For many aspiring homeowners, the thought of purchasing a house can feel daunting, often characterized by a maze of financial terms and complex loan products. Among the most popular options designed to make homeownership more accessible are FHA loans, backed by the Federal Housing Administration. When considering an FHA loan, one of the first and most critical questions that arises is, “What FHA interest rate can I expect?” This isn’t just a simple number; it’s a pivotal factor that will determine your monthly mortgage payments, the total cost of your home over its lifetime, and ultimately, the feasibility of your homeownership dream.

Understanding FHA interest rates requires looking beyond the surface. It involves grasping the unique characteristics of FHA loans, the myriad factors that influence these rates, and how they compare to other financing options. This comprehensive guide will demystify FHA interest rates, offering insightful perspectives to help you navigate the mortgage landscape with confidence and make informed financial decisions on your path to homeownership.

The Fundamentals of FHA Loans and Their Broad Appeal

Before delving into the intricacies of interest rates, it’s crucial to establish a foundational understanding of what FHA loans are and why they have become such a cornerstone of the housing market, particularly for first-time homebuyers or those with less-than-perfect credit.

What Exactly is an FHA Loan?

An FHA loan is a government-insured mortgage provided by FHA-approved lenders. Unlike conventional loans, which are directly underwritten by private lenders, the FHA guarantees a portion of the loan for the lender. This government backing significantly reduces the risk for lenders, making them more willing to offer loans to borrowers who might not meet the stricter criteria of conventional mortgages. This insurance is not free, however, and comes in the form of mortgage insurance premiums (MIP), which we will discuss later. The primary objective of FHA loans is to expand homeownership opportunities, especially for individuals and families who face barriers to traditional financing.

Key Benefits Beyond the Interest Rate

While interest rates are a primary concern, FHA loans offer several other compelling benefits that contribute to their popularity:

