In the modern economic landscape, a business is only as strong as its ability to move goods and services into the hands of paying customers. While many entrepreneurs focus heavily on product development or marketing aesthetics, the most successful organizations prioritize the financial architecture of their distribution. This brings us to the concept of sales channels. At its core, a sales channel is the path through which a company generates revenue and manages its cash flow.

From a financial perspective, choosing the right sales channels is not merely a logistical decision; it is a capital allocation strategy. Every channel carries a different cost structure, a different margin profile, and a different impact on the company’s bottom line. Understanding these nuances is essential for any business owner, investor, or financial analyst looking to maximize profitability and ensure long-term fiscal health.

The Financial Architecture of Sales Channels

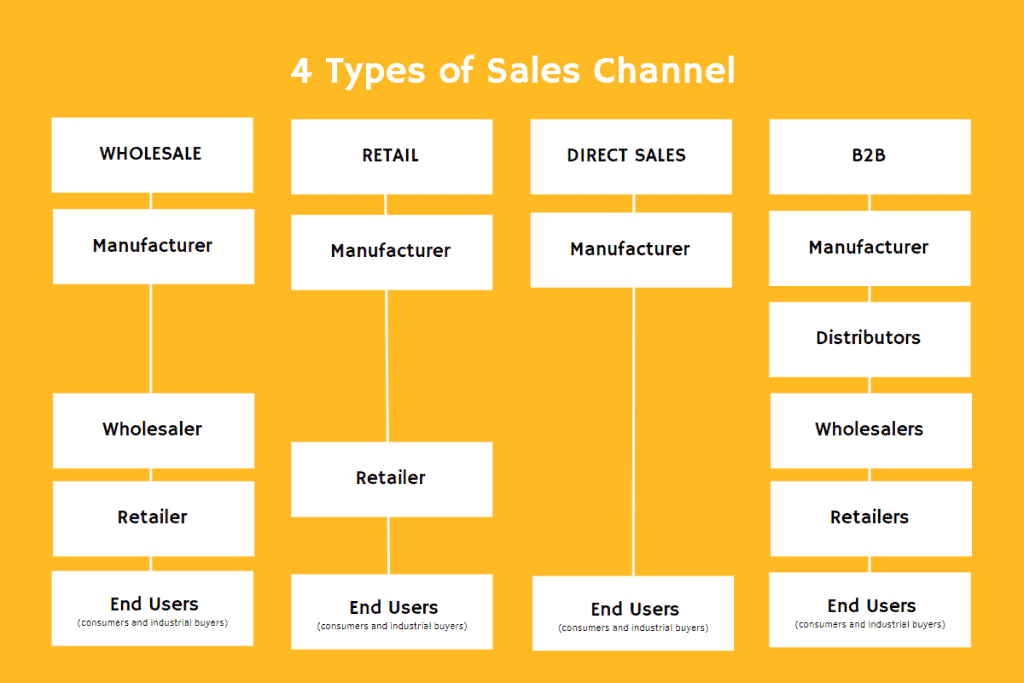

To understand sales channels through the lens of business finance, one must view them as the primary engines of liquidity. A sales channel is the method by which a business delivers value to its customers and receives payment in return. These channels are generally categorized into two main frameworks: direct and indirect. The choice between these frameworks dictates the company’s operating margins and its overall financial risk profile.

Direct vs. Indirect: Impact on Profit Margins

Direct sales channels involve the company selling directly to the end consumer without intermediaries. Common examples include a brand’s own e-commerce website, corporate-owned retail stores, or a direct-to-consumer (DTC) sales force. The primary financial advantage of a direct channel is the retention of the full retail margin. Because there are no wholesalers or retailers taking a “cut” of the transaction, the business captures the maximum possible revenue per unit sold.

Conversely, indirect sales channels involve third parties, such as distributors, brokers, or retail partners. While these intermediaries take a percentage of the sale—thereby reducing the unit margin—they often provide the financial benefit of scale. For a business looking to maximize total net profit rather than just unit margin, indirect channels can offer a lower cost of entry into new markets, leveraging the existing infrastructure of partners to drive high-volume revenue.

Cost of Goods Sold (COGS) and Channel Overhead

When analyzing the financial viability of a sales channel, one must look beyond the top-line revenue. Each channel carries specific overhead costs that must be factored into the Net Profit Margin. Direct channels often require significant upfront capital expenditure (CapEx) for physical locations or heavy investment in digital infrastructure and customer acquisition costs (CAC).

Indirect channels, while sacrificing margin, often shift some of the operational costs—such as storage, logistics, and last-mile delivery—to the partner. From a financial management standpoint, this can improve a company’s “asset-light” profile, allowing it to maintain higher liquidity by avoiding the heavy overhead associated with managing a massive logistics network.

Direct-to-Consumer (DTC) and High-Margin Revenue

The rise of the digital economy has revolutionized the “Money” aspect of sales channels by making Direct-to-Consumer (DTC) models more accessible. For a business, the DTC model is the ultimate strategy for high-margin revenue. By bypassing the “middleman,” companies can reclaim 30% to 50% of the retail price that would otherwise be lost to third-party markups.

Retaining Capital through Owned Platforms

Owned platforms—such as a proprietary Shopify store or a custom-built B2B portal—allow a business to keep its capital “in-house.” Beyond the immediate profit margin, the financial value of an owned channel lies in data ownership. In modern finance, data is an asset. By selling directly, a company gathers first-party data on consumer behavior, which allows for more efficient financial forecasting and inventory management. This reduces the risk of overproduction and “dead stock,” which are common drains on corporate liquidity.

