In the landscape of personal finance, few milestones carry as much weight as “Full Retirement Age” (FRA). For decades, the concept of retirement was tethered to a specific number—65—but as life expectancy has increased and economic policies have evolved, the definition of when one is “fully” retired has shifted. Understanding your Full Retirement Age is not merely a matter of knowing when you can stop working; it is a critical component of a sophisticated financial strategy that dictates the size of your monthly Social Security checks, your tax liabilities, and your long-term portfolio sustainability.

In this guide, we will explore the nuances of Full Retirement Age, the financial implications of timing your claim, and how to integrate this knowledge into a broader wealth management plan.

1. The Evolution and Mechanics of Full Retirement Age

Full Retirement Age is defined by the Social Security Administration (SSA) as the age at which an individual becomes eligible to receive 100% of their primary insurance amount (PIA). While many Americans still associate retirement with age 65, the reality for the modern workforce is quite different.

The 1983 Amendments and the Shift to Age 67

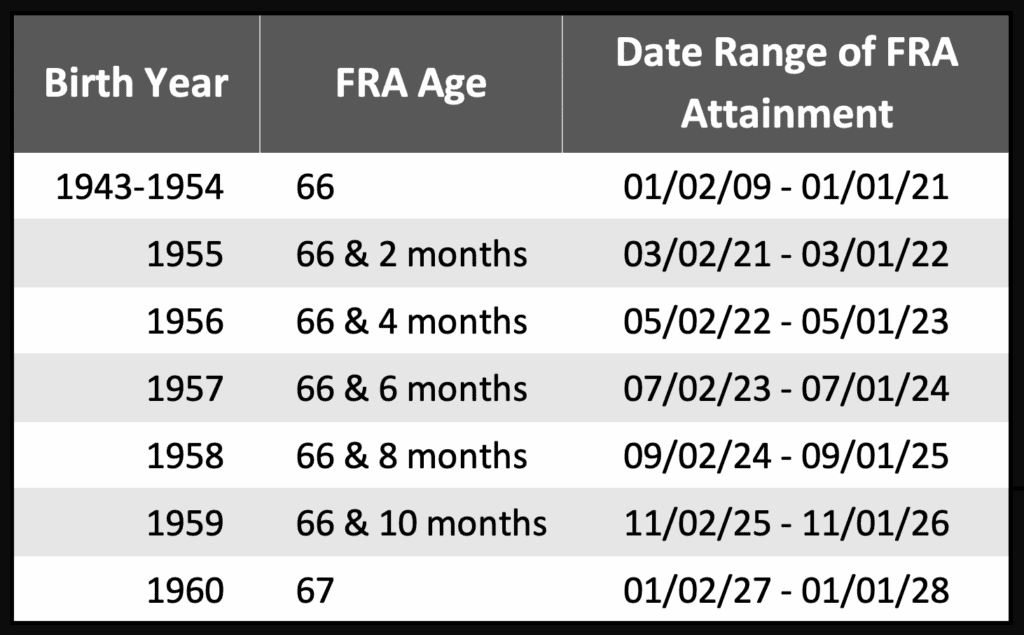

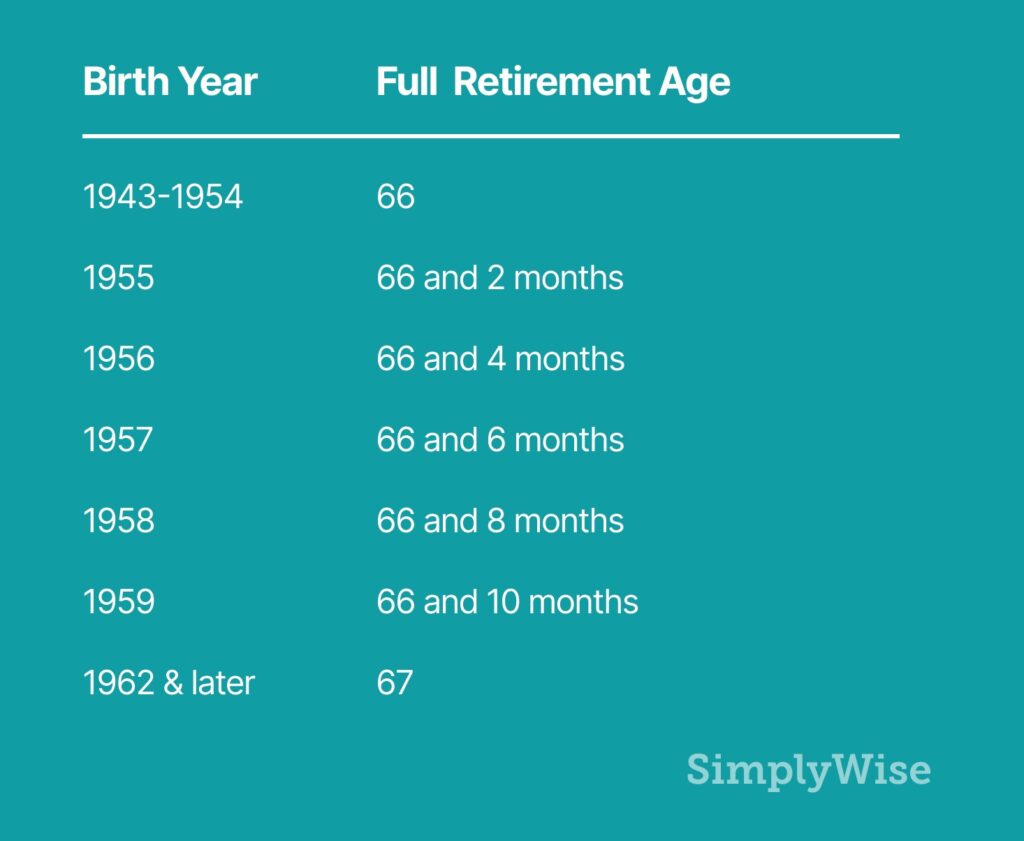

The current trajectory of FRA was set in motion by the Social Security Amendments of 1983. Faced with long-term solvency concerns, Congress mandated a gradual increase in the retirement age. For anyone born between 1943 and 1954, the FRA was established at 66. However, for those born in 1960 or later, the FRA has transitioned to 67. The years in between see a staggered increase in two-month increments. This shift reflects the actuarial reality that people are living longer and, consequently, the system must adjust to ensure it can support beneficiaries over a longer horizon.

