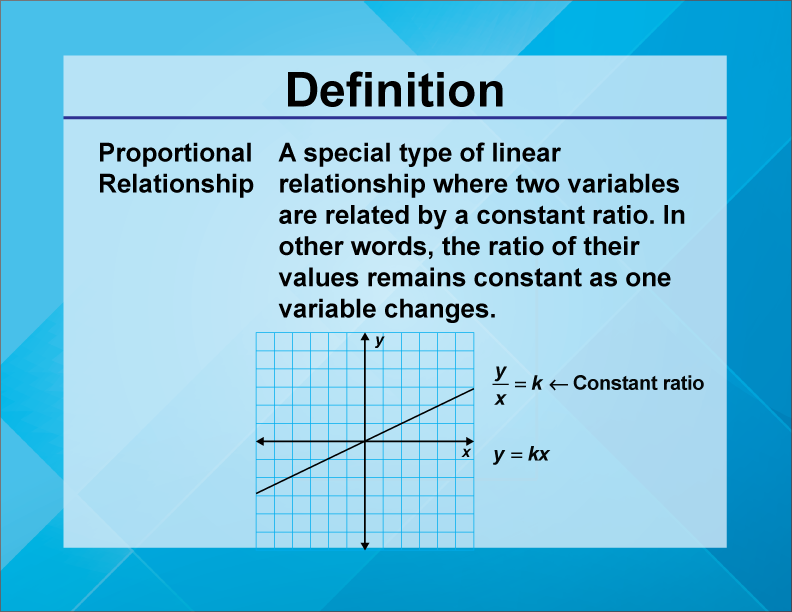

In the world of mathematics, a proportional relationship is defined as a relationship between two quantities where the ratio of one quantity to the other is constant. While this may sound like a dry concept from a middle-school textbook, in the realm of finance, understanding proportional relationships is the foundational difference between those who struggle to balance a checkbook and those who build generational wealth.

In money management, proportionality governs everything from how we budget our monthly income to how we assess the risk of a high-growth stock portfolio. It is the invisible thread that connects our inputs—time, capital, and labor—to our outputs—dividends, interest, and equity. To master your finances is, in many ways, to master the ratios that define them.

Understanding the Mathematical Core of Financial Proportionality

Before diving into complex investment strategies, one must grasp how proportionality functions within an economic framework. At its simplest, a proportional relationship in finance suggests that if you change one variable, another variable changes at a consistent rate.

