In the rapidly evolving landscape of personal finance, the transition from physical cash to digital ecosystems is nearly complete. Peer-to-peer (P2P) payment platforms have evolved from simple “bill-splitting” apps into comprehensive financial tools that impact how we budget, save, and manage our cash flow. At the forefront of this revolution is Venmo. Owned by PayPal, Venmo has become more than just a convenience; it is a fundamental component of the modern financial toolkit.

Setting up Venmo correctly is not merely a matter of downloading an app; it is about integrating a powerful digital wallet into your broader financial strategy. Whether you are a freelancer looking to streamline client payments, a budget-conscious student, or an investor exploring the world of digital assets, understanding the nuances of Venmo’s setup is essential for maintaining financial health and security.

The Strategic Role of Venmo in Modern Money Management

Before diving into the technical steps of the setup, it is vital to understand where Venmo fits within your personal finance ecosystem. Venmo functions as a “bridge” between your traditional banking institutions and your daily social and professional interactions. By effectively managing this bridge, you can gain better visibility into your spending habits and optimize your liquid assets.

Choosing Between Personal and Business Profiles

One of the most critical financial decisions you will make during the setup process is whether to operate a personal profile, a business profile, or both. For many, a personal profile is sufficient for reimbursing friends for dinner or sharing rent costs. However, for those with a side hustle or a small business, a Venmo Business Profile offers specialized features such as tax reporting and professional branding. From a money management perspective, keeping these two streams separate is crucial for accurate accounting and tax compliance, especially following recent IRS regulations regarding 1099-K reporting for P2P transactions.

The Impact on Cash Flow and Budgeting

Venmo can either be a boon or a hindrance to your budget. Because transactions feel “invisible” compared to handing over physical cash, it is easy to overspend. During the setup phase, consider how you will track these expenses. Many high-level financial tracking apps, such as Mint or YNAB (You Need A Budget), can sync with your bank account to categorize Venmo transfers. Recognizing Venmo as a real-time deduction from your wealth, rather than a separate “play money” account, is a hallmark of sophisticated financial planning.

Step-by-Step: Setting Up Your Account for Financial Success

To ensure your Venmo account is a secure and efficient financial tool, you must follow a structured setup process. This ensures that your identity is verified, your funds are accessible, and you are not hit with unexpected fees or transaction limits.

Account Creation and Identity Verification

The first step is downloading the app and creating an account using a secure email and a strong, unique password. However, the most important part of this stage from a financial perspective is identity verification. Under the USA PATRIOT Act, financial institutions are required to verify the identity of their users. By navigating to the “Settings” and completing the identity verification process (which typically requires your legal name, address, and Social Security Number), you unlock higher transaction limits. For individuals moving significant sums of money—such as monthly rent or freelance payments—this step is non-negotiable to avoid having funds frozen during a transfer.

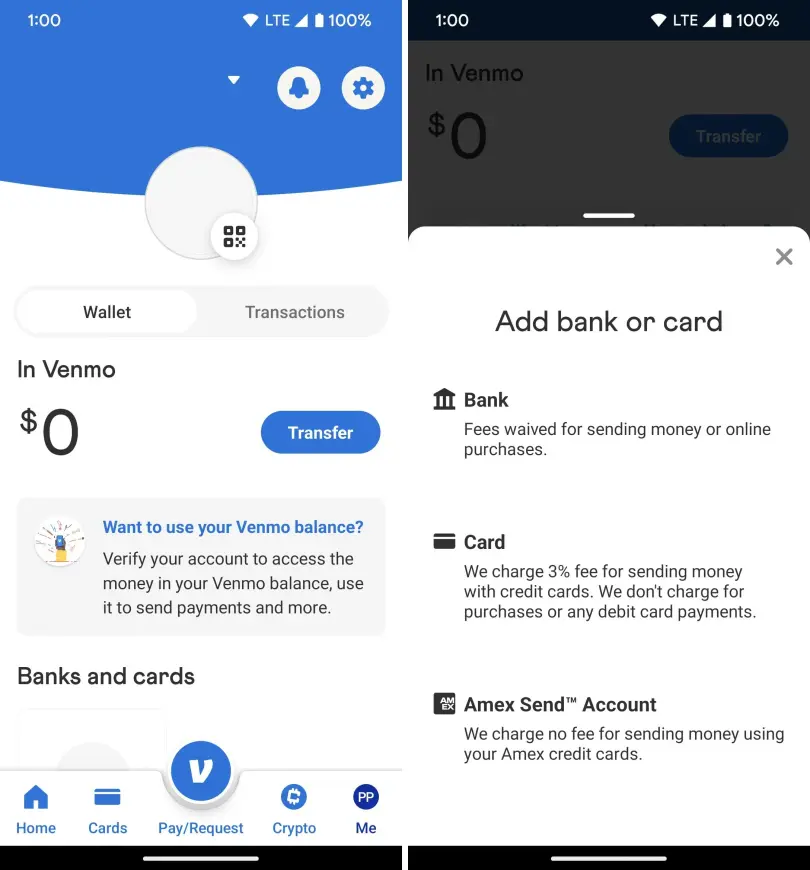

Linking Banking and Credit Assets

Once your profile is established, you must link a funding source. This is where strategic financial decision-making comes into play. You have three primary options:

- Bank Account (ACH): Linking your checking account is generally the most cost-effective method. Transfers are free, making this the ideal choice for regular use.

