In the complex ecosystem of global finance, few figures carry as much weight for the average consumer and business owner as the prime rate. While it often fluctuates quietly in the background of financial news cycles, its ripple effects are felt in every corner of the economy—from the interest you pay on your credit card balance to the feasibility of a small business expansion. Understanding the current prime rate is not merely an academic exercise; it is a fundamental component of strategic personal and business financial planning.

The Fundamentals of the Prime Rate: Defining the Benchmark

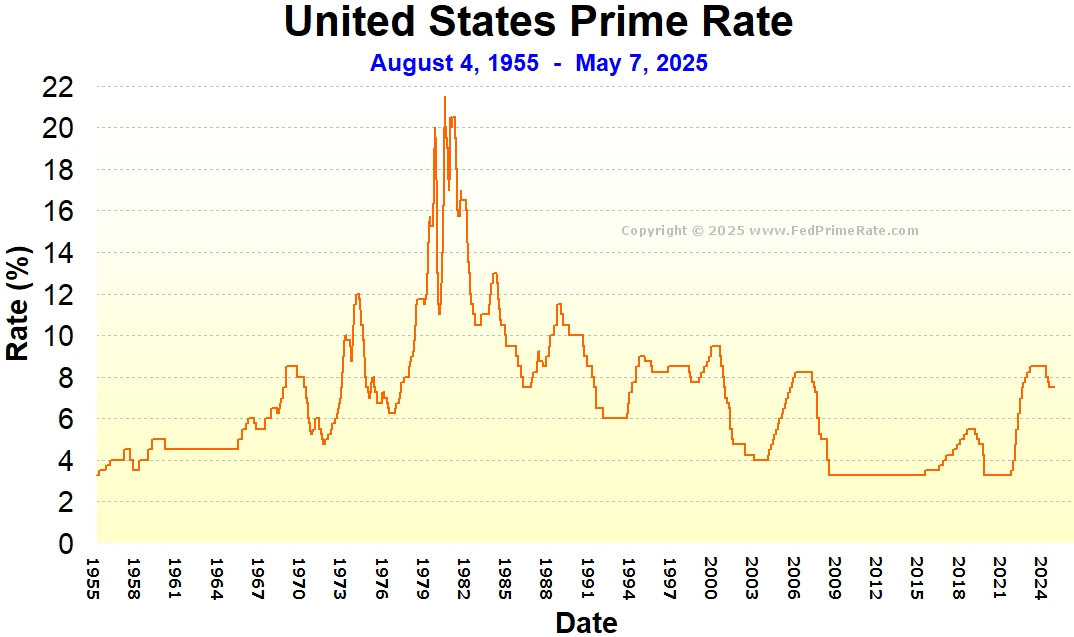

The prime rate, often referred to as the “prime interest rate,” is the base interest rate that commercial banks charge their most creditworthy corporate customers. These are typically large corporations with impeccable financial standing and a very low risk of default. However, its influence extends far beyond these elite entities. The prime rate serves as the foundational index for a vast array of consumer and commercial loan products.

The Wall Street Journal Prime Rate vs. Individual Bank Rates

While any bank can technically set its own prime rate, the industry standard in the United States is the “Wall Street Journal (WSJ) Prime Rate.” The WSJ surveys the 30 largest banks in the country; when at least 23 of them (75%) change their prime rate, the WSJ updates its published figure. This consensus-based approach ensures a level of stability and uniformity across the lending landscape, providing a reliable benchmark for lenders and borrowers alike.

The Mathematical Connection: Prime and the Federal Funds Target Rate

The prime rate does not exist in a vacuum. In the United States, it is directly tied to the Federal Funds Target Rate, which is the interest rate set by the Federal Reserve (the Fed) for overnight loans between banks. Historically, the prime rate is almost always set exactly 3.00 percentage points (300 basis points) above the Federal Funds Target Rate. For example, if the Fed sets its target range at 5.25% to 5.50%, the prime rate will typically be adjusted to 8.50%. This 3% spread covers the banks’ administrative costs and provides a profit margin, while reflecting the inherent risk of lending to even the most stable corporations compared to the risk-free nature of interbank lending.

Why the Prime Rate Matters to Your Personal Wallet

For most individuals, the prime rate is the silent engine behind the “Variable APR” (Annual Percentage Rate) listed on their financial statements. When the prime rate moves, the cost of borrowing for millions of Americans changes almost instantly.

Credit Cards and Variable Interest Rates

The majority of credit cards carry variable interest rates. These rates are usually calculated as “Prime + Margin.” For instance, if your credit card agreement specifies a margin of 15% and the current prime rate is 8.5%, your total APR is 23.5%. When the Federal Reserve raises rates to combat inflation, and the prime rate subsequently increases, your credit card interest rate rises in lockstep. This makes carrying a balance significantly more expensive over time, emphasizing the importance of debt management in high-rate environments.

