Understanding how to calculate interest is one of the most vital skills in the realm of personal and business finance. Whether you are a first-time homebuyer looking at mortgage rates, an entrepreneur seeking a business loan, or an investor trying to project the growth of a retirement account, interest is the invisible force that determines the ultimate cost or value of your capital.

At its core, interest is the price of money. For a borrower, it is the cost of using someone else’s capital. For a lender or investor, it is the compensation for the risk and the “opportunity cost” of not having that money available for other uses. To navigate the financial world successfully, one must move beyond simply looking at a percentage rate and understand the underlying mechanics of how that rate translates into actual currency.

1. The Mechanics of Simple Interest

Simple interest is the most straightforward method of calculating the cost of a loan or the growth of an investment. It is calculated solely on the principal amount—the original sum of money borrowed or invested—and does not account for interest earned or charged in previous periods.

The Simple Interest Formula

The formula for simple interest is universally recognized in finance as:

Interest = P × r × t

In this equation:

- P (Principal): The initial amount of money.

- r (Annual Interest Rate): The interest rate expressed as a decimal (e.g., 5% becomes 0.05).

- t (Time): The duration for which the money is borrowed or invested, usually expressed in years.

For example, if you lend $10,000 to a business associate for three years at a simple interest rate of 6%, the calculation would be: $10,000 × 0.06 × 3 = $1,800. At the end of the term, you would receive your $10,000 back plus $1,800 in interest.

Real-World Applications of Simple Interest

While most modern banking products use more complex methods, simple interest remains prevalent in specific financial areas:

- Short-term Personal Loans: Many informal loans or short-term bridge loans use simple interest to keep the terms clear for both parties.

- Automobile Loans: A significant portion of car loans use a simple interest model, where interest is calculated based on the balance on the day the payment is due. This benefits the borrower who pays early, as it reduces the total interest paid.

- Certificates of Deposit (CDs): Some basic fixed-income products pay out simple interest on a periodic basis rather than reinvesting it.

2. Compound Interest: The Engine of Wealth Creation

If simple interest is a linear progression, compound interest is exponential. Albert Einstein famously referred to compound interest as the “eighth wonder of the world,” noting that “he who understands it, earns it; he who doesn’t, pays it.”

Compounding occurs when interest is added to the principal, and then the interest for the next period is calculated based on that new, larger total. Essentially, you are earning “interest on interest.”

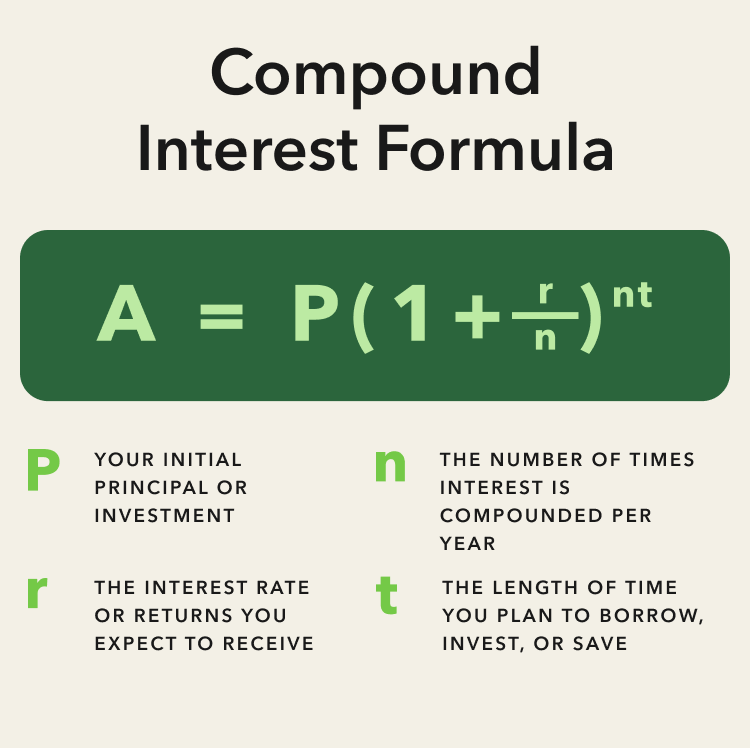

The Compound Interest Formula

Calculating compound interest is more complex because it must account for the frequency of compounding. The formula is:

A = P(1 + r/n)^{nt}

In this equation:

- A: The final amount (Principal + Interest).

- P: The principal amount.

- r: The annual interest rate (decimal).

- n: The number of times interest is compounded per year (e.g., 12 for monthly, 4 for quarterly).

- t: The number of years the money is invested or borrowed.