- Debit Card: This offers the fastest way to pull funds but functions similarly to a bank account.

- Credit Card: While convenient, Venmo charges a 3% fee for transactions funded by a credit card. From a personal finance standpoint, this is rarely advisable unless you are leveraging a specific rewards strategy that outweighs the 3% cost—a difficult feat to achieve.

Understanding Transfer Speeds and Liquidity

Venmo offers two ways to move money from your Venmo balance to your bank account: Standard Transfer and Instant Transfer. The Standard Transfer is free but takes 1-3 business days. The Instant Transfer allows you to move money within minutes for a small percentage fee (typically 1.75%, with a minimum and maximum cap). Effective money management involves planning your liquidity so that you never need to pay for an Instant Transfer. By anticipating your cash needs, you can keep that 1.75% in your own pocket.

Navigating the Financial Nuances: Fees, Limits, and Taxes

A professional approach to using Venmo requires a deep dive into the “fine print” that governs the movement of your money. Understanding the fee structure and the regulatory environment will prevent costly mistakes.

Minimizing Transaction Fees

Beyond the credit card and instant transfer fees mentioned previously, users should be aware of fees associated with the Venmo Business Profile. If you are receiving money for goods or services, Venmo charges a seller fee (currently 1.9% + $0.10). This is a standard cost of doing business, but it must be factored into your pricing strategy. If you are a freelancer, ensure your rates account for these “hidden” costs of digital payment processing.

Managing Transaction and Balance Limits

For unverified accounts, Venmo imposes strict limits on how much you can spend and transfer. Once verified, these limits increase significantly (often up to $60,000 per week for certain transactions). Monitoring these limits is essential for business owners who may need to move large sums for inventory or payroll. From a wealth protection standpoint, you should also decide whether to keep a balance in Venmo or “sweep” it to your high-yield savings account (HYSA) regularly. Since Venmo balances typically do not earn interest, leaving large sums in the app represents an “opportunity cost” where your money isn’t working for you.

Tax Implications and the 1099-K

The IRS has updated its reporting requirements for P2P apps. While the implementation has seen various delays and adjustments, the general trend is toward greater transparency. If you use Venmo for business and exceed certain thresholds, Venmo is required to report that income to the IRS. Setting up your account correctly involves marking business transactions as such to ensure your personal reimbursements aren’t mistakenly flagged as taxable income. Keeping meticulous records of your Venmo history is no longer optional; it is a vital part of modern tax planning.

Security Protocols for Protecting Your Digital Assets

In the digital age, financial security is synonymous with financial health. A compromised Venmo account can provide a gateway to your primary bank accounts, making security the most critical aspect of your setup.

Implementing Multi-Factor Authentication (MFA)

The basic password is no longer sufficient. During setup, you should immediately enable Multi-Factor Authentication. This adds a layer of protection by requiring a code sent to your mobile device or generated by an authenticator app. Furthermore, enable biometric locks (FaceID or Fingerprint) within the app settings. This ensures that even if someone gains physical access to your phone, your financial data remains under lock and key.

Privacy Settings as a Financial Safeguard

Venmo is unique because of its social feed, but from a financial security perspective, “Public” transactions are a liability. Scammers often use public transaction data to “social engineer” victims, or to track your spending habits for more targeted phishing attacks. Professional money management suggests setting your default privacy to “Private.” This ensures that only you and the recipient can see the transaction, keeping your financial life out of the public eye and reducing your profile as a target for fraud.

Venmo as a Financial Growth Tool: Crypto and Credit

For the advanced user, Venmo has expanded its features to include investment opportunities and credit products, transforming it from a simple payment app into a micro-investment platform.

Diversifying into Cryptocurrency

Venmo now allows users to buy, sell, and hold cryptocurrencies like Bitcoin and Ethereum with as little as $1. While this should not replace a primary brokerage account or a cold-storage wallet for serious investors, it offers a low-friction entry point for those looking to diversify a small portion of their portfolio. When setting this up, consider the tax implications: every “sale” of crypto is a taxable event (Capital Gains), and Venmo provides the necessary documentation to track these for your annual filing.

The Venmo Credit Card and Cashback Strategy

For those with disciplined credit habits, the Venmo Credit Card offers a unique “Money” hack. It automatically categorizes your spending and offers 3% cashback on your top spend category. This cashback can even be set to automatically purchase cryptocurrency, creating a “set-it-and-forget-it” investment strategy. Integrating this card into your setup allows you to earn rewards on the very transactions that typically don’t offer them, such as splitting a utility bill with a roommate.

Conclusion: A Proactive Approach to Digital Finance

Setting up Venmo is more than a technical hurdle; it is a strategic move in your personal finance journey. By treating the app as a professional financial tool—complete with identity verification, optimized funding sources, rigorous security protocols, and an eye toward tax compliance—you position yourself to navigate the digital economy with confidence.

As we continue to move toward a “cashless” society, the individuals who master these tools will be the ones who maintain the tightest control over their wealth. Whether you are using it to manage a side hustle or simply to navigate the social complexities of shared expenses, a well-configured Venmo account is a cornerstone of a modern, efficient, and secure financial life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.