The journey from education to employment often comes with a significant financial companion: student loans. For many graduates, navigating the complexities of student loan repayment can feel daunting, a labyrinth of terms, plans, and strategies that seem designed to confuse rather than clarify. However, understanding how to effectively manage and repay your student loans is a cornerstone of sound personal finance, impacting everything from your credit score to your ability to achieve future financial goals like homeownership or retirement. This comprehensive guide will demystify the process, offering actionable insights and clear strategies to help you confidently tackle your student loan debt.

The first step in any successful repayment journey is acknowledging that you are not alone in this challenge. Millions of individuals carry student loan debt, and a wealth of resources and options exist to assist you. The key is to be proactive, informed, and strategic in your approach. From understanding the fundamental differences between loan types to exploring various repayment plans and knowing your options in times of financial hardship, every piece of information arms you with greater control over your financial future. Let’s embark on this crucial financial education, transforming uncertainty into a clear, manageable path forward.

Understanding Your Student Loan Landscape

Before you can chart a course for repayment, it’s imperative to thoroughly understand the terrain you’re traversing. This involves knowing precisely what kind of loans you have, their terms, and who services them. Misinformation or a lack of clarity here can lead to costly mistakes and missed opportunities.

Differentiating Federal vs. Private Loans

The most critical distinction to make is between federal student loans and private student loans. Federal loans are issued by the U.S. government and come with a host of borrower protections and flexible repayment options, including income-driven plans, deferment, forbearance, and potential for forgiveness programs. They generally have fixed interest rates and don’t require a credit check for most undergraduate borrowers. Examples include Direct Subsidized, Unsubsidized, PLUS, and Perkins loans.

Private student loans, on the other hand, are offered by banks, credit unions, and other private lenders. They typically have fewer borrower protections and more stringent eligibility requirements, often relying on your credit score and income or requiring a co-signer. Their interest rates can be fixed or variable and are generally higher than federal loan rates, depending on your creditworthiness. Understanding which type of loan you hold is fundamental, as it dictates the available repayment strategies and relief options.

Key Loan Terms to Know

Familiarizing yourself with key terminology will empower you to make informed decisions.

- Principal: The original amount borrowed, plus any capitalized interest.

- Interest Rate: The cost of borrowing money, expressed as a percentage of the principal. This dictates how much extra you pay over time.

- Accrued Interest: The interest that has accumulated on your loan. For some loans, interest accrues even while you’re in school or during grace periods.

- Loan Servicer: The company that manages your loan, handles billing, and processes your payments. They are your primary point of contact for all repayment-related questions.

- Grace Period: A period, typically six months after you graduate or drop below half-time enrollment, during which you are not required to make payments. Interest may still accrue during this time.

- Default: Failing to make your loan payments as scheduled. This can have severe consequences for your credit score and lead to wage garnishment or tax refund offsets.

Accessing Your Loan Information

You can’t manage what you can’t see. For federal loans, your definitive source of truth is the National Student Loan Data System (NSLDS) at nslds.ed.gov. This database provides a comprehensive view of all your federal loans, including loan servicers, outstanding balances, and repayment statuses. For private loans, you’ll need to check your credit report or contact the lenders directly. Regularly reviewing this information ensures accuracy and keeps you abreast of your total debt burden and who you owe.

Exploring Repayment Strategies and Plans

Once you have a clear picture of your loans, the next step is to select a repayment strategy that aligns with your financial situation and goals. Federal student loans offer a variety of plans designed to accommodate different income levels and circumstances, while private loan options are typically more limited.

Standard Repayment Plans

The default plan for most federal student loans is the Standard Repayment Plan. Under this plan, you make fixed monthly payments for up to 10 years (or 10 to 30 years for consolidated loans). While it often results in the lowest total interest paid over the life of the loan and gets you out of debt the fastest, the monthly payments can be substantial. This plan is ideal if you have a stable income that can comfortably cover the payments and want to minimize the overall cost of your loan.