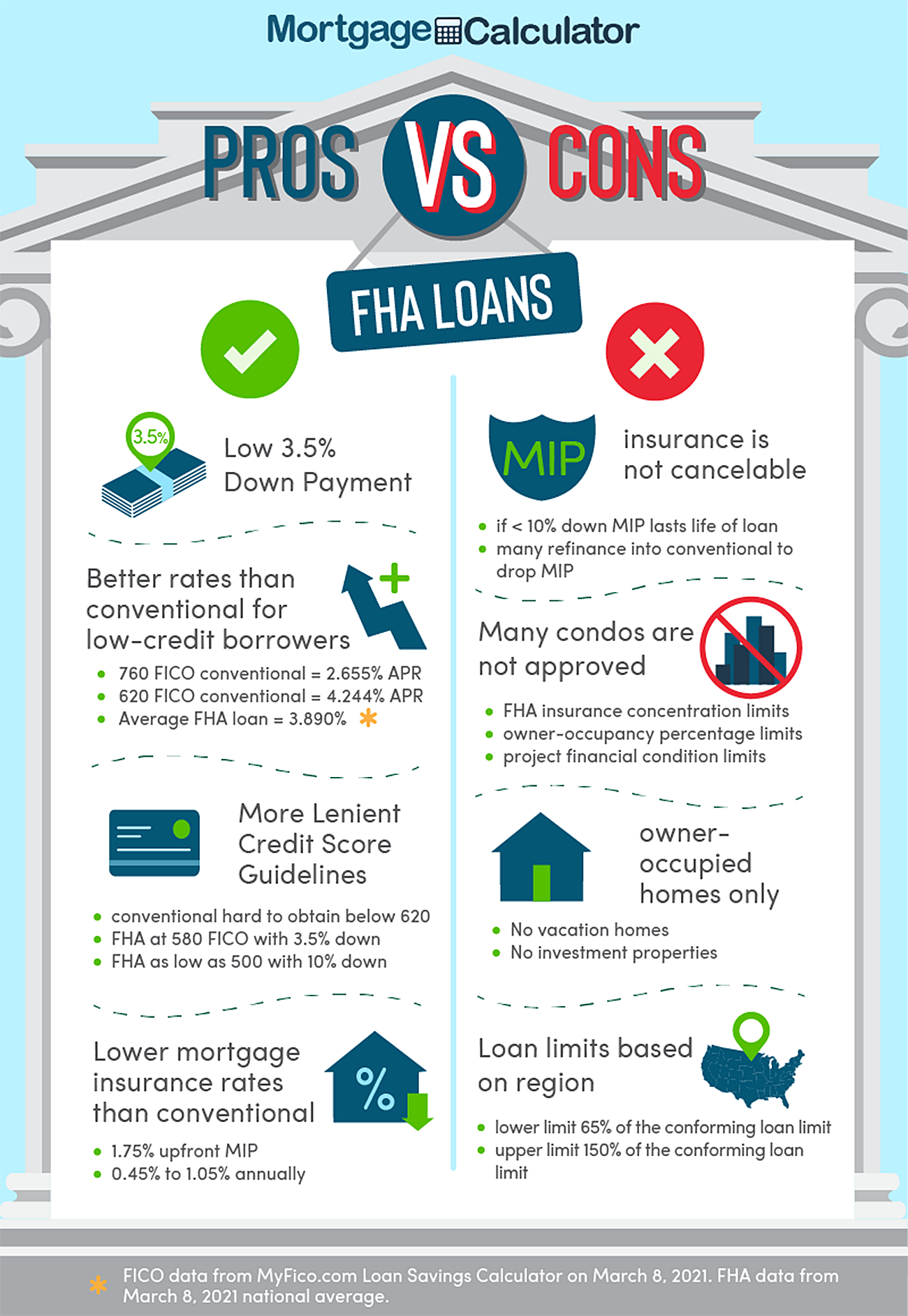

- Lower Down Payment Requirements: One of the most attractive features is the ability to purchase a home with a minimum down payment as low as 3.5% of the purchase price, provided the borrower has a credit score of 580 or higher. For conventional loans, a 20% down payment is often required to avoid private mortgage insurance (PMI).

- More Lenient Credit Score Requirements: FHA loans are more forgiving regarding credit scores. While a 580 FICO score is generally required for the 3.5% down payment, scores as low as 500 might still qualify with a 10% down payment. This flexibility opens doors for many who might otherwise be shut out of the housing market.

- Acceptance of Non-Traditional Credit History: The FHA is often more flexible in considering alternative credit data, such as utility payments or rent history, for borrowers with limited traditional credit files.

- Assumable Mortgages: An often-overlooked benefit is that FHA loans are assumable, meaning a buyer can take over the seller’s mortgage, along with its existing interest rate, which can be advantageous in certain market conditions.

Eligibility Requirements: Who Qualifies?

While FHA loans are more accessible, they do have specific requirements. Beyond credit score and down payment, borrowers must meet income and debt-to-income (DTI) ratio guidelines, though these are typically more flexible than conventional loan standards. The property itself must also meet FHA appraisal standards, which focus on safety, soundness, and security, ensuring the home is habitable and presents a reasonable value. Additionally, the loan must be used for a primary residence, and there are FHA loan limits that vary by county.

Deciphering FHA Interest Rates: What Influences Them?

Understanding the benefits is only half the battle; the other half is comprehending what drives the actual interest rate you’ll be offered on an FHA loan. FHA rates are not universally fixed; they fluctuate based on a complex interplay of market dynamics, lender policies, and your individual financial profile.

Market Forces: The Economy’s Role

The broader economic environment plays a significant role in determining interest rates across the board, including FHA loans. Key economic indicators and policies that influence rates include:

- Federal Reserve Policy: Actions by the Federal Reserve, particularly changes to the federal funds rate, indirectly impact mortgage rates. When the Fed raises rates to combat inflation, mortgage rates tend to follow suit.

- Inflation: Higher inflation erodes the purchasing power of money, leading lenders to demand higher interest rates to compensate for the decreased value of future repayments.

- Economic Growth: A strong economy can lead to higher interest rates as demand for money increases, while a weaker economy might see rates fall as central banks try to stimulate activity.

- Bond Market Performance: Mortgage rates are closely tied to the yield on U.S. Treasury bonds. As bond yields rise, so do mortgage rates, and vice versa.

Lender-Specific Factors and How They Vary

While the FHA insures the loan, individual lenders (banks, credit unions, mortgage brokers) are the ones who set the specific interest rates they offer. Each lender has its own operational costs, risk assessments, and profit margins, leading to variations in rates.

- Lender Overhead and Business Model: Larger institutions might have different cost structures than smaller brokers, impacting the rates they can offer.

- Pricing Strategies: Lenders adjust their rates based on market competition, their current loan volume, and their desire to attract certain types of borrowers.

- Relationship with Lender: Sometimes, existing customers of a bank might receive slightly more favorable terms, though this isn’t always the case.

