The landscape of Indian finance underwent a seismic shift on July 1, 2017, with the implementation of the Goods and Services Tax (GST). For decades, India’s indirect tax system was a labyrinth of overlapping levies, excise duties, and value-added taxes that created a “cascading effect”—essentially a tax on tax. The introduction of GST was not merely a policy change; it was a fundamental restructuring of the nation’s economic DNA. By consolidating multiple taxes into a single, streamlined framework, GST aimed to transform India into a unified common market. For individuals, investors, and business owners, understanding the nuances of GST is essential for navigating the modern financial environment of the Indian subcontinent.

1. The Financial Evolution: From Cascading Taxes to a Unified Structure

Before the dawn of GST, the Indian tax system was notoriously complex. A product manufactured in one state and sold in another was subject to Central Excise Duty, Service Tax, State VAT, Entry Tax, and Luxury Tax, among others. This fragmentation created significant financial friction, making it difficult for businesses to scale and for consumers to understand the true cost of goods.

The “One Nation, One Tax” Philosophy

The core objective of GST was to simplify this chaos under the banner of “One Nation, One Tax.” By eliminating the boundaries between state and central indirect taxes, the government aimed to reduce the overall tax burden on consumers and improve the ease of doing business. In the “Money” niche, this transition represents a shift toward transparency. When taxes are consolidated, the leakage in the financial system is minimized, and the cost of compliance for businesses—though initially high during the transition phase—settles into a more predictable pattern.

Eliminating the Cascading Effect

Perhaps the most significant financial benefit of GST is the removal of the cascading effect. In the old regime, taxes paid at the manufacturing stage were not always creditable against taxes at the retail stage. This meant that consumers were paying interest on the tax itself. GST introduced a seamless “Input Tax Credit” (ITC) mechanism. This allows businesses to claim a credit for the tax paid on inputs, ensuring that the tax is levied only on the value added at each stage of the supply chain. From a personal finance perspective, this efficiency is designed to stabilize prices and prevent the artificial inflation of goods caused by inefficient taxation.

