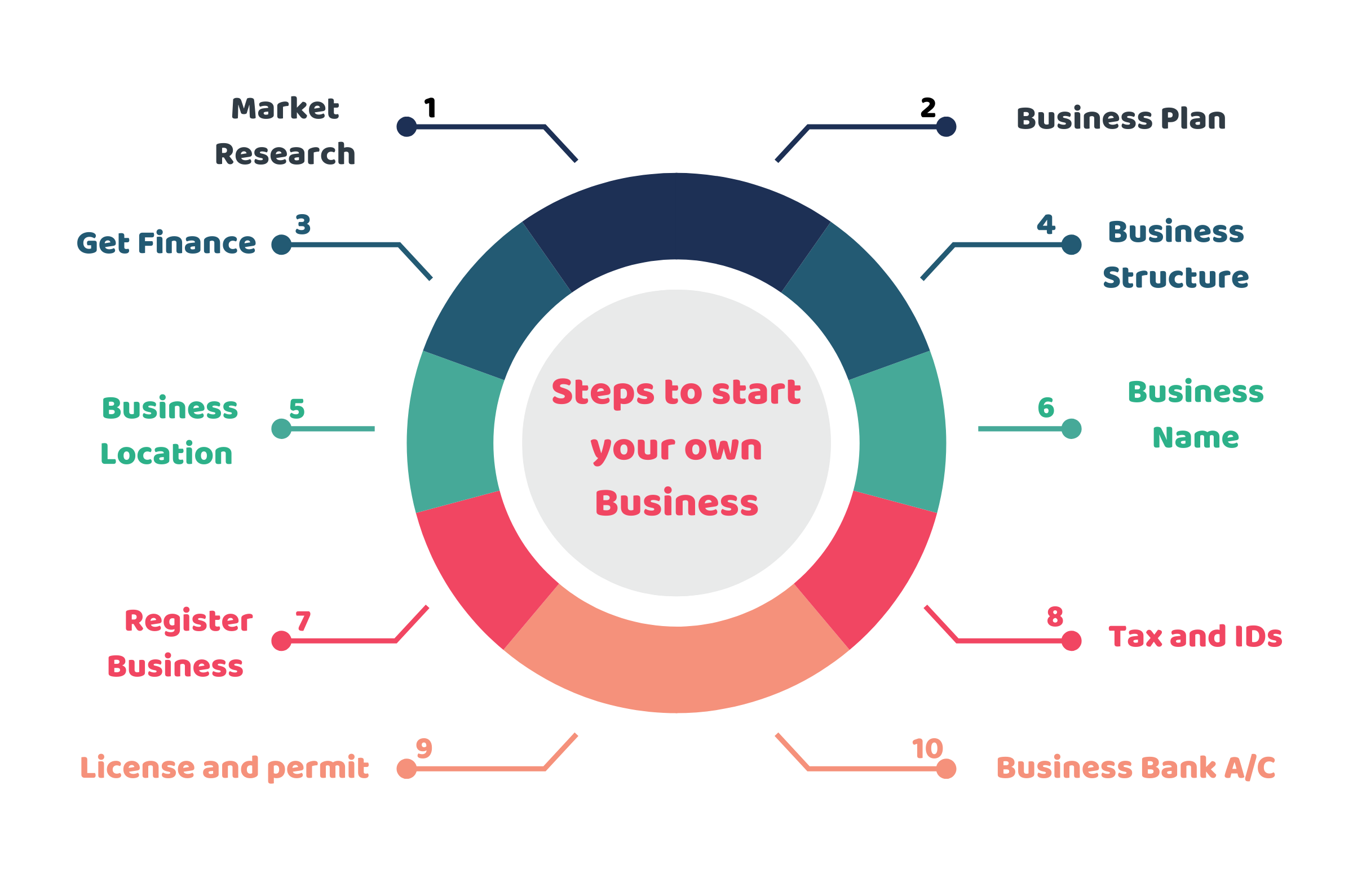

Embarking on the entrepreneurial journey is a profound decision, driven by vision, passion, and the desire for independence. While the allure of creating something new is powerful, the practical foundation of any successful business lies firmly in its financial health. For aspiring entrepreneurs, understanding the monetary mechanics—from initial funding to sustained profitability—is not just important; it’s paramount. This guide delves into the essential financial considerations and steps for launching your own business, ensuring a solid economic footing for your venture.

1. Laying the Financial Foundation: Personal Readiness and Preparation

Before you even draft a business plan, the most critical step is to assess your personal financial situation. Starting a business often entails a period of reduced or unstable personal income, making robust personal financial planning a non-negotiable prerequisite.

