The prime rate stands as a critical benchmark in the financial world, influencing everything from the cost of a business loan to the interest charged on a personal credit card. Understanding what the prime rate is, how it’s determined, and its far-reaching implications is essential for informed financial decision-making, whether you’re managing household budgets, investing, or running a business. This article delves into the mechanics of the prime rate, its impact on various financial products, and strategies for navigating its fluctuations.

Deciphering the Prime Rate: Definition and Mechanics

At its core, the prime rate is the interest rate that commercial banks charge their most creditworthy corporate customers. While it’s theoretically an internal bank decision, in practice, the U.S. prime rate is remarkably consistent across major banks and is directly tied to the Federal Reserve’s monetary policy.

The Federal Funds Rate’s Dominance

The primary driver of the prime rate is the federal funds rate, a target rate set by the Federal Open Market Committee (FOMC) of the Federal Reserve. The federal funds rate is the rate at which banks lend their excess reserves to other banks overnight. When the Fed raises or lowers this target rate, commercial banks typically adjust their prime rate in lockstep. Historically, the prime rate has been approximately 3 percentage points higher than the upper limit of the federal funds rate target range. For instance, if the federal funds rate target is between 5.25% and 5.50%, the prime rate would generally be 8.50%. This relationship ensures that the cost of borrowing for banks (through the federal funds market) translates directly into the cost of borrowing for their customers.

How Banks Determine Their Prime Rate

Although influenced heavily by the Federal Reserve, each bank ultimately sets its own prime rate. However, to remain competitive and aligned with market expectations, major financial institutions rarely deviate significantly from the rate published by the Wall Street Journal, which surveys the 10 largest U.S. banks. This collective adherence creates a standardized benchmark, making it easier for consumers and businesses to compare loan products across different lenders. Factors such as the bank’s cost of funds, credit risk assessments, and competitive landscape also play a subtle role, though the Fed’s influence remains paramount.

The Broad Impact of the Prime Rate on Your Finances

Changes in the prime rate ripple throughout the economy, directly affecting the cost of borrowing and, indirectly, savings and investment opportunities for both individuals and businesses. Understanding these connections is key to effective financial planning.

Consumer Loans and Credit Products

Many consumer lending products are directly indexed to the prime rate, meaning their interest rates fluctuate as the prime rate changes.

Credit Cards

The vast majority of credit cards carry variable annual percentage rates (APRs) that are tied to the prime rate. If the prime rate increases, the interest rate on your outstanding credit card balances will likely increase within one or two billing cycles, leading to higher minimum payments and a greater overall cost of debt. Conversely, a decrease in the prime rate can make carrying a balance less expensive.

Home Equity Lines of Credit (HELOCs)

HELOCs are a popular way for homeowners to tap into their home equity. Almost all HELOCs feature variable interest rates that are directly linked to the prime rate. A rising prime rate means higher monthly payments on your HELOC, which can significantly impact household budgets. It’s crucial for HELOC borrowers to monitor prime rate movements and budget accordingly.

Adjustable-Rate Mortgages (ARMs)

While many mortgages are fixed-rate, ARMs have interest rates that adjust periodically after an initial fixed period (e.g., 5/1 ARM, 7/1 ARM). The adjustment mechanism for ARMs is typically tied to a specific index, and while some use LIBOR (or SOFR, its replacement), others use the prime rate. When an ARM’s rate resets, changes in the prime rate can lead to significant shifts in monthly mortgage payments.

Personal Loans and Small Business Loans

Many variable-rate personal loans and lines of credit, particularly those offered by banks, are priced as a margin above the prime rate (e.g., Prime + 2%). Small business loans and lines of credit are also frequently tied to the prime rate, making it a critical factor in a business’s operational costs and expansion plans. As the prime rate shifts, so does the cost of funding for small enterprises, impacting profitability and investment decisions.

Savings and Investment Implications

While the direct impact on savings accounts is less pronounced—as most savings accounts offer very low, relatively stable interest rates—the overall interest rate environment shaped by the prime rate does affect deposit products and investment strategies.

Certificates of Deposit (CDs) and High-Yield Savings Accounts

When the prime rate rises, banks tend to increase the rates offered on Certificates of Deposit (CDs) and high-yield savings accounts, as their cost of funds (and thus their ability to earn more on lending) has increased. This can be beneficial for savers looking for better returns on their liquid assets.

Bond Markets

The prime rate, being a reflection of the broader interest rate environment, also influences bond yields. When interest rates rise, newly issued bonds offer higher yields, making existing lower-yield bonds less attractive and typically causing their market value to fall. Investors must weigh the impact of rising rates on their fixed-income portfolios.

Tracking and Interpreting Prime Rate Changes

Staying informed about the prime rate is a proactive step in managing your financial health. Understanding where to find current information and how to interpret changes is key.

Reliable Sources for Prime Rate Information

The most widely referenced source for the U.S. prime rate is the Wall Street Journal, which publishes the rate daily based on a survey of the nation’s largest banks. The Federal Reserve also provides comprehensive data and announcements regarding the federal funds rate target, which directly informs the prime rate. Additionally, many financial news outlets, bank websites, and financial data services report the current prime rate.

Decoding Rate Hikes and Cuts

Rate Hikes

When the Federal Reserve raises the federal funds rate, it’s typically in response to concerns about inflation or an overheating economy. A rising prime rate makes borrowing more expensive, which can cool down economic activity by discouraging new loans and encouraging saving. For borrowers, this means higher payments on variable-rate debts. For savers, it can offer opportunities for better returns on deposits.