Your Financial Profile: Credit Score and Down Payment

Your personal financial health is a critical determinant of the FHA interest rate you’ll be offered. Lenders use your profile to assess the risk of lending to you.

- Credit Score: A higher FICO score signals greater financial responsibility and a lower risk of default to lenders. Consequently, borrowers with excellent credit scores (e.g., 700+) will typically qualify for lower FHA interest rates compared to those with minimum qualifying scores (e.g., 580-620).

- Down Payment Amount: While FHA loans are known for low down payments, making a larger down payment can sometimes result in a slightly better interest rate. A larger equity stake reduces the lender’s risk.

- Debt-to-Income (DTI) Ratio: Your DTI ratio, which compares your monthly debt payments to your gross monthly income, is another key factor. A lower DTI indicates that you can more comfortably manage your mortgage payments, potentially leading to a better rate.

Loan Term and Type: Fixed vs. Adjustable Rates

The structure of your FHA loan also influences the interest rate.

- Fixed-Rate Mortgages (FRM): The most common choice for FHA loans are 15-year or 30-year fixed-rate mortgages, where the interest rate remains constant for the life of the loan. This provides predictability in monthly payments. Generally, 15-year fixed rates are lower than 30-year rates because the lender’s money is tied up for a shorter period.

- Adjustable-Rate Mortgages (ARM): FHA also offers ARMs (e.g., 5/1 ARM), where the interest rate is fixed for an initial period (e.g., 5 years) and then adjusts periodically based on a market index. While the initial rate on an ARM can be lower than a fixed rate, the risk of future payment increases makes them less popular for those seeking long-term stability.

Comparing FHA vs. Conventional Loan Interest Rates

A common misconception is that FHA loan interest rates are always significantly lower than conventional loan rates. While FHA loans often appear to have competitive or even slightly lower advertised rates, it’s crucial to look at the full cost picture, particularly concerning mortgage insurance.

The “Lower Rate” Misconception and the Full Cost Picture

When comparing loan estimates, you might indeed see a slightly lower interest rate for an FHA loan compared to a conventional loan for a borrower with similar credit. However, this seemingly lower rate often comes with the mandatory FHA Mortgage Insurance Premiums (MIP), which can significantly impact the overall monthly payment and the total cost over the life of the loan.

Understanding Mortgage Insurance Premiums (MIP)

FHA loans require two types of MIP:

- Upfront Mortgage Insurance Premium (UFMIP): This is a one-time fee, currently 1.75% of the base loan amount, which can be financed into the loan.

- Annual Mortgage Insurance Premium (Annual MIP): This premium is paid monthly and varies based on the loan term, loan amount, and loan-to-value (LTV) ratio. For most FHA loans with a 3.5% down payment and a 30-year term, the annual MIP is 0.55% of the loan amount. Unlike conventional PMI, which can often be canceled once you reach 20% equity, FHA annual MIP is typically paid for the entire life of the loan if your down payment was less than 10%. If your down payment was 10% or more, MIP can be canceled after 11 years. This long-term cost can make an FHA loan more expensive over time than a conventional loan, even with a slightly lower interest rate.

When an FHA Loan Might Still Be Your Best Bet

Despite the MIP, FHA loans remain an excellent option for many borrowers. They are particularly advantageous for:

- Borrowers with Lower Credit Scores: If your credit score prevents you from qualifying for a conventional loan or leads to a significantly higher conventional interest rate, an FHA loan offers a viable path to homeownership.

- Borrowers with Limited Down Payment Funds: The low 3.5% down payment requirement makes FHA loans highly attractive if saving a 20% down payment is challenging.

- High Debt-to-Income Ratios: FHA’s more flexible DTI requirements can be a lifesaver for those with existing debts but stable income.

When comparing, it’s essential to calculate the total monthly payment, including principal, interest, taxes, insurance (PITI), and any mortgage insurance (MIP or PMI), to get an accurate comparison of an FHA loan versus a conventional loan.

Strategies for Securing the Best FHA Interest Rate

While external market forces are beyond your control, there are proactive steps you can take to position yourself for the most favorable FHA interest rate possible. Strategic financial planning can make a tangible difference in your mortgage costs.

Improving Your Credit Score

Your credit score is arguably the most impactful personal factor influencing your interest rate. Prioritizing its improvement before applying for a loan can yield significant savings.

