In the world of personal finance and wealth management, we often speak of risk in terms of market volatility, inflation, and asset allocation. However, one of the most significant, yet overlooked, liabilities on a woman’s personal balance sheet is her health profile. Specifically, understanding what is considered high cholesterol for a woman is no longer just a medical inquiry; it is a fundamental component of long-term financial planning.

Cardiovascular health serves as a primary indicator for insurance underwriters, a predictor of future healthcare expenditures, and a factor in career longevity. When a woman’s total cholesterol exceeds the 200 mg/dL threshold, it triggers a cascade of financial consequences that can alter her retirement trajectory. This article examines high cholesterol not through the lens of biology, but through the lens of money, risk management, and capital preservation.

The Actuarial Threshold: Understanding High Cholesterol Through the Lens of Risk Assessment

To a physician, high cholesterol is a precursor to heart disease. To a financial actuary, it is a data point that suggests a higher probability of a premature claim. For a woman, the definition of “high” cholesterol shifts with age, particularly during the transition into menopause, which significantly alters her risk profile in the eyes of financial institutions.

Clinical vs. Financial Markers

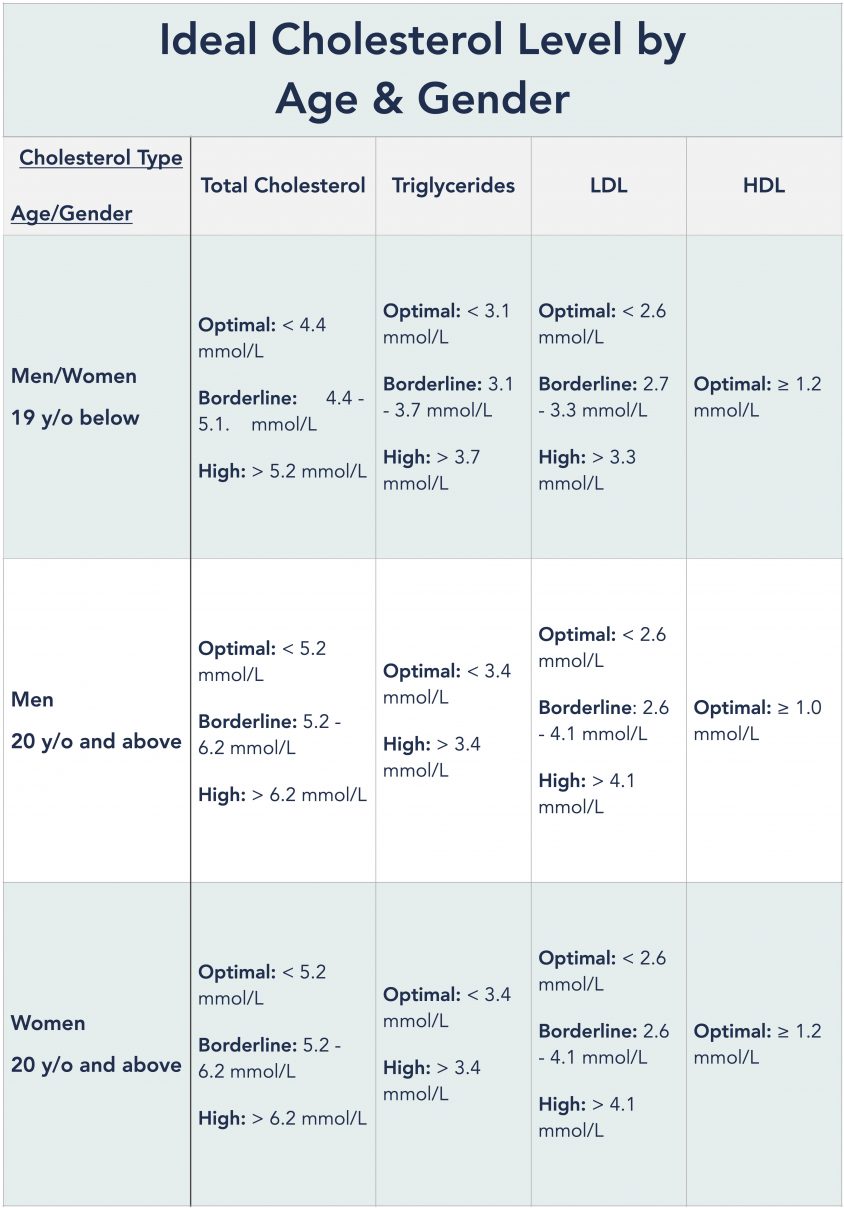

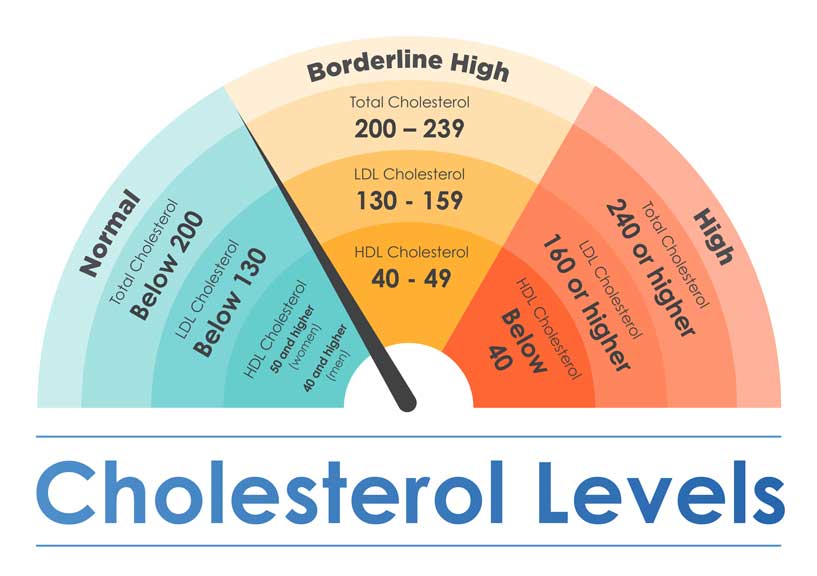

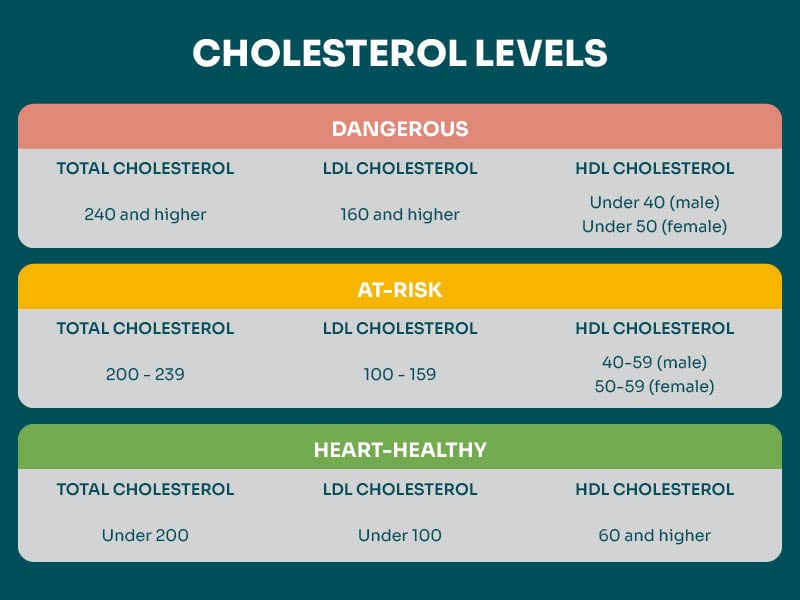

