In the intricate world of personal finance, certain pieces of information act as the foundational keys to managing your money effectively. Among the most critical are your bank account number and routing number. These seemingly simple strings of digits are the backbone of virtually every financial transaction, from receiving your paycheck to paying your bills. Understanding what they are, why they matter, and, most importantly, how to locate them is paramount for anyone navigating their financial life with confidence and security. This guide will demystify these essential banking identifiers, providing a clear roadmap for finding them and insights into their crucial role in your financial ecosystem.

Understanding the Cornerstones of Your Financial Identity

Before delving into the “how-to,” it’s vital to grasp the fundamental nature and purpose of routing and account numbers. They are not interchangeable but rather work in tandem to ensure your money reaches its intended destination securely and efficiently.

What is a Routing Number?

A routing number, often referred to as an ABA (American Bankers Association) transit number, is a nine-digit code that identifies the specific financial institution and its location where an account is held. Think of it as your bank’s address within the vast financial network. When you send money to or from an account, the routing number tells the system which bank to send the funds to.

These numbers are critical for automated clearing house (ACH) transactions, such as direct deposits, automatic bill payments, and electronic transfers between banks. They also play a role in wire transfers and, traditionally, in processing paper checks. While most banks have a primary routing number, larger institutions, or those operating across different regions, might have multiple routing numbers depending on the type of transaction or the specific branch where the account was opened.

What is an Account Number?

Your account number is a unique identifier for your specific checking, savings, or money market account within your financial institution. While routing numbers identify the bank, account numbers pinpoint your individual account at that bank. Typically ranging from 10 to 12 digits, though this can vary, your account number ensures that once funds arrive at the correct bank (identified by the routing number), they are credited or debited to the right individual or entity.

Every financial transaction involving your specific bank account will require this number. It’s your personal identifier for all account-related activities, making it a highly sensitive piece of information. Unlike routing numbers, which can be shared publicly as they identify the institution, account numbers are exclusively tied to you and should be protected diligently.

Why Are These Numbers So Crucial?

The importance of routing and account numbers cannot be overstated. They are the twin pillars supporting the vast majority of modern financial transactions. Without them, the seamless movement of money that we often take for granted would grind to a halt.

Consider direct deposit: your employer uses your bank’s routing number and your specific account number to electronically send your wages directly into your account. Similarly, when you set up automatic bill payments, these numbers facilitate the recurring transfer of funds from your account to your utility provider, landlord, or credit card company. They are also essential for wire transfers, peer-to-peer payment services (when linking an external bank account), and even for simply looking up your account balance or transaction history with customer service. In essence, they are the coordinates that allow your money to travel accurately and securely across the financial landscape.

Navigating the Digital and Physical Realms to Locate Your Numbers

While some people know their account numbers by heart, many do not, and remembering your bank’s specific routing number can be even more challenging. Fortunately, there are several reliable methods to quickly and securely find this vital information.

The Traditional Method: Your Checkbook

For many years, the checkbook was the most common place to find both your routing and account numbers. This remains a simple and effective method for those who still use paper checks.

