The journey to purchasing a new vehicle is often fraught with a myriad of decisions, with perhaps the most significant being the financial commitment involved. In an ever-evolving economic landscape, understanding the average price of a car is more complex than a simple number; it’s a dynamic interplay of market forces, technological advancements, consumer demand, and personal financial readiness. This article delves deep into the current automotive market, dissecting the factors that influence car prices and offering insights into how prospective buyers can navigate this crucial financial decision with wisdom and foresight. Far from being a static figure, the “average price” is a moving target, influenced by everything from global supply chains to local dealership incentives, demanding a comprehensive financial perspective from anyone looking to invest in a set of wheels.

Understanding the Shifting Landscape of Car Prices

The automotive market is a microcosm of the global economy, constantly reacting to supply-demand dynamics, technological innovation, and broader financial trends. For many, a car represents the second-largest purchase they will ever make, only surpassed by a home. Therefore, comprehending the underlying mechanisms that dictate vehicle pricing is paramount for sound financial planning. The notion of an “average price” needs to be contextualized, distinguishing between new and used vehicles, different segments, and the economic conditions prevalent at any given time.

The Current Financial Snapshot: New vs. Used Cars

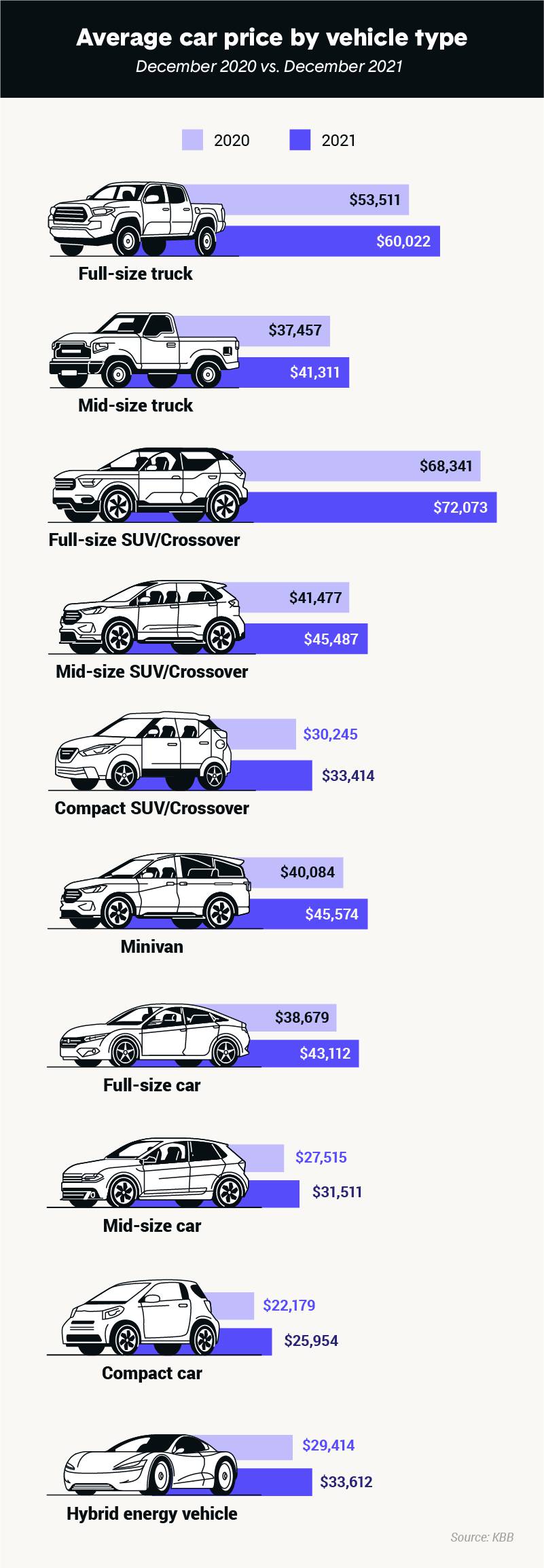

Historically, the average price of a new car has steadily climbed, reflecting advancements in safety, infotainment, performance, and increasingly, electrification. As of early 2024, the average transaction price for a new vehicle in many major markets hovers around the mid-$40,000 to low-$50,000 range. This figure, however, can fluctuate significantly based on brand, vehicle type (sedan, SUV, truck, luxury), and included features.

