In the landscape of modern personal finance, few tools are as potent or as frequently misunderstood as the Roth contribution. Named after Senator William Roth, who championed the Taxpayer Relief Act of 1997, Roth accounts fundamentally changed how Americans save for the future. While traditional retirement contributions offer an immediate tax break, Roth contributions operate on a “pay now, play later” philosophy. By contributing after-tax dollars today, investors secure a future where every penny of growth and every dollar of withdrawal is entirely shielded from the Internal Revenue Service (IRS).

Understanding Roth contributions is not merely a matter of knowing where to click in your payroll portal; it is a strategic decision that can result in hundreds of thousands of dollars in tax savings over a lifetime. This guide explores the mechanics, the legal frameworks, and the strategic advantages of prioritizing Roth contributions in your financial portfolio.

The Fundamental Mechanics of Roth Contributions

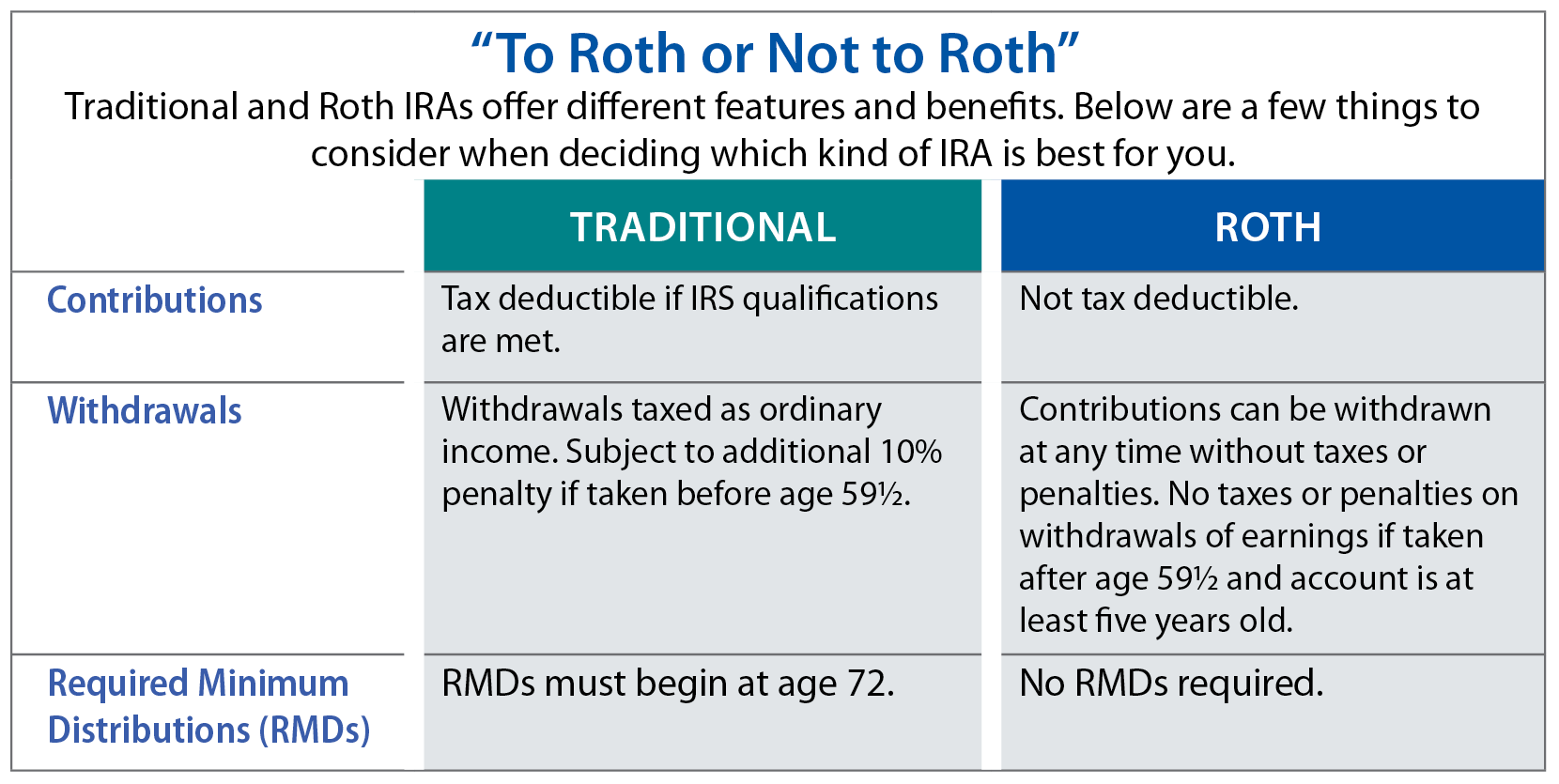

The defining characteristic of a Roth contribution is its tax treatment. Unlike traditional contributions, which are “pre-tax” and reduce your taxable income in the year you make them, Roth contributions are “after-tax.” This means the money goes into your investment account after you have already paid federal and state income taxes on your earnings.

The Principle of After-Tax Funding

When you elect to make a Roth contribution to a 401(k) or an IRA, you are essentially making a bet on your future self. You are choosing to settle your tax bill at your current rate rather than deferring that bill to your retirement years. For many early-to-mid-career professionals, this is a calculated move based on the assumption that their income—and the national tax rates—will likely be higher decades from now.

The Magic of Tax-Free Compound Growth

While losing the immediate tax deduction might seem like a disadvantage, the real “magic” happens inside the account. Once the money is inside a Roth vehicle, it grows tax-deferred. However, unlike a traditional account where the growth is eventually taxed as ordinary income, Roth growth becomes tax-free. If you contribute $100,000 over twenty years and it grows to $500,000 through savvy investing, that $400,000 in capital gains and dividends is yours to keep in its entirety, provided you follow the distribution rules.

Qualified vs. Non-Qualified Distributions

To maintain the tax-free status of your earnings, withdrawals must be “qualified.” Generally, this means the account holder must be at least 59½ years old, and the account must have been open for at least five years. One of the most flexible features of Roth IRAs, specifically, is that you can withdraw your contributions (the original money you put in) at any time, for any reason, without taxes or penalties. It is only the earnings that are subject to the 59½ rule.