Why the “Full” in Full Retirement Age Matters

The term “Full” is significant because it represents the baseline of your benefits. While you can technically begin receiving Social Security benefits as early as age 62, doing so results in a permanent reduction of your monthly payment. Conversely, waiting beyond your FRA allows your benefit to grow. Therefore, the FRA serves as the “neutral” point in the financial see-saw of retirement planning. It is the pivot point from which all reductions or credits are calculated.

2. The Financial Math: Reductions, Credits, and the Cost of Timing

Deciding when to claim benefits is one of the most impactful financial decisions a person will make. The difference between claiming at 62, 67, or 70 can amount to hundreds of thousands of dollars over the course of a retirement.

The Permanent Reduction of Early Claiming

If your Full Retirement Age is 67 and you choose to start receiving benefits at age 62, your monthly check will be reduced by approximately 30%. This reduction is permanent. From a personal finance perspective, this is essentially an “early withdrawal penalty” that lasts a lifetime. For those who have sufficient private savings—such as 401(k)s or IRAs—claiming early is often a sub-optimal move unless health concerns or immediate liquidity needs dictate otherwise.

The Power of Delayed Retirement Credits

On the opposite end of the spectrum is the benefit of patience. For every year you delay claiming Social Security past your Full Retirement Age (up until age 70), your benefit increases by 8% per year. This is known as a Delayed Retirement Credit. In an era of volatile market returns, an 8% guaranteed, inflation-adjusted increase is one of the best “investments” available to a retiree. By waiting until 70, an individual whose FRA is 67 can increase their monthly benefit to 124% of their primary insurance amount.