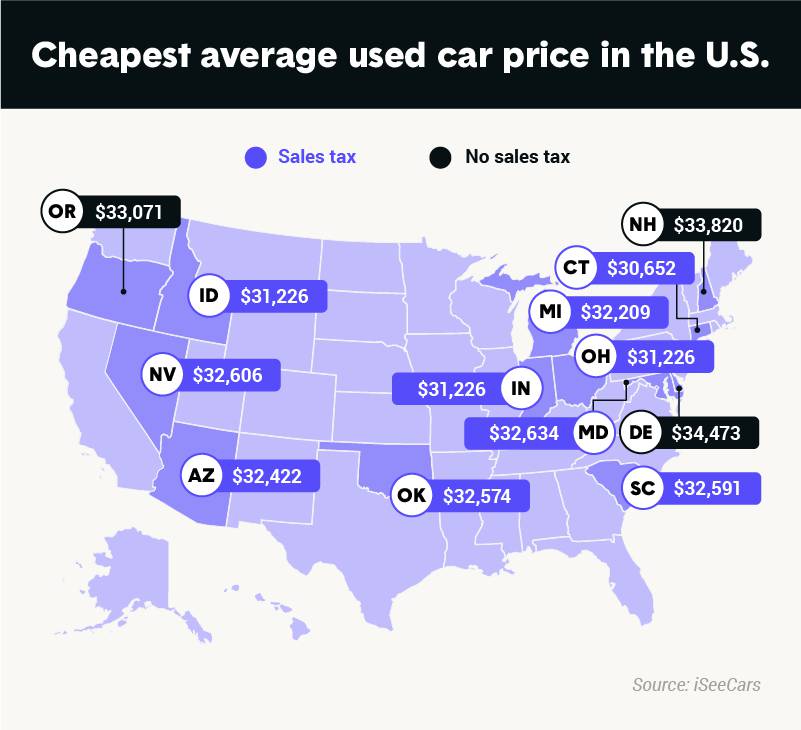

The used car market, while typically offering a more affordable entry point, has experienced unprecedented volatility in recent years. Supply chain disruptions, particularly the semiconductor chip shortage that began during the pandemic, severely curtailed new vehicle production. This created a ripple effect, driving up demand and prices for used cars to historic highs. While prices have begun to stabilize and even slightly decrease from their peaks, the average used car price remains significantly elevated compared to pre-pandemic levels, often residing in the high-$20,000 to mid-$30,000 range. This dynamic underscores the importance of carefully evaluating the financial benefits and drawbacks of both new and used car purchases.

Key Factors Driving Price Volatility

Several macroeconomic and industry-specific factors conspire to create the current pricing environment:

- Supply Chain Resilience: The availability of critical components, from microchips to raw materials like lithium for batteries, directly impacts production volumes. Any disruption can lead to shortages and inflated prices.

- Inflationary Pressures: Broader economic inflation translates into higher manufacturing costs, increased labor expenses, and elevated transportation fees, all of which are passed on to the consumer.

- Interest Rates: Central bank policies on interest rates directly influence the cost of auto loans. Higher interest rates mean a more expensive financing package, increasing the total cost of ownership even if the sticker price remains unchanged.

- Consumer Demand and Preferences: A shift towards larger, more feature-rich SUVs and trucks, often with higher profit margins, has also contributed to the upward creep of average prices. The growing demand for electric vehicles (EVs), which typically command a higher initial price tag, also plays a role.

- Technological Advancements: Modern vehicles are packed with advanced safety features, sophisticated infotainment systems, and complex powertrain technologies. While these add value, they also add to the manufacturing cost.

Regional and Market Segment Disparities

The “average price” can also vary significantly by geographic region within a country, influenced by local taxes, registration fees, and regional demand. For instance, luxury vehicle markets in affluent urban areas might skew averages upward. Similarly, different market segments — economy sedans versus full-size pickup trucks or premium SUVs — will have vastly different average price points. It’s crucial for buyers to consider how their specific needs and location fit into the broader pricing matrix.

Beyond the Sticker Price: The True Cost of Car Ownership

While the initial purchase price is a significant financial hurdle, it represents only a fraction of the total cost of car ownership. Prudent financial planning requires a holistic view that encompasses all ongoing expenses, many of which can accumulate to hundreds or even thousands of dollars annually. Ignoring these “hidden” costs can lead to financial strain and undermine the perceived affordability of a vehicle.

