For aspiring entrepreneurs and seasoned business owners alike, securing adequate funding is often the critical determinant of growth, stability, and even survival. A small business loan can be the lifeline that transforms an innovative idea into a thriving enterprise, helps an existing company expand operations, or provides essential working capital during lean times. However, navigating the complex landscape of business finance to find the right loan can be a daunting task. This comprehensive guide will demystify the options available, providing insights into various lending sources and how to best position your business for success.

Understanding Your Funding Needs and Loan Types

Before embarking on the quest for a loan, it’s crucial to first understand precisely what your business needs the capital for and what type of financing best suits those needs. Different loans are designed for different purposes, and a clear strategy will significantly streamline your search.

Defining Your Capital Requirements

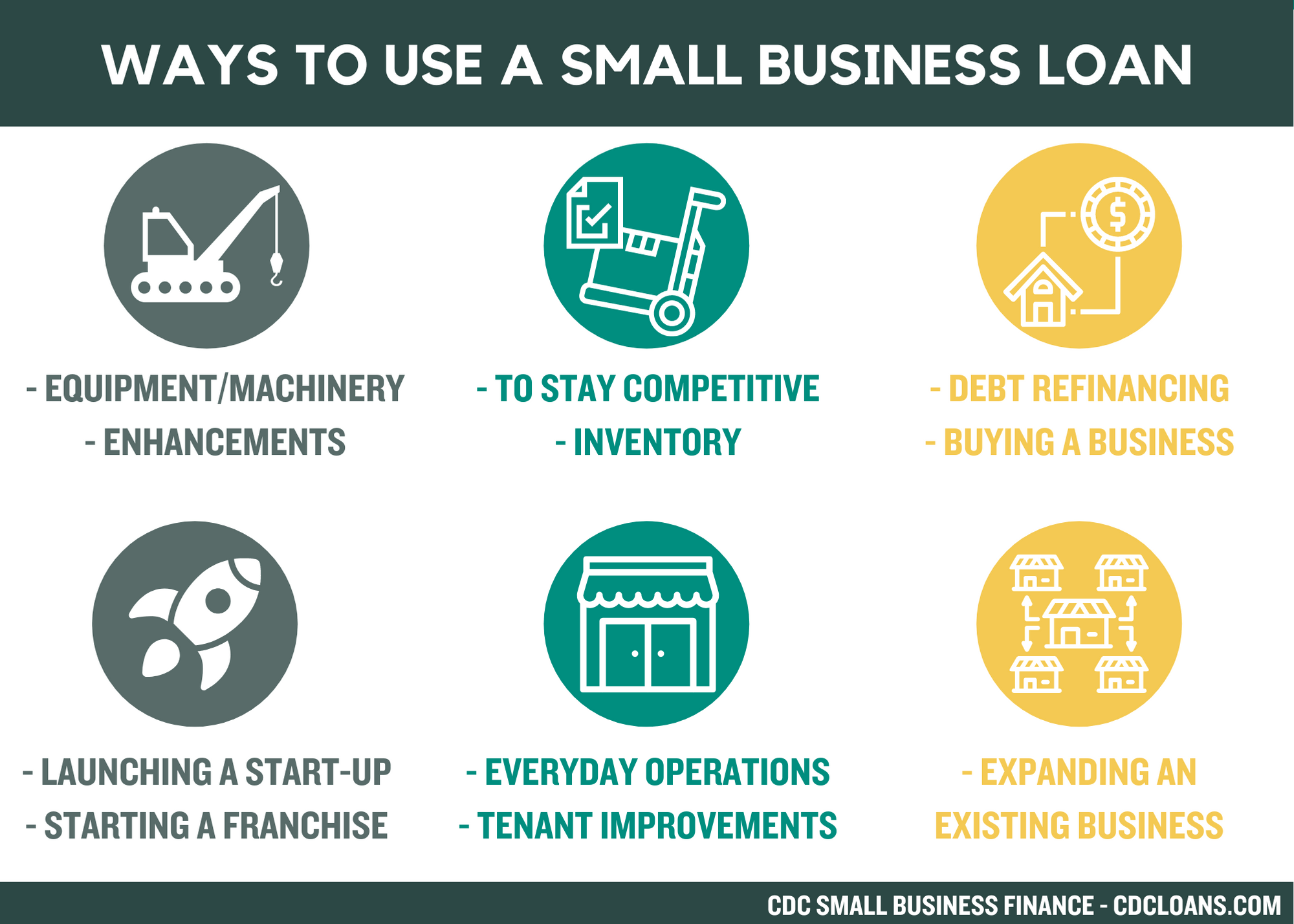

The first step is to quantify your funding gap. Are you seeking capital for startup costs, inventory purchase, equipment upgrades, marketing campaigns, or perhaps to bridge a cash flow gap? A detailed financial projection and a clear understanding of how the funds will be utilized are indispensable. This will not only guide your search but also be a cornerstone of your loan application. Knowing your exact need – whether it’s $5,000 for a microloan or $500,000 for a major expansion – will narrow down the field of potential lenders considerably.

