For countless active-duty service members, veterans, and eligible surviving spouses, the dream of homeownership is not just aspirational but tangibly supported by one of the most powerful financial instruments available: the VA loan. Central to understanding the profound advantage of this benefit is grasping the intricacies of the VA mortgage rate. Far from being a static figure, it is a dynamic component influenced by a confluence of market forces, individual financial health, and the specific characteristics of the loan itself. This article delves deep into what VA mortgage rates are, how they are determined, and what you need to know to secure the most favorable terms for your home financing journey.

The Department of Veterans Affairs (VA) home loan program stands as a beacon of appreciation for those who have served our nation. Unlike conventional mortgages that often require significant down payments and can come with stringent credit score requirements, VA loans offer unparalleled benefits, with their typically competitive interest rates being a cornerstone. Understanding these rates is not merely about a number; it’s about unlocking a significant financial advantage that can translate into substantial savings over the lifespan of a mortgage.

Decoding the Mechanics of VA Mortgage Rates

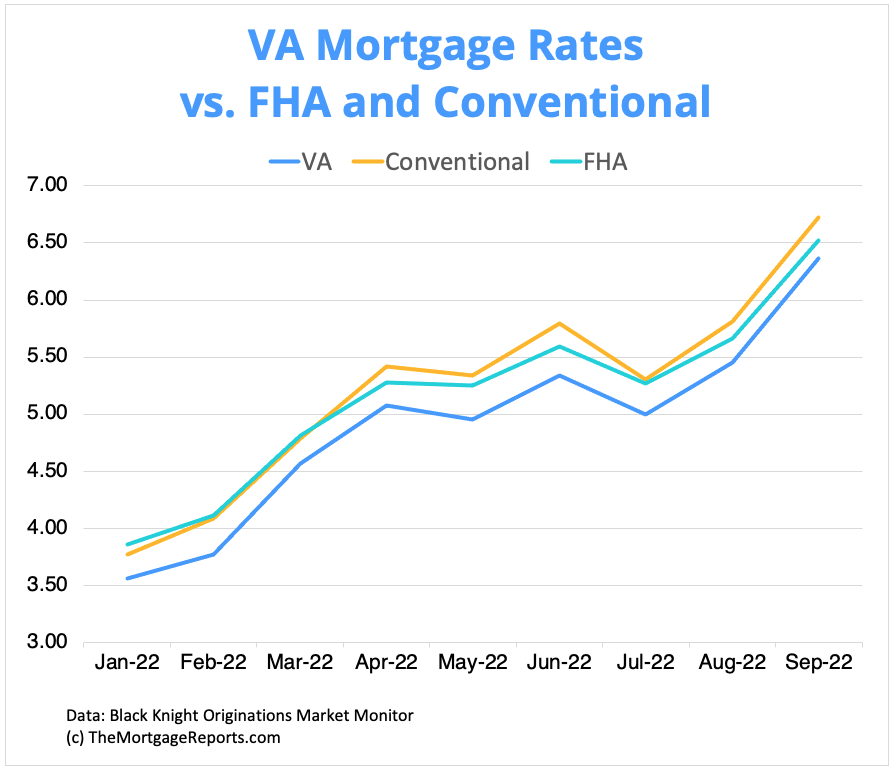

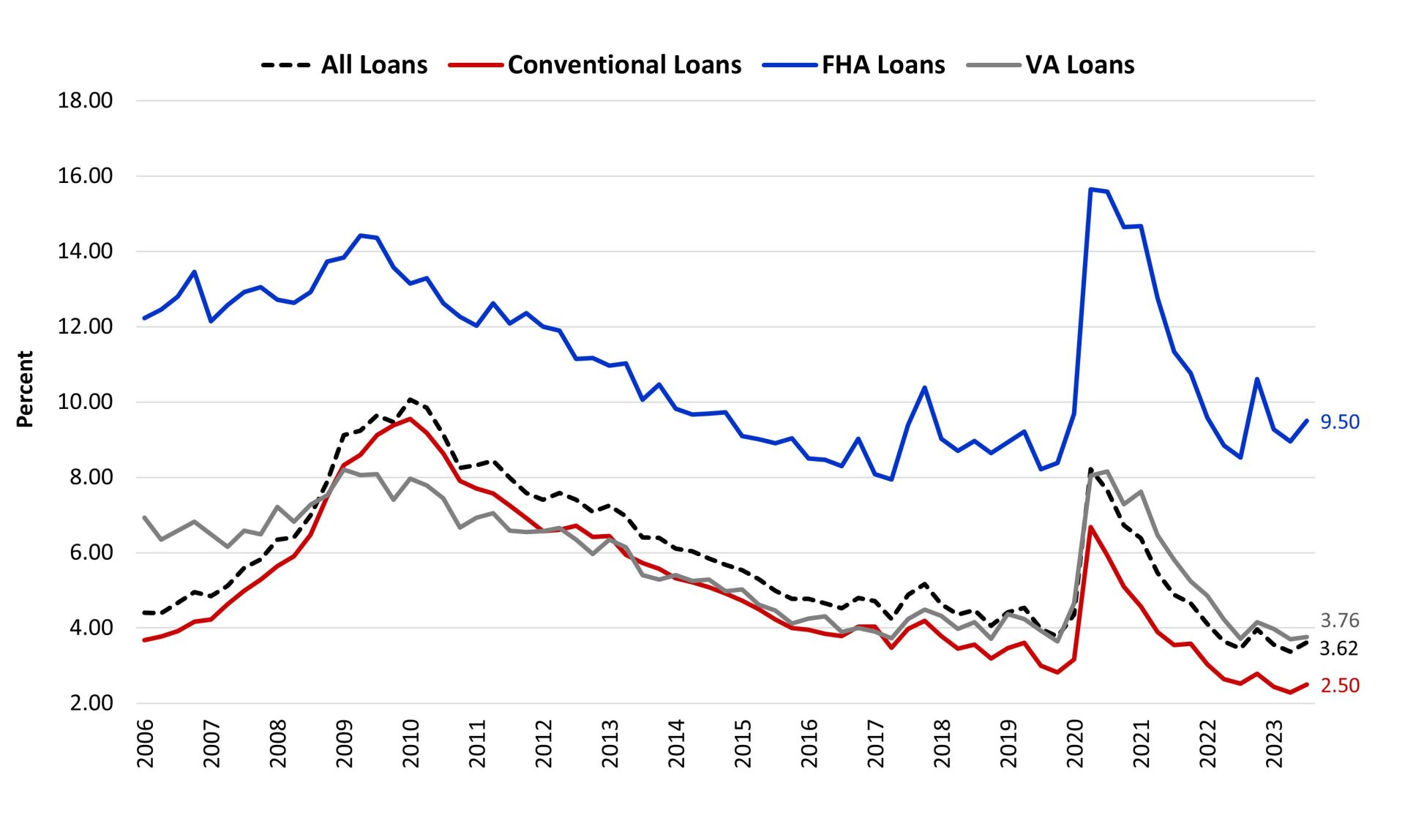

At its core, a VA mortgage rate is the interest charged by a lender for borrowing money to purchase or refinance a home under the VA loan program. It’s crucial to clarify that the VA itself does not set these interest rates. Instead, the VA guarantees a portion of the loan, which significantly reduces the risk for approved private lenders (banks, credit unions, mortgage companies). This government backing is precisely what allows lenders to offer such attractive terms, often resulting in lower rates than conventional or even FHA loans.