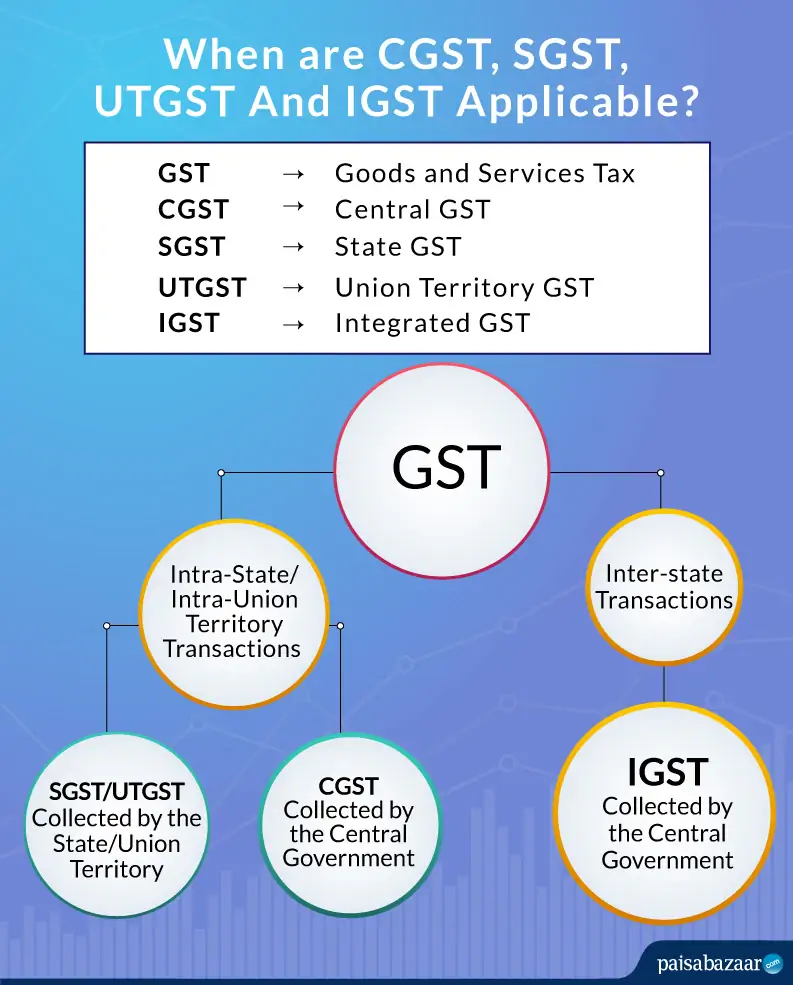

2. Deciphering the GST Components and Tax Slabs

To master the financial implications of GST, one must understand how the tax is categorized and collected. Unlike a single-point tax, GST is a destination-based consumption tax. This means the tax is collected by the state where the goods or services are consumed, rather than where they were manufactured.

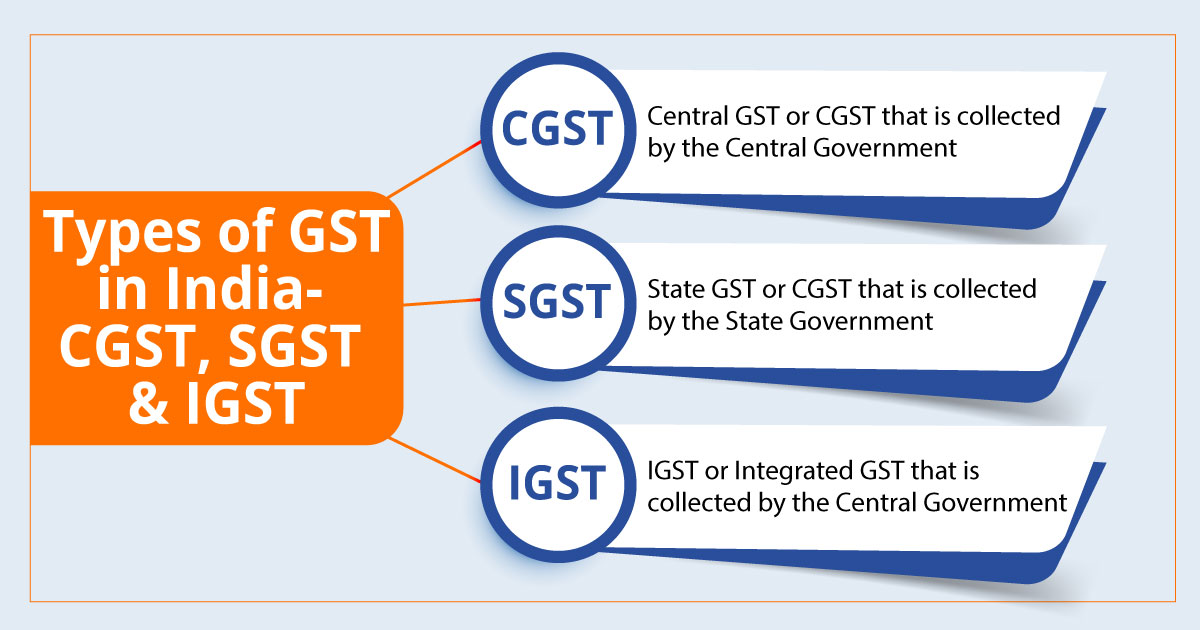

CGST, SGST, and IGST Explained

The Indian GST model is “dual,” meaning both the Union and State governments levy it simultaneously. This is broken down into three main categories:

- Central GST (CGST): Collected by the Central Government on an intra-state sale (e.g., a transaction within Maharashtra).

- State GST (SGST): Collected by the State Government on an intra-state sale.

- Integrated GST (IGST): Collected by the Central Government for inter-state transactions and imports. The IGST is then shared between the Centre and the destination state.

For a business owner or a financial planner, distinguishing between these is vital for accurate bookkeeping. An error in categorizing a transaction as intra-state versus inter-state can lead to compliance hurdles and temporary cash flow disruptions.

The Five-Tier Tax Structure

India does not use a single GST rate. Instead, it employs a multi-tiered structure designed to ensure that essential goods remain affordable while luxury items contribute more to the national exchequer. These slabs are:

- 0% (Exempt): Essential items like fresh vegetables, milk, and bread.