Financing Considerations: Loans, Interest, and Depreciation

The vast majority of new car purchases, and a significant portion of used car acquisitions, are financed through loans. The principal loan amount, interest rate, and loan term are critical variables. A higher interest rate, even on a slightly lower sticker price, can result in a greater total expenditure over the life of the loan. Longer loan terms (e.g., 72 or 84 months) reduce monthly payments but increase the total interest paid and can extend the period during which the vehicle’s value depreciates faster than the principal is paid down, leading to negative equity.

Depreciation, the loss of a vehicle’s value over time, is arguably the most significant “cost” of car ownership. New cars typically lose 15-20% of their value in the first year and continue to depreciate by 10-15% annually for the next few years. Understanding a vehicle’s depreciation curve is vital, especially when considering resale value or future trade-ins.

Insurance, Maintenance, and Fuel: Ongoing Expenses

These are the immediate, tangible costs that accrue from day one:

- Insurance: Premiums vary wildly based on the vehicle type, driver’s age and record, location, and chosen coverage levels. High-value or high-performance vehicles typically incur higher insurance costs.

- Maintenance: Regular maintenance (oil changes, tire rotations, brake service) is essential for longevity and safety. As vehicles age, more significant repairs become inevitable. Luxury and specialized vehicles often have higher maintenance costs due to proprietary parts and specialized labor.

- Fuel/Charging: Fuel efficiency (or electric range and charging costs) is a major ongoing expense. Fluctuating gas prices or rising electricity rates can significantly impact monthly budgets. The type of fuel required (regular vs. premium) also plays a role.

The Hidden Costs: Taxes, Fees, and Future Resale Value

Beyond the primary ongoing expenses, several other financial elements contribute to the true cost:

- Sales Tax and Registration Fees: These vary by state or province and can add several hundred to several thousand dollars to the initial purchase. Annual registration renewals are also recurring costs.

- Dealership Fees: These can include documentation fees, delivery charges, and other administrative costs. While some are legitimate, buyers should scrutinize any excessive or vaguely described fees.

- Customization and Accessories: Aftermarket additions, while enhancing the vehicle, add to the overall investment without always proportionally increasing resale value.

- Future Resale Value: A vehicle’s ability to retain its value can significantly offset its depreciation. Brands known for reliability and strong resale values might command a higher initial price but cost less in the long run. Factors like color, trim level, and vehicle condition also impact resale.

Navigating the Market: Financial Strategies for Car Buyers

With a clear understanding of both the average purchase price and the full scope of ownership costs, prospective car buyers are better equipped to make financially sound decisions. Strategic planning and informed decision-making are key to securing the best deal and ensuring a purchase that aligns with one’s financial capacity.

Budgeting for Your Purchase: Affordability vs. Desirability

Before even looking at cars, establish a realistic budget. This isn’t just about the monthly payment; it’s about the total cost. Financial experts often recommend that car payments, insurance, and fuel combined should not exceed 10-15% of your net monthly income. Consider setting aside an emergency fund for unexpected repairs. Prioritize affordability over pure desirability. While a dream car might be tempting, an affordable car that fits your financial means will offer greater long-term financial stability. Use online budgeting tools to project monthly expenses comprehensively.

New vs. Used: A Financial Trade-off Analysis

The choice between a new and a used car is a pivotal financial decision.

- New Cars: Offer the latest technology, full warranty coverage, and often better financing rates. However, they suffer from rapid depreciation in the first few years. They are a good choice for those who prioritize the latest features, desire a full warranty, and plan to keep the car for an extended period to mitigate the impact of initial depreciation.

- Used Cars: Offer significant savings on the purchase price and avoid the steepest depreciation curve. However, they come with potentially higher maintenance costs (especially older models), limited or no warranty, and sometimes higher interest rates on loans. They are ideal for budget-conscious buyers who are comfortable with potentially older technology and have a robust emergency fund for repairs. Certified Pre-Owned (CPO) programs can offer a middle ground, combining some warranty protection with the cost savings of a used vehicle.

Lease vs. Buy: Understanding the Financial Implications

- Leasing: Essentially renting a car for a set period (typically 2-4 years) with a mileage limit. Monthly payments are generally lower than buying, and you always drive a new car under warranty. At the end of the lease, you return the car or have an option to buy it. Financially, leasing is best for those who enjoy driving new cars frequently, drive a predictable number of miles, and don’t mind not building equity in the vehicle. It’s a consumption model, not an ownership model.

- Buying: You own the car outright once payments are complete, building equity over time. There are no mileage restrictions, and you can customize it as you wish. While initial payments might be higher, you eventually eliminate a monthly car payment and can drive the car for as long as it lasts, offering significant long-term savings. This is generally the more financially sound option for those who keep cars for many years.