Generally, a total cholesterol level below 200 mg/dL is considered “desirable.” Once a woman’s levels reach 200–239 mg/dL, she is categorized as “borderline high,” and anything 240 mg/dL or above is “high.” From a financial perspective, these numbers represent risk tiers. Staying in the “desirable” range is equivalent to maintaining a high credit score; it signals to insurers and lenders that you are a low-risk client, deserving of the best rates. When those numbers climb, your “human capital” depreciates because the likelihood of medical intervention increases.

Why Women Face Unique Financial Risks

Women’s cholesterol levels often fluctuate more than men’s due to hormonal changes. During pregnancy or menopause, LDL (the “bad” cholesterol) can spike. If a woman is applying for a significant financial product—such as a million-dollar life insurance policy—during these windows, a “high” reading can lead to a “rated” policy. A rated policy carries higher premiums, which, over a 30-year term, can cost tens of thousands of dollars in lost opportunity costs that could have otherwise been invested in a brokerage account.

The Direct Impact on Insurance Premiums and Financial Planning

When we discuss personal finance, we focus on the “four pillars”: earning, saving, investing, and protecting. High cholesterol directly attacks the “protecting” pillar. Insurance is the mechanism by which we hedge against catastrophe, but the cost of that hedge is determined by our health metrics.

