The concept of federal tax often looms large in the minds of individuals and businesses alike, representing a significant portion of financial planning and economic activity. At its core, federal tax refers to the mandatory financial contributions levied by a nation’s central government on its citizens, corporations, and other entities to fund public expenditures. In the United States, understanding “what’s the federal tax” involves navigating a complex landscape of different tax types, filing requirements, and economic implications. This article delves into the intricacies of U.S. federal taxation, offering a professional, insightful, and engaging overview for anyone seeking to demystify this critical aspect of personal and business finance.

Understanding the Foundation of Federal Taxation

Federal taxation is not merely a mechanism for revenue generation; it’s a cornerstone of governmental function, societal welfare, and economic policy. Grasping its foundational elements is crucial for a complete understanding.

The Core Purpose of Federal Taxes

The primary purpose of federal taxes is to finance the vast array of public services and governmental operations that underpin a modern society. These include national defense, infrastructure development (roads, bridges, airports), social safety nets (Social Security, Medicare), public education funding, scientific research, and the administration of justice. Without a robust federal tax system, the government would be unable to provide these essential services, directly impacting the quality of life, economic stability, and security of the nation. Beyond revenue, taxes can also serve as tools for economic policy, used to encourage or discourage certain behaviors, redistribute wealth, and stabilize the economy during booms or recessions. For instance, tax credits for renewable energy installations aim to promote environmental sustainability, while excise taxes on tobacco seek to curb public health issues.

Key Federal Taxing Bodies

In the United States, the primary federal body responsible for administering and enforcing tax laws is the Internal Revenue Service (IRS). Established in 1862, the IRS operates under the U.S. Department of the Treasury and is tasked with collecting taxes, issuing regulations, and providing taxpayer services. It plays a pivotal role in ensuring compliance with the tax code. However, the legislative power to create and amend tax laws rests with the U.S. Congress. The House of Representatives, specifically its Ways and Means Committee, and the Senate, through its Finance Committee, debate and pass tax legislation. Once passed by both chambers and signed into law by the President, these new laws are then implemented and enforced by the IRS. Other federal agencies, such as the Social Security Administration, also play roles in the collection and distribution of certain payroll taxes.

A Brief History of U.S. Federal Taxation

The history of federal taxation in the U.S. is one of evolution, reflecting changing economic conditions, societal needs, and political ideologies. Early American history saw federal revenue primarily derived from tariffs on imports and excise taxes on specific goods like whiskey. The Civil War era introduced the nation’s first income tax, though it was temporary. The modern era of federal income tax truly began with the ratification of the 16th Amendment in 1913, which granted Congress the power to “lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.” This amendment fundamentally reshaped federal finance, allowing the government to directly tap into individual and corporate earnings. Over time, other major federal taxes, such as Social Security and Medicare taxes (introduced in the 1930s and 1960s, respectively), estate taxes, and a wider range of excise taxes, have been implemented, gradually building the comprehensive system we know today. Each major historical event, from world wars to economic depressions and booms, has often led to significant shifts in tax policy and structure.

Navigating the Major Types of Federal Taxes

The federal tax system is not monolithic; it comprises several distinct categories, each with its own rules, rates, and implications. Understanding these categories is essential for effective financial management.

Federal Income Tax: Individual and Corporate

The federal income tax is arguably the most prominent and impactful component of the U.S. tax system, levied on the earnings of both individuals and corporations.

Progressive Tax System and Brackets

The U.S. federal income tax system for individuals is progressive, meaning that higher earners pay a larger percentage of their income in taxes. This is achieved through a system of tax brackets, which are ranges of income taxed at specific rates. For example, the first portion of an individual’s taxable income might be taxed at 10%, the next portion at 12%, and so on, up to the highest marginal rate. It’s crucial to understand that only the income within a particular bracket is taxed at that bracket’s rate, not the entire income. This graduated approach aims to distribute the tax burden more equitably across different income levels. Corporations also pay federal income tax on their profits, but their structure typically involves a single flat rate or a simpler tiered system, which has been subject to significant reforms over the years (e.g., the Tax Cuts and Jobs Act of 2017).