How VA Rates are Established

Several primary factors converge to establish the VA mortgage rates offered by lenders. These are not arbitrary figures but rather reflect a complex interplay of economic indicators and risk assessment:

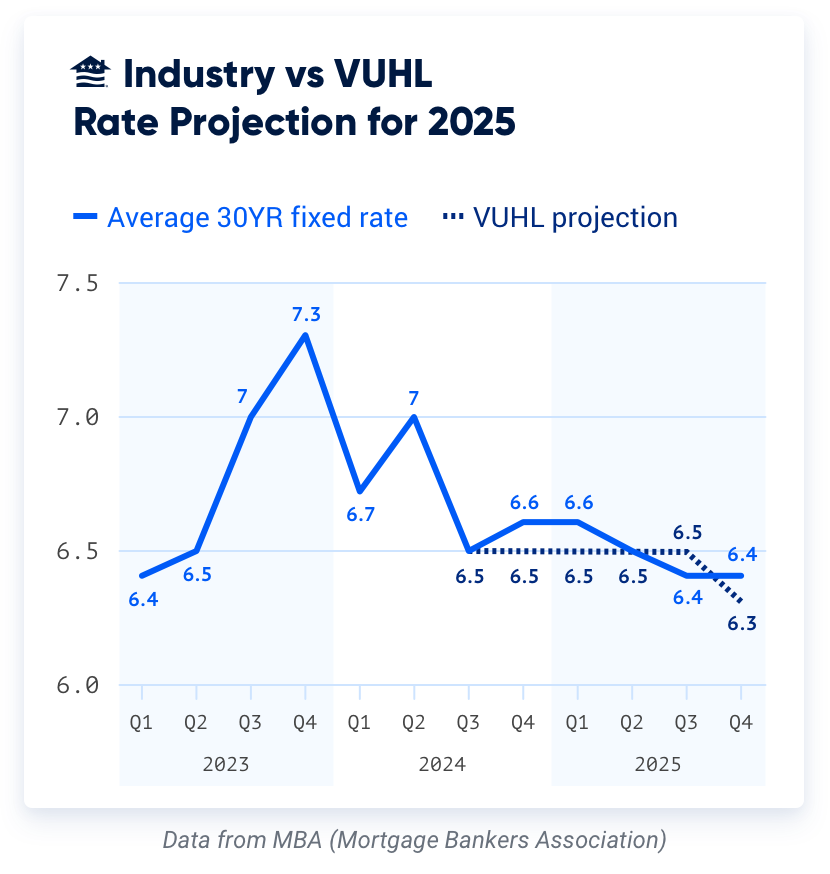

- Market Conditions: The broader economic landscape plays the most significant role. Global financial markets, inflation expectations, the Federal Reserve’s monetary policy, and the yield on U.S. Treasury bonds directly influence mortgage rates across the board, including VA rates. When the economy is strong and inflation is a concern, rates tend to rise. Conversely, during periods of economic uncertainty or lower inflation, rates may fall.

- Lender-Specific Pricing: While the VA guarantees the loan, each approved lender operates independently. They set their own profit margins, account for their overheads, and assess their individual risk tolerance, leading to variations in rates offered. This is why shopping around among multiple lenders is not just recommended but essential.

- Borrower’s Financial Profile: Although VA loans are known for their flexibility, a borrower’s financial health still impacts the rate they receive. A higher credit score signals lower risk to a lender, often resulting in a more favorable interest rate. Similarly, a lower debt-to-income (DTI) ratio demonstrates an applicant’s ability to manage monthly payments, further enhancing their appeal to lenders.

- Loan Characteristics: The type of loan (purchase, refinance), the loan term (15-year vs. 30-year fixed), and whether discount points are paid upfront can all influence the final rate. Shorter-term loans typically carry lower rates because the lender’s risk exposure is reduced over a shorter period.

Fixed-Rate vs. Adjustable-Rate VA Mortgages

VA loans are predominantly offered as fixed-rate mortgages, which means the interest rate remains constant for the entire duration of the loan. This provides stability and predictability in monthly payments, making budgeting straightforward. However, Adjustable-Rate Mortgages (ARMs) are also available, though less common. VA ARMs typically offer a lower initial interest rate for a set period (e.g., 3 or 5 years), after which the rate adjusts periodically based on market indices. While ARMs can offer lower initial payments, they introduce payment volatility, which may not suit every borrower’s financial comfort level. For long-term stability and peace of mind, fixed-rate VA loans are overwhelmingly preferred.