Types of Roth Vehicles: IRA vs. Employer-Sponsored Plans

Not all Roth contributions are created equal. Depending on your employment status and income level, you may have access to different types of accounts, each with its own set of rules and advantages.

The Roth IRA (Individual Retirement Account)

The Roth IRA is a self-directed account that you open through a brokerage. It offers the most significant amount of control, allowing you to invest in almost any stock, bond, or mutual fund. However, it also comes with the strictest income limits. If you earn above a certain threshold, the IRS prevents you from contributing directly to a Roth IRA, forcing high-earners to look toward “Backdoor” strategies or employer-sponsored plans.

Roth 401(k) and 403(b) Plans

Many modern employers now offer a Roth option within their 401(k) or 403(b) plans. The primary advantage here is the contribution limit. While a Roth IRA is capped at a relatively low annual amount ($7,000 in 2024, or $8,000 for those 50+), a Roth 401(k) allows for much higher contributions ($23,000 in 2024, with a $7,500 catch-up). Furthermore, Roth 401(k)s do not have income “phase-outs,” meaning even a CEO earning seven figures can contribute to one if the plan allows it.

The “Backdoor” and “Mega-Backdoor” Roth Strategies

For high-income earners who are locked out of direct Roth IRA contributions, the “Backdoor Roth” provides a legal workaround. This involves contributing to a Traditional IRA (without taking a tax deduction) and immediately converting it to a Roth IRA. Some employer plans also allow for a “Mega-Backdoor Roth,” where after-tax non-Roth contributions are made to a 401(k) and then converted internally to a Roth 401(k) or rolled into a Roth IRA. These advanced maneuvers are staples of sophisticated wealth management.

Eligibility, Limits, and the “Five-Year Rule”

Navigating the world of Roth contributions requires a keen eye on the calendar and the tax code. The IRS adjusts contribution limits and income thresholds annually to account for inflation, and failing to adhere to these can result in excise taxes.

Income Thresholds and Phase-Outs

For the Roth IRA, your eligibility to contribute depends on your Modified Adjusted Gross Income (MAGI). For 2024, single filers begin to see their contribution limit reduced if they earn over $146,000, and they are completely ineligible if they earn over $161,000. For married couples filing jointly, the phase-out range is $230,000 to $240,000. It is crucial to monitor these numbers toward the end of the fiscal year to avoid over-contribution.