Smart Negotiation Tactics and When to Buy

Always negotiate the price. Research the fair market value of the car you’re interested in using online resources. Be prepared to walk away if the deal isn’t right. Consider paying cash if possible to avoid interest payments entirely. The best times to buy often include the end of the month, quarter, or year when dealerships are trying to meet sales quotas, or during major holiday sales events. Waiting for a new model year to be released can also result in discounts on the outgoing models.

The Impact of Economic Trends on Automotive Affordability

Broader economic forces exert a profound influence on both the price of vehicles and a consumer’s ability to afford them. Staying abreast of these trends is crucial for making timely and financially advantageous decisions in the automotive market.

Inflation’s Grip: Erosion of Purchasing Power

Inflation directly impacts the cost of goods and services, and cars are no exception. As the cost of raw materials, labor, and transportation rises, so do vehicle prices. More critically, persistent inflation erodes consumer purchasing power. Even if salaries increase, if they don’t keep pace with inflation, the effective cost of a car becomes higher. This dynamic makes saving for a down payment more challenging and can push desired vehicles further out of reach.

Interest Rate Hikes and Loan Costs

Central banks adjust interest rates to manage inflation and economic growth. When interest rates rise, the cost of borrowing money for an auto loan increases. Even a seemingly small increase in the Annual Percentage Rate (APR) can add hundreds or thousands of dollars to the total cost of a vehicle over a typical 5-7 year loan term. This means that a car that was affordable at a 3% APR might become prohibitively expensive at a 7% APR, even if its sticker price hasn’t changed. Buyers need to factor current interest rates into their budgeting and understand that waiting for rates to fall might be a financially advantageous strategy, or conversely, locking in a low rate when available is wise.

Supply Chain Resilience and its Effect on Inventory

The disruptions caused by global events, from pandemics to geopolitical tensions, highlight the fragility of complex automotive supply chains. Shortages of critical components, such as semiconductors, lead to reduced vehicle production, which in turn results in lower inventory levels at dealerships. When demand outstrips supply, prices inevitably rise, and consumers have less leverage for negotiation. A return to more resilient supply chains would likely stabilize inventory, leading to more competitive pricing and better availability. Monitoring production forecasts and inventory levels in real-time can inform buying decisions, suggesting when to wait for more stock or when to act on limited availability.

Leveraging Financial Tools and Resources for a Prudent Purchase

In today’s digital age, a wealth of financial tools and resources are available to empower car buyers. Utilizing these effectively can transform a daunting purchase into a well-informed and strategic financial move, ensuring the average car price doesn’t become an average financial burden.

Online Calculators and Budgeting Apps

Before stepping into a dealership, harness the power of online auto loan calculators. These tools allow you to input different purchase prices, down payments, interest rates, and loan terms to instantly see estimated monthly payments. Many also calculate the total interest paid over the life of the loan. Coupled with personal budgeting apps, these resources can help you integrate a potential car payment into your overall financial plan, ensuring you don’t overextend yourself. They also help visualize the long-term cost implications of various financing options.

Credit Score Management for Better Loan Terms

Your credit score is a powerful determinant of the interest rate you’ll be offered on an auto loan. Lenders view higher credit scores as indicative of lower risk, leading to more favorable rates and potentially saving you thousands of dollars over the loan’s term. Before applying for financing, check your credit report for inaccuracies and work to improve your score if needed. Paying bills on time, reducing outstanding debt, and avoiding new credit applications immediately prior to a car purchase can significantly impact your financial leverage.

Expert Financial Advice and Dealership Savvy

While online resources are invaluable, sometimes professional guidance can make a difference. Consulting a financial advisor about how a significant car purchase fits into your broader financial goals can provide personalized insights. When engaging with dealerships, remember that their primary goal is to maximize profit. Arm yourself with research, be prepared to negotiate not just the car price but also your trade-in value, and scrutinize every line item in the contract. Consider getting pre-approved for a loan from your bank or credit union before visiting a dealership; this provides a benchmark and negotiation leverage, allowing you to focus on the car price rather than the financing details. Don’t be pressured into purchasing add-ons or extended warranties that don’t offer clear financial value.

In conclusion, understanding the average price of a car extends far beyond a simple figure. It requires a keen awareness of market dynamics, the full spectrum of ownership costs, prevailing economic trends, and the strategic use of financial tools. By adopting a professional, insightful, and financially savvy approach, consumers can navigate the complexities of the automotive market, making a purchase that truly aligns with their long-term financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.