Navigating the landscape of student loan repayment can often feel like a complex journey, fraught with questions about who to pay, how to pay, and the most strategic way to manage this significant financial obligation. For many, the simple act of figuring out “where” to send their money is the first hurdle. This article aims to demystify the process, providing a comprehensive guide rooted in personal finance principles to help borrowers confidently manage their student loan payments and safeguard their financial well-being.

Student loans, whether federal or private, represent a substantial commitment. Understanding the mechanisms of repayment, from identifying your loan servicer to choosing the optimal payment strategy, is paramount. This isn’t just about avoiding late fees; it’s about making informed financial decisions that can save you thousands of dollars over the life of your loan and contribute positively to your overall financial health.

The First Step: Identifying Your Loan Servicer

Before you can make a payment, you need to know who is collecting it. Your loan servicer is the company that handles the billing and other services for your student loan. They are your primary point of contact for questions about your loan, payment options, and managing your account. The identity of your servicer depends largely on whether your loans are federal or private.

Federal Student Loans: The Centralized System

Federal student loans are issued by the U.S. Department of Education, but they are managed by various private companies, known as loan servicers, under contract with the government. These servicers act as the intermediary, processing payments, handling inquiries, and administering repayment plans.

How to Find Your Federal Loan Servicer:

The most reliable resource for federal student loan information is the National Student Loan Data System (NSLDS), which is accessible through StudentAid.gov. By logging in with your FSA ID, you can view a comprehensive record of all your federal student loans, including the loan amount, current status, and, crucially, the name and contact information of your assigned loan servicer(s). It’s possible to have multiple federal loans managed by different servicers, especially if you borrowed over several years.

Overview of Common Federal Loan Servicers:

The roster of federal loan servicers can change, but some of the most prominent ones include:

- Nelnet: A long-standing servicer managing a large portfolio of federal loans.

- MOHELA: The Missouri Higher Education Loan Authority, another major servicer.

- Aidvantage (Maximus Education, LLC): Took over some loan servicing from Navient.

- Edfinancial Services: Another key player in federal loan servicing.

- Great Lakes Educational Loan Services, Inc.: Historically a major servicer, now operating under Nelnet.

Once you identify your servicer, you’ll need to visit their specific website to set up an online account. This online portal will be your primary hub for making payments, viewing your loan details, and communicating with your servicer.

Private Student Loans: Direct Lender Relationships

Private student loans are offered by banks, credit unions, and other financial institutions. Unlike federal loans, there isn’t a centralized government system to track them. Your servicer for a private loan is typically the bank or financial institution that originated the loan, or a company they have contracted to service it.

How to Find Your Private Loan Servicer:

- Loan Agreements: The most direct way is to refer back to your original loan documents. These will clearly state the lender and servicer.

- Credit Report: Your credit report will list all your active loan accounts, including private student loans, along with the names of the lenders. You can obtain a free copy of your credit report annually from AnnualCreditReport.com.

- Bank Statements: If you’ve been making payments, your bank statements will show the recipient of those payments.

Common Private Lenders:

Major private student loan lenders often include institutions like:

- Sallie Mae

- Discover

- Wells Fargo

- Bank of America

- Various credit unions and regional banks

For private loans, you will typically make payments directly through your lender’s website or their designated online payment portal. Each lender will have its own system, so familiarizing yourself with their specific platform is essential.

Understanding Your Payment Options and Methods

Once you’ve identified your servicer, the next step is to understand the various ways you can make payments. While online payments have become the standard, other options exist, each with its own advantages and considerations.

Online Portals: The Primary Method

Almost all student loan servicers and private lenders offer a secure online portal for managing your account and making payments. This is generally the most convenient and efficient method.

Setting Up an Online Account: You’ll typically need your account number and personal information to register. Once registered, you can link your bank account (checking or savings) to facilitate electronic payments.

Making One-Time Payments vs. Scheduled Payments: You have the flexibility to make individual payments as they come due or schedule recurring payments. Scheduled payments can be particularly useful if your paydays don’t perfectly align with your due date, allowing you to pay shortly after receiving your income.

