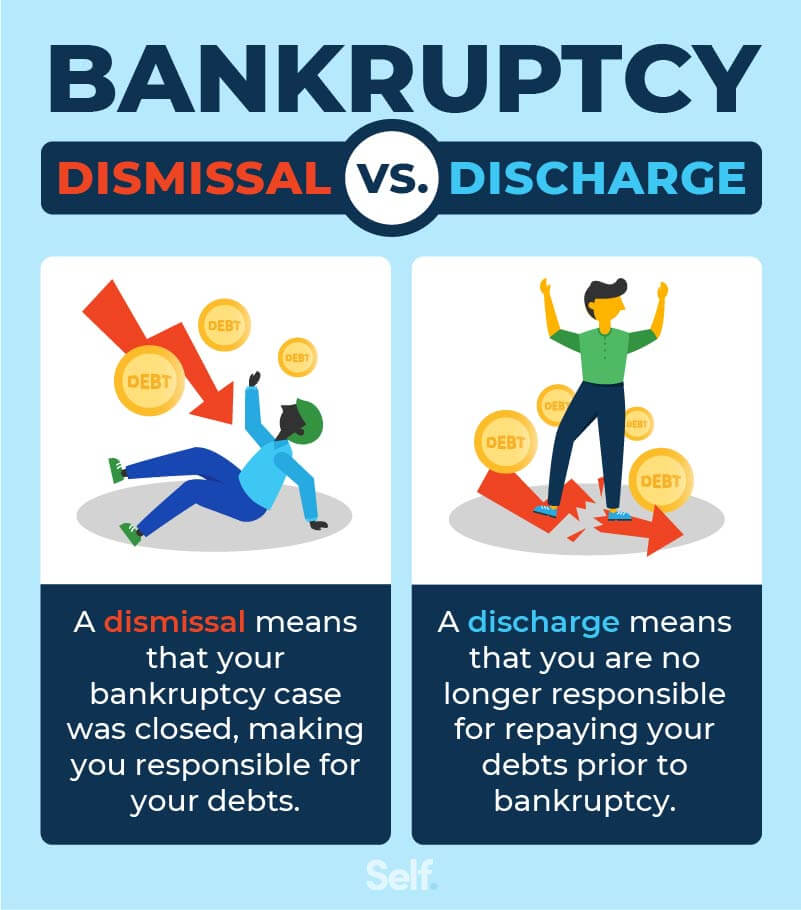

The concept of bankruptcy is often shrouded in stigma and misunderstanding, yet in the realm of personal and business finance, it serves as a critical mechanism for economic recovery. At its core, the primary goal of filing for bankruptcy is to obtain a “discharge.” A bankruptcy discharge releases the debtor from personal liability for certain specified types of debts. In other words, the debtor is no longer legally required to pay any debts that are discharged. Understanding what is—and is not—dischargeable is the most vital step in determining whether bankruptcy is a viable strategic tool for your financial rehabilitation.

1. The Mechanics of the Bankruptcy Discharge

Before diving into specific debt categories, it is essential to understand how the discharge works within the framework of the U.S. Bankruptcy Code. The discharge is a permanent order that prohibits creditors from taking any form of collection action against the debtor, including legal filings, wage garnishments, or even simple communication such as phone calls and letters.

The Timing of the Discharge

The timing of when a debt is discharged depends largely on the chapter under which the bankruptcy is filed. In a Chapter 7 bankruptcy, often referred to as “liquidation,” the discharge usually occurs relatively quickly—typically four to six months after the petition is filed. In contrast, Chapter 13 bankruptcy involves a reorganization of debt where the debtor commits to a three-to-five-year payment plan. In this scenario, the discharge is granted only after the debtor completes all payments required under the plan.

The Role of the Automatic Stay

The moment a bankruptcy petition is filed, an “automatic stay” goes into effect. This is a powerful financial tool that halts almost all collection activities immediately. While the stay is temporary, it provides the breathing room necessary for the court to determine which debts will ultimately be discharged and which must be paid.

