In the complex ecosystem of global finance, few instruments carry as much weight or influence as the 10-year U.S. Treasury bond. Often referred to simply as the “10-year,” this debt obligation issued by the United States federal government serves as a cornerstone for everything from mortgage rates to the valuation of multi-billion dollar corporations. Whether you are a retail investor looking for a safe place to park capital or a homeowner wondering why interest rates are rising, understanding the mechanics and the signaling power of the 10-year Treasury bond is essential.

This article explores the fundamental nature of the 10-year Treasury, its role as a global economic barometer, and how it fits into a modern investment strategy.

1. The Mechanics: What Exactly is a 10-Year Treasury Bond?

At its core, a 10-year Treasury bond is a loan made by an investor to the United States government. When you purchase a bond, you are essentially acting as the lender, and the U.S. Department of the Treasury is the borrower. The government uses these funds to finance its operations, pay for infrastructure, and manage national debt.

How the Bond Functions

The 10-year Treasury is a “fixed-income” security. This means it pays a fixed rate of interest (the coupon) every six months until the bond reaches its maturity date—ten years from the date of issuance. At the end of those ten years, the government returns the original “face value” (or par value) of the bond to the investor.

Because these bonds are backed by the “full faith and credit” of the U.S. government, they are widely considered to be among the safest investments in the world. The risk of the U.S. government defaulting on its debt is historically perceived as near-zero, which is why the interest rate on these bonds is often referred to as the “risk-free rate of return.”

The Auction Process and the Secondary Market

Treasury bonds are initially sold through a competitive auction process managed by the Treasury Department. Large institutional investors, such as central banks, pension funds, and insurance companies, participate in these auctions to determine the initial yield.

However, once issued, these bonds don’t just sit in a vault. They are traded daily on the secondary market. This is where the price of the bond can fluctuate based on supply and demand, changes in economic outlook, and shifts in Federal Reserve policy.

Yield vs. Price: The Inverse Relationship

Understanding the 10-year Treasury requires grasping the inverse relationship between bond prices and yields. When demand for bonds is high, prices go up, but the yield (the effective return on investment) goes down. Conversely, when investors sell off bonds, prices drop, and yields rise. This mathematical reality is a critical component of how bond markets respond to news and economic data.

2. The “North Star” of Finance: Why the 10-Year Yield Matters

The 10-year Treasury yield is more than just a return for bondholders; it is the “North Star” that guides the pricing of almost all other debt products in the economy. Because it is viewed as the benchmark for long-term interest rates, its movement triggers a ripple effect across the entire financial landscape.

Impact on Mortgage Rates and Consumer Loans

If you have ever wondered why mortgage rates suddenly jumped even if the Federal Reserve didn’t move its short-term rates, the answer usually lies with the 10-year Treasury. Lenders typically price 30-year fixed-rate mortgages based on a “spread” above the 10-year Treasury yield. When the yield on the 10-year rises, the cost of borrowing for home buyers almost always follows suit. The same principle applies to auto loans, student loans, and corporate credit.

The Correlation with the Stock Market

For equity investors, the 10-year yield is a crucial metric for valuation. Financial analysts use the “risk-free rate” (the 10-year yield) to discount future corporate earnings back to their present value. When the 10-year yield is low, future earnings are worth more today, which often boosts stock prices—particularly in the tech and growth sectors.

When the 10-year yield rises, the “discount rate” increases, making future earnings less valuable in today’s dollars. Additionally, as bond yields rise, they become more attractive alternatives to stocks, leading some investors to move capital out of the volatile equity market and into the safety of fixed income.

A Mirror of Inflation Expectations

The 10-year Treasury is also a sensitive gauge for inflation. Bondholders are wary of inflation because it erodes the purchasing power of the fixed interest payments they receive. If investors expect inflation to rise over the next decade, they will demand a higher yield to compensate for that risk. Therefore, a rising 10-year yield is often a sign that the market expects higher inflation or stronger economic growth ahead.

3. Investing in 10-Year Treasuries: Weighing Risks and Rewards

While the 10-year Treasury is “risk-free” in terms of default, it is not without risk. Smart investing requires understanding the trade-offs involved in holding government debt.

Interest Rate Risk

The primary risk for a bondholder is interest rate risk. If you buy a 10-year bond today with a 4% yield and interest rates in the general economy rise to 5% next year, your bond becomes less valuable. If you need to sell your bond before the ten years are up, you will have to sell it at a discount because new investors would rather buy the new bonds paying 5%. This is why bond prices fall when interest rates rise.

Inflation Risk and Real Returns

Another critical consideration is the “real yield.” This is the nominal interest rate minus the rate of inflation. If a 10-year bond pays 4% but inflation is running at 5%, the investor is actually losing 1% of their purchasing power every year. For long-term investors, the goal is to find entry points where the yield exceeds the long-term inflation outlook.

