The Price-to-Earnings (P/E) ratio is one of the most fundamental metrics in the world of finance, offering a snapshot of how the market values a company’s earnings. When applied to an entire index like the S&P 500, it becomes a crucial barometer for assessing the overall market’s valuation and investor sentiment. Understanding the S&P 500’s P/E ratio is not merely an academic exercise; it’s an essential tool for investors, economists, and analysts to gauge whether the market is overvalued, undervalued, or fairly priced relative to its historical performance and economic context.

This ratio encapsulates the collective market sentiment towards the earnings power of the 500 largest publicly traded companies in the United States, representing approximately 80% of the total U.S. equity market capitalization. A high P/E might suggest that investors expect strong future growth, or perhaps that the market is currently in an optimistic, or even euphoric, phase. Conversely, a low P/E could indicate subdued growth expectations, investor pessimism, or a potentially undervalued market. Delving into the nuances of the S&P 500’s P/E provides invaluable insights into the broader financial landscape, helping to inform strategic investment decisions and risk assessments in a complex global economy.

Understanding the Price-to-Earnings (P/E) Ratio

At its core, the Price-to-Earnings (P/E) ratio is a valuation multiple that measures a company’s current share price relative to its per-share earnings. For investors, it offers a quick way to determine how much they are willing to pay for each dollar of a company’s earnings.

Definition and Calculation

The basic formula for the P/E ratio is straightforward:

P/E Ratio = Market Price Per Share / Earnings Per Share (EPS)

- Market Price Per Share: This is the current trading price of a single share of a company’s stock. For an index like the S&P 500, this is derived from the aggregate market capitalization of all constituent companies divided by the total number of shares outstanding for the index (a conceptual aggregate, or more practically, the P/E is calculated by taking the sum of the market capitalizations of all companies in the index and dividing it by the sum of their earnings).

- Earnings Per Share (EPS): This represents a company’s profit allocated to each outstanding share of common stock. For an index, it’s the sum of the EPS of all component companies, weighted by their market capitalization.

The resulting number tells investors how many times earnings the market is willing to pay for the stock. For instance, a P/E of 20 means investors are paying $20 for every $1 of the company’s annual earnings.

Types of P/E: Trailing, Forward, and Shiller P/E

While the basic formula is simple, there are different variations of the P/E ratio, each offering a distinct perspective:

- Trailing P/E: This is the most common type, calculated using the past 12 months’ (or four most recent quarters’) earnings per share. It’s based on actual, historical data, making it reliable and objective. However, it’s backward-looking and may not reflect current or future business conditions.

- Forward P/E: This ratio uses estimated future earnings per share, typically for the next 12 months. It’s forward-looking and reflects analysts’ expectations for a company’s or an index’s future profitability. While potentially more relevant to current investment decisions, it relies on forecasts, which can be inaccurate.