- 5%: Common use items like sugar, spices, and life-saving drugs.

- 12% & 18%: The standard rates covering the majority of goods and services, including processed foods, electronics, and professional services.

- 28%: Luxury and “sin” goods, such as tobacco, high-end cars, and carbonated drinks.

Understanding these slabs is crucial for budgeting. For instance, an investor looking into the real estate or automobile sector must factor in these varying rates to calculate the total cost of acquisition and potential Return on Investment (ROI).

3. Financial Implications for Businesses and Consumers

The introduction of GST fundamentally altered the way money moves through the Indian economy. It affected everything from corporate profit margins to the monthly household budget of a middle-class family.

Input Tax Credit (ITC): The Core of Financial Efficiency

For any business entity, the Input Tax Credit is the most powerful financial tool within the GST framework. ITC allows a seller to reduce the tax they have already paid on purchases from their final tax liability on sales. For example, if a furniture maker pays ₹1,000 in GST on timber and owes ₹1,500 in GST on the finished sofa, they only need to pay the remaining ₹500 to the government.

This system encourages businesses to source materials from GST-compliant suppliers. From a business finance strategy, this creates a self-policing loop where every link in the supply chain wants to ensure the previous link has paid their taxes, thereby reducing the “black money” or informal economy.

Impact on Pricing and Purchasing Power

For the individual consumer, the impact of GST is a mixed bag. Services—such as banking, telecommunications, and eating out—generally became more expensive as the tax rate shifted from 15% (Service Tax) to 18% (GST). However, many manufactured goods saw a price reduction because the removal of the cascading tax lowered the overall production cost.

In terms of personal finance management, GST has made indirect taxes more visible. Consumers can now see exactly how much they are contributing to the state and central coffers on every invoice. This transparency allows for better financial planning and a clearer understanding of where one’s money is going.

4. Compliance, Digital Transformation, and Financial Management

GST is not just a tax; it is a digital revolution. The entire system is managed through the Goods and Services Tax Network (GSTN), a sophisticated technological platform that handles registrations, returns, and payments.

The GST Council and Legislative Framework

The financial rules governing GST are not static. The GST Council, chaired by the Union Finance Minister and comprising representatives from all states, meets regularly to adjust tax rates and compliance rules. For those focused on business finance, staying updated with Council meetings is a prerequisite. A shift in a tax slab for a specific industry can overnight change the profitability of a company or the attractiveness of a stock.

Simplifying Filing for Small Businesses and Freelancers

Recognizing that the compliance burden can be heavy for small players, the government introduced the Composition Scheme. Small businesses with an annual turnover below a certain threshold (currently ₹1.5 crore for most states) can opt to pay a fixed, lower rate of tax on their turnover without the need for detailed ITC bookkeeping.

For freelancers and online income earners, the GST threshold (typically ₹20 lakh or ₹40 lakh depending on the state and type of business) provides a buffer. Once this threshold is crossed, obtaining a GSTIN (GST Identification Number) becomes mandatory. While this adds a layer of administrative work, it also professionalizes the business, making it easier to secure corporate contracts and business loans, as a GST-compliant history serves as a mark of financial credibility.

The Future of GST: Long-Term Financial Growth

As the GST regime matures, it continues to evolve toward a more seamless “seamless” experience. Concepts like E-way bills for the movement of goods and E-invoicing for real-time reporting are further reducing tax evasion and streamlining logistics.

From a broader economic perspective, GST has significantly increased the tax base of India. More businesses are now part of the formal economy than ever before. For the nation’s financial health, this means higher tax collections, which the government can reinvest into infrastructure and social sectors, theoretically spurring further economic growth.

For the savvy investor or business professional, GST is more than a line item on an invoice. It is a dynamic financial ecosystem. By mastering the mechanics of GST—from understanding the nuances of IGST to optimizing Input Tax Credits—individuals and corporations can protect their margins, ensure compliance, and leverage the transparency of the Indian market to build lasting wealth. As India continues to position itself as a global economic powerhouse, the GST remains the cornerstone of its financial integrity and fiscal modernization.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.