Annual Contribution Limits

As of 2024, the total limit for all your IRAs (Traditional and Roth combined) is $7,000 ($8,000 if 50+). For employer-sponsored Roth 401(k)s, the limit is much higher at $23,000 ($30,500 if 50+). It is important to note that these limits apply to the employee’s contributions. Employer matching contributions, historically, have always been pre-tax (Traditional), though recent legislation (the SECURE Act 2.0) has begun to allow employers to offer Roth matches if they choose.

The Five-Year Rules

There are two distinct “five-year rules” that govern Roth accounts. The first dictates that you cannot withdraw earnings tax-free until five years have passed since your first contribution to any Roth IRA. The second rule applies specifically to conversions (moving money from a Traditional IRA to a Roth). Each conversion has its own five-year clock regarding the penalty-free withdrawal of the converted principal. Understanding these nuances is vital for those planning an early retirement.

Strategic Benefits: Why Prioritize Roth Contributions?

The decision to choose a Roth contribution over a Traditional one is rarely about simple math; it’s about risk management and long-term flexibility.

Tax Diversification in Retirement

Just as you diversify your investments between stocks and bonds, you should diversify your “tax buckets.” If all your money is in a Traditional 401(k), you are 100% exposed to future tax rate increases. By having a significant portion of your wealth in a Roth account, you can control your taxable income in retirement. For example, you could withdraw $50,000 from a Traditional account (filling up the lower tax brackets) and then take another $30,000 from a Roth account tax-free, keeping your overall tax bill at a minimum.

Exemption from Required Minimum Distributions (RMDs)

One of the most significant advantages of the Roth IRA is that it does not have Required Minimum Distributions (RMDs) during the owner’s lifetime. Traditional accounts force you to start taking money out (and paying taxes) at age 73 or 75, regardless of whether you need the cash. With a Roth IRA, you can let the money sit and grow for your entire life. (Note: Under SECURE Act 2.0, Roth 401(k)s are also now exempt from RMDs starting in 2024).

Estate Planning and Generational Wealth

Roth IRAs are perhaps the single best vehicle for passing wealth to heirs. When you leave a Roth IRA to a beneficiary, they generally receive the assets tax-free. While non-spouse beneficiaries are usually required to empty the account within ten years, that decade of additional tax-free growth is a massive financial gift that Traditional IRAs simply cannot match.

Comparative Analysis: Roth vs. Traditional

The “Roth vs. Traditional” debate is the most common question in personal finance. The answer depends almost entirely on your current tax rate versus your expected tax rate in retirement.

Analyzing Your Current vs. Future Tax Bracket

The math is straightforward: if your tax rate today is lower than it will be when you retire, Roth is the winner. If your tax rate today is very high (e.g., you are in the 37% federal bracket) and you expect to be in a lower bracket in retirement, the immediate tax deduction of a Traditional contribution might be more valuable. However, many experts argue that with the current national debt levels, future tax rates across the board are more likely to rise than fall.

Flexibility and Accessibility

Roth contributions offer superior “liquidity” for a retirement account. Because you can withdraw your contributions (but not earnings) from a Roth IRA at any time without a 10% penalty, it can serve as a “back-up” emergency fund. While it is never recommended to raid retirement savings, the peace of mind that comes with knowing that money isn’t “locked away” behind a tax wall is a significant psychological benefit for many savers.

Conclusion: Making the Most of Your Contribution Strategy

Roth contributions represent a paradigm shift in how we approach long-term wealth. They require a “delayed gratification” mindset—paying the tax bill today to ensure a future of total financial sovereignty. By leveraging the high limits of Roth 401(k)s, the flexibility of Roth IRAs, and the strategic depth of conversion maneuvers, investors can build a fortress that is impervious to future tax hikes.

In a world of economic uncertainty, the Roth contribution is one of the few variables you can truly control. Whether you are just starting your career or are a high-earning professional looking to optimize your estate, prioritizing Roth contributions is a cornerstone of a sophisticated, forward-thinking financial plan. The best time to start was yesterday; the second best time is today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.