Pros and Cons of Online Payments:

- Pros: Convenience, speed, instant confirmation, access to loan details, secure environment.

- Cons: Requires internet access, potential for human error if information is entered incorrectly.

Automated Payments (Auto-Debit): A Smart Strategy

Enrolling in auto-debit, where your monthly payment is automatically deducted from your bank account on the due date, is often the most recommended payment method.

Benefits of Auto-Debit:

- Interest Rate Reduction: Many federal and private lenders offer a small interest rate reduction (e.g., 0.25%) for enrolling in auto-debit. While seemingly small, this can translate to significant savings over the life of your loan.

- Avoiding Missed Payments: Auto-debit eliminates the risk of forgetting a payment, protecting your credit score and preventing late fees.

- Predictability: Knowing your payment will be made automatically provides peace of mind and simplifies budgeting.

How to Enroll in Auto-Debit: You can typically enroll directly through your servicer’s online portal. You’ll need to provide your bank account information (routing and account number) and authorize the recurring debits.

Monitoring Your Auto-Debit Schedule: Even with auto-debit, it’s wise to periodically check your bank statements and loan servicer account to ensure payments are being processed correctly and on time.

Alternative Payment Channels

While online and auto-debit are preferred, other methods are available:

- Paying by Mail: You can mail a check or money order directly to your loan servicer. The mailing address for payments is usually found on your monthly statement or your servicer’s website. Be sure to include your account number to ensure the payment is properly credited. Allow ample time for mail delivery and processing to avoid late payments.

- Paying by Phone: Most servicers offer the option to make payments over the phone, either through an automated system or by speaking with a customer service representative. This can be useful for one-off payments or if you’re experiencing issues with the online portal, but it can be less convenient and may involve hold times.

- Using Third-Party Bill Pay Services: Some banks offer bill pay services that can send payments to your loan servicer. While convenient, exercise caution and ensure you understand how these services work, especially regarding payment processing times, to prevent delays.

Strategic Considerations for Student Loan Repayment

Beyond just knowing where and how to pay, understanding what payment strategy to employ is crucial for effective student loan management. This involves considering various repayment plans and options that can significantly impact your financial future.

Understanding Different Repayment Plans (Federal Loans)

Federal student loans offer a variety of repayment plans designed to accommodate different financial situations. Choosing the right plan can make your monthly payments manageable.

- Standard Repayment Plan: This is the default plan, with fixed monthly payments over a 10-year period (or 10 to 30 years for consolidated loans). It typically results in the least amount paid in interest over time.

- Graduated Repayment Plan: Payments start low and gradually increase, usually every two years, over a 10-year period. This plan is for those who expect their income to rise over time.

- Extended Repayment Plan: For borrowers with more than $30,000 in outstanding federal student loans, this plan allows for fixed or graduated payments over a period of up to 25 years, resulting in lower monthly payments but more interest paid overall.

- Income-Driven Repayment (IDR) Plans: These plans are designed to make federal loan payments affordable by capping them at a percentage of your discretionary income. The four main IDR plans are:

- SAVE (Saving on a Valuable Education) Plan: The newest IDR plan, offering the most generous terms for many borrowers, including potential interest subsidies.

- PAYE (Pay As You Earn) Repayment Plan: Payments are generally 10% of discretionary income.

- IBR (Income-Based Repayment) Plan: Payments are generally 10% or 15% of discretionary income.

- ICR (Income-Contingent Repayment) Plan: Payments are the lesser of 20% of discretionary income or what you would pay on a fixed 12-year plan.

IDR plans also offer the potential for loan forgiveness after 20 or 25 years of qualifying payments (or 10 years for Public Service Loan Forgiveness). You must re-certify your income and family size annually to remain on an IDR plan.

The Role of Refinancing for Private and Federal Loans

Refinancing involves taking out a new loan, typically from a private lender, to pay off one or more existing student loans.

When Refinancing Makes Sense:

- Lower Interest Rates: If your credit score has improved since you first took out your loans, or if interest rates have dropped, you might qualify for a lower rate, saving you money.

