Applying for a new credit card is a significant step in managing your personal finances, offering benefits ranging from rewards points to enhanced purchasing power and crucial credit building. For many, Chase stands out as a top issuer, offering a diverse portfolio of cards tailored for various financial needs, from travel enthusiasts to small business owners. Once an application is submitted, a period of anticipation often follows. Understanding the precise status of your application with Chase is not just about impatience; it’s about informed financial planning. Knowing where your application stands allows you to plan your next financial moves, whether that involves further applications, credit score adjustments, or simply awaiting your new card. This guide delves into the various methods available to check your Chase credit card application status, offering insights into what each status means and how to navigate the post-application phase effectively.

Understanding the Credit Card Application Process and Its Timeline

When you submit a credit card application to Chase, whether online or in person, it initiates a comprehensive review process. This process is designed to assess your creditworthiness, identity, and overall financial profile against Chase’s lending criteria. Initially, an automated system performs a preliminary check, often pulling information from credit bureaus such as Experian, Equifax, and TransUnion. This rapid assessment helps determine if you meet basic eligibility requirements. However, not all applications receive an instant decision. Many require further manual review by an underwriter, particularly if there are nuances in your credit history, recent financial activity, or if the application flags any non-standard information.

The timeline for receiving a decision from Chase can vary. Some applicants receive an instant approval or denial within minutes. Others might find their application status remains “pending” for several days, or even up to two weeks, while Chase gathers additional information or conducts a more in-depth review. This waiting period can be frustrating, especially if you’re eager to utilize a new card’s benefits or need the credit line for an upcoming expense. It’s during this time that proactively checking your application status becomes crucial. Understanding that “pending” doesn’t necessarily mean “denied” can alleviate anxiety and empower you to take necessary follow-up actions if required. Chase, like other major issuers, aims for efficiency, but thoroughness is paramount in their lending decisions to mitigate risk and ensure responsible credit issuance.

Primary Methods to Check Your Chase Application Status

Chase offers several convenient ways for applicants to check the status of their credit card application, catering to different preferences and situations. Utilizing these methods can provide clarity and help you plan your financial future more effectively.

