When a family hears the word “hospice,” the immediate reaction is often emotional. However, from a fiscal and strategic perspective, entering hospice care represents one of the most significant shifts in a household’s financial management and healthcare spending. In the world of personal finance and estate planning, “being on hospice” is a specific status that triggers a unique set of insurance benefits, cost-saving measures, and urgent financial priorities.

Understanding the financial architecture of hospice is essential for protecting a family’s legacy and ensuring that the final stages of life are managed with dignity and fiscal responsibility. This guide explores the economic implications of hospice care, from Medicare structures to the strategic preservation of assets.

The Economics of Hospice: Understanding the Medicare Benefit

Hospice care in the United States is fundamentally defined by its funding source. For the vast majority of seniors, being on hospice means transitioning into a specialized insurance “benefit period” primarily funded by Medicare Part A. This transition changes the way healthcare is billed, moving away from a “fee-for-service” model toward a “per diem” or bundled payment system.

Eligibility and the “Six-Month” Financial Rule

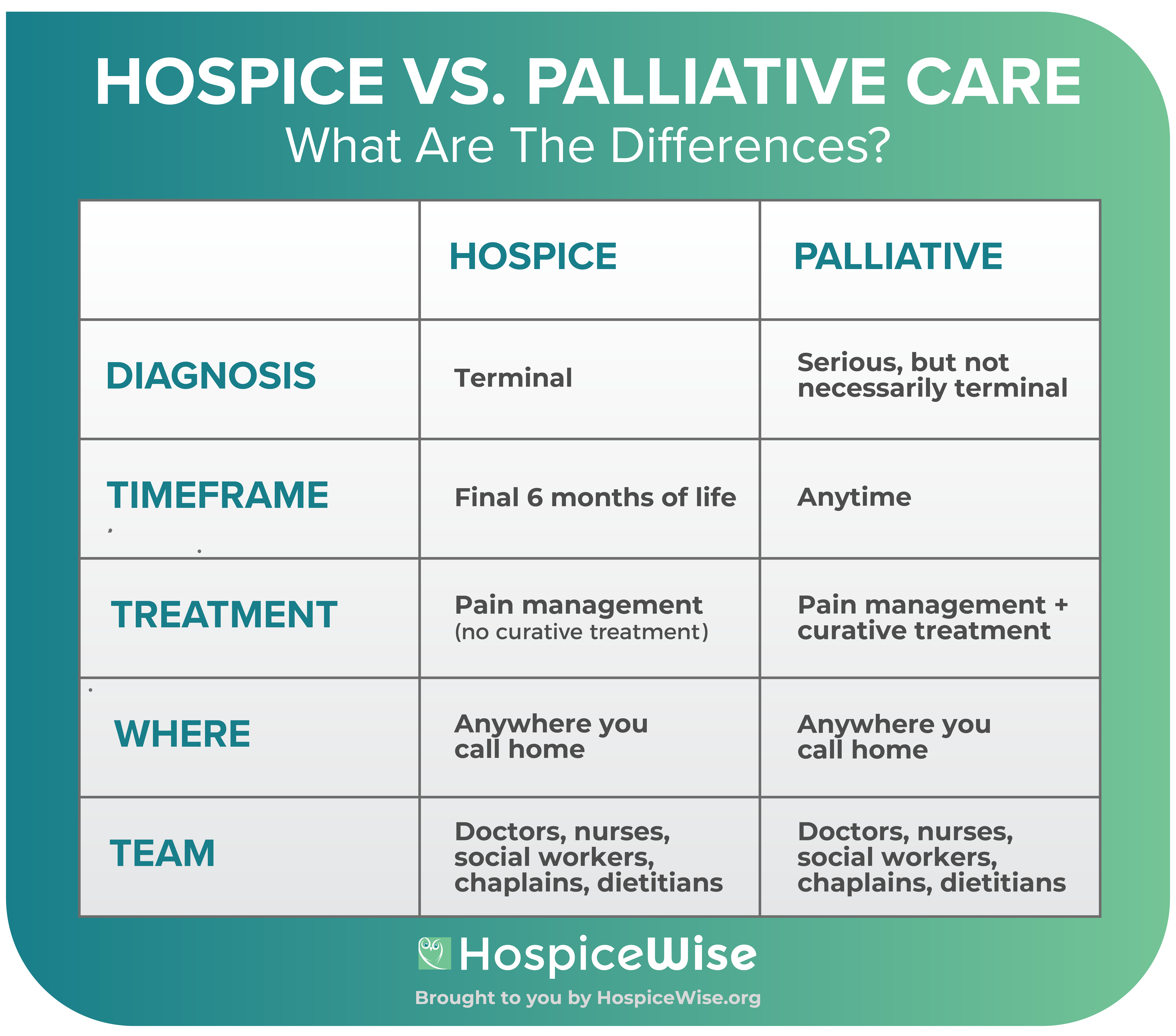

From a financial planning perspective, the primary requirement for hospice is a physician’s certification that the patient has a life expectancy of six months or less, provided the disease runs its normal course. This is not just a medical prognosis; it is a financial gatekeeper. Once this certification is documented, the patient “elects” the hospice benefit. In doing so, they waive the right to traditional Medicare coverage for treatments intended to cure their terminal illness. For the family budget, this represents a pivot from high-cost, high-deductible curative interventions (like chemotherapy or experimental surgeries) to a fully covered comfort-care model.

