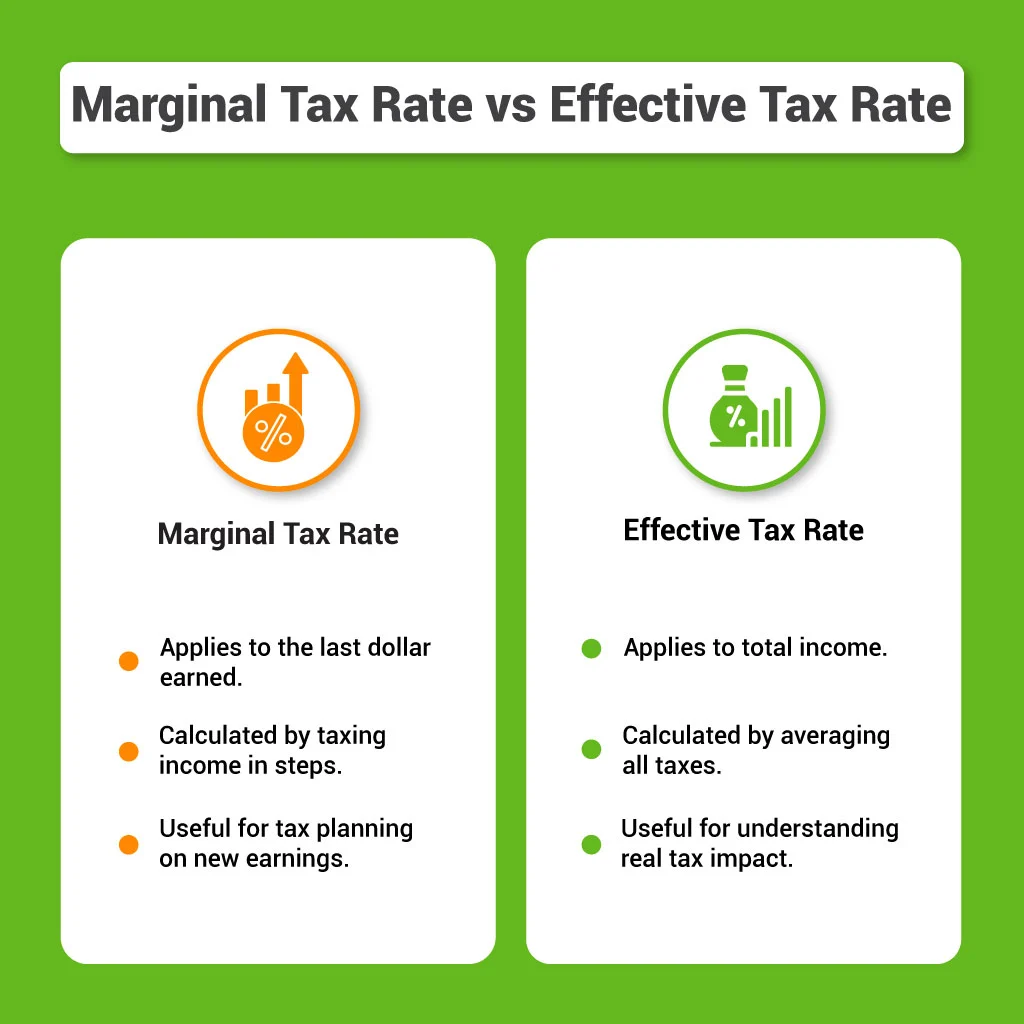

Understanding your taxes is a fundamental pillar of personal finance, yet it remains one of the most misunderstood areas for the average taxpayer. When you hear someone say, “I’m in the 24% tax bracket,” there is often a lingering fear that the government is taking nearly a quarter of every dollar they earn. However, the reality of the U.S. tax system—and many similar progressive systems worldwide—is far more layered. To master your money, you must distinguish between two critical figures: your marginal tax rate and your effective tax rate.

While the marginal rate tells you what happens to the next dollar you earn, the effective rate tells you the actual story of what happened to your total income. Distinguishing between these two is not just an academic exercise; it is a vital skill for making informed decisions regarding raises, investments, and retirement planning.