Income-Driven Repayment (IDR) Plans

For federal loan borrowers who find the Standard Plan payments unaffordable, Income-Driven Repayment (IDR) plans are a crucial safety net. These plans base your monthly payment on your income and family size, rather than your loan balance, making them more manageable during periods of lower earnings. After 20 or 25 years of qualifying payments (depending on the plan and loan type), any remaining balance may be forgiven, though it might be subject to income tax. The main IDR plans include:

- Revised Pay As You Earn (REPAYE): Generally caps payments at 10% of your discretionary income.

- Pay As You Earn (PAYE): Also 10% of discretionary income, but usually has an interest rate cap.

- Income-Based Repayment (IBR): Payments are 10% or 15% of discretionary income, depending on when you received your first loans.

- Income-Contingent Repayment (ICR): Payments are either 20% of your discretionary income or what you would pay on a fixed 12-year payment plan, whichever is less.

It’s vital to re-certify your income and family size annually to ensure your payments remain accurate. Failing to do so can lead to increased payments or interest capitalization.

Graduated and Extended Repayment Plans

Beyond IDR and Standard plans, federal loans offer other options:

- Graduated Repayment Plan: Payments start lower and increase every two years, still over a 10-year term. This can be helpful if you expect your income to rise steadily.

- Extended Repayment Plan: Allows you to stretch payments over 25 years. This results in lower monthly payments than the Standard Plan but significantly increases the total interest paid over the life of the loan. You must have more than $30,000 in direct loans to qualify.

These plans offer greater flexibility but generally come with a higher total cost over the long term.

Refinancing and Consolidation

For both federal and private loans, two major strategies can alter your repayment structure:

- Federal Direct Consolidation: This process combines multiple federal loans into a single new federal loan with one monthly payment. It can extend your repayment period, potentially lower your monthly payment, and make you eligible for certain IDR plans or forgiveness programs you weren’t before. However, it can also lead to more total interest paid over time and you lose any remaining benefits of individual loans (like interest subsidies).

- Private Refinancing: This involves taking out a new private loan to pay off your existing student loans (federal, private, or both). The primary goal is often to secure a lower interest rate, which can save you a substantial amount of money over the loan’s life, or to combine multiple loans into one. You might also choose a new repayment term. However, refinancing federal loans into a private loan means forfeiting all federal loan protections and benefits, including IDR plans, deferment, forbearance, and access to federal forgiveness programs. This step should be carefully considered and typically makes sense only for those with stable, high incomes and excellent credit who are confident they won’t need federal protections.

Navigating Challenges and Optimizing Repayment

Even with a well-chosen repayment plan, life can throw curveballs. It’s crucial to know your options for temporary relief and strategies for optimizing your repayment journey to pay off debt faster or manage it more effectively.

What to Do If You Can’t Pay: Deferment and Forbearance

If you face temporary financial hardship, such as job loss, illness, or economic downturn, federal student loans offer vital protections:

- Deferment: Allows you to temporarily postpone loan payments. For some federal loans (like subsidized loans), interest does not accrue during deferment. Common reasons include enrollment in school, unemployment, economic hardship, or military service.

- Forbearance: Also allows you to temporarily stop or reduce payments. However, interest typically accrues on all loan types during forbearance, which can increase your total loan cost. Forbearance is generally granted for up to 12 months at a time.

Both options offer a temporary reprieve but should be used strategically as interest can continue to accumulate, ultimately increasing your debt. Always explore IDR plans first, as they adjust payments based on income and may offer a more sustainable long-term solution.

Understanding Loan Forgiveness Programs

Certain federal loan borrowers may qualify for loan forgiveness programs, which discharge some or all of their remaining loan balance. These are often tied to specific professions or service:

- Public Service Loan Forgiveness (PSLF): Available to full-time employees of government or qualifying non-profit organizations. After making 120 qualifying monthly payments under a qualifying repayment plan (usually an IDR plan), the remaining balance on Direct Loans may be forgiven.

- Teacher Loan Forgiveness: For teachers who work for five complete and consecutive academic years in low-income schools or educational service agencies. Depending on the subject taught, eligible teachers may receive up to $17,500 in loan forgiveness.

