In the landscape of personal finance and career development, a professional degree represents one of the most significant financial commitments an individual can make. Unlike a general undergraduate degree, which provides a broad foundation of knowledge, a professional degree is a specialized credential designed to prepare students for specific high-stakes careers. From a financial perspective, these degrees are often viewed as “human capital investments.” They require a substantial upfront cost—both in terms of tuition and opportunity cost—with the expectation of generating a premium return in the form of elevated lifetime earnings, job security, and access to exclusive labor markets.

Understanding what professional degrees are requires looking past the curriculum and focusing on the economic impact they have on an individual’s financial portfolio. Whether you are considering a career in law, medicine, business, or architecture, a professional degree is a strategic asset that must be managed with the same rigor as a real estate investment or a stock portfolio.

Defining the Asset Class: Understanding Professional Degrees as Financial Drivers

At its core, a professional degree is a post-graduate qualification that satisfies the legal or regulatory requirements to practice in a specific field. In the world of business and finance, these degrees act as “gatekeeper” credentials. Without them, the highest-earning tiers of certain industries remain inaccessible.

The Distinction Between Academic and Professional Degrees

It is essential to distinguish between a research-based PhD and a professional degree like a Juris Doctor (JD) or a Master of Business Administration (MBA). While a PhD is focused on contributing new knowledge to a field, a professional degree is focused on the application of knowledge. For the financially-minded individual, this distinction is crucial: professional degrees are specifically engineered for the marketplace. They are vocational by design, meaning their primary value is derived from their ability to increase the holder’s market rate.

Common High-Yield Professional Degrees

When we categorize professional degrees by their financial impact, several “high-yield” options emerge. These include:

- Medical Degrees (MD/DO): High entry cost, but offering some of the highest guaranteed salary floors in the economy.

- Legal Degrees (JD): Offers a wide variance in ROI, with “Big Law” positions offering rapid debt repayment.

- Business Degrees (MBA): A versatile degree often used to pivot into high-compensation sectors like private equity or management consulting.

- Pharmacy (PharmD) and Dentistry (DDS): Specialized healthcare roles that offer stable, high-income trajectories.

Calculating the Return on Investment (ROI)

Before committing to a professional degree, a rigorous financial analysis is required. The “sticker price” of tuition is rarely the true cost. To calculate the actual ROI, one must factor in the cost of debt, the years of lost income during study, and the projected “salary bump” post-graduation.

The Debt-to-Income Ratio (DTI)

A common rule of thumb in personal finance is that your total student debt should not exceed your expected first-year salary. For many professional degrees, this ratio is stretched to its limit. For example, a medical student may graduate with $250,000 in debt but anticipate a salary of $300,000 within five years. Conversely, pursuing a professional degree in a field with a lower salary ceiling can lead to a “debt trap.” Calculating the DTI helps in determining if the degree is a sound financial vehicle or a liability.