Deductions, Credits, and Exemptions

Beyond gross income, several mechanisms reduce an individual’s or corporation’s taxable income or the actual tax owed. Deductions reduce taxable income. Common individual deductions include the standard deduction (a fixed amount based on filing status) or itemized deductions (such as mortgage interest, state and local taxes, or medical expenses). For businesses, deductions include operating expenses like salaries, rent, and supplies. Tax credits, on the other hand, directly reduce the amount of tax owed, dollar for dollar. Credits are generally more valuable than deductions because they subtract from the tax liability itself, not just the income. Examples include the Child Tax Credit, education credits, and energy credits. Exemptions (which were largely replaced by a higher standard deduction for individuals under the TCJA) historically allowed taxpayers to subtract a specific amount for themselves and their dependents. Understanding and leveraging these provisions is key to minimizing tax liability.

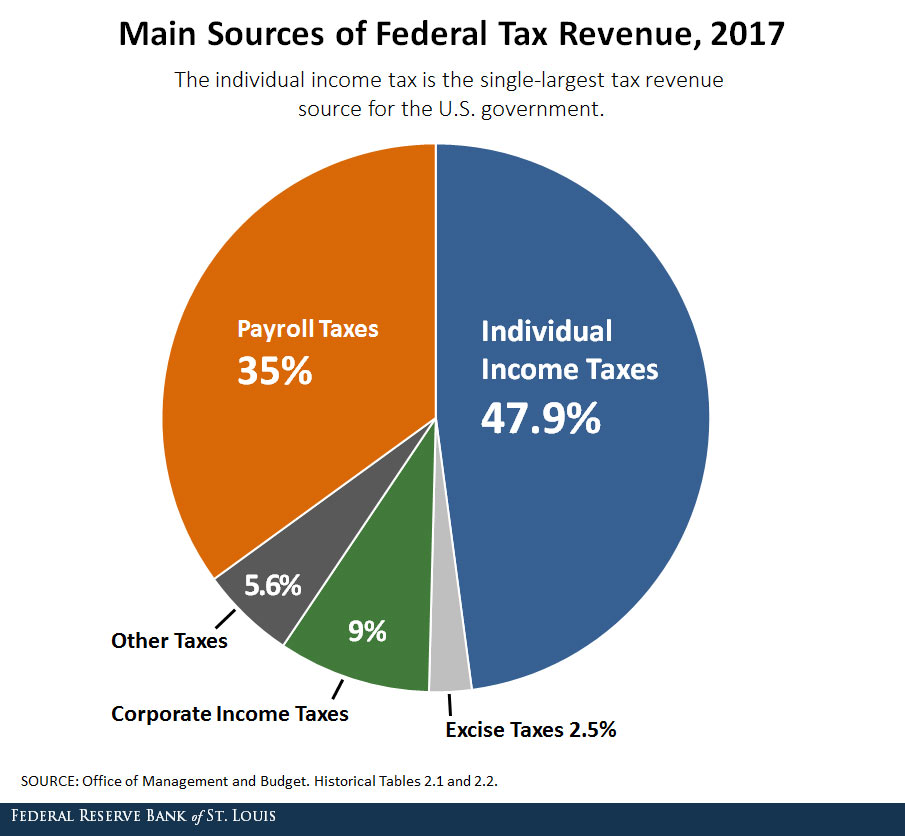

Payroll Taxes: Social Security and Medicare

Often overlooked in daily financial discussions, payroll taxes are a critical component of federal taxation, primarily funding Social Security and Medicare.

Employer and Employee Contributions

Payroll taxes are typically withheld directly from an employee’s paycheck. The Federal Insurance Contributions Act (FICA) tax comprises two main components: Social Security and Medicare. For Social Security, both the employee and employer contribute a percentage of wages up to a certain annual limit. Medicare tax also involves both employee and employer contributions, but there’s no income limit. Employers are responsible for withholding the employee’s portion and remitting both their own and the employee’s share to the IRS. This shared responsibility ensures a broad base of funding for these essential social insurance programs, which provide retirement, disability, and healthcare benefits.