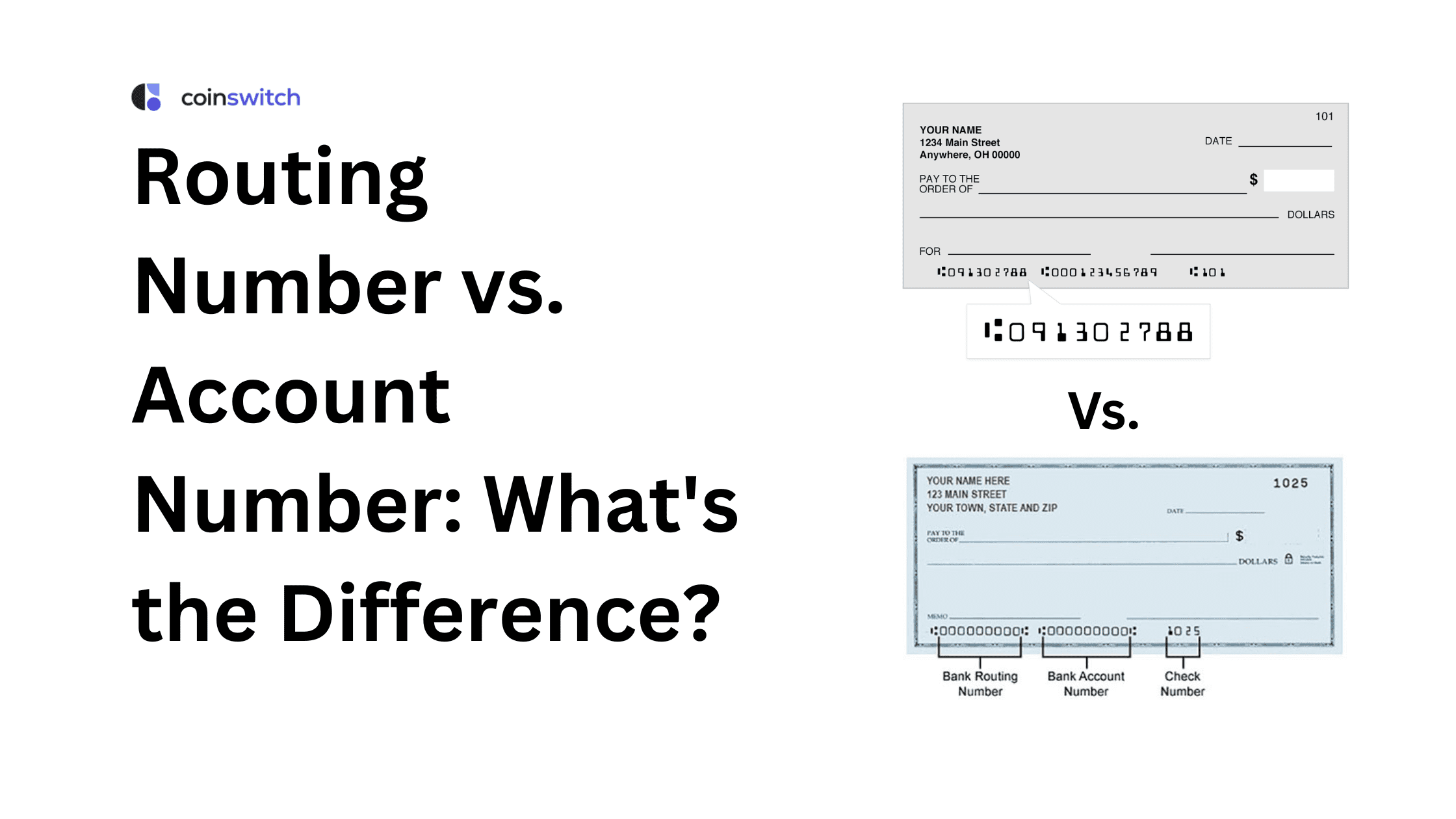

- How to locate: On the bottom of a personal check, you’ll typically see three sets of numbers printed in magnetic ink. From left to right, these are usually:

- Routing Number: The first set of nine digits.

- Account Number: The second set of numbers (length varies).

- Check Number: The third, shorter set of digits, matching the number printed in the top right corner of the check.

It’s important to note that the order can occasionally vary slightly, but the routing number is almost always the nine-digit code, and the account number is usually longer than the check number.

Online Banking Portals: Instant Access at Your Fingertips

In today’s digital age, online banking is arguably the most convenient and common way to access your account information. Most banks make it straightforward to find your routing and account numbers once you’ve logged in.

- How to locate:

- Log in: Access your bank’s official website or mobile app using your secure credentials.

- Navigate to Account Details: Look for a section like “Account Summary,” “Account Details,” “Statements,” or click on the specific checking or savings account you wish to view.

- Find the Information: Your routing and account numbers are often displayed prominently on the account details page. Sometimes, you may need to click an additional link like “Show Details,” “View Account & Routing Numbers,” or similar. For security reasons, some banks might initially mask the numbers (e.g., showing only the last few digits) and require you to click to reveal the full sequence.

Your Monthly Bank Statements

Whether you receive paper statements in the mail or access them electronically, your bank statements are a reliable source for your account information.

- How to locate:

- Paper Statements: Scan the statement for a section usually labeled “Account Summary” or similar. Both your routing number and full account number are typically printed near your name and address, or within the details of your account balance.

- Electronic Statements: If you access statements through your online banking portal, download a PDF copy of your most recent statement. The information will be structured similarly to a paper statement. This is often a good backup if the direct “Account Details” page is less clear.

Direct Communication with Your Bank

If all other methods prove difficult or you prefer direct assistance, contacting your bank is always an option.

- How to locate:

- Customer Service: Call your bank’s customer service line. Be prepared to verify your identity with personal information (e.g., full name, address, date of birth, mother’s maiden name, Social Security number) before they will disclose your account numbers.

- Visit a Branch: Go to a local branch of your bank. A teller or customer service representative can provide your account and routing numbers after verifying your identity, usually requiring a photo ID. This is often the quickest method for in-person assistance.

Practical Applications: When You’ll Need Your Numbers

Knowing how to find your routing and account numbers is one thing; understanding when and why you’ll need them is another. These numbers are indispensable for a wide array of financial tasks.

Setting Up Direct Deposit and Automatic Withdrawals

This is arguably one of the most common uses. When you start a new job, your employer will typically request your routing and account numbers to set up direct deposit for your paychecks. Similarly, many utility companies, loan providers, and subscription services offer automatic withdrawals, requiring this information to pull funds directly from your account on a recurring basis. Providing these numbers ensures your income arrives promptly and your bills are paid on time without manual intervention.

Initiating Wire Transfers and ACH Transactions

Whether you’re sending a large sum of money to purchase a property, or simply transferring funds to a friend’s account at another institution, these numbers are essential.

- Wire Transfers: For expedited, high-value transfers, both your bank’s routing number and your account number (along with the recipient’s corresponding details) are mandatory. Wire transfers are typically irreversible and subject to fees.