Assessing Your Personal Financial Stability

Take a candid look at your current income, expenses, assets, and liabilities. Do you have outstanding high-interest debt that could cripple your ability to invest in your business or weather lean months? Are your personal expenses under control? A clear understanding of your personal financial runway is crucial. Entrepreneurs often underestimate the time it takes for a new business to generate consistent income, and personal financial stress can quickly derail even the most promising ventures. Consolidate debts where possible, negotiate better rates, and critically evaluate every recurring expense. This phase is about creating maximum financial flexibility for yourself.

Budgeting for the Transition: From Employee to Entrepreneur

If you’re transitioning from a steady job, you’re likely giving up a predictable paycheck. Create a detailed personal budget that accounts for a potential dip in income during the initial startup phase. Determine your absolute minimum living expenses. How long can you sustain yourself without a significant income from your business? This “financial runway” will dictate how much pressure you’re under and how long you have to make your business profitable. Consider cutting discretionary spending, reducing unnecessary subscriptions, and finding ways to lower fixed costs like rent or transportation. Every dollar saved personally is a dollar you don’t have to borrow or earn immediately.

Building an Emergency Fund for Your Business and Yourself

Just as a personal emergency fund protects you from unexpected life events, a business emergency fund is vital for weathering early-stage challenges. Beyond your personal savings, aim to build a separate financial buffer specifically for your business. This fund can cover unexpected startup costs, a slow initial sales period, or critical equipment repairs. Experts often recommend having at least 3-6 months of operating expenses saved up. This financial cushion provides peace of mind and allows you to make strategic decisions rather than desperate ones when unforeseen circumstances arise. Without this buffer, a minor setback can quickly escalate into a catastrophic financial crisis for your nascent enterprise.

2. Funding Your Venture: Smart Capital Acquisition

Once your personal finances are in order, the next significant financial hurdle is securing capital for your business. The funding landscape is diverse, offering various avenues, each with its own advantages and financial implications. Choosing the right funding strategy is crucial for your business’s long-term financial health.

Bootstrapping: Maximizing Personal Resources and Minimizing Debt

Bootstrapping means funding your business primarily through personal savings, early sales, and minimal external capital. This approach is often the most financially prudent, as it avoids interest payments and equity dilution. It forces you to be lean, resourceful, and focused on generating revenue from day one. Many successful businesses began this way, leveraging existing skills, pre-sales, or low-cost online platforms. While slower, bootstrapping fosters financial discipline and ensures you retain full ownership and control. It also proves your business model’s viability before seeking external investment, making you a more attractive prospect if external funding becomes necessary later.

Exploring Debt Financing: Loans, Lines of Credit, and Micro-lenders

If bootstrapping isn’t sufficient, debt financing offers a way to inject capital without surrendering equity.

- Small Business Loans: Banks and credit unions offer various loan products, often requiring a solid business plan, collateral, and a good personal credit score. The interest rates can be favorable, but approval can be challenging for new businesses without a track record.

- Lines of Credit: More flexible than traditional loans, a business line of credit allows you to borrow up to a certain limit, repay it, and borrow again, similar to a credit card. It’s ideal for managing fluctuating cash flow but comes with variable interest rates.

- SBA Loans (Small Business Administration): Government-backed loans often have more flexible terms and lower down payments, making them accessible to a broader range of small businesses.

- Micro-lenders: Non-profit organizations specializing in small loans to startups and underserved communities, often with less stringent requirements than traditional banks.

Each option carries interest costs and repayment obligations, which must be meticulously factored into your financial projections. Defaulting on debt can severely damage your personal and business credit, making future financing difficult.

Understanding Equity Financing: Angel Investors and Venture Capital (Financial Dilution)

For businesses with high growth potential, equity financing involves selling a percentage of ownership (equity) in your company to investors in exchange for capital.

- Angel Investors: High-net-worth individuals who invest their own money, often providing mentorship alongside capital.

- Venture Capital (VC) Firms: Professional investors who manage funds from various sources and invest in companies with significant growth potential, typically in later stages or for larger capital needs.

While equity financing provides substantial capital without repayment obligations, it comes at the cost of ownership dilution. You give up a piece of your company, and investors will expect a return on their investment, potentially influencing strategic decisions. The financial implication is a shared future profit and a potentially lower personal payout if the company is sold or goes public. Carefully assess the long-term financial impact of giving away equity.

Grants and Alternative Funding Sources

Don’t overlook grants, which are essentially free money that doesn’t need to be repaid. These are often offered by government agencies, non-profits, or corporations for businesses aligned with specific missions (e.g., environmental, technological innovation, minority-owned businesses). Competition is fierce, and the application process can be lengthy.