Home Equity Lines of Credit (HELOCs)

Unlike most primary mortgages, which are fixed-rate, Home Equity Lines of Credit (HELOCs) are almost always tied to the prime rate. Because HELOCs are revolving lines of credit, the interest rate you pay on your outstanding balance can fluctuate monthly. For homeowners using a HELOC for renovations or debt consolidation, a rising prime rate can lead to unexpected increases in monthly minimum payments, potentially straining household budgets.

Impact on Auto Loans and Personal Loans

While many auto loans and personal loans offer fixed rates at the time of signing, the initial offer you receive from a lender is heavily influenced by the current prime rate. Lenders use the prime rate as their “floor.” When the prime rate is low, banks compete for borrowers by offering lower margins, leading to the “cheap money” eras that encourage consumer spending. Conversely, when the prime rate is high, the barrier to entry for affordable financing becomes much higher, often cooling the market for high-ticket items like vehicles.

The Macroeconomic Drivers Behind Rate Changes

To understand where the prime rate is going, one must understand why it moves. The prime rate is a reactive tool used to manage the broader health of the national economy.

The Role of the Federal Open Market Committee (FOMC)

The Federal Open Market Committee (FOMC) meets eight times a year to review economic data and decide whether to change the Federal Funds Rate. Their primary mandate is “dual”: to promote maximum employment and maintain stable prices (low inflation). When the economy is growing too fast and inflation begins to rise, the FOMC increases interest rates to “cool” the economy. This ripple effect immediately raises the prime rate, making borrowing more expensive and slowing down spending and investment.

Inflation Targets and Monetary Tightening

Inflation is the primary enemy of a stable prime rate. When the cost of goods and services rises beyond the Fed’s traditional 2% target, the central bank enters a phase of “monetary tightening.” By raising the prime rate, the cost of capital increases for businesses. This leads to a reduction in expansion projects and potentially slower hiring, which eventually reduces the amount of money circulating in the economy. Understanding this cycle allows investors and savers to anticipate shifts in the prime rate based on monthly Consumer Price Index (CPI) reports.

Strategic Financial Planning in a Fluctuating Prime Rate Environment

A changing prime rate requires a proactive financial strategy. Whether the rate is rising or falling, there are specific steps individuals and businesses can take to protect their capital.

Consolidating High-Interest Debt

In an environment where the prime rate is expected to rise, the most effective strategy is to move variable-rate debt into fixed-rate products. For consumers with high credit card balances, this might involve a balance transfer to a 0% APR card or taking out a fixed-rate personal loan to pay off the variable-rate debt. By locking in a rate before the prime rate climbs higher, you insulate yourself from future interest hikes.

Balancing Fixed-Rate vs. Variable-Rate Financing

For businesses and sophisticated investors, the choice between fixed and variable rates is a matter of risk management. When the prime rate is at a historical peak, it may actually be beneficial to take a variable-rate loan if you anticipate that the Fed will cut rates in the near future. This allows your interest expense to decrease automatically without the need for a costly refinancing process. Conversely, in a low-rate environment, locking in long-term fixed financing is the gold standard for protecting against future volatility.

The Silver Lining: Impact on Savings and Cash Reserves

While a high prime rate is a burden for borrowers, it is a boon for savers. Banks typically increase the rates offered on High-Yield Savings Accounts (HYSAs) and Certificates of Deposit (CDs) when the prime rate rises. For those with significant cash reserves, a high prime rate environment provides an opportunity to earn a meaningful, low-risk return on capital that was not possible during the “near-zero” rate eras.

The Future Outlook for the Prime Rate

Predicting the future of the prime rate involves a careful analysis of global supply chains, labor markets, and geopolitical stability.

Watching Economic Indicators

To forecast the direction of the prime rate, one must look at leading economic indicators. High unemployment usually signals that the Fed will lower rates (and thus the prime rate) to stimulate the economy. Conversely, a “hot” labor market with high wage growth often suggests that inflation may persist, leading the Fed to keep the prime rate elevated for a longer period.

Preparing Your Business for Interest Rate Volatility

For business owners, the current prime rate dictates the “hurdle rate”—the minimum return a project must generate to be worth the investment. In a high-rate environment, businesses must be more selective with their capital expenditures. Preparing for volatility means maintaining a “liquidity cushion” and stress-testing your business model to ensure you can meet debt obligations even if the prime rate increases by another 100 or 200 basis points.

In conclusion, the current prime rate is more than just a statistic; it is a barometer of the economic climate. By staying informed about how it is calculated, why it changes, and how it affects various financial products, you can make more informed decisions regarding your debt, your savings, and your long-term investment strategy. Whether you are a first-time homebuyer or a seasoned corporate treasurer, the prime rate remains one of the most vital metrics in your financial toolkit.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.