide you through the process of securing your funds and identity.

Verifying Information for Wires and Large Transfers

For high-value transactions like wire transfers, an extra layer of verification is essential.

- Always Double-Check: Before initiating any wire transfer, meticulously double-check every digit of the routing and account number with the recipient. A single incorrect digit can send funds to the wrong account, which can be incredibly difficult, if not impossible, to recover.

- Confirm via Separate Method: For significant transfers, particularly to new recipients or if the information was provided via email, always confirm the banking details by speaking directly with the recipient over a verified phone number. Do not rely solely on email, as business email compromise (BEC) scams are prevalent, where fraudsters intercept communications and alter banking details.

Conclusion

Your routing and account numbers are vital components of your financial identity, enabling the seamless flow of money in today’s digital economy. Whether you’re setting up direct deposit, paying bills, or transferring funds, knowing how to locate these numbers is a fundamental personal finance skill.

From the familiarity of a paper bank statement to the convenience of online banking portals and mobile apps, or the tried-and-true method of checking your physical checks or contacting your bank directly, multiple avenues exist to access this information. Crucially, remember that with great convenience comes great responsibility. Safeguarding these numbers through smart practices and vigilance against scams is paramount to protecting your financial well-being. By understanding where to find them and how to keep them secure, you empower yourself to navigate your financial life with confidence and control.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.