The year 1929 stands as an indelible marker in the annals of financial history, a pivot point that dramatically reconfigured global economic thought and practice. While the “Roaring Twenties” had been characterized by unprecedented prosperity, technological innovation, and a burgeoning consumer culture, 1929 delivered a stark, brutal awakening. It was the year the speculative bubble burst, exposing deep-seated vulnerabilities within the financial system and unleashing a cascade of events that would plunge the world into the most severe economic downturn it had ever witnessed. To understand “what was going on in 1929” is to delve into a complex interplay of market exuberance, unchecked speculation, structural economic weaknesses, and a profound lack of regulatory foresight that ultimately led to the Wall Street Crash and laid the groundwork for the Great Depression. This retrospective aims to dissect the financial landscape of that fateful year, offering insights into its causes, immediate impacts, and enduring lessons for modern finance.

(Note: As I cannot access the local file D:/Canh/Hugo/aviewfromthecave/node-aviewfromthecave/HTML/what_was_going_on_in_1929.txt, the following content and structure are derived from general historical knowledge about the financial events of 1929, tailored to the “Money” category.)

The Zenith of Speculation: A Market on Borrowed Time

Leading up to 1929, the American economy, and by extension much of the Western world, had enjoyed nearly a decade of sustained growth and optimism. Post-World War I recovery, coupled with technological advancements like widespread electrification, the automobile, and radio, fueled industrial output and consumer spending. This economic boom, however, fostered an environment of increasingly reckless financial behavior, particularly in the stock market. The allure of quick riches drew ordinary citizens and seasoned investors alike into a speculative frenzy that, in hindsight, was unsustainable.

Unprecedented Market Exuberance

The stock market became the primary arena for this optimism. Share prices soared to dizzying heights, often disconnected from the underlying value or earnings potential of the companies they represented. Iconic indices saw year-on-year double-digit growth, creating a powerful psychological feedback loop where rising prices attracted more buyers, further inflating prices. People genuinely believed that stocks could only go up, driven by an almost mystical faith in American ingenuity and endless prosperity. This widespread belief, often termed “irrational exuberance,” overshadowed any sober assessment of risk. Investing transitioned from a long-term strategy of capital allocation to a short-term game of speculation, where the aim was simply to buy low and sell higher, often within days or weeks.

The Peril of Margin Buying

A critical accelerant to this speculative fire was the pervasive practice of “buying on margin.” This allowed investors to purchase stocks by putting down only a small percentage of the stock’s price (often as little as 10-20%) and borrowing the rest from their broker. The borrowed money was secured by the stocks themselves. As long as stock prices continued to rise, investors could leverage small amounts of capital into large profits. However, this also meant that a relatively small dip in stock prices could trigger a “margin call,” forcing investors to deposit more funds or sell their holdings. This created an incredibly fragile financial ecosystem, where a market correction could quickly turn into a panic, as falling prices forced more margin calls, leading to more selling, and a vicious downward spiral. Banks and brokers, eager for commission and interest payments, readily extended these loans, further entrenching the risk throughout the financial system.

Black Tuesday and the Unraveling of Confidence

The bubble burst definitively in October 1929, culminating in a series of catastrophic market days that would forever be etched into financial history. These events didn’t just wipe out fortunes; they shattered public confidence in the financial system and the broader economy, setting off a chain reaction that would define the next decade.

The Cracks Appear: Black Thursday

The first major tremor occurred on Thursday, October 24, 1929. Following several days of declining prices, a wave of panic selling hit the New York Stock Exchange. The market opened with a sharp drop, and by noon, prices were in freefall. Trading volume surged to unprecedented levels as investors desperately tried to unload their shares. Leading bankers, including J.P. Morgan Jr. and Charles E. Mitchell of National City Bank, attempted to stem the tide by pooling resources and buying large blocks of stocks above current market prices, a tactic that had worked in the Panic of 1907. This intervention brought a temporary reprieve, and the market recovered some ground by the close, leading to a cautiously optimistic outlook in Friday’s papers. The feeling was that the worst was over.