Coverage Specifics: Medications, Equipment, and Nursing

One of the most significant financial reliefs for families on hospice is the comprehensive nature of the coverage. Under the Medicare Hospice Benefit, almost all costs related to the terminal diagnosis are covered at 100%, with little to no out-of-pocket expense. This includes:

- Durable Medical Equipment (DME): Hospital beds, oxygen concentrators, and wheelchairs are delivered to the home at no cost to the family.

- Medications: Drugs for pain management and symptom control related to the terminal illness are typically covered with a small co-pay (often no more than $5).

- The Interdisciplinary Team: The cost of nurses, social workers, home health aides, and spiritual counselors is bundled into the daily rate paid to the hospice provider, meaning the family does not receive separate bills for these professional services.

Comparing Costs: Hospice vs. Traditional Hospitalization

When managing the finances of a terminal illness, the “cost of care” can vary wildly depending on the setting. Traditional acute care in a hospital setting is one of the most expensive ways to manage the end of life, often draining a family’s savings through co-insurance and unmet deductibles.

The Cost-Saving Nature of Palliative Care

Studies consistently show that hospice care reduces overall healthcare spending. For the individual, the financial benefit is found in the avoidance of the “ICU cycle.” A single day in an Intensive Care Unit can cost upwards of $10,000, much of which may fall on the patient if they have already exhausted certain Medicare benefit periods. Hospice, by contrast, focuses on stabilizing the patient in their place of residence. By preventing 911 calls and emergency room visits, hospice acts as a financial buffer, preserving the patient’s remaining assets for their heirs rather than liquidating them to pay hospital collections.

Out-of-Pocket Expenses and Room & Board Considerations

While the medical care in hospice is largely covered, there is a major “money trap” that families must be aware of: Room and Board. It is a common misconception that “being on hospice” means Medicare pays for a nursing home. In reality, while Medicare pays for the hospice services provided within a facility, it does not pay for the rent of the room in a skilled nursing facility or assisted living center. Families must plan for these costs, which can range from $5,000 to $12,000 per month, often requiring the utilization of long-term care insurance or Medicaid “spend-down” strategies.

Financial Planning and Asset Management During Hospice

Being on hospice provides a unique, albeit somber, “planning window.” Because the patient is no longer seeking aggressive, unpredictable treatments, the family can gain a clearer view of the financial runway ahead. This period is critical for finalizing the transition of wealth and ensuring that all financial instruments are aligned.

Activating Long-Term Care Insurance

If the patient has a private Long-Term Care (LTC) insurance policy, the move to hospice is usually the “triggering event” for benefits. Most LTC policies require that the patient needs help with “Activities of Daily Living” (ADLs) or has a terminal illness. Families should immediately file a claim once hospice begins. These daily stipends can be used to hire additional private-duty caregivers, covering the gaps that the standard Medicare hospice benefit does not provide, such as 24/7 bedside monitoring.

Estate Planning and Power of Attorney: Financial Safeguards

The hospice period is often the final opportunity to ensure that the Financial Power of Attorney (POA) is active and recognized by banking institutions. In this stage, the financial focus shifts to:

- Beneficiary Audits: Ensuring that “Transfer on Death” (TOD) or “Payable on Death” (POD) designations are correct on all bank accounts and retirement funds to avoid the costly and time-consuming probate process.

- Liquidity Management: Ensuring that the surviving spouse or heirs have access to enough liquid cash to cover immediate funeral expenses and estate taxes without having to sell assets in a “fire sale.”

- Gifting Strategies: Depending on the size of the estate, financial advisors may recommend utilizing the annual gift tax exclusion to move assets out of the taxable estate while the patient is still living.

The Business of Care: Choosing Between Non-Profit and For-Profit Providers

The hospice industry has seen a massive influx of private equity and venture capital over the last decade. As a consumer and a financial decision-maker for a loved one, it is vital to understand that not all hospice agencies operate with the same fiscal philosophy.

Evaluating Transparency and Quality Metrics

When choosing a provider, families should look at the “Business of Care” metrics. For-profit hospices, while often efficient, are sometimes scrutinized for their “live discharge” rates or for providing fewer nursing visits to maximize their profit margins from the Medicare per-diem rate. Non-profit hospices, conversely, may reinvest their surpluses into “charity care” for patients who don’t have insurance. From a financial perspective, the best choice is a provider that offers “General Inpatient Care” (GIP) at a dedicated facility, as this provides a higher tier of Medicare-covered care during a crisis without additional cost to the family.

Impact on Family Wealth and Legacy

The decision of which hospice to use can indirectly impact family wealth. A high-quality hospice provider will have an robust social work department that assists with Medicaid applications and Veterans Affairs (VA) benefits. For a veteran, being on hospice can unlock “Aid and Attendance” benefits, which provide an additional monthly pension to help pay for home care. Utilizing these “hidden” financial resources is a key part of an intelligent end-of-life financial strategy.

Summary: The Bottom Line of Hospice

Ultimately, being on hospice means transitioning into a highly regulated, federally funded healthcare niche designed to prioritize comfort over cure. From a money management perspective, it is a period of “de-escalation” in medical spending and “acceleration” in estate planning.

By understanding that hospice is a comprehensive insurance benefit, families can stop the hemorrhaging of funds associated with chronic hospitalizations and focus their financial resources on legacy preservation. While the emotional toll of hospice is great, the financial structure of the benefit is designed to provide a “safety net,” ensuring that the cost of dying does not become a catastrophic burden for those who are left behind. Understanding these financial levers allows for a more stable, secure, and dignified transition for the entire family unit.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.