Crowdfunding platforms (e.g., Kickstarter, Indiegogo) also offer a way to raise capital directly from the public, often in exchange for pre-orders or unique perks rather than equity or debt. This can also serve as market validation for your product or service.

3. Mastering Business Finance: Operational & Strategic Insights

With funding secured, the focus shifts to day-to-day financial management and strategic financial planning. This is where your business’s financial health is cultivated and sustained.

Developing a Robust Financial Plan and Projections

A financial plan is the backbone of your business strategy. It details your startup costs, operating expenses, revenue forecasts, and projected profitability.

- Startup Costs: List every initial expense—legal fees, equipment, permits, website development, initial inventory.

- Operating Expenses: Project recurring monthly costs—rent, utilities, salaries, marketing, supplies.

- Revenue Projections: Forecast your sales based on market research, pricing, and sales volume estimates. Be realistic, and then be conservative.

- Cash Flow Statement: Project money coming in and going out, ensuring you don’t run out of cash, even if you’re profitable on paper.

- Profit and Loss (P&L) Statement: Forecast your revenues, costs of goods sold (COGS), and operating expenses to determine your net profit.

- Balance Sheet: Project your assets, liabilities, and owner’s equity at specific points in time.

These projections are living documents, requiring regular review and adjustment. They help you set financial goals, track performance, and make informed decisions.

Pricing Your Products/Services for Profitability

Pricing is a delicate balance between perceived value, market rates, and your cost structure.

- Cost-Plus Pricing: Calculate all costs associated with producing your product or service, then add a desired profit margin. This ensures you cover costs but may not reflect market value.

- Value-Based Pricing: Price based on the perceived value to the customer, rather than just your costs. This requires deep understanding of your target market.

- Competitive Pricing: Benchmark against competitors’ prices, adjusting for your unique value proposition.

- Penetration Pricing: Set lower prices initially to attract customers and gain market share, then gradually raise them.

Never price below your break-even point consistently. Understand your variable costs (those that change with production volume) and fixed costs (those that remain constant) to ensure every sale contributes to your bottom line. Underpricing is a common mistake that can cripple a business financially.

Cash Flow Management: The Lifeblood of Your Business

Profitability doesn’t always equal cash in hand. A business can be profitable on paper but still run out of cash if receivables are slow or large expenses hit unexpectedly. Effective cash flow management involves:

- Monitoring Inflows and Outflows: Keep a close eye on when money comes in and when it goes out.

- Managing Accounts Receivable: Implement clear invoicing terms and follow up promptly on overdue payments.

- Managing Accounts Payable: Strategically pay your bills to maximize cash on hand without incurring late fees.

- Maintaining a Cash Reserve: As mentioned, an emergency fund is critical.

Poor cash flow is a leading cause of small business failure. Regular cash flow forecasting is essential to anticipate shortages and plan accordingly.

Essential Financial Tools and Accounting Practices

Even for solopreneurs, robust financial record-keeping is non-negotiable.

- Accounting Software: Tools like QuickBooks, Xero, or FreshBooks simplify invoicing, expense tracking, payroll, and financial reporting. They automate many tasks, reduce errors, and provide real-time insights into your financial health.

- Separate Business Bank Accounts: Keep personal and business finances strictly separate from day one. This simplifies accounting, tax preparation, and demonstrates professionalism.

- Regular Reconciliation: Regularly compare your bank statements with your accounting records to ensure accuracy.

- Professional Help: Consider hiring a bookkeeper or accountant, especially as your business grows. Their expertise can save you time, ensure compliance, and identify financial efficiencies. The cost is often a wise investment.

4. Navigating Legal & Tax Landscapes for Financial Efficiency

The legal and tax structures you choose have significant financial implications for your business, impacting liability, reporting requirements, and ultimately, your net income.

Choosing the Right Business Structure: Tax Implications and Liability

Your business structure dictates how your business is taxed and your personal liability for business debts.

- Sole Proprietorship: Simple to set up, but no legal distinction between you and your business. All business income/losses are reported on your personal tax return. High personal liability.

- Partnership: Similar to sole proprietorships but with two or more owners. Shared profits, losses, and liabilities.

- Limited Liability Company (LLC): Offers personal liability protection (separates personal and business assets) while providing flexible taxation options (can be taxed as a sole proprietorship, partnership, or corporation). A popular choice for small businesses.

- Corporation (S-Corp, C-Corp): Provides the strongest liability protection. C-corps are subject to “double taxation” (corporate profits taxed, then dividends to shareholders taxed). S-corps avoid double taxation by passing profits and losses directly to owners’ personal income.

