The persistent question of “when will rates drop” has become a central point of discussion for economists, policymakers, businesses, and households worldwide. After a period of aggressive monetary tightening aimed at taming runaway inflation, central banks across major economies, most notably the U.S. Federal Reserve, have held interest rates at multi-decade highs. This environment has profound implications for everything from mortgage payments and business investments to savings returns and the overall economic outlook. Understanding the factors influencing these decisions and the potential timing of a shift is crucial for financial planning and economic strategy.

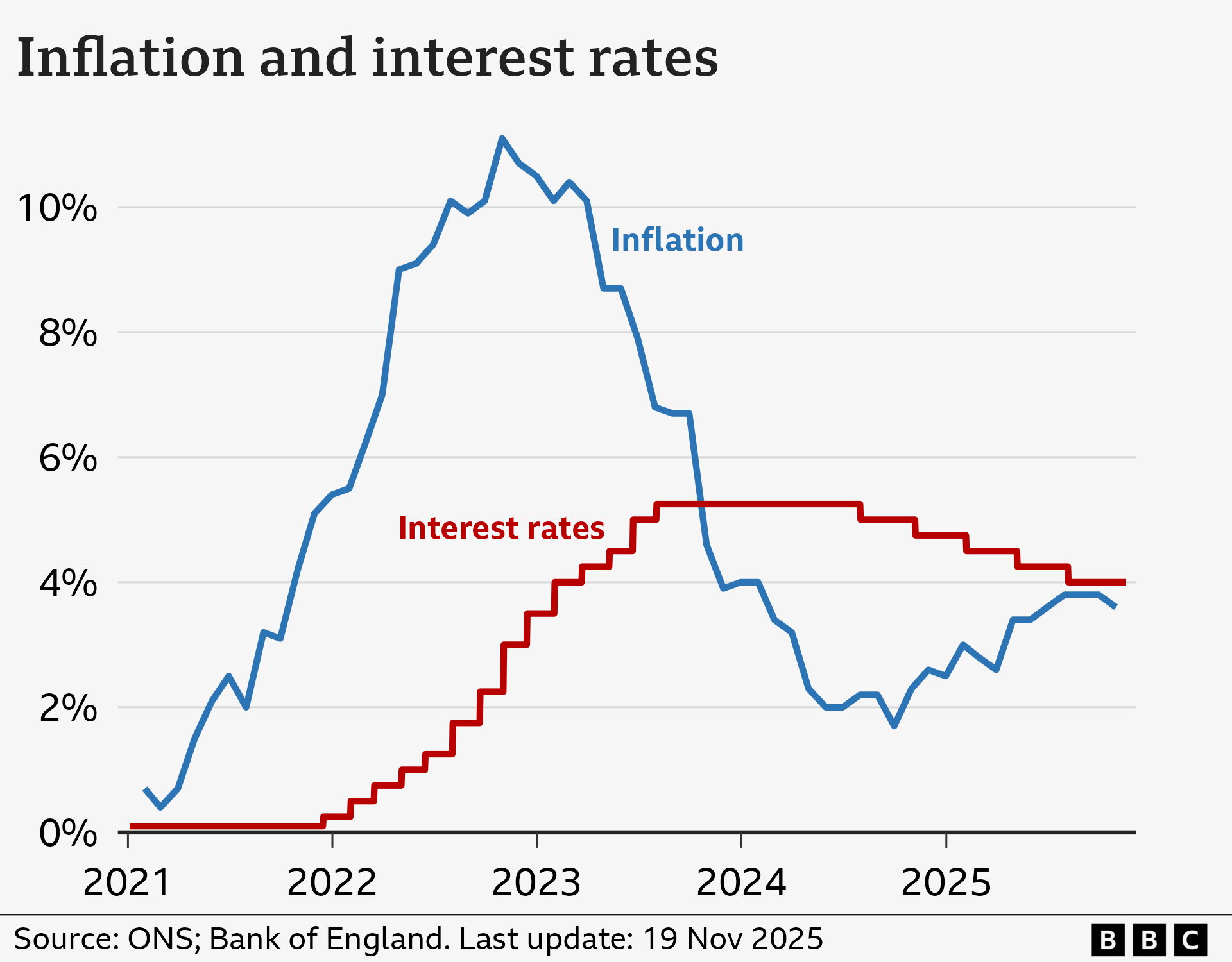

The journey to higher rates began in earnest as inflation, initially deemed “transitory,” proved to be more persistent and widespread, fueled by supply chain disruptions, robust consumer demand, and geopolitical tensions. Central banks, tasked with maintaining price stability, responded by rapidly increasing their benchmark rates, making borrowing more expensive to cool the economy and bring inflation back to target levels, typically around 2%. Now, as inflation shows signs of moderation, albeit unevenly, the focus has shifted from raising rates to holding them and, eventually, cutting them. The timing and magnitude of these potential cuts are subjects of intense debate and speculation, shaping market sentiment and economic expectations.

The Current Economic Landscape and Central Bank Stance

The global economy is navigating a complex terrain marked by resilient labor markets, easing but still elevated inflation, and varying degrees of growth. Central banks, particularly the U.S. Federal Reserve, the European Central Bank (ECB), and the Bank of England (BoE), are walking a tightrope, balancing the risk of cutting rates too soon and reigniting inflation against the danger of keeping them too high for too long and triggering a recession.

The Fight Against Inflation: Mission Accomplished?

The primary driver behind the rate hike cycle was inflation. After peaking in 2022, consumer price indices (CPI) and personal consumption expenditures (PCE) have shown a consistent downtrend in many regions. However, core inflation, which excludes volatile food and energy prices, has proven stickier, particularly in services sectors. Central bankers are keenly observing these trends, looking for convincing evidence that inflation is not just falling but is firmly on a sustainable path back to their 2% target. They emphasize the need for “data-dependent” decisions, signaling that future actions will be dictated by incoming economic reports rather than predetermined schedules. Until they are confident that the battle against inflation is decisively won, a cautious approach to rate cuts is likely to prevail.