Calculating the “Break-Even” Point

A common tool in financial planning is the break-even analysis. This calculation determines the age at which the total cumulative benefits of waiting to claim (higher monthly checks) surpass the total cumulative benefits of claiming early (more checks, but smaller amounts). Generally, the break-even point for waiting until FRA versus claiming at 62 is around age 77 or 78. If you expect to live well into your 80s or 90s, the financial logic heavily favors waiting for your FRA or even until age 70.

3. Working, Taxes, and the FRA Earnings Test

One of the most misunderstood aspects of Full Retirement Age is how it interacts with earned income. Many retirees wish to continue working part-time or even full-time while collecting Social Security, but doing so before reaching FRA can trigger the Social Security “Earnings Test.”

The Earnings Test Trap

If you are under your Full Retirement Age and your earned income exceeds a certain annual limit ($22,320 in 2024), the SSA will withhold $1 in benefits for every $2 you earn above that limit. In the year you reach FRA, the rules become more lenient, and once you reach the exact month of your Full Retirement Age, the earnings test disappears entirely. You can earn an unlimited amount of money without any reduction in your Social Security benefits.

The Recalculation Benefit

It is important to note that the money withheld under the earnings test is not “lost” forever. Once you reach your Full Retirement Age, the SSA recalculates your benefit amount to account for the months in which benefits were withheld. Effectively, your monthly check increases to “pay back” those withheld funds over time. However, from a cash-flow management perspective, it is often more efficient to wait until FRA to claim if you plan on remaining in the workforce.

Taxation of Benefits

Regardless of your age, Social Security benefits may be subject to federal income tax if your “combined income” (adjusted gross income + tax-exempt interest + half of your Social Security benefits) exceeds certain thresholds. For individuals, if this total is between $25,000 and $34,000, you may pay tax on up to 50% of your benefits. Above $34,000, up to 85% of benefits may be taxable. Understanding these tax brackets is essential for high-net-worth individuals who are balancing Social Security with RMDs (Required Minimum Distributions) from retirement accounts.

4. Integrating FRA into a Holistic Wealth Strategy

Full Retirement Age should not be viewed in a vacuum. It must be synchronized with other pillars of your financial life, including healthcare and private investment accounts.

Medicare vs. Full Retirement Age

A frequent point of confusion is the difference between the Medicare eligibility age and the Social Security Full Retirement Age. Regardless of when your FRA is, Medicare eligibility begins at age 65. If you delay Social Security until 67 or 70, you must still remember to enroll in Medicare at 65 to avoid late-enrollment penalties, unless you have qualifying coverage through a current employer. This “gap” between 65 and 67 requires careful budgeting for healthcare premiums and out-of-pocket costs.

Using Private Assets to Bridge the Gap

For many investors, the optimal strategy involves using distributions from a 401(k) or brokerage account to fund the years between retirement and claiming Social Security at FRA or age 70. This “bridge strategy” allows the Social Security benefit—which is a government-backed, inflation-adjusted annuity—to grow to its maximum potential. By spending down taxable assets first, you may also reduce the size of your future RMDs, potentially lowering your tax burden in later years.

Spousal and Survivor Benefit Considerations

The Full Retirement Age also dictates the maximum amount a spouse can receive. A spousal benefit can be up to 50% of the worker’s benefit at FRA. Furthermore, for married couples, the timing of the higher-earning spouse’s claim is vital for survivor benefits. If the high-earner waits until 70 to claim, they lock in a higher base benefit that will transfer to the surviving spouse after their death. This makes the FRA and delayed claiming not just a personal choice, but a life insurance-like strategy for the household.

Conclusion: The Strategic Value of the FRA

Full Retirement Age is more than just a bureaucratic milestone; it is the cornerstone of a secure financial future. By understanding the specific age at which you are entitled to your full benefits, you gain the ability to make informed decisions about when to stop working, how to manage your tax liability, and how to maximize the lifetime value of your Social Security income.

Whether you choose to claim at your FRA, take an early reduction for immediate liquidity, or wait until age 70 for the maximum possible credit, the decision should be rooted in a deep understanding of your personal health, your investment portfolio, and your long-term income needs. In the world of money management, knowledge of the FRA is power—the power to ensure that your golden years are funded with precision and confidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.