Understanding how to calculate loan payments is a fundamental skill for anyone managing personal or business finances. Whether you’re considering a mortgage, a car loan, student loans, or personal financing, knowing the mechanics behind your monthly obligation empowers you to make informed decisions, budget effectively, and potentially save thousands over the life of the loan. This guide will demystify the process, breaking down the essential components and providing practical methods to calculate your loan payments with confidence.

At its core, a loan payment calculation determines the fixed amount you’ll pay periodically (usually monthly) to gradually repay the principal amount borrowed, plus the accumulated interest, over a specified loan term. It’s a critical piece of financial literacy that transforms complex financial products into manageable, predictable commitments.

The Foundational Elements of Loan Payments

Before diving into formulas and calculations, it’s crucial to grasp the key variables that influence every loan payment. These elements are the building blocks, and a clear understanding of each will set the stage for accurate computation.

Principal Amount (P)

The principal is the initial sum of money you borrow from a lender. If you take out a $20,000 car loan, $20,000 is your principal. It’s the base figure upon which interest is calculated and which you are ultimately obligated to repay. The higher the principal, all else being equal, the higher your loan payment will be.

Annual Interest Rate (r)

The interest rate is the cost of borrowing money, expressed as a percentage of the principal per year. It’s the fee lenders charge for the use of their capital. While often quoted as an annual percentage rate (APR), for calculation purposes, it needs to be converted into a periodic (e.g., monthly) rate. A higher interest rate directly translates to a larger portion of your payment going towards interest, thus increasing your total payment and the overall cost of the loan.

Loan Term (n)

The loan term, also known as the amortization period, is the length of time over which you agree to repay the loan. It’s typically expressed in years but must be converted into the total number of payment periods for calculations. For instance, a 5-year loan with monthly payments has a term of 60 periods (5 years * 12 months/year). Longer loan terms generally result in lower monthly payments, but you’ll pay more interest over the life of the loan. Conversely, shorter terms mean higher monthly payments but less total interest paid.

Payment Frequency

While most loans are structured with monthly payments, some might be bi-weekly, weekly, or quarterly. The payment frequency dictates how many times per year you make a payment. For consistency, the annual interest rate and loan term must always align with this frequency when performing calculations. For example, if payments are monthly, the annual interest rate is divided by 12, and the loan term in years is multiplied by 12.

The Amortization Formula: Your Calculation Blueprint

The most common method for calculating loan payments is through the amortization formula, which determines a fixed periodic payment that gradually pays down both principal and interest over the loan’s term. This formula is the engine behind most loan calculators and financial software.

Understanding the Variables in the Formula

Let’s define the variables specifically for the amortization formula:

- M: Your monthly loan payment (the value you want to calculate).

- P: The principal loan amount.

- r: Your monthly interest rate (the annual interest rate divided by 12, expressed as a decimal). For example, if the annual rate is 5%, then r = 0.05 / 12 = 0.00416667.

- n: The total number of payments (the loan term in years multiplied by 12). For example, a 30-year loan has n = 30 * 12 = 360 payments.

The Amortization Payment Formula

The formula for calculating the fixed monthly payment (M) is as follows:

$$ M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1 ] $$

Where:

- M = Monthly payment

- P = Principal loan amount

- i = Monthly interest rate (annual rate / 12)

- n = Total number of payments (loan term in years * 12)

Let’s break down how to apply this formula with an example.

Step-by-Step Calculation Guide with Examples

Applying the formula might seem daunting at first, but by breaking it down into manageable steps, it becomes straightforward.

Example 1: Calculating a Car Loan Payment

Let’s say you want to borrow $25,000 for a new car at an annual interest rate of 6% over 5 years.

Step 1: Identify your variables.

- P (Principal) = $25,000

- Annual Interest Rate = 6%

- Loan Term = 5 years

Step 2: Convert annual rate to monthly rate (i) and loan term to total payments (n).