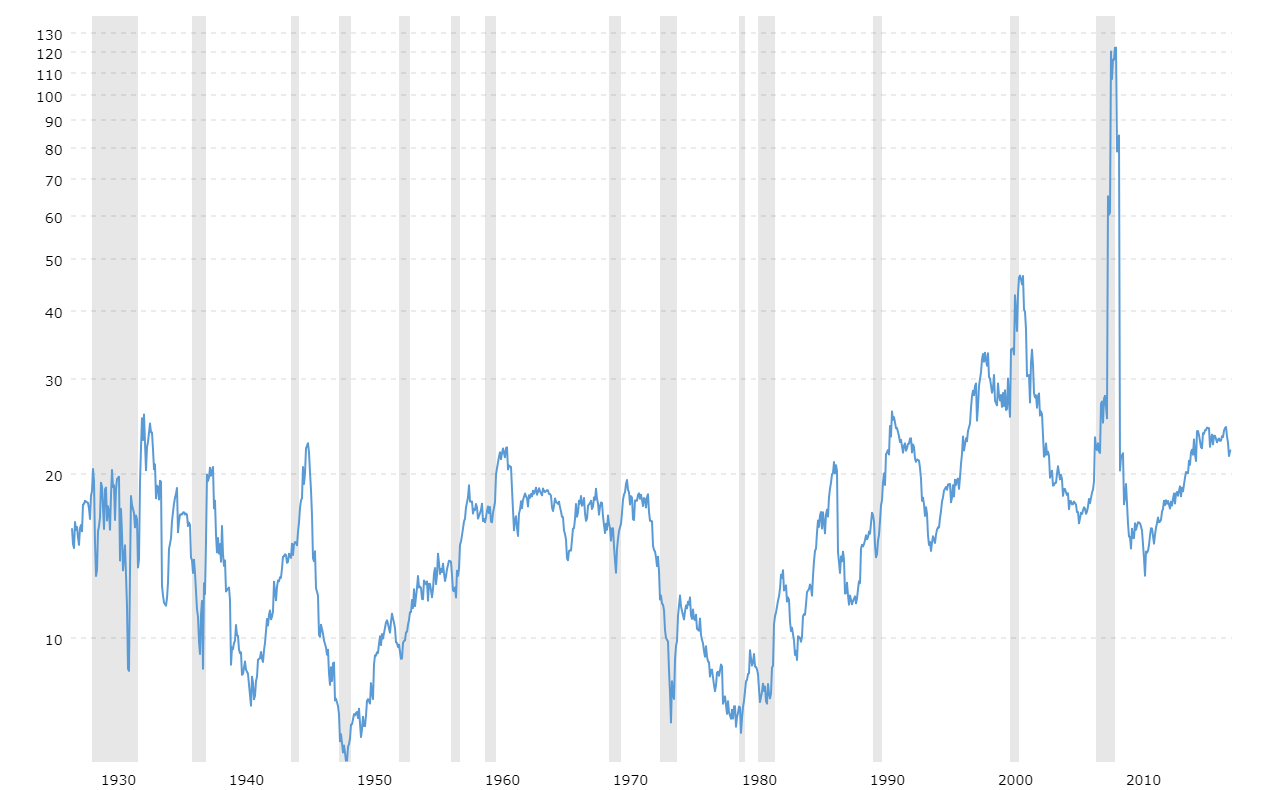

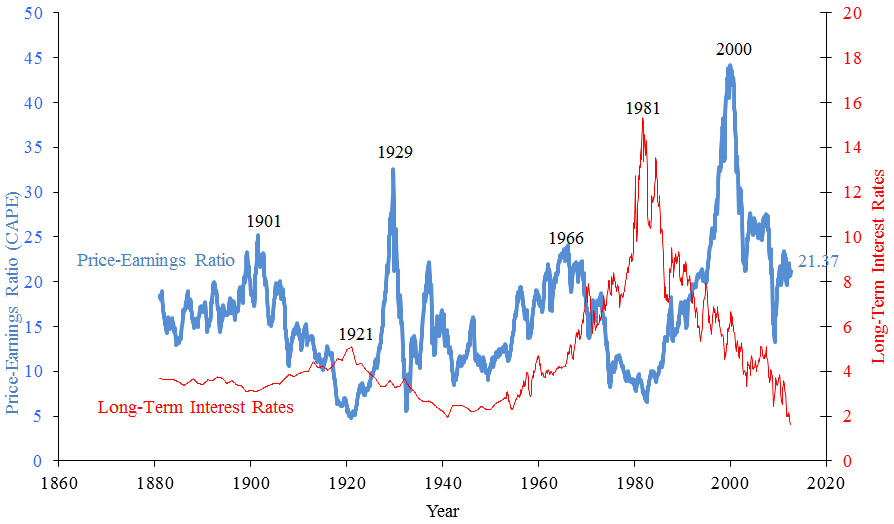

- Shiller P/E (CAPE Ratio – Cyclically Adjusted P/E Ratio): Developed by Nobel laureate Robert Shiller, the CAPE ratio aims to smooth out cyclical fluctuations in earnings by averaging real (inflation-adjusted) EPS over the past 10 years. This smoothed average is then divided into the current real market price. The Shiller P/E is considered a more robust indicator of long-term market valuation, often used to predict potential future returns over longer horizons. It helps to identify periods when earnings might be temporarily inflated or depressed, providing a clearer picture of underlying valuation trends.

What a High vs. Low P/E Implies

The interpretation of a P/E ratio depends heavily on context:

- High P/E: A high P/E ratio generally indicates that investors have high expectations for future earnings growth. They are willing to pay a premium today for anticipated higher earnings tomorrow. It can also signify a “growth stock” or a market experiencing strong bullish sentiment. However, an exceptionally high P/E might suggest the market is overvalued or that the stock/index is in a bubble, making it more vulnerable to corrections if growth expectations aren’t met.