Defining Proportionality in an Economic Context

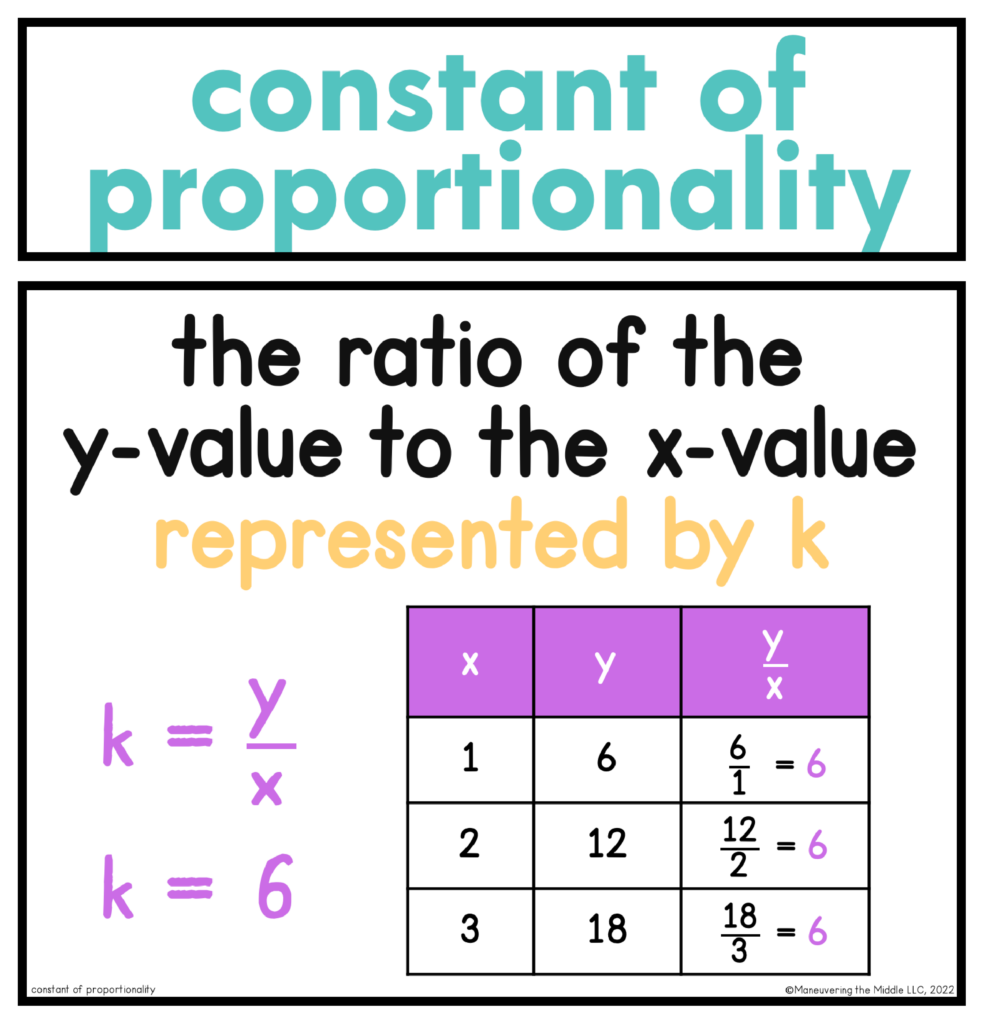

In finance, we often look for “direct proportionality.” For instance, if you earn a fixed commission of 5% on every sale, your income is directly proportional to your sales volume. If you sell $1,000 worth of goods, you earn $50; if you sell $10,000, you earn $500. The constant of proportionality here is 0.05.

However, the professional investor also looks for “inverse proportionality.” A classic example is the relationship between bond prices and interest rates. Generally, when interest rates rise, bond prices fall. Understanding these inverse relationships allows a financier to hedge against market volatility. Without a grasp of these ratios, an individual is merely guessing, rather than calculating, their financial future.

Linear Growth vs. Exponential Scalability

Most people live their lives in a linear proportional relationship: they trade one hour of time for a set amount of dollars. This is $Y = kX$, where $Y$ is earnings, $k$ is the hourly rate, and $X$ is the time worked. The limitation here is that time is a finite resource.

To achieve true financial freedom, one must move toward relationships that are disproportional in favor of the earner. This is where “scalability” enters the conversation. In a scalable business model—such as software sales or digital products—the cost of producing an extra unit is near zero, while the revenue remains constant. This breaks the linear proportional bond between labor and income, allowing for exponential wealth accumulation.

Proportional Relationships in Personal Finance and Budgeting

Effective money management is less about the total amount of money you earn and more about the proportions in which you distribute that money. A high earner who spends 100% of their income is mathematically closer to poverty than a modest earner who saves 20% of their income.

The 50/30/20 Rule: Proportionality in Cash Flow

One of the most enduring frameworks in personal finance is the 50/30/20 rule. This is a proportional guideline that suggests allocating 50% of your net income to “needs” (housing, utilities, groceries), 30% to “wants” (entertainment, dining out), and 20% to “financial goals” (savings, debt repayment, investments).

The beauty of this rule lies in its proportionality. As your income increases, your lifestyle can expand, but only in proportion to your savings. If you receive a $1,000 raise, the rule dictates that $200 of that must go toward your future. By maintaining these constant ratios, you ensure that “lifestyle creep” does not outpace your ability to build a safety net.