Online Status Checker

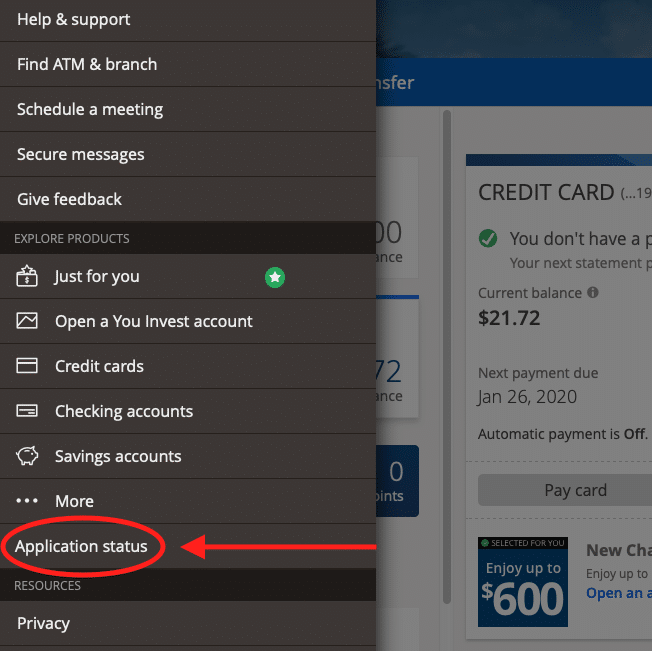

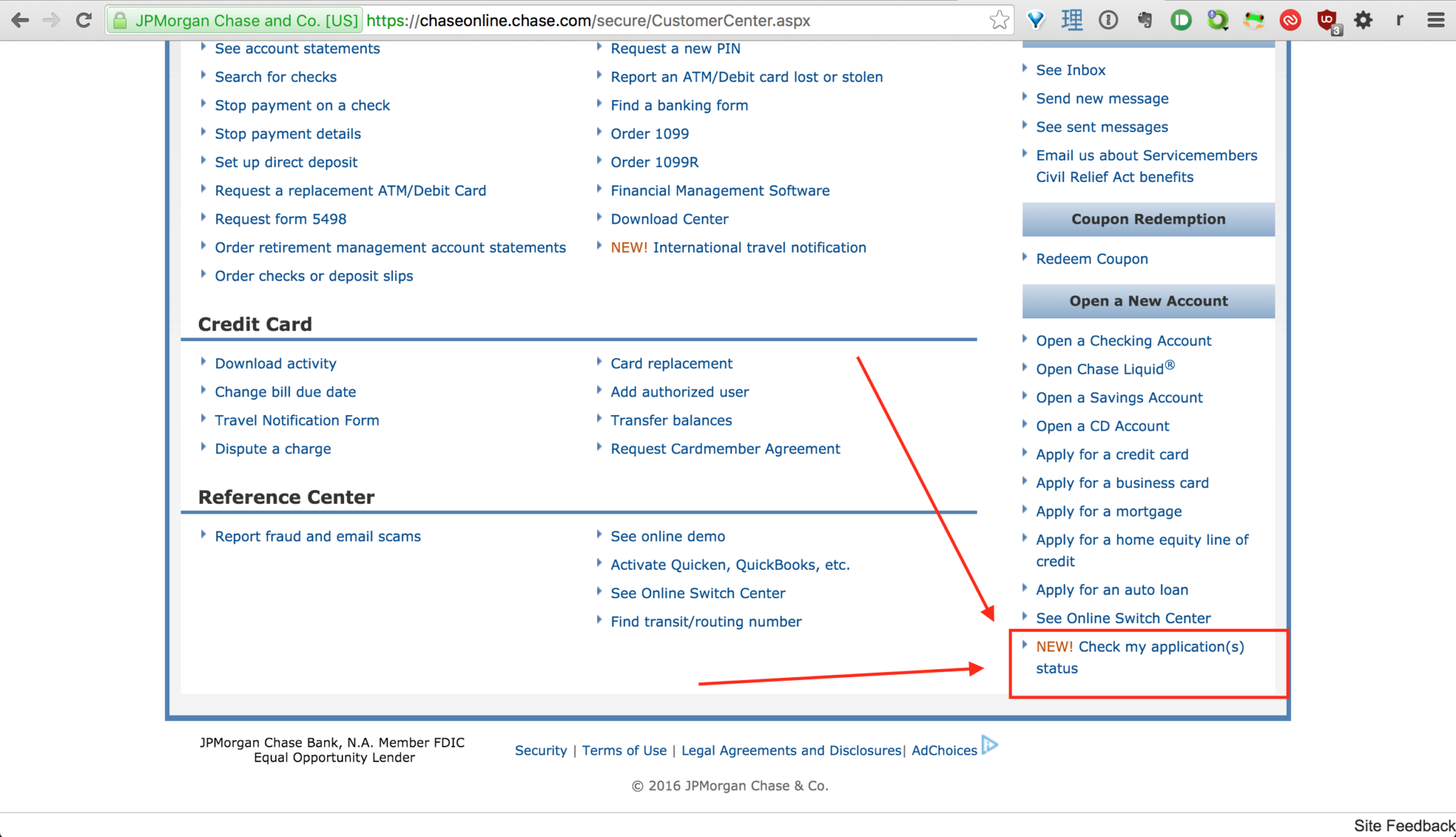

The most common and often quickest method is through Chase’s dedicated online application status tool. This digital portal is designed for ease of use and instant access to your application’s real-time progress. To use it, you’ll typically need to provide your application ID number, which is usually provided upon submission, or other identifying information like your Social Security Number (SSN) and ZIP code.

- How to Access: Navigate to the Chase website and search for “Check Application Status” or look for a direct link within the credit card section.

- Information Required: Be prepared to enter your SSN and the ZIP code you provided on your application. Sometimes an application ID might also be requested.

- Benefits: Available 24/7, provides immediate updates, and eliminates the need for phone calls. It’s an efficient way to monitor progress without delay.