Common Small Business Loan Types

The world of business loans offers a variety of structures, each with its own advantages and ideal use cases:

- Term Loans: These are perhaps the most traditional form of financing, offering a lump sum of capital that is repaid over a fixed period, typically with fixed interest rates. They are excellent for significant, one-time investments like purchasing equipment or real estate.

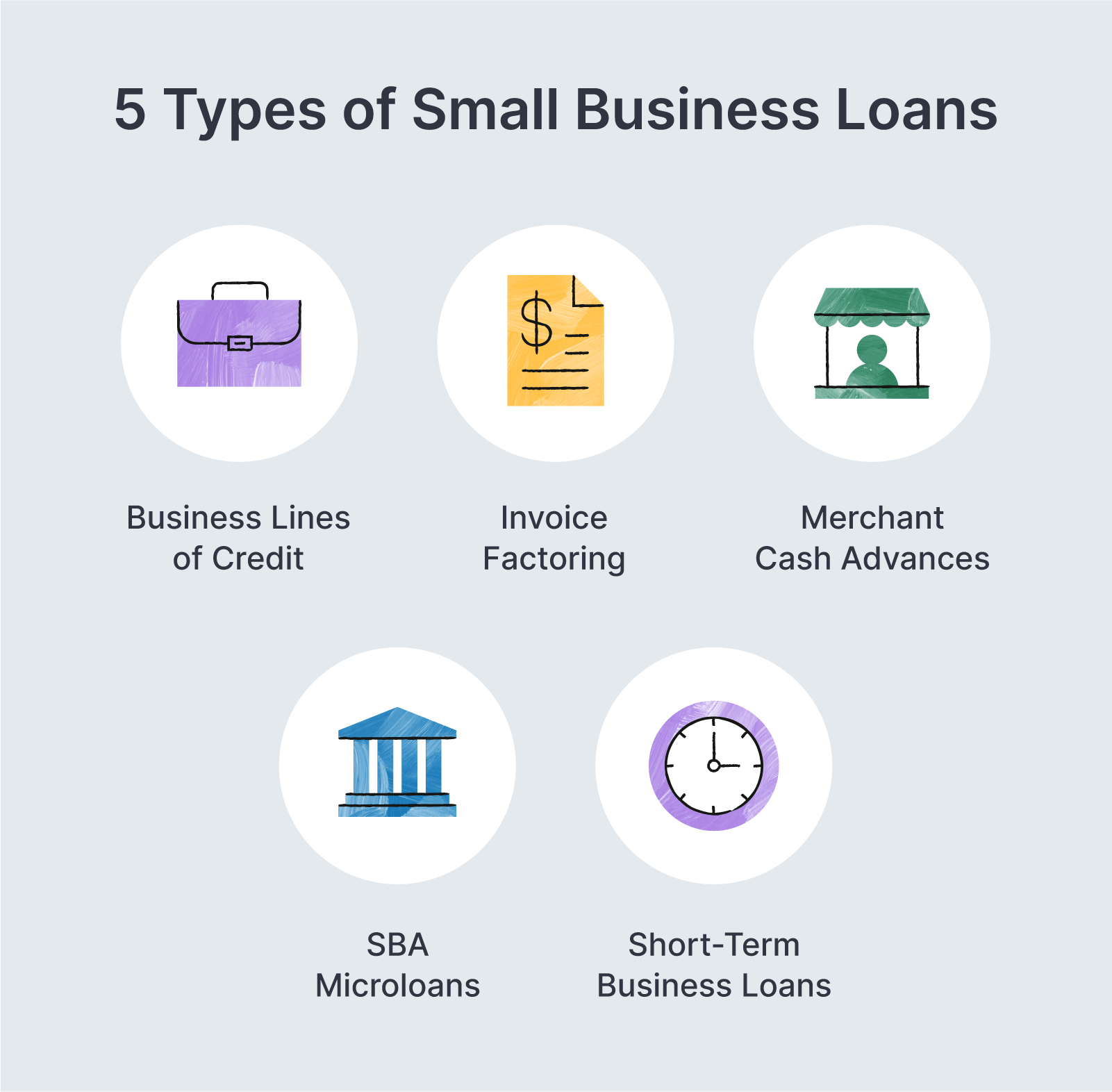

- Lines of Credit: Unlike term loans, a line of credit provides access to a maximum amount of funds that can be drawn upon as needed, repaid, and then redrawn. It’s akin to a credit card for your business, ideal for managing fluctuating cash flow or covering unexpected expenses.