- Simpler Payments: Consolidating multiple loans into one new loan can simplify your monthly payments, as you’ll only have one bill and one due date.

- Changing Loan Terms: Refinancing can allow you to choose a shorter or longer repayment term to either save on interest or lower your monthly payment.

Losing Federal Protections When Refinancing Federal Loans: This is a critical consideration. Refinancing federal loans into a new private loan means you forfeit valuable federal benefits, such as access to IDR plans, deferment and forbearance options, and potential federal loan forgiveness programs. This step should only be taken after careful consideration of your financial stability and future career plans.

Comparing Refinancing Lenders: Shop around and compare offers from multiple private lenders. Look at interest rates (fixed vs. variable), loan terms, and any fees involved.

Managing Multiple Loans and Consolidation

Many borrowers have multiple student loans, each with its own interest rate and terms. Efficiently managing these can be challenging.

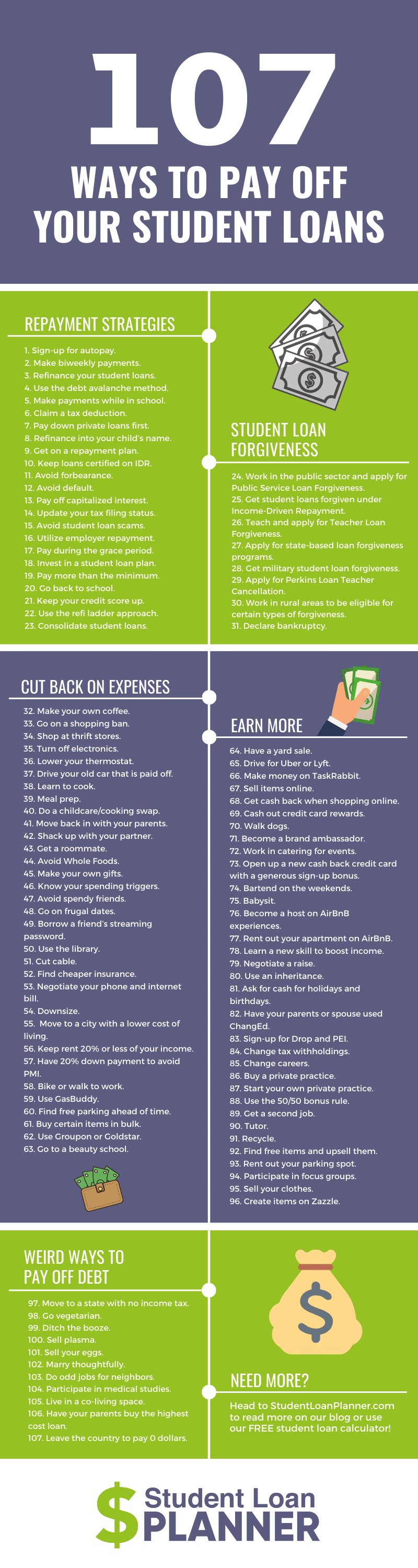

- Prioritizing Payments: A common strategy is the “debt avalanche” method: make minimum payments on all loans, but direct any extra money you can afford toward the loan with the highest interest rate. This minimizes the total interest paid over time.

- Federal Direct Consolidation Loans: This option allows you to combine multiple federal student loans into a single new federal loan. The interest rate on a consolidation loan is a weighted average of your previous loans, rounded up to the nearest one-eighth of a percent. While it doesn’t typically lower your interest rate, it can simplify payments and sometimes help you qualify for certain IDR plans or Public Service Loan Forgiveness if your original loans weren’t eligible. It does not offer the same benefits as private refinancing.

Essential Tools and Best Practices for Seamless Payments

Effective student loan management goes beyond just making payments; it involves proactive planning and leveraging available resources.

Leveraging Technology for Financial Management

A variety of digital tools can help you stay on top of your student loan obligations.

- Budgeting Apps and Software: Tools like Mint, YNAB (You Need A Budget), or Personal Capital can help you track your income and expenses, allowing you to allocate funds for loan payments and identify areas for savings.