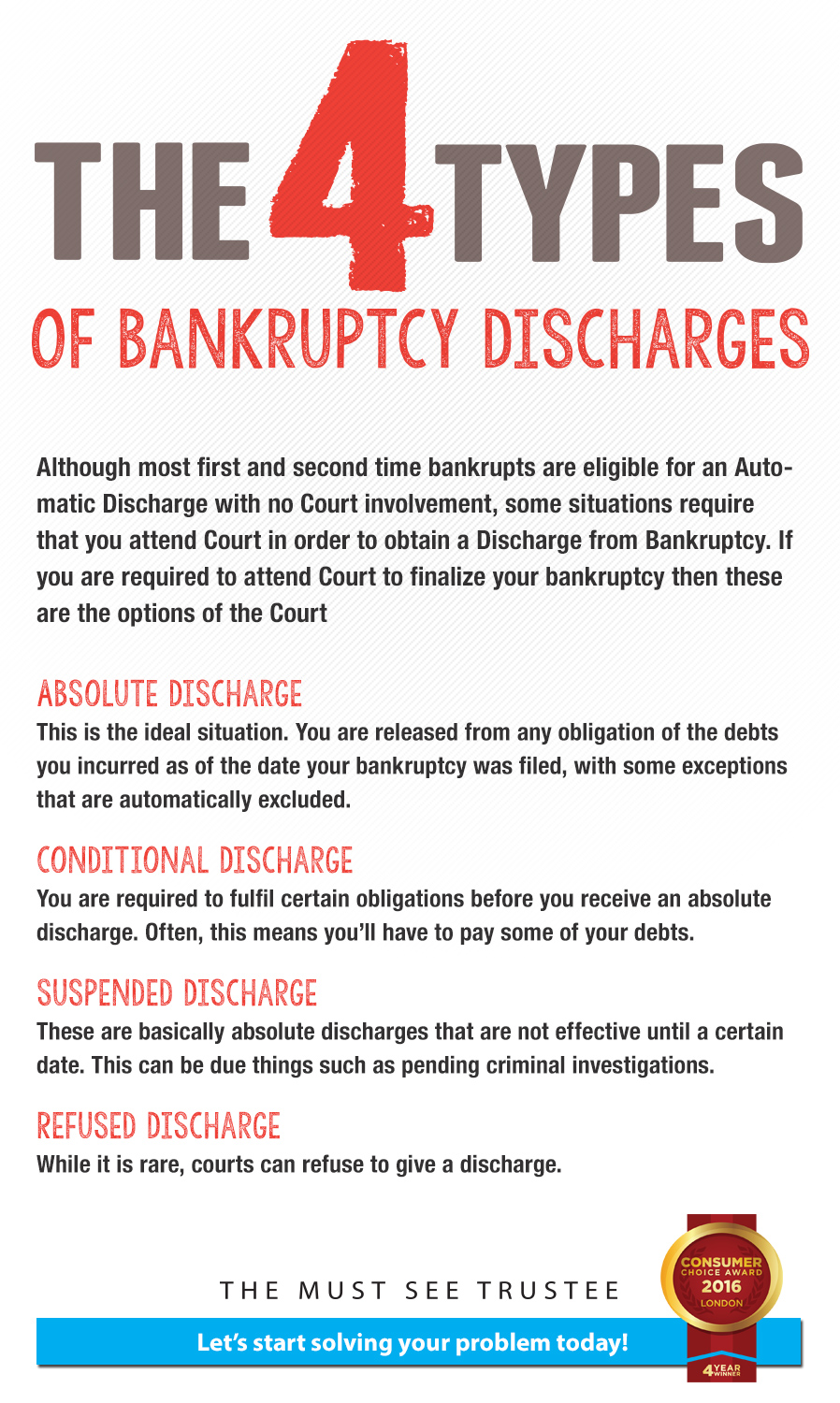

Limitations on the Right to Discharge

It is a common misconception that filing for bankruptcy guarantees a discharge of all debts. The court has the authority to deny a discharge if the debtor has engaged in fraudulent behavior, such as concealing assets, destroying financial records, or making false statements during the proceedings. Therefore, transparency is the cornerstone of a successful financial reset.