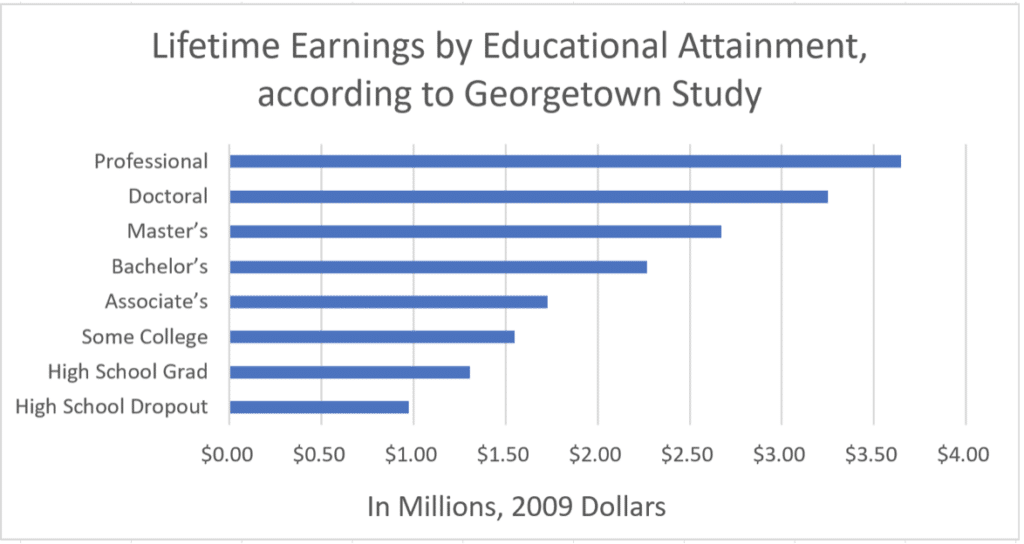

Lifetime Earning Potential and Compound Interest

The true power of a professional degree lies in the “slope” of the career earnings curve. A professional degree typically allows an individual to start at a higher pay grade and receive more significant percentage raises over time. When these increased earnings are invested early into retirement accounts or brokerage portfolios, the compound interest effect is magnified. A professional degree holder who earns $50,000 more per year than a peer and invests half of that surplus can end their career with a net worth millions of dollars higher, even after accounting for the initial cost of the degree.

Strategic Financial Planning for Advanced Education

Because the costs are so high, the method of financing a professional degree can be just as important as the degree itself. Smart financial planning during the education phase can save tens of thousands of dollars in interest and lost opportunity.

Navigating Scholarships, Grants, and Fellowships

While undergraduate scholarships are common, professional school funding is often more competitive but more lucrative. Many corporations offer fellowships for MBAs in exchange for post-graduation service. In the medical field, programs like the National Health Service Corps (NHSC) offer full tuition reimbursement for those willing to work in underserved areas. From a wealth-building perspective, these programs are “pure profit,” as they remove the burden of interest-bearing debt.

Employer Sponsorship as a Capital Strategy

Many professionals in the corporate world pursue an MBA or a specialized Master’s while working. High-tier firms often have tuition reimbursement programs where they cover 50% to 100% of the cost. This is the gold standard for ROI; the individual gains the asset (the degree) while the employer pays the capital expenditure. This strategy eliminates the “opportunity cost” of leaving the workforce, allowing the professional to continue earning a salary and contributing to a 401(k) while upgrading their credentials.

Private vs. Federal Loan Structures

For those who must borrow, understanding the mechanics of debt is vital. Federal loans often offer Income-Driven Repayment (IDR) plans and Public Service Loan Forgiveness (PSLF), which can be a financial lifesaver for those entering lower-paying public sector professional roles. However, for those entering high-earning private sectors, refinancing with private lenders post-graduation to secure a lower interest rate is often the most efficient way to maximize net cash flow.

Navigating the Modern Job Market: Degrees as Career Leverage

A professional degree does more than just teach skills; it functions as a “signaling” mechanism in the labor market. In economic terms, it reduces “information asymmetry” between the employer and the candidate.

Credentialism and Market Demand

In a saturated job market, “credential inflation” is a real phenomenon. Roles that once required only a Bachelor’s degree now often favor those with professional Master’s degrees. Having the right professional degree provides “career insurance.” During economic downturns, data consistently shows that individuals with advanced professional degrees have lower unemployment rates and higher wage stability. This resilience is a critical component of a robust financial plan.

Diversifying Income Post-Degree

A professional degree also opens doors to secondary income streams that are not available to the general public. A JD can provide legal consulting on the side; an MD can engage in medical writing or expert witness testimony; a CPA can manage a private tax practice during peak seasons. These “side hustles” are high-margin because they leverage the specialized authority granted by the degree, allowing the professional to bill at significantly higher hourly rates than they could with a general skill set.

The Financial Risks and Opportunity Costs

No investment is without risk. For every success story, there are individuals who find themselves “over-educated and under-capitalized.”

The Sunk Cost Fallacy in Education

One of the greatest financial risks is the “sunk cost fallacy”—the idea that because you have already spent two years and $100,000 on a professional degree, you must finish it even if the market for that role has collapsed. It is vital to keep an eye on industry trends. For example, if AI begins to automate entry-level legal research, the ROI for a JD from a lower-tier school may plummet. Staying agile and being willing to pivot your financial strategy is essential.

The Time-Value of Money (TVM)

The most overlooked cost of a professional degree is the time-value of money. If a student spends four years in professional school and three years in residency, that is seven years of missed contributions to a Roth IRA or 401(k). By the time they start earning a high salary, they are “behind” on the compounding curve. To mitigate this, professional degree holders must be aggressive savers in their early 30s to catch up with peers who entered the workforce at age 22.

In conclusion, professional degrees are powerful financial instruments that can catapult an individual into the upper echelons of wealth and career stability. However, they are not a guaranteed ticket to prosperity. They require a clear-eyed analysis of costs, a strategic approach to debt, and a long-term view of market demand. By treating a professional degree as a high-stakes business investment, you can ensure that the “letters after your name” translate into “dollars in your bank account.”

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.