Life Insurance Underwriting Tiers

Life insurance companies categorize applicants into tiers: Super Preferred, Preferred, Standard Plus, and Standard. For a woman, a total cholesterol reading of 240 mg/dL might move her from “Super Preferred” to “Standard.”

- The Cost Delta: A 45-year-old woman in excellent health might pay $100 a month for a 20-year term policy.

- The Cholesterol Penalty: If her cholesterol is high enough to drop her two tiers, that premium could jump to $165.

- The Compound Loss: That $65 difference, if invested in an S&P 500 index fund at a 7% annual return, would grow to approximately $34,000 over 20 years. In this context, high cholesterol isn’t just a health stat; it’s a $34,000 wealth tax.

Disability Insurance and Income Protection

For high-earning female professionals, their greatest asset is their ability to earn an income. High cholesterol is often linked with secondary conditions like hypertension or metabolic syndrome, which can complicate the acquisition of long-term disability insurance. If a woman is deemed a higher risk for a cardiovascular event, her “own-occupation” disability premiums will be significantly higher, or she may face exclusions. Protecting your income becomes more expensive the moment your cholesterol crosses the high threshold.

The Hidden Costs of Management: Budgeting for Chronic Cardiovascular Health

Managing high cholesterol is a line item in a household budget that many fail to account for until it becomes a necessity. These costs are not merely the price of a co-pay; they represent a diversion of capital from productive assets to maintenance expenses.

Out-of-Pocket Expenses and Health Savings Accounts (HSAs)

Even with robust insurance, the costs of managing high cholesterol—statins, regular lipid panels, specialist consultations with cardiologists, and potentially more advanced testing like a Calcium Score or a CIMT—add up. For a woman in her 50s, these costs might consume a significant portion of her annual HSA contributions. While HSAs are excellent tax-advantaged investment vehicles, using them to pay for chronic condition management instead of letting the funds grow for retirement is a strategic disadvantage.

The Opportunity Cost of Poor Health

The most significant “money” aspect of high cholesterol is the opportunity cost of time and productivity. Heart disease remains the leading cause of death for women, but even non-fatal cardiovascular issues lead to absenteeism and “presenteeism” (being at work but not fully productive). For entrepreneurs and freelancers, a day lost to a medical appointment or fatigue is a direct hit to the top-line revenue. By maintaining “desirable” cholesterol levels, a woman is essentially performing a “preventive maintenance” routine on her most valuable revenue-generating machine: herself.

Investing in Longevity: The ROI of Preventive Health in Your 40s and 50s

In finance, we often talk about the “Return on Investment” (ROI). The ROI of maintaining healthy cholesterol levels is among the highest available in the market. It is a form of “defensive investing” that protects your principal (your life) and your dividends (your future earnings).

Hedging Against Long-Term Care Costs

One of the greatest threats to a woman’s retirement nest egg is the cost of long-term care (LTC). Cardiovascular health is a major determinant of whether a woman will need assisted living or nursing care in her 80s. High cholesterol in one’s 40s and 50s is a leading indicator of vascular dementia and stroke risk later in life. By aggressively managing cholesterol today, a woman is effectively hedging against the $100,000-per-year costs of a private nursing home room in the future.

Health as a Non-Correlated Asset

The stock market may crash, and real estate may slump, but your physical health is a non-correlated asset. It provides value regardless of what the Federal Reserve does with interest rates. A woman who understands that “high cholesterol” is a financial red flag can take steps—through diet, exercise, or early medical intervention—to “buy back” her health. This “buyback” is similar to a company repurchasing its own shares; it increases the value of the remaining assets and ensures the long-term viability of the enterprise.

Conclusion: The Wealth-Health Connection

What is considered high cholesterol for a woman? Medically, it is a number on a lab report. Financially, it is a risk multiplier. It increases the cost of insurance, drains Health Savings Accounts, threatens future earning potential, and elevates the risk of catastrophic long-term care expenses.

Professional financial planning must evolve beyond spreadsheets and stock picks to include health optimization. For the modern woman, tracking her lipid profile is as vital as tracking her 401(k) balance. By treating a cholesterol reading above 200 mg/dL as a “sell signal” for her health and a “buy signal” for lifestyle intervention, she can protect her wealth and ensure that she has the vitality to enjoy it. In the final analysis, your net worth is inextricably linked to your health; you cannot maximize one while ignoring the other. High cholesterol is a liability—manage it with the same rigor you would apply to a high-interest debt, and your financial future will be much more secure.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.