To find the interest alone, you subtract the principal from the final amount (A – P).

The Power of Compounding Frequency

The frequency of compounding ($n$) has a dramatic impact on the final result. The more frequently interest is compounded—daily versus annually, for example—the faster the balance grows.

Consider an investment of $10,000 at a 10% interest rate for 10 years.

- Annual Compounding: $10,000(1 + 0.10/1)^{10} = $25,937.42

- Monthly Compounding: $10,000(1 + 0.10/12)^{120} = $27,070.41

- Daily Compounding: $10,000(1 + 0.10/365)^{3650} = $27,179.10

For the savvy investor, choosing a vehicle with high compounding frequency can lead to significantly higher returns over long periods. Conversely, for a borrower, high-frequency compounding (common in credit cards) can lead to a debt spiral.

3. Interest in the Context of Personal Debt

While interest is a tool for growth in investing, it is a cost to be managed in debt. Understanding how interest is applied to mortgages and credit cards is essential for maintaining a healthy balance sheet.

Amortization and Mortgage Interest

Most mortgages use a process called amortization. In the early years of a 30-year mortgage, the majority of your monthly payment goes toward paying off the interest, while only a small fraction reduces the principal.

To calculate the interest portion of a single monthly mortgage payment, you can use the following:

(Remaining Loan Balance × Annual Interest Rate) / 12 months

Because the “Remaining Loan Balance” decreases every month, the interest portion of your payment slowly shrinks over time, allowing more of your money to go toward the principal in the later years of the loan. This is why making extra principal payments early in the life of a mortgage can save a homeowner tens of thousands of dollars in total interest.

Credit Card APR and Daily Periodic Rates

Credit cards are among the most expensive forms of debt due to how they calculate interest. Banks typically use an “Annual Percentage Rate” (APR), but they apply it daily.

To find your daily periodic rate, you divide your APR by 365. If your APR is 24%, your daily rate is approximately 0.0657%. Most credit card issuers use the Average Daily Balance method. They track your balance every single day of the billing cycle, add them up, divide by the number of days in the cycle, and then multiply that average by the daily periodic rate and the number of days in the month.

Because credit cards compound daily, carrying a balance is one of the most significant obstacles to building personal wealth.

4. Advanced Financial Tools and Strategic Short-cuts

In a professional financial setting, you won’t always have time to run complex formulas manually. Understanding the “short-cuts” and tools available can help you make rapid, informed decisions.

The Rule of 72

The Rule of 72 is a simplified way to estimate how long it will take for an investment to double at a fixed annual rate of interest.

Years to Double = 72 / Interest Rate

For example, if you are earning a 6% return on your mutual funds, it will take approximately 12 years (72 / 6) for your money to double. If you can increase that return to 9%, your money will double in just 8 years. This rule is a powerful mental model for comparing different investment opportunities or understanding the impact of inflation on your purchasing power.

Nominal vs. Effective Interest Rates

When comparing financial products, it is crucial to distinguish between the nominal rate and the Effective Annual Rate (EAR). The nominal rate is the stated interest rate, but the EAR accounts for the effects of compounding within the year.

EAR = (1 + r/n)^n – 1

If a savings account offers a 5% nominal rate compounded monthly, the EAR is actually 5.116%. In the “Money” niche, always look for the Annual Percentage Yield (APY) for savings and APR for loans, as these figures are designed to provide a more accurate “apples-to-apples” comparison by accounting for compounding and fees.

Leveraging Financial Software

For complex business finance or multi-year investment projections, tools like Microsoft Excel or Google Sheets are indispensable. Key functions include:

- =PMT(rate, nper, pv): Calculates the payment for a loan based on constant payments and a constant interest rate.

- =FV(rate, nper, pmt, [pv]): Calculates the future value of an investment based on periodic, constant payments and a constant interest rate.

- =INTEREST(p, r, t): Various built-in templates allow users to visualize amortization schedules instantly.

Conclusion: The Strategic Value of Interest Literacy

Calculating interest is not merely a mathematical exercise; it is a strategic necessity. In the world of money, interest represents the boundary between profit and loss. By mastering the distinction between simple and compound interest, understanding the weight of daily compounding in debt, and utilizing tools like the Rule of 72, you gain a significant advantage in managing your financial life.

For the investor, interest is the wind at your back, pushing your capital toward a future of financial independence. For the borrower, interest is a hurdle that must be cleared with precision and care. Whether you are balancing a corporate budget or a checkbook, the ability to calculate and respect the power of interest is the hallmark of financial maturity. Always remember: in the economy of today, those who calculate interest accurately are the ones who ultimately control their financial destiny.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.