- Payment Reminder Tools: Set up calendar alerts, use your servicer’s reminder notifications, or utilize dedicated financial apps to ensure you never miss a payment due date.

- Financial Aggregators: Platforms that pull all your financial accounts into one dashboard can give you a holistic view of your financial health, including your student loan balances and progress.

Proactive Communication with Your Servicer

Your loan servicer isn’t just a bill collector; they are a resource. Don’t hesitate to reach out if you anticipate difficulty or have questions.

- When to Contact Your Servicer:

- If you’re experiencing financial hardship and may struggle to make payments.

- If you have questions about your repayment plan options.

- If your income or family size changes (especially for IDR plans).

- If you notice any discrepancies on your account.

- Understanding Deferment and Forbearance: These are temporary options to pause or reduce your payments. While they can provide short-term relief, interest often continues to accrue, potentially increasing your total loan cost. Understand the terms and implications before using them.

- Documenting All Interactions: Keep records of all communications with your servicer, including dates, names of representatives, and summaries of conversations. This can be invaluable if disputes arise.

Staying Informed About Policy Changes

Student loan policies, particularly federal ones, can change. Staying informed is vital.

- Importance of Monitoring Federal Policy Updates: Keep an eye on news from the Department of Education, StudentAid.gov, and reputable financial news sources. Major policy shifts can impact repayment plans, interest rates, and loan forgiveness programs.

- Impact of Changes on IDR Plans, Interest Rates, and Loan Forgiveness Programs: For instance, the recent introduction of the SAVE Plan significantly altered IDR benefits. Being aware of such changes can help you adjust your strategy and take advantage of new opportunities.

Avoiding Common Pitfalls and Ensuring Financial Health

Successfully managing student loans also means being aware of potential traps and proactive in protecting your financial standing.

The Dangers of Missed Payments and Default

Failing to make timely payments can have severe and long-lasting consequences.

- Consequences of Late Payments:

- Late Fees: Servicers typically charge a fee for late payments.

- Credit Score Damage: Late payments are reported to credit bureaus and can significantly harm your credit score, making it harder to get approved for future loans, mortgages, or even rental agreements.

- Accrued Interest: Interest continues to accrue, increasing your total debt.

- What Happens in Default: Default occurs after an extended period of non-payment (usually 270 days for federal loans). The consequences are dire:

- Wage Garnishment: Your employer may be legally required to withhold a portion of your wages.

- Tax Refund Offset: Your federal and state tax refunds may be withheld to pay off your debt.

- Social Security Benefit Offset: A portion of your Social Security benefits can be withheld.

- Loss of Eligibility for Federal Aid: You lose access to federal student aid programs.

- Collection Fees: The government can add collection costs to your loan balance.

- Strategies to Avoid Default: The best defense is proactive communication. If you foresee difficulties, contact your servicer immediately to explore options like changing repayment plans, deferment, or forbearance. Never ignore your loan obligations.

Guarding Against Scams and Misinformation

The student loan landscape is unfortunately a target for scammers.

- Identifying Legitimate Communication from Your Servicer: Official communications will typically come from your servicer’s recognized name and contact information. Be wary of generic emails or calls demanding immediate payment or personal information.

- Beware of Unsolicited Offers for “Debt Relief” or “Loan Forgiveness” for a Fee: Legitimate loan forgiveness programs (like PSLF or IDR forgiveness) do not require upfront payments. Scammers often promise quick fixes or full forgiveness in exchange for fees, then disappear.

- Using Official Government Resources (StudentAid.gov): Always cross-reference information with official sources. StudentAid.gov is the definitive resource for federal student loan information, including legitimate programs and warnings about scams. Never give your FSA ID or personal information to third parties.

Paying your student loans is more than a monthly transaction; it’s an ongoing commitment that requires diligence, understanding, and strategic planning. By knowing where to direct your payments, understanding your available options, and maintaining proactive engagement with your financial health, you can successfully navigate your repayment journey and move confidently toward financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.