Rate Cuts

Conversely, the Fed lowers the federal funds rate to stimulate economic growth, often during periods of economic slowdown or recession. A declining prime rate makes borrowing cheaper, encouraging consumer spending and business investment. For borrowers, this can lead to lower payments on variable-rate loans. For savers, it may result in lower returns on interest-bearing accounts.

Strategies for Navigating a Changing Rate Environment

Proactive financial planning can mitigate the negative effects of rising rates and capitalize on favorable conditions.

For Borrowers: Managing Debt Effectively

Prioritize Variable-Rate Debt

If the prime rate is on an upward trajectory, focus on aggressively paying down high-interest, variable-rate debts like credit card balances and HELOCs. Reducing the principal balance will lessen the impact of future rate increases.

Consider Refinancing

For those with variable-rate personal loans, ARMs nearing their reset period, or variable-rate business loans, consider refinancing into a fixed-rate product if current rates are still favorable. This can provide payment stability and predictability, protecting you from future rate hikes. Evaluate the costs of refinancing against the potential savings.

Lock in Rates Where Possible

When applying for new loans, especially during periods of rising rates, opt for fixed-rate options if they align with your financial goals. This could include fixed-rate personal loans, business loans, or traditional fixed-rate mortgages.

Budget for Higher Payments

If you have significant variable-rate debt, create a budget that can absorb potential payment increases. Set aside extra funds or reduce discretionary spending to prepare for higher monthly obligations.

For Savers and Investors: Optimizing Returns

Seek Higher-Yield Accounts

In a rising rate environment, shop around for high-yield savings accounts, money market accounts, and Certificates of Deposit (CDs). Banks become more competitive for deposits as their ability to lend at higher rates increases. Look for online banks, which often offer better rates than traditional brick-and-mortar institutions due to lower overheads.

Re-evaluate Investment Portfolios

For investors, rising interest rates can impact various asset classes. Fixed-income investors might consider shorter-duration bonds or bond funds to reduce interest rate risk, or explore Treasury Inflation-Protected Securities (TIPS) if inflation is also a concern. Equity investors should assess how rate changes might affect company earnings, particularly for highly leveraged companies or those sensitive to consumer spending.

Review Business Cash Management

Businesses should review their cash management strategies, ensuring that excess funds are earning competitive interest. Additionally, analyze existing lines of credit and consider locking in rates on new loans if long-term financial stability is prioritized over potential short-term rate dips.

Historical Context and Future Outlook

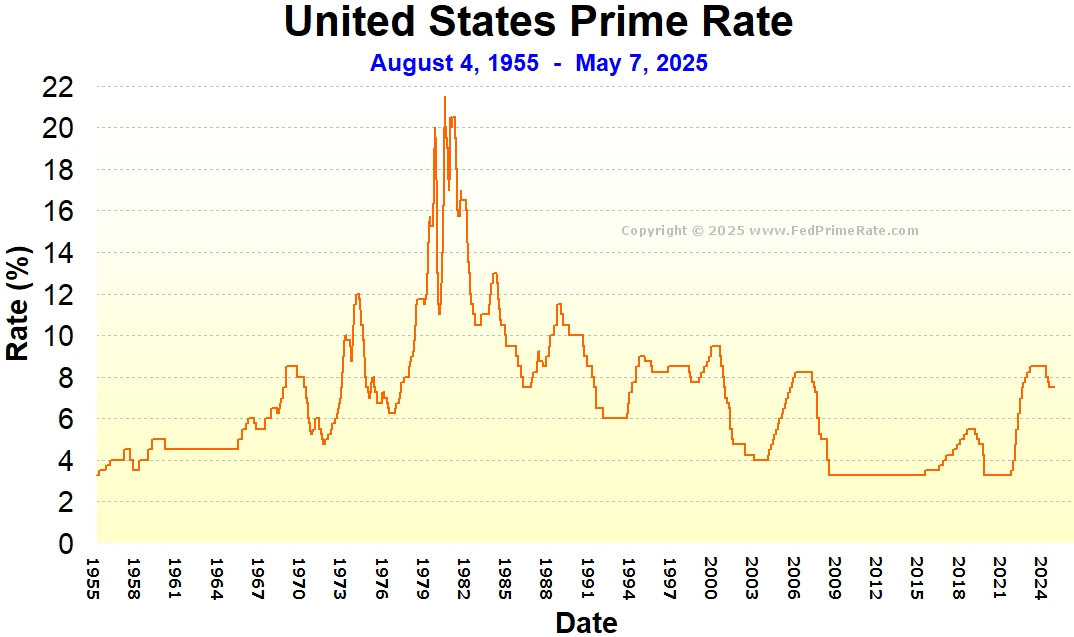

The prime rate has fluctuated significantly throughout history, reflecting periods of economic expansion, contraction, and shifts in monetary policy. For instance, the early 1980s saw the prime rate soar to unprecedented highs (above 20%) as the Federal Reserve battled rampant inflation. Conversely, the aftermath of the 2008 financial crisis and the COVID-19 pandemic saw the prime rate drop to historical lows, reflecting efforts to stimulate economic activity.

Looking ahead, the prime rate’s trajectory will continue to be dictated by the Federal Reserve’s response to economic indicators such as inflation, employment rates, and overall economic growth. Financial analysts and economists constantly monitor these metrics to predict the Fed’s next moves. Understanding these signals—and remembering that forecasting is not an exact science—can help individuals and businesses anticipate potential shifts and adjust their financial strategies accordingly.

In conclusion, the prime rate is more than just a number; it’s a dynamic indicator of economic health and a direct determinant of the cost of money for millions. By staying informed and proactive, you can effectively navigate its changes and optimize your financial outcomes.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.