- Other Forgiveness Programs: There are also specialized programs for nurses, doctors in underserved areas, and other professions, as well as discharge options for total and permanent disability or school closure.

Investigate these programs thoroughly if you believe you might qualify, as they can significantly reduce your debt burden.

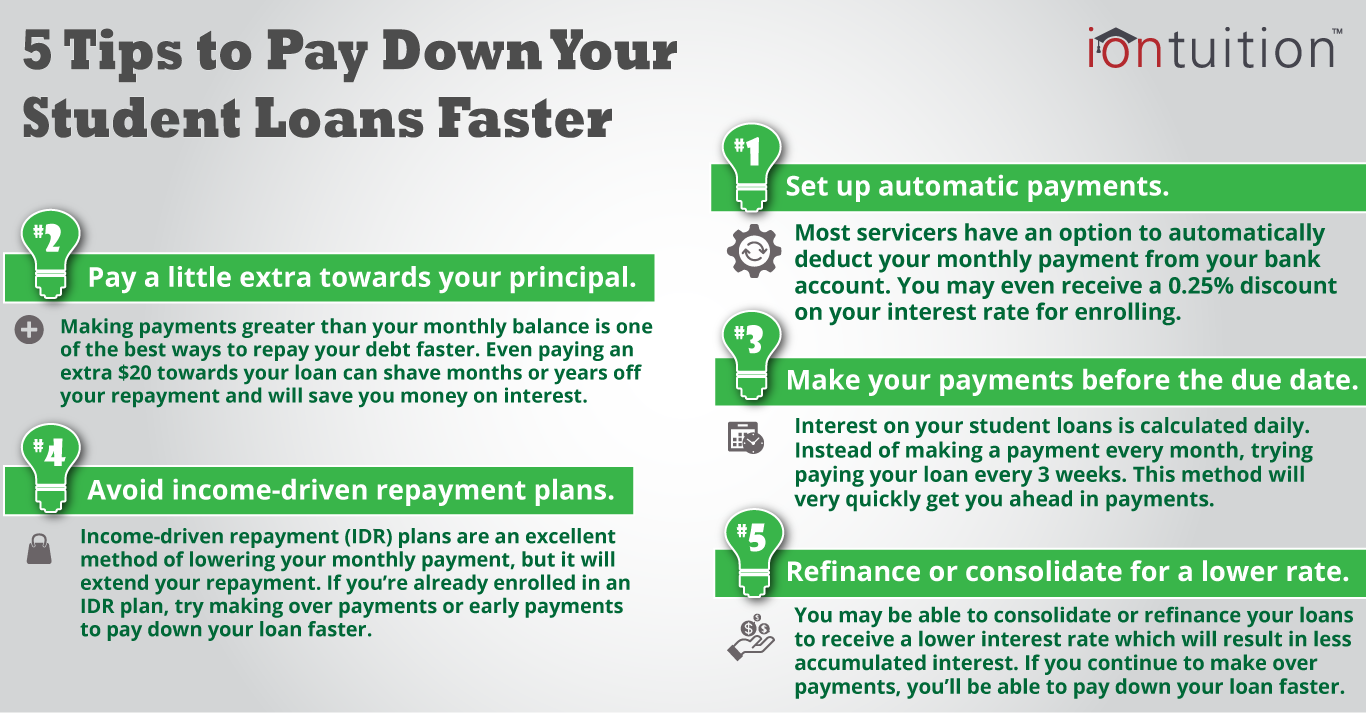

Strategies for Accelerating Repayment

If your financial situation allows, accelerating your loan repayment can save you thousands in interest and free you from debt sooner.

- Pay More Than the Minimum: Even an extra $50 or $100 per month can make a significant difference over the life of the loan. Instruct your servicer to apply extra payments to the principal balance.

- Make Bi-Weekly Payments: Instead of one monthly payment, pay half your monthly amount every two weeks. This results in 13 full payments per year instead of 12, effectively adding an extra payment annually.

- Round Up Payments: If your payment is $287, round it up to $300. Small, consistent increases add up.

- Apply Windfalls: Use bonuses, tax refunds, or unexpected income to make lump-sum payments toward your principal.