- SBA Loans (Small Business Administration): Government-backed loans offered through a network of partner lenders. SBA loans come with attractive terms, lower interest rates, and longer repayment periods, making them highly sought after.

- Microloans: Smaller loans, often under $50,000, typically offered by non-profit organizations or community development financial institutions (CDFIs). These are designed to support startups and very small businesses, often those that struggle to secure traditional financing.

- Equipment Financing: A specialized loan where the equipment itself serves as collateral. This allows businesses to acquire necessary machinery or technology without tying up other assets.

- Invoice Factoring/Financing: This involves selling your outstanding invoices (accounts receivable) to a third party at a discount to get immediate cash. It’s a viable option for businesses with many slow-paying customers.

- Merchant Cash Advances (MCAs): A lump sum payment provided in exchange for a percentage of future credit card sales. While fast and accessible, MCAs often come with very high effective interest rates and are generally considered a last resort.

Exploring Traditional Lending Institutions

For many businesses, traditional banks and credit unions remain the first port of call due to their established reputation, competitive rates, and comprehensive financial services.

Commercial Banks

Major banks such as Chase, Bank of America, Wells Fargo, and countless regional institutions offer a wide array of small business loan products. They are typically the most cost-effective option for businesses with strong financial histories and solid credit scores.

- Pros: Generally lower interest rates, longer repayment terms, established reputation, and often a broader suite of financial services (checking accounts, treasury management, etc.).

- Cons: Stricter eligibility requirements, lengthy application processes, and often a preference for businesses with a proven track record (typically two years or more in operation). Startup businesses may find it challenging to qualify.

- Eligibility: Banks typically look for strong personal and business credit scores, a detailed business plan, comprehensive financial statements (profit and loss, balance sheet, cash flow), collateral, and sufficient cash flow to cover debt service.

Credit Unions

Often overlooked, credit unions can be excellent alternatives to large commercial banks, particularly for small and community-focused businesses. As member-owned non-profits, they often offer more personalized service and may be more flexible with lending criteria.

- Pros: Potentially lower interest rates and fees compared to banks, more personalized customer service, community-focused approach, and sometimes more lenient underwriting for local businesses.

- Cons: Loan amounts may be smaller than what major banks offer, and their technology platforms might not be as sophisticated as those of larger institutions.

- Eligibility: Similar to banks, but credit unions might place a greater emphasis on the borrower’s relationship with the institution and local community impact. Good credit, a solid business plan, and demonstrable repayment capacity are essential.

Navigating Alternative and Online Lenders

The financial technology (FinTech) revolution has profoundly reshaped the lending landscape, offering faster, more accessible, and often more flexible financing options, particularly for businesses that may not qualify for traditional bank loans.

Online Lenders

A rapidly expanding sector, online lenders leverage technology to streamline the application and approval process, often providing funding within days, sometimes even hours. Companies like OnDeck, Funding Circle, and Bluevine offer various products, from term loans to lines of credit.

- Pros: Rapid application and approval process, less stringent eligibility criteria than traditional banks, often more accommodating to newer businesses or those with less-than-perfect credit, and convenient online platforms.

- Cons: Generally higher interest rates and fees compared to banks, shorter repayment terms, and less personalized service. Borrowers must carefully review all terms to avoid costly surprises.

- Eligibility: Requirements vary widely but often focus on cash flow, business revenue, and shorter operational histories (e.g., 6 months to 1 year). Personal credit scores are still considered but may not be the sole determining factor.

Peer-to-Peer (P2P) Lending

P2P platforms connect borrowers directly with individual or institutional investors willing to fund small business loans. Platforms like Funding Circle (which also offers direct online lending) facilitate these connections.

- Pros: Can offer competitive rates, potentially more flexible terms, and access to funding for businesses that might be rejected by traditional lenders.

- Cons: The availability and terms depend on investor appetite, and platform fees can add to the overall cost.

- Eligibility: Typically assessed based on business financials, credit history, and the perceived risk by individual investors.

Merchant Cash Advances (MCAs)

While technically not a loan, MCAs are an advance on future credit or debit card sales. A fixed sum is provided, and the lender takes a percentage of daily sales until the advance, plus a fee, is repaid.

- Pros: Very fast funding, minimal documentation, and approval based on sales volume rather than credit score or collateral. Accessible to businesses with poor credit.

- Cons: Extremely high effective interest rates (often annualized to triple-digits), short repayment periods, and can quickly become a debt trap if sales decline. This option should be approached with extreme caution.

- Eligibility: Primarily based on consistent daily or monthly credit card sales volume.