Central Bank Mandates and Communication

Central banks operate under dual mandates in many countries, aiming for both price stability and maximum sustainable employment. While the focus has largely been on price stability during the inflationary surge, the health of the labor market remains a critical consideration. A robust job market, with low unemployment and steady wage growth, provides a buffer against economic downturns but can also contribute to inflationary pressures. Central bank communications are meticulously scrutinized by markets, as every word from officials can sway expectations. Their consistent messaging has been one of patience and vigilance, reiterating that a premature pivot could undo the progress made in stabilizing prices. This deliberate communication strategy aims to manage expectations and ensure financial conditions remain appropriate for achieving their policy goals.

Global Economic Headwinds and Tailwinds

Beyond domestic factors, global economic conditions play a significant role. Geopolitical tensions, particularly ongoing conflicts and trade disputes, can disrupt supply chains and commodity markets, exerting upward pressure on prices. The economic performance of major trading partners also influences domestic growth and inflation dynamics. Conversely, advancements in technology, particularly AI, and sustained productivity gains could act as disinflationary forces over the long term, potentially offering central banks more flexibility. The interplay of these global forces adds layers of complexity to central banks’ decision-making processes, requiring them to consider a broader array of risks and opportunities when contemplating rate adjustments.

Key Indicators Influencing Rate Decisions

Central banks rely on a suite of economic indicators to gauge the health of the economy and the trajectory of inflation. These data points serve as their compass, guiding their monetary policy decisions.

Inflationary Pressures: CPI and PCE

The Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) price index are paramount. CPI measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services, while PCE, preferred by the Fed, reflects the prices of goods and services purchased by consumers. Both core and headline figures are critical. Sustained declines in both, particularly core PCE, towards the 2% target are essential prerequisites for rate cuts. Central banks look beyond month-to-month volatility, seeking a clear trend that suggests inflation is durably subdued.