- Monthly Interest Rate (i) = 6% / 12 = 0.06 / 12 = 0.005

- Total Number of Payments (n) = 5 years * 12 months/year = 60 payments

Step 3: Plug the values into the formula.

$$ M = 25000 [ 0.005(1 + 0.005)^{60} ] / [ (1 + 0.005)^{60} – 1 ] $$

Step 4: Calculate the components.

(1 + 0.005)=1.005(1.005)^{60}≈1.34885015

Now, substitute these back into the formula:

$$ M = 25000 [ 0.005 * 1.34885015 ] / [ 1.34885015 – 1 ] $$

$$ M = 25000 [ 0.00674425 ] / [ 0.34885015 ] $$

$$ M = 168.60625 / 0.34885015 $$

$$ M approx 483.25 $$

So, your estimated monthly car loan payment would be approximately $483.25.

Example 2: Understanding a Mortgage Scenario

Consider a more complex scenario: a $300,000 mortgage at an annual interest rate of 4.5% over 30 years.

Step 1: Identify your variables.

- P = $300,000

- Annual Interest Rate = 4.5%

- Loan Term = 30 years

Step 2: Convert to monthly rate (i) and total payments (n).

- Monthly Interest Rate (i) = 4.5% / 12 = 0.045 / 12 = 0.00375

- Total Number of Payments (n) = 30 years * 12 months/year = 360 payments

Step 3: Plug the values into the formula.

$$ M = 300000 [ 0.00375(1 + 0.00375)^{360} ] / [ (1 + 0.00375)^{360} – 1 ] $$

Step 4: Calculate the components.

(1 + 0.00375)=1.00375(1.00375)^{360}≈3.83405366

Now, substitute these back into the formula:

$$ M = 300000 [ 0.00375 * 3.83405366 ] / [ 3.83405366 – 1 ] $$

$$ M = 300000 [ 0.01437769 ] / [ 2.83405366 ] $$

$$ M = 4313.307 / 2.83405366 $$

$$ M approx 1521.99 $$

Your estimated monthly mortgage payment would be approximately $1,521.99. These examples illustrate the power and necessity of accurate calculations.

Tools and Resources for Effortless Calculation

While understanding the manual calculation is invaluable, practical application often involves leveraging readily available tools that streamline the process and minimize human error.

Online Loan Calculators

The internet is brimming with free online loan calculators provided by financial institutions, independent financial websites, and even search engines. These tools are incredibly user-friendly: you simply input the principal, interest rate, and loan term, and they instantly provide the monthly payment, often accompanied by an amortization schedule.

- Benefits: Speed, ease of use, often include amortization schedules and graphs.

- Considerations: Double-check the source’s credibility; ensure it’s calculating based on your desired payment frequency.

Spreadsheet Software (Excel, Google Sheets)

For those who prefer a more hands-on approach or need to perform multiple calculations and scenarios, spreadsheet software like Microsoft Excel or Google Sheets is indispensable. These programs have built-in financial functions that make loan payment calculations simple.