- ACH Transactions: For less urgent, lower-cost electronic transfers, ACH (Automated Clearing House) services rely heavily on routing and account numbers. This includes setting up recurring payments, inter-bank transfers, and even some online payment platforms.

Paying Bills Electronically

Beyond direct debits, many online bill payment systems allow you to manually enter your bank account and routing number to make one-time or recurring payments directly from your checking account, bypassing credit cards or third-party processors. This is often preferred for avoiding credit card processing fees or managing cash flow directly.

Linking External Accounts and Financial Apps

In today’s interconnected financial landscape, you might want to link your bank account to various external services. This could include:

- Investment Platforms: Funding a brokerage account or transferring money to a retirement account.

- Budgeting Tools: Connecting your bank account to apps like Mint or Personal Capital for automated transaction tracking.

- Peer-to-Peer Payment Apps: While some use debit cards, linking your bank account directly often allows for larger transfers or withdrawal of funds.

- Other Bank Accounts: Transferring money between your own accounts held at different financial institutions.

In all these scenarios, your routing and account numbers serve as the secure bridge for transferring funds and data.

Safeguarding Your Financial Information: Security Best Practices

Given their critical role, your routing and account numbers are sensitive pieces of information that demand careful protection. Unauthorized access could lead to significant financial fraud or identity theft.

The Risks of Unauthorized Access

If a scammer obtains your routing and account numbers, they could potentially:

- Initiate unauthorized withdrawals from your account.

- Forge checks.

- Make unauthorized electronic payments.

- Attempt to access other financial services by impersonating you.

While banks have fraud protection measures in place, preventing unauthorized access in the first place is always the best defense.

Secure Handling and Storage

- Physical Checks: Keep your checkbook in a secure location. Avoid leaving loose checks lying around. When disposing of old checks or bank statements, shred them thoroughly.

- Digital Records: Only access your online banking from secure, trusted devices and networks. Never save your login credentials on public computers. Be wary of where you store digital copies of bank statements or documents containing this information. Password-protect any sensitive files.

- Emails and Texts: Your bank will never ask you to email or text your full account number, routing number, or other sensitive information. Be extremely suspicious of any unsolicited requests for this data.

Verifying Recipients and Transactions

Always double-check the legitimacy of any request for your banking information. If you’re setting up a new direct deposit or automatic payment, confirm the details with the recipient through an independent channel (e.g., calling a known customer service number, not one provided in an email). Verify that the company or individual you are providing your numbers to is legitimate and trustworthy.

Recognizing and Avoiding Scams

Be vigilant against phishing attempts, where scammers try to trick you into revealing your banking details through fake emails, websites, or phone calls. Look for red flags such as poor grammar, urgent threats, or requests to click suspicious links. Your bank will use secure, encrypted channels for communication and will never ask for your full account details via unsecured methods. If in doubt, contact your bank directly using their official contact information.

Distinguishing Between Similar Numbers and Avoiding Common Misconceptions

The financial world is rife with various numerical identifiers, and it’s easy to confuse them. A clear understanding prevents errors and enhances security.

Credit Card Numbers vs. Bank Account Numbers

It’s a common mistake to confuse a credit card number with a bank account number.

- Credit Card Number: This is a 13- to 19-digit number that identifies your specific credit card account. It’s used for purchases and credit transactions. While tied to your credit issuer, it does not directly link to your checking or savings account for withdrawals. Sharing this poses a risk to your credit line.

- Bank Account Number: This is specific to your checking, savings, or money market account and is used for direct debits, deposits, and transfers of actual funds held in your bank account. Sharing this number carries the risk of direct fund withdrawal.

Never use a credit card number when a bank account number is requested, or vice-versa.

Different Routing Numbers for Different Transaction Types

While your bank usually has a primary routing number, it’s not uncommon for larger institutions to have different routing numbers for specific purposes.

- ACH vs. Wire Transfers: Some banks use a distinct routing number for incoming wire transfers compared to the routing number used for ACH transactions (like direct deposits). Always verify the correct routing number for the specific type of transaction you are initiating or receiving. Using the wrong one can delay or even reject a transfer.

- Regional Variations: Historically, banks in different regions might have had different routing numbers. While less common with national banks today, it’s still possible depending on the bank’s structure.

Always confirm the correct routing number with your bank or on your bank’s official website for the exact transaction type and account you are using.

Business vs. Personal Account Numbers

While the fundamental structure and purpose remain the same, business accounts often have their own unique account numbers, distinct from any personal accounts you might hold with the same bank. Furthermore, depending on the business entity type (sole proprietorship, LLC, corporation), routing numbers might also differ, particularly for specific business services or international transactions. Always ensure you are using the correct account and routing numbers specific to the business account when conducting business-related financial activities. Accuracy is key to avoiding delays and errors in business finance, which can have significant operational impacts.

Mastering the art of finding and protecting your routing and account numbers is a fundamental skill for sound financial management. By understanding their purpose, knowing where to locate them, recognizing their practical applications, and adhering to robust security practices, you empower yourself to navigate your financial landscape with efficiency, confidence, and peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.