Government-Backed Programs: SBA Loans

The U.S. Small Business Administration (SBA) doesn’t lend money directly (except in disaster situations) but instead guarantees a portion of loans made by approved lenders. This reduces the risk for lenders, encouraging them to offer loans on more favorable terms to small businesses.

The SBA 7(a) Loan Program

This is the most popular and flexible SBA program, suitable for a wide range of business purposes, including working capital, equipment purchase, real estate acquisition, and refinancing existing debt.

- Pros: Longer repayment terms (up to 25 years for real estate, 10 years for equipment/working capital), lower down payments, competitive interest rates (capped by the SBA), and no balloon payments.

- Cons: Extensive application process, significant paperwork, and strict eligibility requirements that can lead to longer approval times.

- Eligibility: Businesses must meet the SBA’s definition of “small,” be for-profit, operate in the U.S., and have equity invested by the owner. Lenders will assess creditworthiness, management experience, and capacity to repay.

SBA Microloan Program

Targeted towards very small businesses and startups, the Microloan program provides loans up to $50,000, administered through non-profit community-based organizations.

- Pros: Ideal for businesses needing smaller amounts of capital, often accompanied by business counseling and technical assistance, making it suitable for first-time entrepreneurs.

- Cons: Loan amounts are capped, and the administrative process, while less rigorous than 7(a), still requires diligence.

- Eligibility: Similar to other SBA programs but with an emphasis on local community impact and a willingness to participate in business support services.

Other SBA Programs

The SBA offers other specialized programs, such as the SBA 504 loan for major fixed-asset purchases (real estate, equipment), and disaster loans, which provide financial assistance to businesses located in declared disaster areas. Each program has unique eligibility and use cases.

Preparing for Your Loan Application

Regardless of where you seek funding, thorough preparation is paramount to increasing your chances of approval and securing the best possible terms. Lenders want to see a clear picture of your business’s health and potential.

Building a Strong Financial Foundation

Before approaching any lender, ensure your business’s financial house is in order. This includes:

- Comprehensive Business Plan: A detailed document outlining your business model, market analysis, marketing and sales strategy, operational plan, and management team. This proves you have a clear vision and strategy.

- Financial Statements: Up-to-date and accurate profit and loss statements, balance sheets, and cash flow projections for at least the past three years (if applicable). New businesses will need robust projections.

- Personal and Business Credit Scores: Lenders will review both. Work to improve any deficiencies in your personal credit, as it heavily influences early-stage business financing. Monitor your business credit score through agencies like Dun & Bradstreet, Experian Business, and Equifax Business.

- Collateral: Many loans, especially traditional bank loans, require collateral (assets like real estate, equipment, or accounts receivable) to secure the loan, mitigating risk for the lender.

- Tax Returns: Personal and business tax returns for the past few years provide historical financial verification.

- Legal Documents: Business licenses, articles of incorporation, partnership agreements, and any other relevant legal paperwork.

Demonstrating Repayment Capacity

Lenders fundamentally want assurance that you can repay the loan. This is assessed through your business’s cash flow. Be prepared to show how the borrowed funds will generate enough income or savings to comfortably cover the loan principal and interest payments. A strong debt service coverage ratio (DSCR) is a key metric lenders evaluate.

Choosing the Right Loan for Your Business

With numerous options available, selecting the ideal loan can feel overwhelming. The key is to compare offers meticulously and consider factors beyond just the interest rate.

Key Comparison Factors

When evaluating loan offers, look beyond the headline interest rate:

- Annual Percentage Rate (APR): This provides the true annual cost of a loan, including interest and all fees. It’s the best metric for comparing different loan offers.

- Repayment Terms: Understand the loan duration, frequency of payments (daily, weekly, monthly), and whether there are any prepayment penalties or balloon payments.

- Fees: Be aware of origination fees, application fees, closing costs, and any other hidden charges that can add significantly to the overall cost.

- Flexibility: Does the loan offer flexibility in drawing funds, or is it a one-time lump sum? Can you easily adjust payments if needed (though this is rare)?

- Speed of Funding: If you need capital quickly, online lenders or MCAs might be your only viable options, despite their higher costs. For planned expansions, traditional and SBA loans offer better terms.

- Lender Reputation and Support: Choose a lender with a good reputation and a track record of supporting small businesses. Good customer service can be invaluable.

The Importance of Due Diligence

Never rush into a loan agreement. Read all terms and conditions carefully, ask questions, and don’t hesitate to seek advice from a financial advisor or an attorney specializing in business finance. A poorly chosen loan can hinder your business’s growth rather than fuel it.

Securing a small business loan is a significant step, representing both a financial commitment and a vote of confidence in your entrepreneurial journey. By understanding your needs, exploring the diverse range of funding sources, preparing diligently, and comparing options wisely, you can confidently navigate the lending landscape and find the capital that empowers your business to thrive.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.