Self-Employment Tax Considerations

Individuals who are self-employed (freelancers, independent contractors, small business owners) are responsible for paying both the employer and employee portions of FICA taxes. This is known as self-employment tax. The rate is typically double the employee-only rate for Social Security and Medicare, applied to net earnings from self-employment. While this can seem like a significant burden, self-employed individuals can deduct one-half of their self-employment tax when calculating their adjusted gross income, providing some relief. Accurate record-keeping and quarterly estimated tax payments are crucial for self-employed individuals to avoid penalties.

Estate and Gift Taxes

These taxes are designed to address the transfer of wealth, either during one’s lifetime or after death.

Transferring Wealth Across Generations

The federal estate tax is levied on the total value of a deceased person’s assets (the “estate”) that are transferred to heirs. However, there’s a substantial exclusion amount, meaning only estates above a very high threshold are subject to this tax. This tax aims to prevent vast accumulations of wealth from passing entirely tax-free from one generation to the next. The federal gift tax applies to transfers of property or money from one person to another while the giver is still alive. Similar to the estate tax, there’s an annual exclusion amount per recipient, allowing individuals to give away a certain amount each year without incurring gift tax. Gifts exceeding this annual limit may count against the lifetime exclusion amount, potentially triggering gift tax if the cumulative lifetime and death transfers exceed the exemption. These taxes are complex and often require careful planning, typically with the assistance of financial and legal professionals, to navigate effectively.

Excise Taxes and Other Specific Levies

Beyond income, payroll, estate, and gift taxes, the federal government also collects revenue through various specialized levies.

Taxes on Goods, Services, and Activities

Excise taxes are taxes levied on the sale of specific goods or services, often considered “luxury” items, harmful products, or those that have external costs. Examples include taxes on gasoline, tobacco products, alcoholic beverages, airline tickets, and tanning services. These taxes are generally built into the price of the product or service and are paid by the consumer indirectly. They serve multiple purposes: raising revenue, discouraging consumption of certain goods (e.g., tobacco), and funding specific projects (e.g., gas taxes often fund highway maintenance). Other less common federal taxes include user fees for specific government services, customs duties on imported goods, and specialized taxes on certain industries or activities.

The Impact of Federal Taxes on Personal Finance and Business

Federal taxes are not just an annual obligation; they are a constant factor shaping financial decisions for both individuals and businesses. Proactive tax planning can significantly influence long-term financial health.

Tax Planning Strategies for Individuals

Effective tax planning is an ongoing process that goes beyond simply filing a tax return. It involves making informed financial decisions throughout the year to optimize one’s tax position.

Retirement Accounts and Tax Deferral

One of the most powerful tools for individual tax planning involves utilizing tax-advantaged retirement accounts. Accounts like 401(k)s and traditional IRAs allow individuals to contribute pre-tax dollars, reducing their current taxable income. The investments grow tax-deferred until retirement, at which point withdrawals are taxed. Roth 401(k)s and Roth IRAs offer the opposite benefit: contributions are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. Strategic use of these accounts can significantly reduce an individual’s lifetime tax burden, making them cornerstones of long-term financial planning.

Maximizing Deductions and Credits

Diligent record-keeping and an understanding of available deductions and credits are crucial. Individuals should regularly review their eligibility for standard versus itemized deductions. For those who itemize, tracking expenses such as mortgage interest, charitable contributions, medical expenses (above a certain threshold), and state and local taxes (subject to limits) can be beneficial. Similarly, understanding eligibility for various tax credits – such as those for education, dependent care, or energy-efficient home improvements – can provide direct reductions to tax liability. Many software programs and tax professionals can help identify these opportunities.

Corporate Tax Compliance and Planning

For businesses, federal taxes present a complex landscape that requires meticulous planning and adherence to regulations to ensure financial stability and growth.

Understanding Business Deductions and Credits

Businesses, regardless of size, face a multitude of federal tax obligations. Effective planning involves maximizing deductions for legitimate business expenses, such as salaries, rent, utilities, supplies, and depreciation of assets. Research and development (R&D) tax credits, energy credits, and various hiring incentives are also available to qualifying businesses, offering significant tax relief. The structure of a business (sole proprietorship, partnership, S-corporation, C-corporation) also dictates its federal tax treatment, with pass-through entities (like S-corps) avoiding corporate-level taxation but passing income (and losses) directly to owners’ individual tax returns.