The Cataclysm: Black Monday and Black Tuesday

The respite was tragically short-lived. The following Monday, October 28, the market plunged again, suffering an unprecedented 12.8% loss, an event now known as “Black Monday.” The sheer scale of the decline ignited widespread fear. Any remaining hope evaporated on Tuesday, October 29 – “Black Tuesday.” The selling intensified into a full-blown panic. An astonishing 16 million shares were traded, a record that would stand for nearly 40 years. Ticker tapes ran hours behind, creating chaos and uncertainty as investors couldn’t confirm transaction prices. Prices plummeted across the board, wiping out billions of dollars in market value. Fortunes accumulated over years, sometimes generations, vanished in mere hours. The crash wasn’t a single event but a prolonged period of intense selling that saw the Dow Jones Industrial Average lose nearly 90% of its value between its peak in September 1929 and its trough in July 1932.

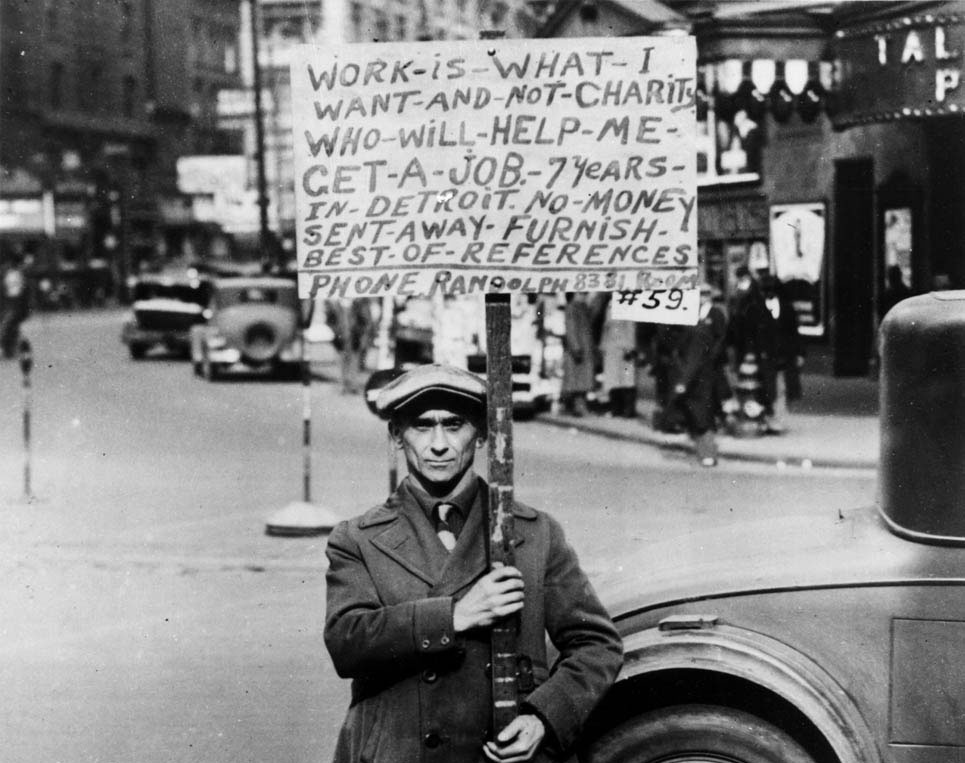

Immediate Repercussions on Personal and Business Finance

The immediate impact of the crash was devastating. Investors who had bought on margin were ruined, often losing not only their entire investment but also owing their brokers money. Banks that had lent heavily to brokers and investors faced massive losses, leading to widespread closures. Businesses found their access to capital severely restricted. Consumer confidence plummeted, leading to a sharp drop in spending. This contraction in demand forced businesses to cut production, leading to layoffs, which in turn further reduced consumer spending. The financial pain quickly spread beyond the stock market, affecting every facet of the economy and marking the definitive end of the Roaring Twenties.

Deep-Seated Economic Fragilities and Systemic Weaknesses

While the stock market crash was the dramatic trigger, 1929’s events were amplified by underlying structural problems within the American and global economies. These long-simmering issues meant that the crash was not merely a market correction, but a catalyst for a much deeper and prolonged economic crisis.

Agricultural Distress and Overproduction

Even during the boom years of the 1920s, a significant sector of the American economy was already in recession: agriculture. Following World War I, European demand for American farm products declined as European agriculture recovered. Farmers, encouraged by wartime demand, had expanded production and taken on debt. The resulting oversupply led to continually falling crop prices throughout the decade. Farmers struggled to pay their mortgages and loans, leading to widespread foreclosures and rural poverty. This meant that a large segment of the population had already depleted their savings and possessed little purchasing power, making the overall economy more vulnerable to a shock.