Consult with a financial advisor or attorney to choose the structure that best balances liability protection and tax efficiency for your specific business goals.

Understanding Business Taxes and Deductions

Taxes are an unavoidable financial reality. You’ll likely be responsible for:

- Income Tax: Based on your business’s profits.

- Self-Employment Tax: Covers Social Security and Medicare for self-employed individuals.

- Sales Tax: If you sell goods or certain services, you may need to collect and remit sales tax.

- Payroll Tax: If you have employees.

- Estimated Taxes: As a business owner, you’ll typically pay estimated taxes quarterly, as taxes are not automatically withheld from your income. Failure to do so can result in penalties.

Crucially, understand what business expenses are tax-deductible. These can significantly reduce your taxable income. Examples include office supplies, travel, marketing, professional development, and home office expenses. Diligent record-keeping of all expenses is vital for maximizing deductions and minimizing your tax burden.

Compliance and Record-Keeping for Financial Integrity

Beyond taxes, various financial regulations and reporting requirements exist, depending on your industry and business structure. Maintaining accurate and organized financial records is not just good practice; it’s a legal necessity. This includes:

- Receipts for all expenses.

- Invoices for all sales.

- Bank statements and credit card statements.

- Payroll records.

- Contracts and agreements.

Good record-keeping ensures you can justify deductions, comply with audits, and accurately track your business’s financial performance. It’s the foundation of financial integrity.

5. Sustainable Growth and Financial Scaling

Launching your business is just the beginning. True entrepreneurial success lies in sustainable financial growth, ensuring your venture can not only survive but thrive and expand.

Reinvesting Profits Strategically

As your business begins to generate profits, the decision of what to do with that money becomes crucial. While it’s tempting to draw it out for personal use, strategic reinvestment is key to growth. Consider using profits for:

- Expanding operations: Hiring new staff, purchasing additional equipment.

- Marketing and sales initiatives: Increasing your reach and customer acquisition.

- Research and development: Innovating new products or services.

- Improving infrastructure: Upgrading technology or office space.

- Building a larger cash reserve: Strengthening your financial stability.

Each reinvestment should be evaluated for its potential return on investment (ROI) and alignment with your long-term financial goals. Avoid impulsive spending; every dollar reinvested should have a clear purpose to drive future profitability.

Monitoring Key Financial Performance Indicators (KPIs)

To manage growth effectively, you need to track your financial pulse. Key Performance Indicators (KPIs) are measurable values that demonstrate how effectively your business is achieving its financial objectives. Important financial KPIs include:

- Gross Profit Margin: Revenue minus Cost of Goods Sold, divided by Revenue. Indicates profitability of core products/services.

- Net Profit Margin: Net Income divided by Revenue. Shows overall profitability after all expenses.

- Operating Cash Flow: Cash generated from normal business operations.

- Customer Acquisition Cost (CAC): The cost of gaining a new customer.

- Customer Lifetime Value (CLTV): The total revenue a customer is expected to generate over their relationship with your business.

- Burn Rate: The rate at which your business is spending its cash reserves (especially relevant for startups not yet profitable).

Regularly reviewing these KPIs allows you to identify trends, spot potential problems early, and make data-driven financial decisions to optimize performance.

Planning for Future Financial Milestones and Exit Strategies

Sustainable growth isn’t just about day-to-day management; it’s about envisioning the future. Set financial milestones for your business—e.g., reaching a certain revenue target, achieving consistent profitability, or expanding into new markets. These provide clear financial objectives to work towards.

Equally important, even from the early stages, is considering an “exit strategy.” This doesn’t mean you plan to sell immediately, but understanding potential financial outcomes for your business provides a long-term perspective. Options could include:

- Selling the business: Preparing your financials for a profitable sale.

- Passing it on to family: Planning for financial succession.

- Going public: A complex financial endeavor for large, high-growth companies.

- Closing down: Understanding the financial implications of winding down operations.

A well-thought-out exit strategy ensures that your years of hard work translate into a significant financial return for you and your stakeholders, providing a defined end goal to your entrepreneurial financial journey.

Starting your own business is an exciting endeavor that demands meticulous financial planning and disciplined management. By prioritizing personal financial stability, strategically acquiring and managing capital, mastering operational finance, navigating the complexities of taxes and regulations, and planning for sustainable growth, you lay an unshakeable financial groundwork for your entrepreneurial success. Remember, money is the fuel that keeps your business engine running; understanding and managing it expertly is the key to reaching your destination.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.