- Low P/E: A low P/E ratio often suggests that investors have lower expectations for future growth, or that the market perceives the company/index as having higher risk. It could indicate a “value stock” or a market that is undervalued and potentially ripe for recovery. However, a very low P/E could also signal underlying problems, such as declining earnings, increased competition, or systemic economic issues.

The S&P 500: A Benchmark for the U.S. Stock Market

The S&P 500 is more than just a list of companies; it’s a critical barometer for the health and direction of the U.S. economy and its equity markets. Its composition and behavior reflect the broader economic narrative, making its valuation a key point of analysis.

What is the S&P 500?

The S&P 500, or Standard & Poor’s 500, is a stock market index maintained by S&P Dow Jones Indices. It comprises 500 of the largest publicly traded companies in the United States, selected by a committee based on criteria such as market size, liquidity, and sector representation. Unlike some other indices, the S&P 500 is market-capitalization weighted, meaning companies with larger market values have a greater impact on the index’s performance and, consequently, on its aggregate P/E ratio. This weighting ensures that the index accurately reflects the economic impact of its largest constituents. Its diverse composition spans all major sectors, from technology and finance to healthcare and industrials, providing a comprehensive representation of the U.S. economy.

Why its P/E Matters

The P/E ratio of the S&P 500 is crucial because it provides an overarching view of the valuation of the U.S. stock market as a whole. It serves multiple vital functions:

- Economic Barometer: The S&P 500’s P/E can reflect prevailing economic conditions and expectations. During periods of robust economic growth and low interest rates, P/E ratios tend to be higher as investors anticipate strong corporate earnings and are willing to pay more for future income streams. Conversely, economic slowdowns or rising interest rates can lead to lower P/Es.

- Investor Sentiment: Beyond fundamental economics, the index’s P/E ratio is a powerful indicator of collective investor sentiment. High P/Es often accompany bullish enthusiasm and risk-on attitudes, while low P/Es might signal widespread fear, uncertainty, or a preference for safer assets.

- Long-Term Return Indicator: Historically, studies using the Shiller P/E (CAPE ratio) have shown a negative correlation between high starting P/E ratios for the S&P 500 and subsequent long-term (e.g., 10-year) market returns. A significantly higher-than-average P/E might suggest lower future returns, while a lower-than-average P/E could precede stronger returns. This makes the S&P 500 P/E an essential tool for strategic asset allocation.

Analyzing the S&P 500’s P/E Ratio

Interpreting the S&P 500’s P/E ratio requires context, particularly when comparing current figures to historical averages and considering the various factors that influence it.

Current vs. Historical P/E Averages

The S&P 500’s P/E ratio is not static; it fluctuates significantly over time due to shifts in earnings, market prices, and investor sentiment. To understand if the current P/E is “high” or “low,” it’s essential to compare it to its own historical averages.

- Long-Term Trends: Historically, the average trailing P/E for the S&P 500 has hovered around 15-16x over many decades. However, this average can be misleading due to significant deviations. For instance, during the dot-com bubble of the late 1990s, the P/E surged dramatically, reaching levels well above 30x. Conversely, during periods of economic distress, like the 2008 financial crisis, it often dipped significantly.

- Deviation from the Mean: A P/E ratio significantly above its long-term average might suggest an overvalued market, while one below the average could indicate an undervalued market. However, “average” doesn’t necessarily mean “fair value,” as structural changes in the economy, such as persistently lower interest rates or the rise of highly profitable tech giants, can justify a sustainably higher P/E.

Factors Influencing the S&P 500’s P/E

Several macroeconomic and market-specific factors consistently influence the aggregate P/E of the S&P 500:

- Interest Rates: Perhaps the most significant driver. Lower interest rates generally lead to higher P/E ratios because they reduce the discount rate used in valuation models, making future earnings more valuable today. They also make bonds less attractive, pushing investors towards equities. Conversely, rising rates tend to compress P/E multiples.

- Economic Growth: Strong, sustainable economic growth typically translates to higher corporate earnings and improved investor confidence, supporting higher P/E ratios.

- Corporate Earnings Growth: Direct impact. If aggregate earnings for S&P 500 companies are expected to grow rapidly, investors are willing to pay a higher multiple for those future earnings, thus increasing the P/E.