- Pay Bills on Time: Payment history is the largest factor in credit scoring.

- Reduce Existing Debt: Lowering your credit utilization ratio (amount of credit used vs. available) can boost your score.

- Avoid New Credit: Don’t open new credit accounts or take on additional debt immediately before applying for a mortgage.

- Check Your Credit Report: Dispute any errors that could be negatively affecting your score.

Shopping Around for Lenders

Interest rates for FHA loans are not standardized across all lenders. Each institution sets its own rates, fees, and closing costs.

- Compare Multiple Offers: Obtain loan estimates from at least three to five different lenders (banks, credit unions, mortgage brokers). This allows you to compare not only interest rates but also origination fees, discount points, and other closing costs.

- Utilize Mortgage Brokers: A mortgage broker works with multiple lenders and can often find competitive rates that you might not uncover on your own.

- Look Beyond the Rate: While the interest rate is crucial, also consider the lender’s reputation, customer service, and the efficiency of their loan process.

Optimizing Your Down Payment

While FHA loans are known for low down payments, contributing more than the minimum 3.5% can have benefits.

- Reduced Loan Amount: A larger down payment means you’re borrowing less, which reduces your total interest paid over the life of the loan.

- Potentially Lower MIP: In some cases, a larger down payment (e.g., 10% or more) can lead to a shorter duration for your annual MIP payments (11 years instead of the life of the loan).

- Increased Equity: Starting with more equity in your home provides a stronger financial position from day one.

Considering Discount Points

Discount points are optional upfront fees paid to the lender in exchange for a lower interest rate over the life of the loan. One discount point typically costs 1% of the loan amount.

- Cost-Benefit Analysis: Paying points can save you a substantial amount in interest over the long term, but it increases your upfront closing costs. You need to calculate the “break-even point” – how long it takes for the monthly savings to offset the cost of the points. This strategy is usually more beneficial if you plan to stay in the home for many years.

- Negotiation: Discuss the option of paying points with your lender to see if it aligns with your financial goals and projected tenure in the home.

The Application Process: From Inquiry to Closing

Navigating the FHA loan application process efficiently is key to securing your desired interest rate and making your homeownership dream a reality. While the specifics can vary slightly by lender, there’s a general roadmap to follow.

Pre-Approval: Your First Critical Step

Before you even start house hunting, getting pre-approved for an FHA loan is essential.

- Determines Affordability: Pre-approval gives you a clear understanding of how much you can realistically afford, setting a realistic budget for your home search.

- Strengthens Offers: A pre-approval letter demonstrates to sellers that you are a serious and qualified buyer, giving your offer more weight in a competitive market.

- Identifies Potential Issues: The pre-approval process involves a preliminary review of your finances, allowing you to identify and address any credit or documentation issues early on.

Documentation Needed for an FHA Loan

Be prepared to provide a comprehensive set of documents to your lender. This typically includes:

- Proof of Income: Pay stubs, W-2 forms, tax returns for the past two years.

- Asset Verification: Bank statements, investment account statements to show down payment funds and reserves.

- Credit History: Lenders will pull your credit report, but you may need to explain any derogatory marks.

- Employment Verification: Contact information for your employer(s).

- Identification: Government-issued ID.

Having these documents organized and readily available will streamline the application process.

What to Expect During Underwriting

After you find a home and your offer is accepted, your loan application moves into the underwriting phase. This is where the lender thoroughly verifies all the information you’ve provided.

- Detailed Review: Underwriters meticulously examine your financial stability, creditworthiness, and the property’s appraisal. They ensure the loan meets both the lender’s guidelines and FHA requirements.

- Conditional Approval: It’s common to receive a conditional approval, meaning the underwriter needs additional documentation or clarification on specific items before granting final approval. Respond to these requests promptly.

- FHA Appraisal: An FHA-approved appraiser will assess the home’s value and ensure it meets FHA minimum property standards, which focus on safety, soundness, and security.

Finally, upon successful underwriting and appraisal, your loan will be cleared to close, bringing you one step closer to receiving the keys to your new home.

In conclusion, understanding “what FHA interest rate” truly means involves a multifaceted approach. It’s not just about the number itself, but about comprehending the loan’s unique structure, the economic and personal factors that shape the rate, and the comparison with other financing options. By being informed, strategic, and proactive, aspiring homeowners can navigate the complexities of FHA loans and secure a financial arrangement that truly supports their long-term homeownership aspirations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.