Calling the Chase Application Status Phone Line

For those who prefer direct human interaction or cannot find their application status online, Chase provides a dedicated phone line. This method can be particularly useful if your application requires additional information or if you wish to discuss your application in more detail.

- Dedicated Number: The direct number for checking Chase credit card application status is typically 1-800-432-3117.

- Operating Hours: While the online tool is always available, the phone line operates during specific business hours. It’s advisable to check Chase’s customer service hours before calling.

- What to Expect: When you call, you’ll likely need to verify your identity using personal information such as your SSN, date of birth, and possibly the application ID. A representative can then provide your status and, in some cases, offer more context or even process additional information that might be needed to finalize your application. This can be an opportune moment to address any ambiguities or provide clarifying details that could sway a pending decision.

Checking Your Mail or Email

While less immediate, Chase will also communicate decisions and requests for additional information through traditional mail or email.

- Mail: For approvals, denials, or requests for further documentation, Chase often sends official letters. These letters can take several business days to arrive after a decision has been made.

- Email: If you provided an email address during the application, Chase might send email notifications regarding your application status or to confirm receipt of your application. Always verify the sender to guard against phishing scams.

- Importance: These official communications are vital, especially for denials, as they will contain information regarding the reasons for the denial and your rights under the Equal Credit Opportunity Act, including how to request a free copy of your credit report if the decision was based on information from a credit bureau.

Deciphering Your Application Status

Once you’ve successfully checked your application status, you’ll typically encounter one of a few common outcomes. Each status carries specific implications for your financial planning and potential next steps.

Approved

Congratulations! An “approved” status means Chase has decided to extend you a line of credit. The notification will often include your initial credit limit and information about when you can expect your physical card to arrive.

- Next Steps: Upon receiving your card, activate it according to the instructions provided. Review your cardholder agreement for details on interest rates, fees, and rewards programs. Start using your card responsibly to build a positive credit history.

Denied

A “denied” status indicates that Chase has declined your application. While disappointing, this is not the end of your credit journey. Federal law requires creditors to provide a specific reason or reasons for denying credit.

- Reasons for Denial: Common reasons include a low credit score, high credit utilization on existing accounts, too many recent credit inquiries, insufficient income, or a short credit history.

- Next Steps:

- Review the Denial Letter: Chase will send an adverse action notice detailing the reasons for denial. This letter is crucial for understanding specific areas for improvement.

- Check Your Credit Report: Obtain a free copy of your credit report from AnnualCreditReport.com for each of the three major bureaus. Look for inaccuracies or outdated information that might have negatively impacted your application.

- Consider Reconsideration: If you believe there was a misunderstanding or you have new information (e.g., a recent pay raise not reflected on your application), you can call the Chase reconsideration line (often 1-888-270-2127). Be prepared to articulate why you believe you are a good candidate for the card, emphasizing any positive financial changes or a long-standing relationship with Chase.

Pending/In Review

This is the most common status after submission, indicating that your application requires further scrutiny beyond the initial automated review.

- Why It’s Pending: This could be due to a need for more verification of your identity, income, or employment. Sometimes, it means an underwriter needs to manually review your credit file because it falls into a gray area—neither an immediate approval nor an outright denial.

- Next Steps:

- Be Patient: Wait a few business days. Often, Chase will reach a decision without any action on your part.

- Check Online/Call: Use the online status checker or the phone line periodically. If the status remains pending for an extended period (more than 7-10 business days), a call to the reconsideration line might be warranted to inquire about the delay or offer additional information.

- Respond to Requests: If Chase reaches out for additional documents (e.g., pay stubs, bank statements), respond promptly to avoid further delays or a potential denial due to lack of information.

Factors Influencing Your Chase Credit Card Application Outcome

Understanding the key metrics Chase considers can provide valuable insights into your own financial standing and help you improve your chances for future applications. These factors are central to the credit card issuer’s risk assessment.

Credit Score and History

Your credit score is arguably the most critical factor. Chase, like other major lenders, uses FICO scores (or similar proprietary models) to gauge your creditworthiness. A higher score typically indicates a lower risk.

- Excellent Credit (750+): Generally, the best chance for premium cards with high limits and favorable terms.

- Good Credit (700-749): Still very strong, likely to qualify for most cards.