Diversification and Capital Preservation

Despite these risks, the 10-year Treasury remains a vital tool for capital preservation. During periods of extreme stock market volatility or economic recession, investors often engage in a “flight to quality.” They sell risky assets and buy Treasuries. This surge in demand drives bond prices up, providing a “cushion” for a diversified portfolio. This is the logic behind the classic 60/40 portfolio (60% stocks, 40% bonds), where the bond portion acts as a stabilizer.

4. Strategic Approaches: How to Incorporate the 10-Year into a Portfolio

Modern investors have several ways to gain exposure to the 10-year Treasury, ranging from direct ownership to liquid exchange-traded funds (ETFs).

Buying Directly via TreasuryDirect

The most straightforward way to invest is through the U.S. government’s website, TreasuryDirect.gov. Here, individuals can buy bonds at auction without paying a fee to a broker. This is an excellent option for those who plan to hold the bond for the full ten years and want to ensure they receive the exact yield offered at the time of purchase.

Treasury ETFs and Mutual Funds

For those who prefer liquidity and the ability to trade intraday, Treasury ETFs are a popular choice. Funds like the iShares 7-10 Year Treasury Bond ETF (IEF) track the performance of 10-year notes. These funds provide a way to bet on the direction of interest rates or to hedge a stock-heavy portfolio without the complexity of managing individual bond maturities.

Understanding the Yield Curve

Sophisticated investors also monitor the “yield curve”—a graph that plots the interest rates of Treasuries with different maturity dates (from 1 month to 30 years). Usually, longer-term bonds like the 10-year pay more than short-term bonds because investors demand more compensation for locking their money away for longer.

However, when the 10-year yield falls below short-term yields (like the 2-year note), it is known as a “yield curve inversion.” Historically, an inverted yield curve has been one of the most reliable predictors of an impending economic recession, making the 10-year yield a critical watch-point for anyone managing a business or a retirement fund.

5. The Global Perspective: A Safe Haven in an Uncertain World

Finally, it is important to recognize that the 10-year Treasury is a global asset. It is held in massive quantities by foreign governments, most notably China and Japan, as part of their foreign exchange reserves.

The Role of the Federal Reserve

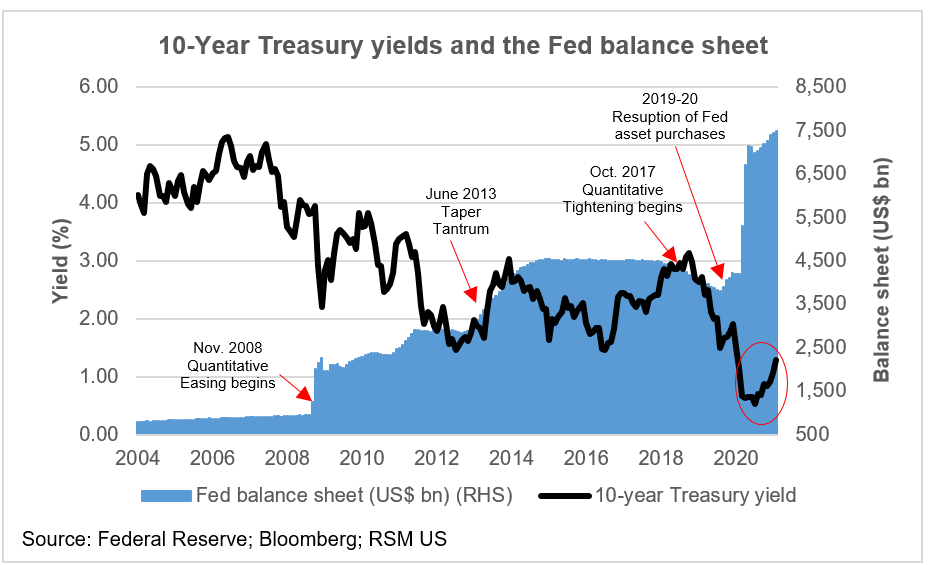

The Federal Reserve, the central bank of the United States, uses the 10-year Treasury as a tool for monetary policy. While the Fed directly sets short-term rates, it can influence the 10-year yield through “Quantitative Easing” (buying bonds to lower yields and stimulate the economy) or “Quantitative Tightening” (selling bonds or letting them mature to raise yields and cool inflation).

The Dollar’s Dominance

The 10-year Treasury also supports the status of the U.S. dollar as the world’s reserve currency. Because there is a deep, liquid, and transparent market for 10-year Treasuries, global investors always have a place to store “excess” dollars. This demand helps the U.S. fund its budget deficits at lower rates than most other nations could ever achieve.

Conclusion

The 10-year Treasury bond is far more than a simple debt instrument; it is the foundational pulse of the global economy. By understanding how its yield is calculated, why it influences consumer borrowing, and how it reacts to inflation and Fed policy, investors can make more informed decisions. Whether you are seeking the safety of a guaranteed return or trying to time your next real estate purchase, keeping an eye on the 10-year Treasury is perhaps the single most important habit for anyone navigating the world of personal and business finance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.