-

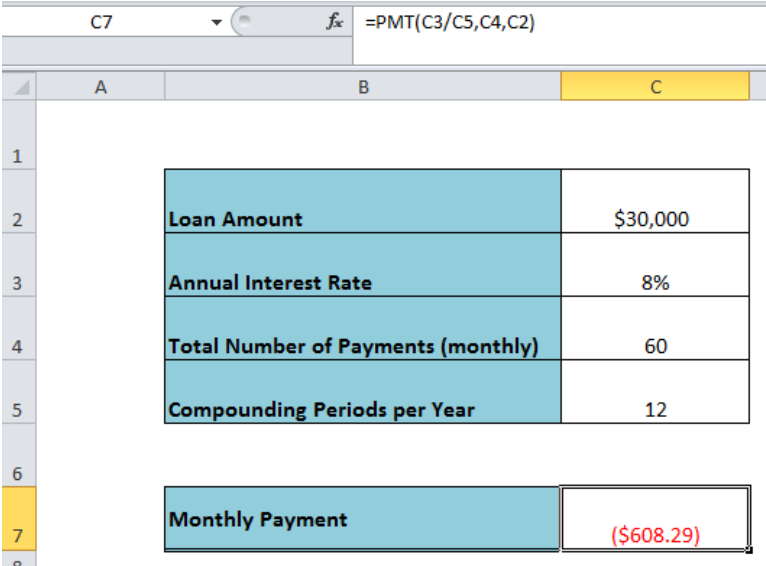

The PMT Function: Excel and Google Sheets feature a

PMTfunction designed specifically for this purpose. The syntax is=PMT(rate, nper, pv, [fv], [type]).rate: The interest rate per period (e.g., annual rate / 12).nper: The total number of payments (loan term in years * 12).pv: The present value or principal loan amount.fv: [Optional] The future value, or a cash balance you want to attain after the last payment. Defaults to 0.type: [Optional] Indicates when payments are due (0 for end of period, 1 for beginning of period). Defaults to 0.

-

Example for Excel: For the $25,000 car loan (6% over 5 years):

=PMT(0.06/12, 5*12, 25000)- The result will be

-483.32. The negative sign indicates an outflow of cash (a payment).

Spreadsheets offer flexibility to change variables and see the immediate impact, making them powerful tools for financial planning and scenario analysis.

Financial Calculators

Dedicated financial calculators (like the HP 12c or Texas Instruments BA II Plus) are portable devices designed for complex financial computations. They are widely used by finance professionals and students. While they have a learning curve, they are powerful for on-the-go calculations without an internet connection.

Beyond the Numbers: Factors Affecting Your Loan Payment

While the formula provides the absolute payment, several other factors influence the actual amount you’ll pay and the overall cost of borrowing. Understanding these can help you optimize your loan terms.

Impact of Interest Rates and APR

The interest rate is arguably the most significant factor. Even a small difference in the annual rate can lead to substantial savings or additional costs over a long loan term. It’s crucial to differentiate between the nominal interest rate and the Annual Percentage Rate (APR). The APR includes the interest rate plus other charges (like origination fees), giving a more accurate total cost of borrowing. Always compare APRs when evaluating loans.

Choosing the Right Loan Term

The loan term is a double-edged sword. A longer term means lower monthly payments, which can make a loan seem more affordable in the short run. However, it also means you pay interest for a longer period, resulting in a significantly higher total interest paid over the life of the loan. Conversely, a shorter term has higher monthly payments but less total interest. Balancing affordability with total cost is key.

The Role of Your Credit Score

Your credit score is a primary determinant of the interest rate you’ll be offered. Borrowers with excellent credit scores are perceived as lower risk, qualifying them for the most favorable (lowest) interest rates. A lower credit score often leads to higher interest rates, increasing your monthly payments and the overall cost of the loan. Improving your credit score before applying for a major loan can translate into substantial savings.

Understanding Amortization Schedules

An amortization schedule is a table detailing each payment made over the life of a loan, showing how much of each payment goes towards interest and how much goes towards the principal balance. In the early stages of a loan, a larger portion of your payment goes towards interest. As the loan matures, more of each payment is applied to the principal. This schedule helps you visualize the repayment process and understand how your principal balance is reduced over time.

Conclusion

Calculating loan payments is a fundamental skill that empowers you to navigate the world of personal and business finance with greater confidence. By understanding the principal, interest rate, and loan term, and by applying the amortization formula, you can accurately project your financial obligations. While manual calculations provide invaluable insight, leveraging online calculators and spreadsheet functions offers efficiency and accuracy for real-world scenarios.

Beyond the raw numbers, remember that your credit score, the chosen loan term, and the overall APR significantly impact the true cost of borrowing. Being diligent in your research, comparing offers, and understanding these underlying factors will not only help you calculate your payments but also enable you to make smarter financial decisions that align with your long-term monetary goals. Equip yourself with this knowledge, and take control of your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.