- Fair Credit (650-699): May qualify for some entry-level cards, but premium cards might be out of reach.

- Credit History: Lenders look at the length of your credit history, payment history (any late payments?), and types of credit accounts (revolving, installment). A long history of responsible credit use is highly favorable.

Income and Employment Stability

Chase wants to ensure you have the financial capacity to repay any debt incurred. Your stated income on the application is a significant data point.

- Debt-to-Income Ratio: Lenders assess your gross monthly income against your monthly debt payments. A lower ratio suggests you have more disposable income to manage new credit.

- Employment: Stable employment history demonstrates consistent income. Self-employed individuals may need to provide additional documentation to verify income.

Existing Relationship with Chase

If you already bank with Chase (e.g., checking, savings, mortgage), this existing relationship can sometimes be a positive factor. Chase has a clearer picture of your financial habits and may be more inclined to approve your application.

Recent Credit Inquiries and New Accounts

Applying for multiple credit cards or loans within a short period can raise red flags. Each “hard inquiry” on your credit report can temporarily lower your score and signal to lenders that you might be taking on too much debt too quickly.

- Chase 5/24 Rule: A well-known internal Chase rule often limits approvals for applicants who have opened 5 or more personal credit cards from any issuer within the last 24 months. While not always strictly applied, it’s a significant consideration for many Chase card applications.

Credit Utilization Ratio

This refers to the amount of credit you’re using compared to your total available credit. A high utilization ratio (e.g., using 50% or more of your available credit) suggests you might be over-reliant on credit, which can negatively impact your score and application chances. Keeping this ratio low (ideally below 30%) is beneficial.

What to Do After Receiving a Decision

Regardless of the outcome, understanding the next steps is crucial for sound financial management.

If Approved: Maximizing Your New Credit Card

Upon approval, you’re not just getting a new piece of plastic; you’re gaining a financial tool that, if managed wisely, can be incredibly beneficial.

- Activate and Understand: Activate your card immediately upon receipt. Carefully read the cardholder agreement, paying close attention to the annual percentage rate (APR), fees (annual, late payment, foreign transaction), and the details of any rewards program or sign-up bonus.

- Set Up Payments: Consider setting up automatic payments for at least the minimum due to avoid late fees and protect your credit score. Ideally, aim to pay your statement balance in full each month to avoid interest charges.

- Monitor Spending: Keep track of your spending to stay within your budget and avoid over-utilizing your credit limit. Tools like the Chase Mobile app offer excellent ways to monitor transactions and manage your account.

- Utilize Benefits: Familiarize yourself with all the perks and benefits of your card, such as travel insurance, purchase protection, extended warranty, or access to exclusive events. Make sure you understand how to earn and redeem any rewards points efficiently.

If Denied: Strategizing for Future Success

A denial is an opportunity to improve your financial profile. It’s a signal to review and adjust your credit strategy.

- Understand the Reasons (Revisit Denial Letter): The adverse action notice is your roadmap. It highlights specific areas that need attention.

- Improve Your Credit Score:

- Pay Bills on Time: Payment history is the most significant factor in your credit score. Ensure all bills are paid punctually.

- Reduce Credit Utilization: Pay down existing credit card balances to lower your utilization ratio.

- Avoid New Credit Applications: Give your credit report a break from new inquiries, especially after a denial.

- Address Errors on Credit Report: Dispute any inaccuracies found on your credit reports with the respective credit bureaus.

- Consider a Secured Card: If your credit score is the primary barrier, a secured credit card (which requires a cash deposit as collateral) can be an excellent stepping stone to rebuilding credit.

- Reapply Strategically: After several months of demonstrating improved credit habits, and once the reasons for your initial denial have been addressed, you can consider reapplying for the same or a different Chase card. Ensure you meet the minimum recommended credit score for the desired card and that your financial situation has genuinely improved.

Checking your Chase credit card application status is more than just a quick lookup; it’s an integral part of responsible personal finance management. It provides immediate feedback on your financial health as seen by a major lender and empowers you to make informed decisions moving forward, whether that means celebrating a new approval or strategically working to strengthen your credit profile for future success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.