Critical Factors Influencing Your Individual VA Mortgage Rate

Beyond the general market trends, several specific elements directly within your control, or at least amenable to strategic planning, will dictate the precise VA mortgage rate you qualify for. Understanding and optimizing these factors can lead to significant long-term savings.

The Power of Your Credit Score

Your credit score is a numerical representation of your creditworthiness. While the VA itself does not set a minimum credit score requirement, most VA-approved lenders will have their own internal credit score thresholds. Generally, a FICO score of 620-640 is a common minimum, but higher scores (e.g., 700+) will consistently unlock access to the most competitive interest rates. A strong credit history demonstrates responsible financial behavior and a lower likelihood of default, making you a more attractive borrower to lenders.

- Improving Your Credit Score: Before applying for a VA loan, review your credit report for inaccuracies. Pay down high-interest debt, avoid opening new lines of credit, and ensure timely payments on all existing obligations to boost your score.

Debt-to-Income (DTI) Ratio and Residual Income

Lenders assess your ability to manage new mortgage payments by evaluating your Debt-to-Income (DTI) ratio. This ratio compares your total monthly debt payments (including the proposed mortgage) to your gross monthly income. While the VA has a general guideline of 41% for DTI, it also uses a unique metric called “residual income.” Residual income is the amount of disposable income left over each month after all major expenses (debts, taxes, insurance, utilities, etc.) are paid. The VA has specific residual income requirements based on family size and region. A lower DTI and sufficient residual income indicate a greater capacity to handle your mortgage payments, which can positively influence the rate offered.

Loan Term and Loan Type

The length of your mortgage term significantly impacts the interest rate. A 15-year fixed-rate VA loan typically comes with a lower interest rate compared to a 30-year fixed-rate VA loan. This is because lenders assume less risk over a shorter period. However, the trade-off is higher monthly payments for the 15-year term. For purchase loans, the goal is often the lowest possible rate, while for refinancing, the specific refinance program (e.g., VA Streamline Refinance or Interest Rate Reduction Refinance Loan – IRRRL, or a VA Cash-Out Refinance) can also influence rates and associated fees.

Discount Points and Lender Fees

When you receive a loan offer, you might be presented with the option to pay “discount points.” One discount point typically equals 1% of the loan amount. Paying points upfront allows you to “buy down” your interest rate, reducing it for the life of the loan. While this means a higher upfront cost, it can lead to substantial savings over many years. Conversely, some lenders may offer a slightly higher interest rate in exchange for covering some of your closing costs. Understanding this trade-off is key to determining the best financial strategy for your individual circumstances. Be sure to compare the Annual Percentage Rate (APR), which includes the interest rate plus certain closing costs and fees, for a more accurate comparison between loan offers.

The Unique Aspect: The VA Funding Fee

One distinctive feature of VA loans that can indirectly impact the overall cost, though not the interest rate itself, is the VA Funding Fee. This is a one-time fee paid by the veteran to the VA, which helps to defray the costs of the program and keep it running for future generations of service members.

Understanding the Funding Fee’s Purpose and Structure

The VA Funding Fee eliminates the need for private mortgage insurance (PMI), a common requirement for conventional loans with less than a 20% down payment. While it’s a separate charge from the interest rate, it’s an important cost to factor into your total loan calculations. The amount of the funding fee varies depending on several factors:

- Type of Loan: Whether it’s a purchase loan or a refinance (IRRRL vs. Cash-Out).

- Down Payment Amount: Higher down payments generally result in lower funding fee percentages.

- Prior Use of VA Loan Benefit: First-time users often pay a lower fee than subsequent users.

- Service Status: Active duty, Reserves, National Guard, or veteran status.