Furthermore, owned platforms facilitate “Up-selling” and “Cross-selling” strategies that are often impossible in a third-party retail environment. This increases the Average Order Value (AOV), directly boosting the company’s cash flow without a proportional increase in marketing spend.

Managing Customer Acquisition Costs (CAC)

While DTC channels offer high margins, they come with a significant financial challenge: the cost of driving traffic. In the world of online income and business finance, the Customer Acquisition Cost (CAC) is a critical metric. If the cost to acquire a customer through digital advertising exceeds the profit generated from that customer’s first purchase, the sales channel may be unsustainable in the short term.

Smart financial planning requires a deep dive into the “LTV to CAC” ratio (Lifetime Value to Customer Acquisition Cost). A healthy business usually aims for an LTV that is at least three times the CAC. If a direct sales channel cannot achieve this ratio, it may be more financially sound to pivot toward a wholesale or marketplace model where the partner bears the burden of attracting the customer.

Leveraging Third-Party Marketplaces for Scalable Income

For many businesses, especially those in the “side hustle” or “online income” phase, third-party marketplaces like Amazon, eBay, or Walmart.com are the most effective sales channels for generating immediate cash flow. These platforms offer a ready-made audience, which can drastically reduce the initial financial risk of launching a product.

The Trade-off: Volume vs. Unit Profitability

The financial reality of third-party marketplaces is one of high volume and lower unit profitability. These platforms typically charge referral fees (often 8% to 15%) and fulfillment fees if the business uses the platform’s logistics (like Fulfillment by Amazon).

From a financial strategy perspective, the goal here is “Inventory Turnover.” Even if the margin per unit is lower than on a direct website, if the marketplace allows the business to sell 10 times more units, the total gross profit will be significantly higher. This rapid turnover is essential for maintaining healthy working capital, allowing the business to reinvest in more inventory and scale operations faster.

Commission Structures and Financial Risks

When utilizing indirect channels or marketplaces, a business must be wary of “Platform Risk.” This is a financial risk where a change in the platform’s commission structure or search algorithm can instantly evaporate profit margins. Diversifying sales channels is, therefore, a fundamental principle of financial risk management. Relying on a single marketplace for 100% of revenue is a precarious position; a balanced financial portfolio of sales channels includes both high-volume marketplaces and high-margin direct sites.

Modern B2B and Digital Monetization Strategies

Sales channels are not limited to physical products. In the realm of software, services, and digital products, the channels used to move “value” have unique financial implications, particularly regarding recurring revenue and passive income.

Affiliate and Referral Networks as Low-Risk Side Hustles

Affiliate marketing is a unique sales channel where the “product creator” pays a commission to “partners” only when a sale is made. For the product creator, this is an incredibly efficient financial model because it represents a “Pay-for-Performance” marketing cost. There is no upfront financial risk; marketing expenses are only incurred after revenue is secured.

For the affiliate (the person or business promoting the product), this serves as a potent “side hustle” or online income stream. It requires minimal capital investment, as the affiliate does not need to manufacture products or handle customer service. The financial focus here is on “Return on Effort” and “Conversion Rates.”

Subscription Models and Recurring Revenue Streams

Perhaps the most sought-after sales channel in modern finance is the subscription model (SaaS or recurring service). From a valuation perspective, a business with recurring revenue is worth significantly more than a business with one-off sales. This is because subscription channels provide “Revenue Predictability.”

Predictable cash flow allows a business to take on strategic debt for expansion, as lenders and investors view recurring revenue as a lower-risk profile. When analyzing the finance of sales channels, the transition from transactional sales to subscription-based channels is often the key to unlocking massive corporate valuation.

Financial Analysis and Channel Optimization

To truly master sales channels, a business must move beyond simply “making sales” and begin “optimizing returns.” This requires a rigorous analytical approach to every dollar spent and earned across various platforms.

Calculating Return on Ad Spend (ROAS) per Channel

Not all revenue is created equal. A $10,000 sale on a high-commission marketplace might actually net less profit than a $7,000 sale on a direct website. Financial managers must calculate the Return on Ad Spend (ROAS) and the Contribution Margin for each specific channel.

This involves subtracting all variable costs (shipping, commissions, packaging, and advertising) from the gross revenue of that channel. By comparing the “Channel Contribution Margin,” a business can identify which channels are actually “profit centers” and which are merely “vanity metrics” that drive top-line growth without adding to the bottom line.

Scaling Financial Growth through Multi-Channel Diversification

The ultimate goal of sales channel strategy in business finance is diversification. Just as an investor would not put all their money into a single stock, a robust business should not rely on a single sales channel. Multi-channel selling spreads the financial risk.

If one channel experiences a downturn—perhaps due to a retail recession or a digital advertising price hike—other channels can provide the necessary liquidity to keep the business operational. Furthermore, a multi-channel approach allows a business to capture different customer segments with different “Price Elasticities,” maximizing the total addressable market and the overall financial health of the enterprise.

In conclusion, sales channels are the lifeblood of business finance. By strategically selecting between direct and indirect models, managing acquisition costs, and diversifying revenue streams, a business can transform its sales operations into a powerful engine for capital growth and long-term financial stability. Whether you are running a small side hustle or a large corporation, the way you choose to sell is the most important financial decision you will make.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.