Building a home is often the most significant financial undertaking an individual or family will ever experience. Unlike purchasing an existing property, where the price tag is fixed and transparent from the outset, new construction is a dynamic financial journey. Understanding the average cost of building a house requires a deep dive into personal finance, capital allocation, and market economics. In the current economic climate, characterized by fluctuating material costs and shifting interest rates, a precise financial roadmap is essential for any prospective homeowner.

The national average to build a house typically ranges from $200,000 to $500,000, excluding the cost of land. However, these figures are merely a baseline. To truly grasp the financial commitment, one must analyze the interplay between hard costs, soft costs, and the external economic factors that drive them.

Breaking Down the Core Financial Components of Home Construction

When analyzing the budget for a new build, it is helpful to categorize expenses into distinct financial buckets. This allows for better cash flow management and helps identify where a budget is most likely to experience “scope creep.”

Land Acquisition and Preparation Costs

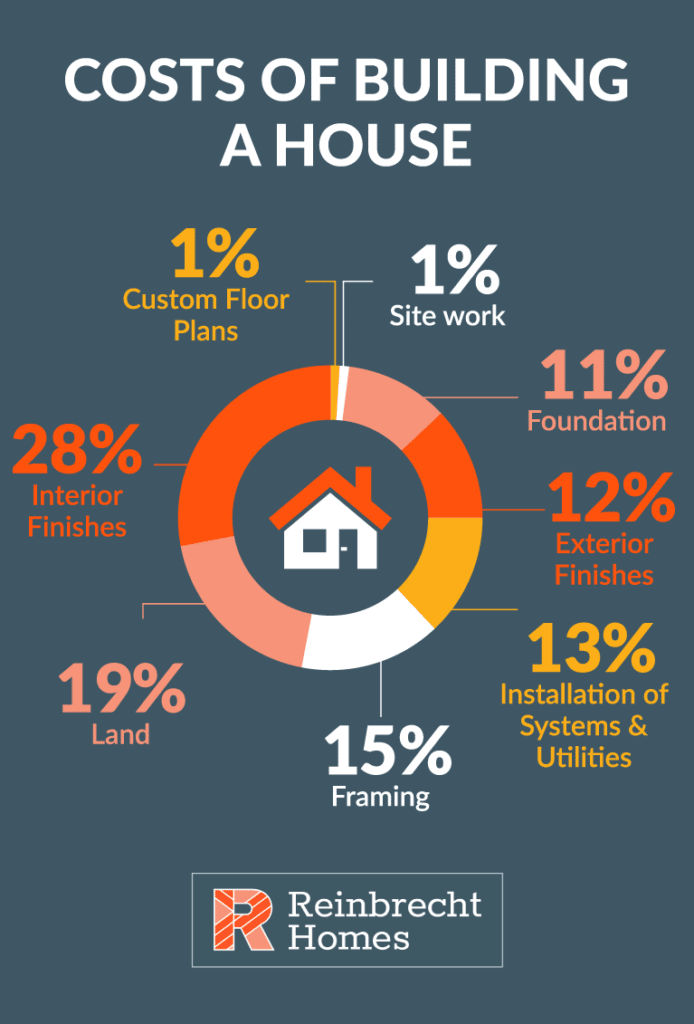

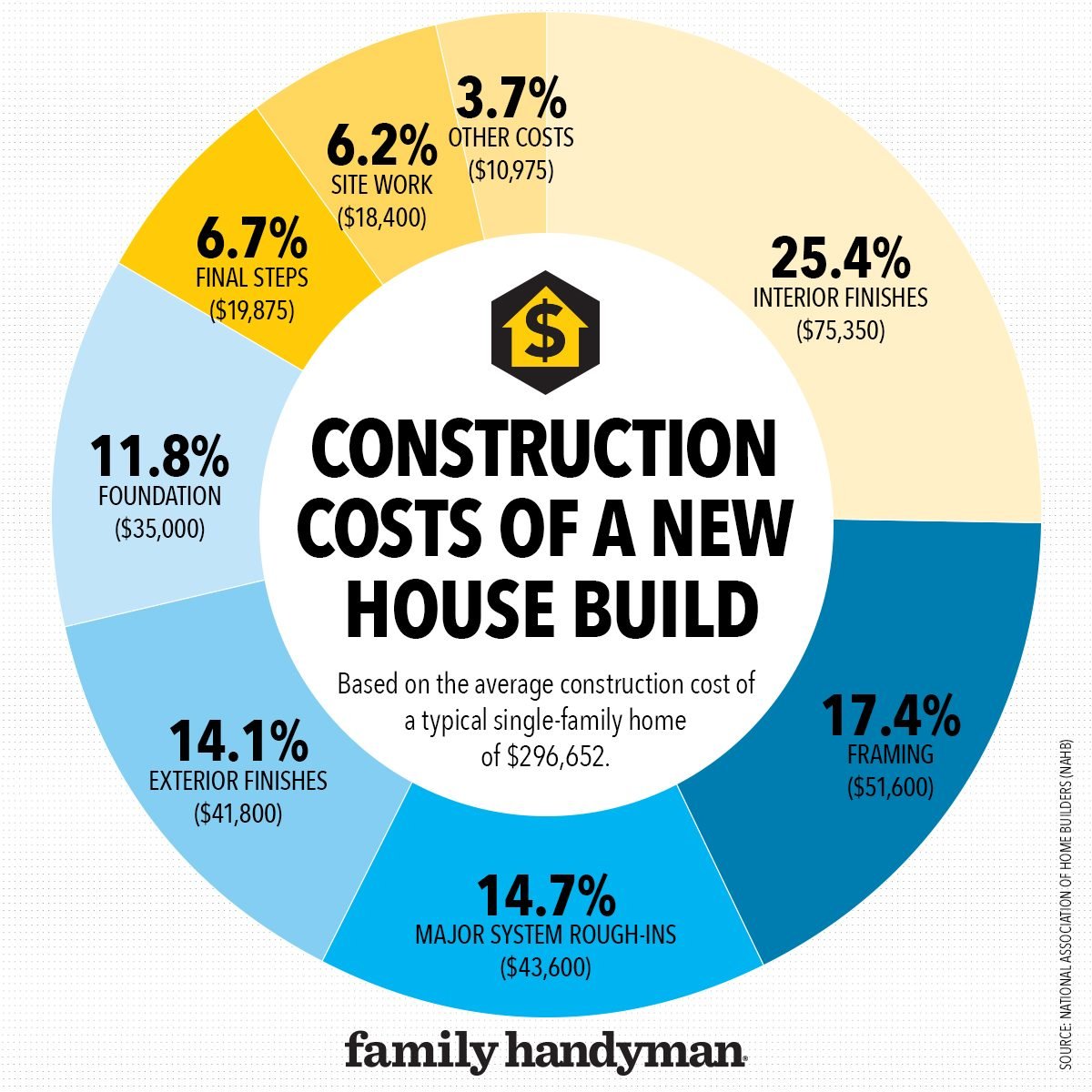

The first major capital outlay is the land itself. From a financial perspective, land is a non-depreciable asset, but its preparation is a significant “soft cost” that can fluctuate wildly. The purchase price of the lot is just the beginning; investors must account for surveying, clearing, grading, and connecting to public utilities (water, sewer, electricity) or installing private systems like septic tanks and wells. In some regions, land preparation can account for 10% to 15% of the total project budget.

Hard Costs vs. Soft Costs: Understanding the Distinction

In construction finance, “hard costs” refer to the tangible assets and labor required to physically erect the structure. This includes the foundation, framing, roofing, plumbing, and interior finishes. These are the costs most susceptible to inflation and supply chain disruptions.

“Soft costs,” on the other hand, are the intangible expenses necessary to move the project forward. These include architectural fees, engineering reports, building permits, legal fees, and construction insurance. While often overlooked, soft costs can easily consume 20% of a total budget. For a $400,000 home, failing to account for $80,000 in soft costs can lead to a catastrophic funding gap mid-project.

Labor and Material Volatility in the Current Economy

From a personal finance standpoint, the volatility of raw materials (lumber, steel, copper, and concrete) has made fixed-price contracts rarer and more expensive. Labor shortages in the skilled trades have also driven up the cost of human capital. When calculating the average cost, one must realize that labor usually accounts for roughly 30% to 40% of the total build cost. Managing these variables requires a robust contingency fund—a pillar of sound financial planning in construction.

Geographic and Structural Variables Influencing Your Investment

The “average” cost is a statistical abstraction that varies wildly depending on where you build and what you build. Real estate is inherently local, and the financial implications of location cannot be overstated.