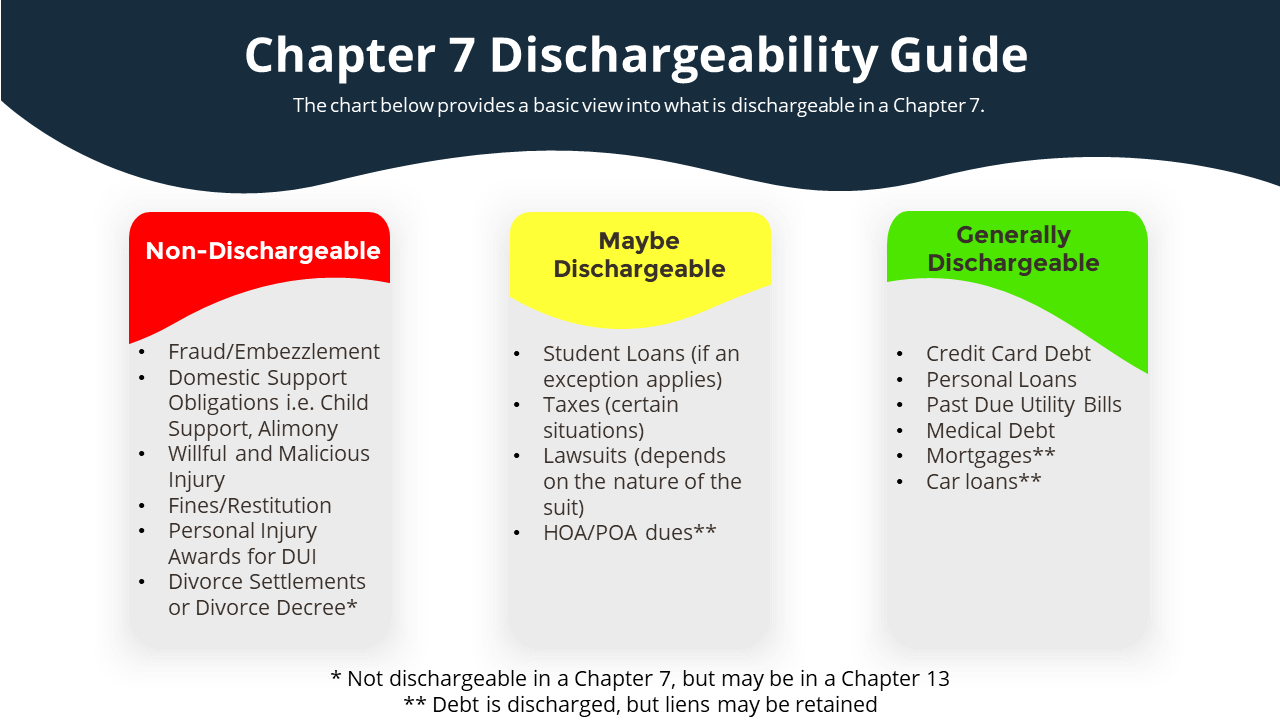

2. Commonly Dischargeable Debts: Creating Room for Recovery

The majority of people seeking bankruptcy relief are burdened by “unsecured” debts. These are liabilities that are not backed by collateral (like a house or a car). Most unsecured debts are fully dischargeable, providing the “fresh start” that is the hallmark of the bankruptcy system.

Credit Card Debt and Personal Loans

Credit card balances are perhaps the most common form of debt eliminated in bankruptcy. Whether the debt was incurred through daily living expenses or financial mismanagement, it is generally treated as a general unsecured claim and wiped clean. Similarly, unsecured personal loans from banks, credit unions, or online lenders are typically fully dischargeable.

Medical Bills

In the United States, medical debt is a leading cause of financial insolvency. Fortunately, medical bills are considered unsecured debts. Whether the debt is owed to a hospital, a private clinic, or a collection agency, it can be entirely discharged in both Chapter 7 and Chapter 13 filings. This allows individuals who have suffered from health crises to recover financially without the shadow of mounting healthcare costs.

Past-Due Utility Bills and Lease Terminations

Debts owed for past-due utilities (electricity, water, gas) are dischargeable, although utility companies may require a security deposit to continue service post-bankruptcy. Additionally, if you choose to “reject” a lease (such as an apartment lease or a car lease) during the bankruptcy process, any remaining balance or penalty for breaking the contract early is generally dischargeable.

Certain Civil Court Judgments

If a creditor has sued you and obtained a judgment for a breach of contract or an unpaid debt, that judgment is usually dischargeable. However, there are exceptions if the judgment resulted from “willful and malicious injury” or fraud, which are discussed in the following sections.

3. Non-Dischargeable Debts: What You Must Still Pay

While the bankruptcy code is designed to be forgiving, public policy dictates that certain obligations remain the debtor’s responsibility. These are known as non-dischargeable debts.