Decoding the Marginal Tax Rate: The “Next Dollar” Concept

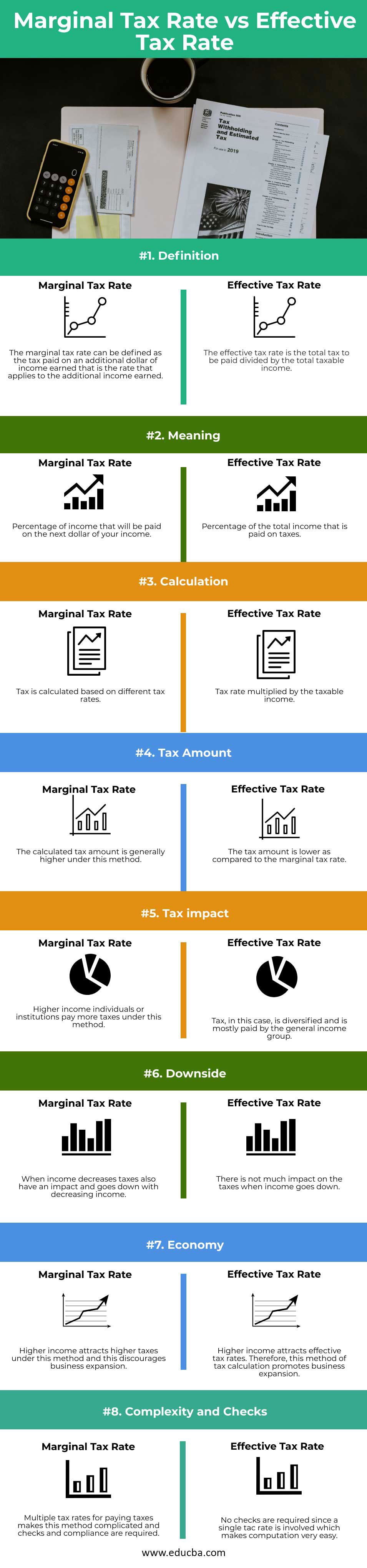

The marginal tax rate is often the figure that makes headlines and causes the most anxiety. In a progressive tax system, income is divided into segments, or “brackets,” and each segment is taxed at a different rate. Your marginal tax rate is the percentage of tax applied only to the very last dollar you earned. It represents the highest tax bracket you fall into based on your total taxable income.

How Tax Brackets Function as “Buckets”

To visualize the marginal tax rate, imagine a series of buckets. The first bucket holds a certain amount of income and is taxed at a very low rate (e.g., 10%). Once that bucket is full, any additional income spills over into the second bucket, which is taxed at a slightly higher rate (e.g., 12%). This continues through various tiers—22%, 24%, 32%, and so on.

When you say you are in the 32% bracket, it does not mean your entire income is taxed at 32%. It simply means that your final “bucket” of income reached that level. The dollars sitting in the lower buckets are still being taxed at those lower 10% and 12% rates.

The Progressive Tax Logic

The philosophy behind the marginal tax rate is “ability to pay.” The logic is that those who earn more can afford to contribute a higher percentage of their top-tier earnings toward public services without compromising their basic standard of living. This progressive structure ensures that low-income earners are protected by lower rates, while high-income earners contribute proportionally more on their surplus wealth.

Debunking the “Moving Up a Bracket” Myth

One of the most persistent myths in personal finance is that getting a raise can actually result in less take-home pay because it pushes you into a higher tax bracket. Because of the “bucket” system described above, this is mathematically impossible in a standard progressive system. Only the money above the threshold of the new bracket is taxed at the higher rate. Your previous earnings remain taxed at the lower levels. Understanding your marginal rate is essential when considering a side hustle or a promotion, as it helps you calculate exactly how much of that “new” money you will actually keep.

Understanding the Effective Tax Rate: The “Actual Burden” Concept

While the marginal tax rate focuses on the ceiling of your income, the effective tax rate looks at the whole floor. Your effective tax rate is the actual percentage of your total income that goes to the IRS after all calculations are complete. It is essentially the “blended” or “average” rate of tax you pay across all the brackets you touched.

The Calculation Formula

Calculating your effective tax rate is straightforward: divide your total tax or total tax liability by your total taxable income. For example, if you earned $100,000 and paid $15,000 in total federal income tax, your effective tax rate is 15%. This is a much more accurate reflection of your tax burden than your marginal rate, which might be 22% or 24% for that same income level.

Why Your Effective Rate is Always Lower

For almost every taxpayer, the effective tax rate will be significantly lower than their marginal tax rate. This occurs for two reasons. First, as mentioned, your income is spread across lower brackets before hitting your marginal peak. Second, the tax code allows for various “leaks” from the buckets in the form of deductions and credits.

Standard deductions, itemized deductions, and personal exemptions (where applicable) reduce your “taxable income” before the brackets are even applied. Consequently, your effective rate provides a realistic view of your contribution to the system relative to your total earnings.

The Role of Tax Credits

While deductions lower the amount of income subject to tax, tax credits are even more powerful because they provide a dollar-for-dollar reduction in the tax you owe. Credits for children, education, or energy-efficient home improvements directly lower your total tax liability, which in turn pulls your effective tax rate even further down. When evaluating your financial health, the effective rate is the metric that tells you how much of your labor is being diverted to the state.