Labor Market Strength and Wage Growth

Employment figures, including the unemployment rate, non-farm payrolls, and average hourly earnings, offer insights into the health of the labor market. A strong labor market, while desirable, can fuel wage-price spirals if wage growth outpaces productivity gains. Central banks look for a rebalancing in the labor market, where job openings decline, quit rates normalize, and wage growth moderates to a level consistent with stable inflation without significant job losses. A sudden deterioration in the labor market could, however, prompt earlier rate cuts to avert a deeper recession.

GDP Growth and Consumer Spending

Gross Domestic Product (GDP) provides a broad measure of economic activity, indicating whether the economy is expanding, contracting, or stagnating. Robust GDP growth coupled with strong consumer spending suggests underlying economic strength but could also indicate potential inflationary pressures. Conversely, a significant slowdown or contraction in GDP would signal a weakening economy, making a case for monetary easing. Retail sales data and consumer confidence surveys also offer timely insights into consumer behavior, which is a major component of aggregate demand.

Geopolitical and Financial Stability Factors

Beyond traditional economic metrics, central banks also monitor geopolitical developments and financial stability risks. Major global events, such as conflicts, energy crises, or significant disruptions to global trade, can have profound effects on inflation and economic growth, potentially forcing central banks to adjust their timelines. Similarly, concerns about financial system stability, such as stresses in banking sectors or excessive leverage, could also influence monetary policy, potentially overriding other economic considerations in an emergency.

Impact of Rate Changes Across Financial Sectors

The anticipation and eventual reality of rate drops have far-reaching implications across virtually every financial sector, affecting individuals, businesses, and investors alike.

Mortgage Market Volatility and Housing

For homeowners and prospective buyers, interest rates are a primary concern. High rates have made mortgages significantly more expensive, cooling housing markets in many regions. A sustained drop in rates would likely lead to a resurgence in housing demand, potentially making homes more affordable for buyers through lower monthly payments, and incentivizing existing homeowners to refinance their mortgages. However, the exact impact will depend on the speed and magnitude of rate cuts, as well as the underlying supply-demand dynamics in local markets. Lower rates could also stimulate new construction, helping to alleviate supply shortages.

Consumer Loans and Credit Cards

Borrowers with variable-rate loans, such as certain types of credit cards, personal loans, and auto loans, would see their interest payments decrease with rate drops. This provides direct financial relief to households, freeing up disposable income. For those contemplating new borrowing, lower rates make taking on debt more attractive, potentially stimulating consumer spending on big-ticket items. Businesses also benefit from cheaper credit for expansion, inventory, and operational needs, which can spur economic activity and job creation.

Savings Accounts and Certificates of Deposit (CDs)

Savers have enjoyed elevated returns on high-yield savings accounts, money market accounts, and Certificates of Deposit (CDs) during the high-rate environment. When rates begin to fall, these returns will inevitably decrease. This means savers will need to adjust their expectations and potentially seek alternative investment vehicles to maintain their income levels. While the absolute return might diminish, a healthier overall economy fostered by lower rates could present other investment opportunities in equities or other asset classes.

Bond Market Dynamics and Equity Valuations

The bond market is directly inverse to interest rates: when rates fall, bond prices generally rise. This makes existing bonds, especially those issued at higher rates, more valuable. For equity markets, lower interest rates typically lead to higher valuations. This is because future corporate earnings are discounted at a lower rate, increasing their present value, and cheaper borrowing costs can boost corporate profitability. Companies with high debt loads or those that rely heavily on future growth projections (e.g., tech stocks) often benefit disproportionately from a lower-rate environment.

Forecasting the Future: Scenarios and Expert Predictions

Predicting the exact timing and trajectory of interest rate changes is notoriously difficult, even for seasoned economists and market participants. However, various scenarios and expert consensus provide valuable frameworks for understanding potential paths forward.