Unequal Distribution of Wealth

Another critical underlying issue was the highly unequal distribution of wealth and income. While industrial output soared, the benefits were disproportionately concentrated at the top. A relatively small percentage of the population controlled the vast majority of the nation’s wealth. This meant that the economy relied heavily on continued investment by the wealthy and the spending power of a small elite. When the crash occurred, and the wealth of this elite evaporated, there was no broad-based consumer demand to cushion the blow. The vast majority of working-class and middle-class families had little savings and were living paycheck to paycheck, leaving them extremely vulnerable to job losses and economic downturns. This imbalance created a fragile consumer market, unable to sustain economic growth when investment faltered.

Flaws in the Financial and Regulatory System

The financial system of 1929 was remarkably unregulated compared to today. There was no federal deposit insurance (FDIC), meaning that bank runs were a constant threat. When banks failed, depositors lost all their savings. The Federal Reserve, established in 1913, failed to act as an effective lender of last resort or to adequately manage the money supply. Its initial response to the crisis was to raise interest rates, fearing inflation, which further choked off credit and exacerbated the contraction. There were also no strict rules regarding corporate transparency, accounting standards, or insider trading, allowing for widespread manipulation and a lack of investor protection. The banking system was fragmented, with thousands of small, independent banks susceptible to local downturns, amplifying the collapse of confidence.

Lessons Learned: Preventing Future Catastrophes

The harrowing experience of 1929 and the subsequent Great Depression served as a brutal, yet invaluable, lesson for policymakers, economists, and individuals. The immediate aftermath prompted critical reevaluations of government’s role in the economy and laid the foundation for modern financial regulation.

The Imperative of Robust Regulation and Oversight

One of the most profound lessons was the critical need for governmental oversight of financial markets. The lack of regulation allowed speculative excesses to spiral out of control. In response, the New Deal era introduced landmark legislation:

- The Securities Act of 1933 and the Securities Exchange Act of 1934: These acts created the Securities and Exchange Commission (SEC) to regulate stock exchanges, prevent fraud, and ensure greater transparency in financial markets.

- Glass-Steagall Act (1933): Separated commercial banking from investment banking, aimed at preventing banks from engaging in risky speculative activities with depositor funds. (Though largely repealed in 1999, the principle of financial separation and risk mitigation remains debated).

- Federal Deposit Insurance Corporation (FDIC, 1933): Provided government insurance for bank deposits, restoring public confidence in the banking system and preventing bank runs.

These measures transformed the financial landscape, creating safeguards designed to prevent a recurrence of the 1929 collapse.

Central Bank’s Role: Lender of Last Resort and Monetary Policy

The Federal Reserve’s failure to adequately respond to the crisis highlighted the critical role of central banks. Modern central banking principles now emphasize the importance of acting as a lender of last resort during financial crises, providing liquidity to prevent system-wide collapses. Furthermore, the understanding of monetary policy’s impact on economic cycles has evolved significantly, with central banks now actively managing interest rates and money supply to stabilize economies.

Personal Financial Prudence and Risk Management

For individuals, 1929 underscored the enduring importance of sound personal financial management. The dangers of excessive leverage, speculative bubbles, and concentrated investments became painfully clear. The principles of diversification, investing based on fundamentals rather than hype, maintaining emergency savings, and avoiding high-risk debt remain as relevant today as they were almost a century ago. The memory of 1929 serves as a constant reminder that financial markets, while offering opportunities for growth, are also susceptible to irrational behavior and systemic risks.

Conclusion: 1929’s Enduring Legacy in Finance

“What was going on in 1929” transcends a simple historical account; it is a foundational narrative in the study of economics and finance. It represents a watershed moment where the perceived invincibility of free markets collided with the harsh realities of speculative excess and systemic fragility. The catastrophic events of that year irrevocably altered government’s relationship with the economy, giving birth to a framework of regulation and central bank intervention designed to temper the volatility of capitalism. While financial crises have continued to occur in various forms throughout history, the lessons from 1929 – about the dangers of unchecked speculation, the importance of equitable wealth distribution, and the necessity of robust financial oversight – continue to inform policy debates and guide personal financial decisions, ensuring its place as a cornerstone of financial education and historical awareness.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.