- Inflation: High inflation can be detrimental to P/E ratios. It erodes the purchasing power of future earnings and often prompts central banks to raise interest rates, which, as noted, puts downward pressure on valuations.

- Market Sentiment and Risk Appetite: Periods of optimism and low perceived risk (e.g., during market rallies) can inflate P/E ratios, as investors are more willing to take on risk. Conversely, periods of uncertainty, fear, or geopolitical instability can lead to P/E contraction.

- Sector Composition: The P/E of the S&P 500 is an aggregate. If high-growth sectors with inherently higher P/Es (like technology) constitute a larger portion of the index, the overall index P/E will naturally trend higher.

Different Measures: Trailing, Forward, and Shiller P/E for the Index

When discussing the S&P 500’s P/E, it’s crucial to specify which measure is being used:

- Trailing P/E for the S&P 500: Calculated using the sum of the last four quarters of reported earnings for all S&P 500 companies, weighted by their market capitalization. This is the most frequently cited P/E.

- Forward P/E for the S&P 500: Uses consensus analyst estimates for the next 12 months’ earnings for all S&P 500 companies. This provides a more current outlook but is subject to the accuracy of analyst forecasts.

- Shiller P/E (CAPE) for the S&P 500: Uses the S&P 500’s inflation-adjusted price divided by the average of the previous 10 years’ inflation-adjusted earnings. This long-term, cyclically adjusted metric is invaluable for understanding broader valuation cycles and identifying periods of significant over- or undervaluation that might precede long-term market reversals.

Interpreting the S&P 500 P/E for Investment Decisions

The S&P 500’s P/E ratio is a powerful analytical tool, but its utility in investment decision-making depends on a nuanced understanding of its implications and limitations. It’s not a standalone signal but rather a piece of a larger puzzle.

Is a High P/E Justified?

A common question arises when the S&P 500’s P/E is significantly above its historical average: Is it justified, or is the market overvalued? Several arguments can support a higher P/E in certain environments:

- Lower-for-Longer Interest Rates: A prolonged period of low interest rates (as seen in recent decades) can fundamentally justify higher P/E ratios. When the risk-free rate of return is low, investors are willing to pay more for future equity earnings, as their alternative investments (like bonds) offer less yield.

- Higher Quality, More Resilient Earnings: The S&P 500’s composition has evolved, with a greater emphasis on asset-light technology and service-oriented companies that often boast higher margins, stronger competitive moats, and more predictable earnings streams compared to traditional industrial companies of the past.

- Global Reach and Diversification: Many S&P 500 companies derive a substantial portion of their revenue and earnings from international markets, providing a degree of diversification and access to faster-growing economies, which can command a premium.

- Technological Innovation and Productivity Gains: Ongoing technological advancements can lead to sustained productivity growth and cost efficiencies, potentially supporting higher profit margins and, consequently, higher valuations.

However, even with these justifications, an extremely high P/E warrants caution, as it implies that a significant portion of future growth is already priced into the market, leaving less room for positive surprises.

Pitfalls and Limitations of Using P/E in Isolation

While informative, relying solely on the S&P 500’s P/E ratio can be misleading due to several limitations:

- Earnings Manipulation: Corporate earnings can sometimes be subject to accounting adjustments or one-time events that distort the true underlying profitability, especially when looking at trailing P/E.

- Ignoring Debt: The P/E ratio does not account for a company’s debt levels. A company with high debt and low earnings might appear to have a high P/E, but its enterprise value (which includes debt) might suggest a different picture.

- Sector Differences: Comparing the S&P 500’s P/E to a single company’s P/E, or even to a specific sector’s average, can be inappropriate. Different industries inherently have different average P/E ratios due to varying growth profiles, capital requirements, and business cycles.

- Does Not Reflect Growth: A high P/E doesn’t automatically mean overvalued if earnings are growing rapidly. This is where the PEG (Price/Earnings to Growth) ratio can be more insightful, though rarely applied to an entire index.

- Historical Context is Key: An “average” P/E today might be different from an “average” P/E fifty years ago due to structural changes in the economy, interest rate environments, and accounting standards.

P/E as Part of a Broader Valuation Toolkit

For a truly comprehensive market assessment, the S&P 500’s P/E ratio should always be considered alongside other financial metrics and qualitative factors:

- Price-to-Book (P/B) Ratio: Compares market value to book value, useful for asset-heavy industries.