Implications of Tax Reform

Corporate tax rates and regulations are frequently subject to reform, often with significant implications for business strategy. Recent reforms, such as the Tax Cuts and Jobs Act of 2017 (TCJA), dramatically lowered the corporate income tax rate and introduced new provisions like the qualified business income (QBI) deduction for pass-through entities. Businesses must stay abreast of these legislative changes, as they can impact investment decisions, hiring practices, and overall profitability. Engaging with tax counsel or an experienced CPA is vital for navigating complex reform landscapes and optimizing a business’s tax position.

How Federal Taxes Influence Economic Behavior

Beyond individual and business balance sheets, federal taxes play a profound role in shaping broader economic behavior and policy. Tax incentives can spur investment in certain sectors, encourage savings, or promote specific social objectives. For example, investment tax credits can stimulate capital expenditures, while tax breaks for homeownership influence real estate markets. Conversely, high taxes on certain activities can discourage them. The overall tax burden and the structure of the tax system can impact decisions about where businesses choose to locate, how much individuals save and spend, and the flow of capital throughout the economy. Governments also use tax policy as a counter-cyclical tool, adjusting rates or offering rebates to stimulate demand during economic downturns or curb inflation during periods of overheating.

Resources and Best Practices for Federal Tax Compliance

Navigating the intricacies of federal tax requires access to reliable information and, often, professional guidance. Staying informed and compliant is paramount.

Utilizing IRS Resources and Publications

The IRS website (IRS.gov) is the official and most comprehensive source for federal tax information. It offers a wealth of resources, including:

- Tax Forms and Publications: Access to all official forms, instructions, and detailed publications (e.g., Publication 17, “Your Federal Income Tax,” or Publication 334, “Tax Guide for Small Business”).

- FAQs and Tax Topics: Extensive databases covering common questions and specific tax subjects.

- Interactive Tax Assistant: A tool to help taxpayers determine if certain income is taxable or if they can claim specific deductions or credits.

- Taxpayer Assistance Center (TAC) Locator: Information on in-person assistance, though appointments are often required.

- Free Tax Help: Information on programs like Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) for qualifying taxpayers.

Regularly consulting these resources can help individuals and businesses understand their obligations and rights.

The Role of Tax Professionals

For many, particularly those with complex financial situations, engaging a qualified tax professional is not just a convenience but a necessity. Tax professionals, such as Certified Public Accountants (CPAs), Enrolled Agents (EAs), and tax attorneys, offer expertise in tax law, planning, and compliance. They can:

- Prepare and file tax returns accurately.

- Provide strategic tax planning advice to minimize liabilities.

- Represent taxpayers before the IRS in audits or other disputes.

- Assist with complex issues like international taxation, estate planning, or business tax structuring.

Choosing a reputable professional with appropriate credentials and experience is crucial.

Staying Informed About Tax Law Changes

Federal tax laws are not static; they are subject to frequent changes driven by legislative action, economic conditions, and judicial interpretations. What was true for last year’s tax return might not be true for this year’s. Therefore, a key best practice for effective financial management is to stay informed about current tax law changes. This can be achieved by:

- Subscribing to financial news outlets and tax-specific publications.

- Consulting with a tax professional who actively monitors legislative developments.

- Regularly checking the IRS website for updates and announcements.

- Participating in tax-related webinars or seminars.

Proactive awareness allows individuals and businesses to adapt their financial strategies in a timely manner, ensuring ongoing compliance and optimization of their tax position.

In conclusion, “what’s the federal tax” is a question with a multi-layered answer, encompassing a vast system designed to fund the nation’s operations and influence its economy. From understanding the core purpose and types of taxes to engaging in strategic planning and utilizing available resources, a comprehensive grasp of federal taxation is indispensable for sound personal finance and business success. By demystifying these complexities, individuals and businesses can navigate their tax obligations with greater confidence and foresight.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.