Consensus Expectations and Potential Timelines

As of late 2023 and early 2024, the general consensus among many economists and market analysts leaned towards rate cuts beginning in mid-2024, with central banks taking a gradual approach. The expectation was for several 25-basis point cuts throughout the year, potentially extending into the following year, bringing rates down from their peaks to a more “neutral” level. However, this consensus is fluid and highly sensitive to incoming data. Stronger-than-expected inflation or a surprisingly resilient economy could push back the timing of cuts, while a significant economic slowdown or financial stress could accelerate them.

Dovish vs. Hawkish Outlooks

Within the broader consensus, there are naturally dovish and hawkish perspectives. Dovish economists argue that inflation is sufficiently under control, and the risks of a recession due to overly tight monetary policy are paramount. They advocate for earlier and potentially more aggressive rate cuts to support economic growth and prevent unnecessary job losses. Conversely, hawkish voices emphasize the lingering risks of inflation resurging, citing sticky core inflation and robust labor markets. They caution against premature easing, advocating for rates to remain “higher for longer” to ensure inflation is fully vanquished, even if it means some economic pain. The actual path taken by central banks often represents a compromise between these viewpoints, reflecting the ongoing assessment of evolving economic data.

Risks to the Outlook

Several risks could alter the current projections. An unexpected resurgence in inflation, perhaps due to new supply shocks or aggressive fiscal spending, would force central banks to maintain or even raise rates again. Conversely, a sharper-than-expected economic downturn, evidenced by significant job losses or a severe contraction in GDP, would likely prompt more rapid and substantial rate cuts. Geopolitical events, such as an escalation of conflicts or major trade wars, also pose significant unquantifiable risks that could swing the pendulum in either direction, depending on their impact on global supply chains, commodity prices, and investor confidence. The path of rates is not a straight line but a dynamic response to a constantly shifting economic and geopolitical landscape.

Navigating the Shifting Rate Environment

For individuals and businesses, understanding and adapting to the evolving interest rate environment is crucial for financial well-being and strategic planning.

For Homeowners and Buyers

Prospective homebuyers should monitor mortgage rates closely. A decline in rates could significantly improve affordability. For existing homeowners, rate drops present opportunities for refinancing, potentially locking in lower monthly payments and reducing long-term interest costs. However, it’s also important to consider closing costs and the remaining term of the current mortgage before refinancing. Those on variable-rate mortgages will see direct relief as rates fall.

For Savers and Investors

Savers should be prepared for lower returns on cash deposits as rates decline. This might necessitate exploring alternative investment avenues, such as bond funds, dividend-paying stocks, or real estate investment trusts (REITs), to seek higher yields. Investors in equity markets might benefit from generally higher valuations in a lower-rate environment, but it’s important to maintain a diversified portfolio and align investments with long-term financial goals and risk tolerance. Actively managed portfolios or seeking advice from financial planners can help optimize strategies.

For Borrowers and Businesses

Individuals with consumer debt, particularly variable-rate credit cards or personal loans, should consider using the opportunity of falling rates to aggressively pay down high-interest debt, or explore consolidation options. Businesses can leverage lower borrowing costs to fund expansion projects, invest in research and development, or optimize their capital structure. This can lead to increased profitability and competitiveness. Strategic planning around debt management and capital allocation becomes even more critical in a changing rate environment.

Adaptability as a Key Strategy

Ultimately, the key to navigating the shifting rate environment is adaptability. Economic forecasts are inherently uncertain, and central bank policies can change in response to new data. Maintaining a flexible financial plan, regularly reviewing budgets, debt levels, and investment portfolios, and staying informed about economic trends will enable individuals and businesses to make timely and informed decisions, positioning themselves to both mitigate risks and capitalize on opportunities as interest rates eventually begin their descent. While the exact timing remains uncertain, preparing for “when rates drop” is a prudent financial strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.