- Dividend Yield: Indicates the dividend income relative to the stock price, crucial for income-focused investors.

- Enterprise Value to EBITDA (EV/EBITDA): Often preferred for comparing companies with different capital structures, as it includes debt and is unaffected by depreciation and amortization.

- Discounted Cash Flow (DCF) Analysis: A fundamental valuation method that estimates the intrinsic value of an asset based on its expected future cash flows.

- Interest Rate Spreads and Yield Curve: Provide insights into the macro environment and credit markets.

- Economic Indicators: GDP growth, inflation rates, employment figures, and consumer confidence all play a role in shaping the market’s fundamental value.

By integrating the S&P 500’s P/E with these other tools, investors can develop a more robust and informed perspective on market valuation and potential future performance.

The Future Outlook and P/E Dynamics

Predicting the exact future trajectory of the S&P 500’s P/E is challenging, as it’s influenced by a confluence of dynamic factors. However, understanding the key drivers can help investors anticipate potential shifts in market valuation.

What to Watch For

Several critical indicators will continue to shape the S&P 500’s P/E in the coming periods:

- Corporate Earnings Growth: This is the most direct and fundamental driver. Sustained, robust earnings growth across S&P 500 companies will support higher valuations. Any deceleration or contraction in earnings could put downward pressure on the P/E, especially if prices remain elevated.

- Federal Reserve Policy and Interest Rates: The Fed’s stance on monetary policy, particularly interest rate decisions, will remain paramount. A shift towards tighter monetary policy, with continued rate hikes, typically leads to P/E compression. Conversely, a dovish pivot or rate cuts could provide tailwinds for higher valuations.

- Inflation Trends: The persistence or abatement of inflation is a key determinant. High and persistent inflation can erode profit margins, increase input costs, and provoke central bank tightening, all of which are negative for P/E ratios.

- Economic Growth and Recession Risk: The broader economic environment, including GDP growth forecasts and the probability of a recession, will heavily influence investor sentiment and, consequently, how much they are willing to pay for each dollar of earnings. A robust economy supports higher P/Es, while recession fears tend to depress them.

- Geopolitical Stability: Global events, trade tensions, and geopolitical conflicts can introduce significant uncertainty, leading to increased risk aversion and a contraction in P/E multiples.

- Technological Innovation and Productivity: Ongoing advancements in areas like AI, automation, and biotechnology can drive future earnings potential and justify higher valuations for the companies leading these trends, which in turn can influence the aggregate index P/E.

Long-term Perspective on Market Valuation

From a long-term perspective, the S&P 500’s P/E ratio tends to revert to its mean. While periods of significant deviation can last for years, market forces eventually lead to a normalization. The Shiller P/E (CAPE ratio) is particularly useful for this long-term analysis, as it smooths out short-term earnings volatility. Historically, extremely high CAPE ratios have preceded periods of lower long-term returns, and unusually low CAPE ratios have been followed by stronger returns.

Investors should acknowledge that the “new normal” might mean a slightly higher average P/E compared to several decades ago due to structural shifts like lower interest rates, increased globalization, and the dominance of high-growth, asset-light tech companies. However, this does not negate the principle that extreme valuations eventually face headwinds. A balanced and disciplined approach, combining P/E analysis with other valuation metrics and a keen eye on macroeconomic developments, is crucial for navigating the evolving landscape of market valuation.

Conclusion

The P/E ratio of the S&P 500 is a multifaceted and indispensable metric for understanding the valuation of the broader U.S. stock market. It provides valuable insights into investor sentiment, expectations for future corporate earnings, and the prevailing economic climate. While a high P/E can be justified by factors such as low interest rates and robust growth prospects, it also signals that a significant amount of optimism is already priced into the market. Conversely, a low P/E might present opportunities for long-term investors, assuming the underlying earnings power remains strong.

However, the P/E ratio is not a crystal ball. Its true power lies in its application within a comprehensive analytical framework, comparing it against historical averages, considering various types (trailing, forward, Shiller P/E), and, most importantly, integrating it with a suite of other financial indicators and macroeconomic factors. By employing a disciplined and holistic approach, investors can leverage the S&P 500’s P/E to make more informed decisions, gauge market risk, and align their portfolios with their long-term financial objectives.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.