For example, a first-time VA loan user with no down payment might pay a funding fee of 2.15% of the loan amount for a purchase. For a subsequent user with no down payment, this could rise to 3.3%. These fees can often be financed into the loan, meaning they are added to your loan balance rather than paid out-of-pocket, increasing your total loan amount and, consequently, the amount of interest you will pay over time.

Exemptions from the VA Funding Fee

Crucially, some veterans are exempt from paying the VA Funding Fee. These include:

- Veterans receiving VA compensation for a service-connected disability.

- Veterans who would be entitled to receive VA compensation for a service-connected disability if they did not receive retirement or active duty pay.

- Surviving spouses of veterans who died in service or from a service-connected disability.

If you believe you may be exempt, it is vital to confirm your status with the VA or your lender, as this exemption can lead to significant savings.

Strategic Steps to Secure the Best VA Mortgage Rate

Securing the best possible VA mortgage rate is not a matter of luck but rather a result of informed decision-making and proactive effort. By following a strategic approach, you can significantly enhance your chances of locking in a favorable rate.

The Imperative of Shopping Around

The single most impactful action you can take is to compare offers from multiple VA-approved lenders. As established earlier, lenders set their own rates and fees, leading to variations even for the same borrower. Obtaining at least three to five loan estimates allows you to directly compare:

- Interest Rates: The nominal rate offered.

- APR (Annual Percentage Rate): A broader measure of the cost of the loan, including the interest rate and most closing costs and fees.

- Closing Costs: All associated fees, including origination fees, appraisal, title, and recording fees.

- Discount Points: The cost to “buy down” the rate.

Don’t just look at the lowest interest rate; consider the overall cost of the loan as reflected in the APR and total closing costs.

Understanding the Loan Estimate

Once you apply for a mortgage, lenders are required by law to provide you with a standardized document called a Loan Estimate within three business days. This document details the estimated interest rate, monthly payment, closing costs, and other key loan terms. It is designed for easy comparison across different lenders. Pay close attention to:

- Page 1: Loan terms, projected payments, and estimated closing costs.

- Page 2: Itemized closing costs, broken down by lender fees and third-party fees.

- Page 3: Key comparisons, including the APR and total interest percentage (TIP).

Using these estimates as a direct comparison tool empowers you to negotiate or select the most advantageous offer.

Leveraging Your Entitlement

Each eligible veteran has a VA loan entitlement, which is the amount the VA will guarantee on their loan. For most eligible veterans, there is no maximum loan amount the VA will guarantee, provided the veteran has full entitlement. However, for those with partial entitlement or prior VA loan use, specific limits may apply. Understanding your entitlement amount helps you and your lender determine how much you can borrow with the VA guarantee, impacting your loan options and potentially indirectly influencing the rate if a larger loan requires a more robust financial profile.

Timing Your Rate Lock

Once you have chosen a lender and are moving forward with your application, you will typically have the option to “lock in” your interest rate. A rate lock guarantees that your interest rate will not change between the time you lock it and the time your loan closes. The duration of the lock can vary (e.g., 30, 45, or 60 days). It’s crucial to time your rate lock carefully, especially in volatile markets. Locking too early might mean missing out if rates drop further, while waiting too long risks rates increasing before you can secure your loan. Your loan officer can provide guidance on the current market sentiment and help you decide the best time to lock.

Conclusion

The VA mortgage rate is a dynamic and multifaceted aspect of the VA home loan benefit, offering unparalleled opportunities for service members, veterans, and their families to achieve homeownership. While the VA sets the framework for these loans, individual lenders determine the specific rates, driven by market forces, the borrower’s financial health, and the unique characteristics of each loan.

By understanding how VA rates are established, optimizing personal financial factors like credit scores and DTI, accounting for the VA Funding Fee, and diligently shopping around among multiple lenders, you can strategically position yourself to secure the most competitive rate available. The VA loan program is a powerful testament to our nation’s commitment to its heroes; mastering the nuances of its mortgage rates is a critical step in harnessing this benefit to its fullest potential and realizing the dream of affordable homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.