The Impact of Location on Price per Square Foot

In the world of real estate finance, the price per square foot is the standard metric for comparison. In low-cost-of-living areas, you might see construction costs as low as $100 to $150 per square foot. In high-demand metropolitan hubs or coastal regions, that number can easily soar to $400 or $500 per square foot. This discrepancy is driven by local labor rates, the stringency of regional building codes, and the cost of transporting materials to the site. A homeowner must evaluate whether the local market’s “ceiling” supports the investment; building a $600,000 house in a neighborhood where the average home value is $300,000 is a poor financial move that results in immediate negative equity.

Architectural Complexity and Customization Premiums

The shape and design of a house have a direct impact on the bottom line. From a cost-efficiency perspective, a two-story square or rectangular house is the most economical to build because it minimizes the foundation and roof area relative to the total living space.

Customization is where many budgets collapse. High-end finishes, such as quartz countertops, custom cabinetry, and professional-grade appliances, represent a “lifestyle premium” rather than a fundamental structural necessity. From a wealth-building perspective, it is often wiser to invest in structural integrity and energy efficiency—which offer long-term savings—rather than trend-based aesthetic upgrades that may depreciate or lose appeal over time.

Financing the Build: Loans, Interest, and Cash Flow Management

Unless you are self-funding with liquid capital, the strategy you use to finance your build will significantly impact the total “cost of ownership” over time.

Comparing Construction Loans to Traditional Mortgages

Financing a new build is more complex than a standard 30-year fixed mortgage. Most builders utilize a “Construction-to-Permanent” loan. During the building phase, you typically pay only the interest on the money that has been “drawn” or paid out to the builder. Once the home is complete and receives a Certificate of Occupancy, the loan converts into a traditional mortgage.

The financial risk here lies in the interest rate environment. If rates rise during the 12 to 18 months it takes to build, your eventual mortgage payment could be significantly higher than originally projected. Some financial products allow you to “lock in” a rate at the start of construction, providing a hedge against market volatility.

Planning for the “Hidden” Costs and Contingency Funds

A cardinal rule in business finance is to expect the unexpected. In home construction, a 10% to 20% contingency fund is non-negotiable. Unexpected soil issues, weather delays that extend labor hours, or price hikes in materials can quickly erode a tight budget.

Furthermore, many homeowners forget the “post-build” financial requirements. Landscaping, window treatments, and furniture are rarely included in the builder’s quote. If your construction budget is $500,000, you should realistically have access to an additional $50,000 to $75,000 to ensure the property is move-in ready and functional without resorting to high-interest credit card debt.

Long-term Financial Outlook: ROI and Resale Value

When calculating the average cost of building a house, one must also consider the “return on investment” (ROI). Building a home is not just an expense; it is the acquisition of a primary asset.

Assessing the Value of Energy-Efficient Upgrades

Modern building science allows for investments that significantly lower the total cost of ownership. High-performance insulation, solar readiness, and high-efficiency HVAC systems have a higher upfront cost but offer a measurable internal rate of return (IRR) through reduced utility bills. From a financial planning perspective, these upgrades can be viewed as an annuity—upfront capital spent today to guarantee lower monthly outflows for decades. Furthermore, as “green” building standards become the norm, energy-efficient homes tend to hold their value better and sell faster in the secondary market.

Market Trends: New Construction vs. Existing Home Purchases

Finally, an investor must weigh the cost of building against the cost of buying an existing home. Historically, building a new home was more expensive than buying an old one. However, in markets with low inventory, the “new construction premium” has narrowed.

A new home offers the financial advantage of having no “deferred maintenance.” When you buy a 20-year-old house, you must budget for the imminent replacement of the roof, the furnace, and the water heater. With a new build, these major capital expenditures are delayed by two decades. Additionally, new homes are built to current codes, often resulting in lower insurance premiums—another vital factor in the long-term personal finance equation.

Conclusion

The average cost of building a house is a multifaceted figure that depends on land costs, material prices, geographic location, and financing structures. By approaching the project with a rigorous financial mindset—separating hard costs from soft costs, maintaining a healthy contingency fund, and focusing on long-term ROI—homeowners can navigate the complexities of construction without jeopardizing their financial future. While the process is capital-intensive, a well-planned build serves as a cornerstone of personal wealth, providing both a residence and a high-value asset in an ever-evolving real estate market.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.