- Debt Avalanche or Snowball Method:

- Avalanche: Pay off the loan with the highest interest rate first while making minimum payments on others. This saves the most money on interest.

- Snowball: Pay off the smallest balance loan first for psychological momentum, then roll that payment into the next smallest.

The Impact of Interest Capitalization

Interest capitalization occurs when unpaid interest is added to your loan’s principal balance. This increases the principal, meaning future interest will be calculated on a larger amount, leading to higher overall costs. Capitalization can happen after periods of deferment or forbearance (if interest accrued), if you leave an IDR plan, or if you fail to re-certify your income on an IDR plan. Understanding when and why this happens can help you avoid it or minimize its impact.

The Long-Term Impact of Student Loan Repayment

Managing student loans effectively isn’t just about making monthly payments; it’s about integrating this debt into your broader financial life and understanding its long-term implications. How you handle your student loans can significantly affect your credit score, your ability to save, and your pursuit of major life goals.

Credit Score Implications

Your student loan repayment history is reported to credit bureaus and plays a significant role in your credit score.

- Positive Impact: Consistent, on-time payments demonstrate financial responsibility and build a strong credit history, which is crucial for obtaining favorable rates on mortgages, car loans, and credit cards.

- Negative Impact: Late payments, missed payments, or defaulting on your loans can severely damage your credit score, making it difficult and more expensive to borrow money in the future. A default can remain on your credit report for seven years and lead to wage garnishment, tax refund offsets, and even a loss of professional licenses.

It’s paramount to communicate with your loan servicer immediately if you foresee difficulty making a payment. Proactive communication can help you explore options before a negative mark impacts your credit.

Balancing Student Loans with Other Financial Goals

Student loan debt can feel like a heavy anchor, but it shouldn’t completely derail your other financial aspirations. A balanced approach is key:

- Emergency Fund: Prioritize building an emergency fund of 3-6 months’ worth of living expenses. This provides a buffer against unforeseen financial hardships, reducing the likelihood of missing loan payments.

- Retirement Savings: Don’t neglect retirement savings. Even small contributions to a 401(k) (especially if there’s an employer match) or an IRA early in your career can compound significantly over time. The “opportunity cost” of delaying retirement savings can be enormous.

- Homeownership: Student loan debt can affect your debt-to-income (DTI) ratio, a key factor lenders consider for mortgages. Managing your student loans responsibly and strategically reducing the principal can improve your DTI and your chances of qualifying for a mortgage.

- Other Debt: Evaluate high-interest debts, such as credit card balances. Sometimes, tackling these first can free up more cash flow to apply to student loans, or vice versa, depending on interest rates.

The strategy of “paying yourself first” applies here: allocate funds to savings and investments alongside your debt repayment.

Seeking Professional Financial Advice

While this guide provides a comprehensive overview, personal finance is inherently personal. There may be complex situations, unique loan structures, or specific financial goals that warrant individualized attention.

- Certified Financial Planners (CFPs): Can help you integrate student loan repayment into your broader financial plan, including retirement, investments, and estate planning.

- Student Loan Counselors: Organizations like the National Foundation for Credit Counseling (NFCC) offer certified credit counselors who can help you understand your options and create a personalized repayment plan.

- Tax Professionals: Can advise on the tax implications of interest deductions, IDR plan forgiveness (which can be taxable income), and other tax-related aspects of student loans.

Don’t hesitate to seek professional guidance when needed. An objective, expert perspective can provide clarity, identify overlooked opportunities, and offer peace of mind.

Conclusion

Repaying student loans is a marathon, not a sprint, demanding patience, discipline, and an informed strategy. From understanding the nuances of federal versus private loans to selecting the most suitable repayment plan and navigating potential hardships, every step you take brings you closer to financial freedom. By being proactive, leveraging available resources, and integrating your repayment strategy into your overall financial plan, you can transform what initially felt like an insurmountable burden into a manageable and ultimately conquerable goal. Your financial future is largely in your hands; arm yourself with knowledge, make thoughtful decisions, and commit to consistent action, and you will successfully repay your student loans, paving the way for a more secure and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.