Debt-to-Income Ratios: The Scale of Creditworthiness

From the perspective of a lender, proportional relationships are the primary tools used to assess risk. The Debt-to-Income (DTI) ratio is a calculation of your total monthly debt payments divided by your gross monthly income.

Lenders typically look for a DTI of 36% or less. This proportional limit exists because historical data shows that when debt consumes a higher percentage of income, the likelihood of default rises exponentially. For the consumer, keeping this relationship in check is vital for maintaining access to low-interest capital, which is a key lever in wealth building.

![]()

Investing and the Proportionality of Risk and Reward

In the investment world, the most famous proportional relationship is the “Risk-Reward Tradeoff.” This principle states that the potential return on an investment rises with an increase in risk. To seek higher returns, one must be willing to accept a higher probability of loss.

Modern Portfolio Theory: Assets in Proportion

Modern Portfolio Theory (MPT) is a framework for assembling a portfolio of assets such that the expected return is maximized for a given level of risk. The core of MPT is asset allocation—the proportional distribution of your money across different categories like stocks, bonds, real estate, and cash.

An investor might decide on a 70/30 split between equities and fixed income. The goal is to maintain this proportion regardless of market swings. If the stock market performs exceptionally well, the equities portion might grow to represent 80% of the portfolio. A disciplined investor will “rebalance,” selling off the excess stocks to buy more bonds, returning the portfolio to its original 70/30 proportion. This forced discipline ensures that the investor “buys low and sells high” systematically.

Risk Management: Why Losses Aren’t Always Proportional to Gains

It is a dangerous financial misconception to assume that a 10% loss and a 10% gain cancel each other out. In reality, the relationship is asymmetrical. If you have $100 and lose 10%, you have $90. To get back to $100, you now need a gain of 11.1%. If you lose 50%, you need a 100% gain just to break even.

Understanding this disproportionality is why professional money managers focus heavily on “downside protection.” By limiting the proportion of the portfolio at risk of significant loss, they ensure that the mathematical path back to profitability remains manageable.

Proportional Scaling in Business and Online Income

For entrepreneurs and side-hustlers, understanding the proportional relationship between expenses and revenue is the key to sustainability. This is often analyzed through the lens of operating leverage.

Variable vs. Fixed Costs: Maintaining Margin Proportions

In business, costs are generally divided into fixed costs (rent, salaries) and variable costs (raw materials, shipping). A healthy business strives for a proportional relationship where “Contribution Margin” remains high.

If it costs $5 to produce a widget that sells for $20, your margin is 75%. As you scale, you want to ensure that your variable costs do not grow faster than your revenue. If a business doubles its sales but its costs triple, the proportional relationship has broken down, leading to what is known as “diseconomies of scale.” Financial success in business requires keeping these ratios lean as the volume of transactions grows.

Scalability: When Effort is Disproportional to Output

The “Holy Grail” of modern finance, particularly in the tech-enabled side hustle and creator economy, is finding a disproportional relationship between input and output. In a traditional service business (like consulting), your income is strictly proportional to the hours you bill.

In contrast, creating a digital course or writing a book involves a high initial input of effort, but the subsequent sales are disproportional to any additional work. Once the asset is created, you can sell 1,000 copies as easily as 10. This creates a “long-tail” financial effect where the ratio of profit to effort increases over time, leading to passive income streams that are the hallmark of modern wealth.

Conclusion: Leveraging Ratios for Long-Term Financial Health

Proportional relationships are far more than just mathematical abstractions; they are the governing laws of the financial universe. By viewing your money through the lens of ratios and proportions, you shift from a reactive mindset to a strategic one.

Whether you are balancing your monthly budget using the 50/30/20 rule, rebalancing an investment portfolio to maintain a specific risk profile, or seeking out scalable business models that offer disproportional returns on your time, the goal remains the same: balance.

True financial mastery requires the wisdom to know which proportions to keep constant and the courage to break those that limit your growth. As you move forward, ask yourself: Is the relationship between my effort and my income linear or exponential? Is my debt in healthy proportion to my earnings? By answering these questions, you take control of the mathematical engine that drives your financial destiny.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.