Domestic Support Obligations

Debts related to family law are strictly non-dischargeable. This includes child support and alimony (spousal maintenance). The legal system prioritizes the welfare of dependents over the debtor’s need for financial relief. These obligations must be paid in full, and bankruptcy will not stop the enforcement of these payments.

Student Loans and the “Undue Hardship” Bar

One of the most discussed topics in personal finance is the status of student loans in bankruptcy. Currently, student loans are non-dischargeable by default. To have them wiped out, a debtor must prove that repayment would impose an “undue hardship” on them and their dependents. This usually requires a separate legal action within the bankruptcy case known as an “adversary proceeding.” While the standard for undue hardship is historically high (often requiring proof of a permanent inability to pay), recent shifts in Department of Justice guidelines have begun to make this process slightly more accessible for certain debtors.

Tax Obligations

Not all tax debt is created equal. While some older income taxes can be discharged if they meet specific criteria (such as being at least three years old and filed on time), most recent tax debts are non-dischargeable. Furthermore, “trust fund taxes”—taxes withheld from employees’ paychecks by a business owner—can never be discharged.

Debts Incurred Through Fraud or Luxury Purchases

The bankruptcy court will not reward bad faith. Debts incurred through the use of false financial statements or fraudulent representations are non-dischargeable. Additionally, “luxury goods” purchased within 90 days of filing for bankruptcy (exceeding a certain dollar threshold) or cash advances taken shortly before filing are presumed to be non-dischargeable.

4. Strategic Financial Planning: Secured Debts and Liens

Understanding dischargeability is only half the battle; one must also account for secured debts. A discharge eliminates your personal liability for a debt, but it does not automatically remove a lien from a piece of property.

Mortgages and Auto Loans

If you have a mortgage or a car loan, the creditor has a “security interest” in the property. While the bankruptcy discharge might wipe out your personal obligation to pay the loan, it does not stop the bank from foreclosing on the house or repossessing the car if you stop making payments. For those looking to keep these assets, a Chapter 13 plan is often the better financial tool, as it allows you to catch up on arrears over time.

Reaffirmation Agreements

In Chapter 7, some debtors choose to sign a “reaffirmation agreement.” This is a legally binding contract filed with the court where the debtor waives the discharge of a specific debt (like a car loan) to keep the collateral. While this can help retain an essential asset, it carries the risk that you will remain personally liable for the debt even after the bankruptcy case is closed.

Lien Avoidance

In specific circumstances, the bankruptcy code allows debtors to “avoid” (remove) certain liens on personal property or household goods. This is a technical area of financial law that can turn a secured debt into an unsecured, dischargeable one, further enhancing the debtor’s net worth post-bankruptcy.

5. Life After Discharge: Rebuilding Your Financial Identity

The primary goal of identifying dischargeable debts is to position oneself for a successful post-bankruptcy life. Once the discharge order is signed, the focus shifts from debt management to wealth building and credit restoration.

The Impact on Credit Scores

While a bankruptcy filing remains on a credit report for seven to ten years, the actual impact on a credit score often stabilizes sooner than expected. By discharging a high volume of delinquent debt, a debtor’s debt-to-income ratio improves overnight. Many individuals find that they are able to obtain secured credit cards and even move toward traditional financing within two years of receiving their discharge.

Financial Literacy and Budgeting

The discharge provides a “clean slate,” but without a change in financial habits, the cycle of debt can repeat. Most bankruptcy filers are required to complete a financial management course. Utilizing the lessons from these courses—such as building an emergency fund and tracking discretionary spending—is essential to ensure that the “fresh start” leads to long-term prosperity.

Strategic Rebuilding

Post-discharge, the key to financial health is intentionality. This involves monitoring credit reports to ensure that all discharged debts are correctly reported as having a “$0 balance.” It also means being wary of “predatory” lenders who target recent bankruptcy filers with high-interest products. By focusing on low-utilization credit and consistent, on-time payments, the discharge becomes the foundation of a new, stable financial legacy.

In conclusion, knowing what is dischargeable in bankruptcy is the most powerful piece of information a person in financial distress can possess. It transforms bankruptcy from a scary, nebulous concept into a structured, predictable financial strategy. By identifying which liabilities can be shed and which must be managed, you can take the first definitive step toward reclaiming your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.