Key Differences and Why They Matter for Financial Planning

The distinction between these two rates isn’t just semantics; it changes how you approach your financial life. Knowing which rate to use in different scenarios can prevent costly errors and help you optimize your wealth-building strategies.

Decision-Making: Investments and Side Hustles

When you are deciding whether to take on extra work, work overtime, or start a side business, you should look at your marginal tax rate. Since this is “new” money, it will be taxed at your highest current rate. If you are in the 32% bracket, you need to be comfortable knowing that nearly a third of your side hustle profits will go to taxes.

Conversely, when you are looking at your annual budget to see how much you can afford for a mortgage or a car payment, you should look at your effective tax rate. This gives you the reality of your “net” take-home pay over the course of the year.

Tax Planning vs. Tax Compliance

Tax compliance is simply paying what you owe, but tax planning is the art of legally minimizing what you owe. Effective tax planning often focuses on lowering the marginal rate by shifting income into lower-taxed vehicles. For instance, contributing to a traditional 401(k) reduces your taxable income from the “top down.” If you are in a high marginal bracket, a $10,000 contribution to a 401(k) doesn’t just save you $10,000 for retirement; it saves you $10,000 multiplied by your marginal rate in immediate tax outflows.

Impact on Investment Choices

Capital gains and dividends often have different tax structures than ordinary income. Understanding how these interact with your marginal and effective rates is crucial. For some, earning more ordinary income might push them into a higher bracket for capital gains, illustrating why a holistic view of both rates is necessary for high-net-worth individuals or those with significant brokerage accounts.

Practical Examples: A Tale of Two Taxpayers

To see these concepts in action, let’s look at two hypothetical taxpayers using simplified versions of tax brackets to illustrate the spread between marginal and effective rates.

Example 1: The Early-Career Professional

Sarah is a single filer who earns $60,000 in taxable income.

- The first $11,600 is taxed at 10% ($1,160).

- The amount from $11,601 to $47,150 is taxed at 12% ($4,266).

- The remaining $12,850 ($60,000 – $47,150) is taxed at 22% ($2,827).

Sarah’s marginal tax rate is 22%, because that is the rate applied to her last dollar. However, her total tax bill is $8,253. When we divide $8,253 by her $60,000 income, we find her effective tax rate is approximately 13.7%.

Example 2: The High-Earning Executive

Mark is a single filer who earns $250,000 in taxable income. His marginal tax rate is 35%. However, because he benefits from the large chunks of income taxed at 10%, 12%, 22%, 24%, and 32%, his total tax bill might be around $53,000 (assuming no other credits). His effective tax rate would be roughly 21.2%. Even as a high earner, his actual “blended” tax burden is much lower than the intimidating 35% marginal figure often cited in political or social discourse.

Optimizing Your Strategy: Lowering Both Rates

The ultimate goal of financial management is to keep more of what you earn. By understanding the relationship between marginal and effective rates, you can employ strategies to drive both figures down.

Maximizing Pre-Tax Retirement Contributions

The most effective way to lower your marginal rate is to reduce your taxable income. Contributing to a traditional 401(k), 403(b), or traditional IRA allows you to deduct those contributions from your gross income. If those contributions are enough to pull your total taxable income into a lower bracket, you have effectively lowered your marginal rate and, by extension, your effective rate.

Leveraging Health Savings Accounts (HSAs)

For those with high-deductible health plans, an HSA is a powerful financial tool. Contributions are 100% tax-deductible (lowering your taxable income), the growth is tax-free, and withdrawals for medical expenses are tax-free. It is one of the few “triple tax-advantaged” tools available that works directly to lower your effective tax rate.

Strategic Tax-Loss Harvesting

In the world of investing, you can use “losses” to your advantage. Tax-loss harvesting involves selling investments that are at a loss to offset gains realized in other parts of your portfolio. If your losses exceed your gains, you can even use up to $3,000 of that loss to offset your ordinary income, which directly lowers the income subject to your marginal tax rate.

Conclusion: Clarity Breeds Financial Confidence

The difference between a marginal and effective tax rate is more than just a quirk of accounting; it is the difference between fear-based financial decisions and strategy-based ones. When you realize that your marginal rate only affects your “next” dollar and your effective rate defines your “actual” burden, the tax code becomes a landscape you can navigate rather than a cage that limits you.

By focusing on strategies that lower your taxable income and maximize your credits, you can narrow the gap between what you earn and what you keep. Whether you are negotiating a salary, planning for retirement, or simply trying to understand your paycheck, keep both rates in mind. Clarity in your taxes is the first step toward true mastery of your personal finances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.